유럽의 경상용차 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Europe Light Commercial Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1693626

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

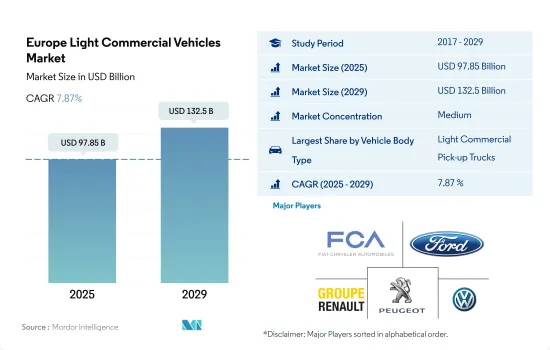

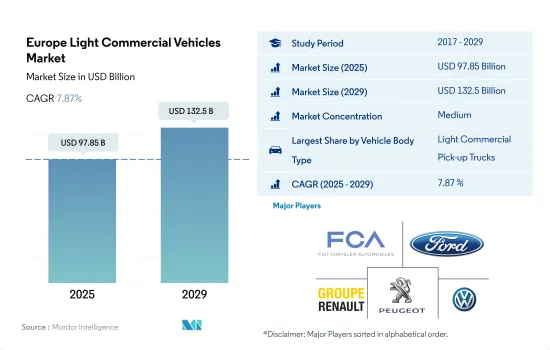

유럽의 경상용차(LCV) 시장 규모는 2025년에 978억 5,000만 달러로 추정되고, 2029년에는 1,325억 달러에 이를 것으로 예측되며, 예측 기간(2025-2029년)의 CAGR은 7.87%를 나타낼 것으로 예측됩니다.

인프라 투자와 전자상거래 급증으로 번창하는 유럽 LCV 시장, 도시화와 친환경 노력에 힘입어 지속적인 성장이 예상됩니다.

2022년 유럽의 경상용차(LCV) 시장은 6.2%의 견고한 판매량 성장을 기록했습니다. 이러한 긍정적인 모멘텀은 2023년에도 3.5%의 성장이 예상되는 가운데 지속될 것으로 전망됩니다.

2017년부터 2023년까지 유럽의 LCV 시장은 38%나 급증하는 등 괄목할 만한 상승세를 보였습니다. 이러한 급증은 전자상거래 붐으로 인해 배송 네트워크가 확장되고 밴 판매가 증가하면서 촉진되었습니다. 또한 소매업, 건설업, 서비스업 등의 분야에서 발생한 교체 수요도 중요한 역할을 했습니다. 2020년에는 팬데믹으로 인한 혼란으로 시장이 위축되었지만, 디지털 도입이 가속화되면서 빠르게 반등했습니다.

유럽의 LCV 시장은 2024년부터 2030년까지 3.1%의 연평균 성장률을 기록할 것으로 전망됩니다. 이러한 성장 궤적은 지속적인 인프라 개발, 라스트마일 배송 네트워크의 지속적인 확장, 도시화 추세의 증가에 의해 촉진될 것입니다. 이러한 요인들은 서비스, 음식 배달, 건설 부문에서 LCV에 대한 수요 증가와 함께 유망한 전망을 제시합니다. 그러나 배기가스 배출과 도시 접근성에 대한 규제가 강화되면서 대체 연료 밴의 채택이 증가할 수 있기 때문에 시장은 역풍에 직면할 수도 있습니다.

유럽의 경상용차 시장의 국가별 동향은 이 지역의 배출 가스 삭감과 효율 향상의 추진을 부각하고 있습니다.

주요 유럽 시장은 각기 다른 경제 환경을 반영하듯 2022년에 다양한 LCV 판매량을 기록했습니다. 독일은 경제 회복세에 힘입어 6.3%의 견고한 성장세를 보였습니다. 반면, 영국은 경제 불확실성에 직면하여 LCV 판매량이 2.1% 감소했습니다. 프랑스, 이탈리아, 스페인은 거시경제의 어려움과 함께 3-5%의 감소를 경험했습니다.

2017년부터 2021년까지 독일, 프랑스, 이탈리아, 스페인, 폴란드 등 유럽의 주요 LCV 시장은 팬데믹 이전 약 3-5%의 연평균 성장률을 기록하며 견조한 성장세를 보였습니다. 이러한 성장은 특히 건설, 배송, 서비스 등의 산업에서 견고한 경제 활동에 힘입어 이루어졌습니다.

유럽 LCV 시장은 2023년부터 2029년까지 연평균 3-4% 성장할 것으로 예상되는 등 꾸준한 성장 궤도에 오를 것으로 전망됩니다. 인프라 투자, 라스트마일 배송 네트워크의 부상, 지속적인 경제 회복과 같은 요인이 수요를 강화할 것으로 예상됩니다. 그러나 높은 인플레이션, 에너지 비용, 정치적 불확실성 등의 요인으로 인한 위험도 존재합니다.

유럽의 경상용차 시장 동향

환경 문제, 정부 지원, 탈탄소화 목표가 유럽 전기자동차 수요와 판매를 촉진합니다.

유럽 국가의 전기차 수요와 판매량은 지난 몇 년 동안 크게 증가했습니다. 독일은 2021년 대비 2022년 전기차 판매량이 22% 증가했으며, 영국은 2021년 대비 2022년 18.40%의 증가율을 보였습니다. 환경에 대한 관심 증가, 엄격한 정부 규범, 연비, 낮은 유지비, 탄소 배출 없음, 정부의 보조금 등 전기자동차의 장점은 유럽 국가에서 전기자동차가 성장하는 데 기여하는 요인 중 일부입니다.

유럽 국가에서는 전기 상용차, 특히 경트럭에 대한 수요가 점차 증가하고 있습니다. 또한 여러 국가의 정부도 전기자동차 도입을 지원하고 있습니다. 2021년 11월, 영국 정부는 2040년까지 모든 대형 차량을 무공해 차량으로 만들겠다는 공약을 발표했습니다. 이러한 요인으로 인해 영국 내 전기 상용차 판매량은 2021년 대비 2022년에 23.17% 증가했으며, 여러 국가에서 유사한 정책이 시행되면서 유럽 전역에서 전기 상용차에 대한 수요가 증가하고 있습니다.

유럽 국가들의 차량 전기화는 향후 몇 년 동안 엄청난 성장을 이룰 것으로 예상됩니다. 탈탄소화를 위한 각국 정부의 노력이 유럽 내 전기 상용차 시장을 견인할 것으로 예상됩니다. 예를 들어, 2022년 1월 독일 교통부 장관은 2030년까지 1,500만 대의 전기차를 도로에 배치하겠다는 목표를 발표했습니다.

유럽의 경상용차 산업 개요

유럽의 경상용차 시장은 적당히 통합되어 있으며 상위 5개 기업이 62.47%를 점유하고 있습니다. 이 시장의 주요 업체는 Fiat Chrysler Automobiles N.V, Ford Motor Company, Groupe Renault, Peugeot S.A. Volkswagen AG(알파벳 순 정렬)입니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

인구

1인당 GDP

차량 구매를 위한 소비자 지출(CVP)

인플레이션율

자동차 대출 금리

공유 차량 서비스

전기화의 영향

EV 충전소

배터리 팩 가격

Xev 신모델 발표

연료 가격

OEM 생산 통계

규제 프레임워크

밸류체인과 유통채널 분석

제5장 시장 세분화

차량 부문

상용차

경 상용 픽업 트럭

경 상용 밴

추진 부문

하이브리드 자동차 및 전기자동차

연료 카테고리별

BEV

FCEV

HEV

PHEV

ICE

천연가스

디젤

가솔린

LPG

국가명

오스트리아

벨기에

체코 공화국

덴마크

에스토니아

프랑스

독일

아일랜드

이탈리아

라트비아

리투아니아

노르웨이

폴란드

러시아

스페인

스웨덴

영국

기타 유럽

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

Fiat Chrysler Automobiles NV

Ford Motor Company

Groupe Renault

Mercedes-Benz

Peugeot SA

Toyota Motor Corporation

Volkswagen AG

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

출처 및 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

HBR

영문 목차

영문목차

The Europe Light Commercial Vehicles Market size is estimated at 97.85 billion USD in 2025, and is expected to reach 132.5 billion USD by 2029, growing at a CAGR of 7.87% during the forecast period (2025-2029).

The European LCV market thrives on infrastructure investments and e-commerce surge, with continued growth expected amid urbanization and green initiatives

In 2022, the light commercial vehicle (LCV) market in Europe witnessed a robust 6.2% growth in sales volume. This positive momentum is expected to carry forward, with a projected growth of 3.5% in 2023. This growth is primarily fueled by heightened infrastructure investments and the surging tide of e-commerce. The EU's focus on transportation and energy projects has stimulated demand for LCVs, especially from the construction and utilities sectors. The expansion of last-mile delivery networks, a trend amplified during the pandemic, has spurred purchases of light commercial vans for parcel and food delivery.

From 2017 to 2023, Europe's LCV market witnessed a remarkable upswing, with volumes surging by 38%. This surge was propelled by the e-commerce boom, which fueled the expansion of delivery networks and subsequently boosted van sales. Additionally, replacement demand from sectors like retail, construction, and services played a pivotal role. While the market contracted in 2020 due to pandemic disruptions, it swiftly rebounded, riding the wave of accelerated digital adoption. Overall, steady economic growth and robust infrastructure investments were key drivers of the European LCV market's expansion during this period.

The LCV market in Europe is poised to register a CAGR of 3.1% from 2024 to 2030. This growth trajectory will be propelled by ongoing infrastructure development, the continued expansion of last-mile delivery networks, and the rising urbanization trend. These factors, coupled with the increasing demand for LCVs in services, food delivery, and construction sectors, paint a promising outlook. However, the market may face headwinds as evolving regulations on emissions and urban access could bolster the adoption of alternatively fueled vans.

Country-specific trends within the European light commercial vehicles market highlight the region's push toward reducing emissions and enhancing efficiency

Major European markets witnessed varying LCV sales volumes in 2022, reflecting their distinct economic landscapes. Germany, buoyed by a resilient economy, saw a robust 6.3% growth. Conversely, the United Kingdom faced economic uncertainties, leading to a contraction of 2.1% in LCV sales. France, Italy, and Spain experienced declines of 3% to 5%, aligning with broader macroeconomic challenges. However, as the post-pandemic conditions improve, 2023 is projected to witness a rebound, with most countries eyeing a volume growth of 4-6%.

From 2017 to 2021, the prominent European LCV markets - Germany, France, Italy, Spain, and Poland - showcased healthy expansion, registering a pre-pandemic CAGR of approximately 3-5%. This growth was propelled by robust economic activities, particularly in industries like construction, delivery, and services. While the pandemic-induced contractions in 2020 were relatively short-lived, the recovery has been uneven, primarily due to disparities in fiscal stimulus measures and vulnerabilities in industries such as retail and hospitality.

The European LCV market is poised for a steadier growth trajectory, with an anticipated annual average of 3-4% from 2023 to 2029. Factors such as infrastructure investments, the rise of last-mile delivery networks, and ongoing economic recovery are expected to bolster demand. However, risks loom from factors like high inflation, energy costs, and political uncertainties. Additionally, the market's shift toward electric drivetrains will further shape its dynamics. The European LCV market is set for a gradual expansion in the long run.

Europe Light Commercial Vehicles Market Trends

Environmental concerns, government support, and decarbonization goals fuel European electric vehicle demand and sales

The demand and sales of electric vehicles in European countries have grown significantly over the past few years. Germany witnessed a growth in the sales of electric cars by 22% in 2022 over 2021, followed by the United Kingdom with an 18.40% increase in 2022 over 2021. Growing environmental concerns, stringent governmental norms, advantages of electric vehicles such as fuel efficiency, low service cost, no carbon emissions, and subsidies by the government are some of the factors contributing to the growth of electric vehicles in European countries.

The demand for electric commercial vehicles, especially light trucks, is growing gradually in European countries. Moreover, the governments of various countries are also supporting the adoption of electric vehicles. In November 2021, the government of the United Kingdom announced a pledge that all heavy-duty vehicles would be zero-emission by the year 2040. Such factors have increased the sales of electric commercial vehicles in the United Kingdom by 23.17% in 2022 over 2021, and similar practices in various countries are enhancing the demand for electric commercial vehicles across Europe.

It is projected that the electrification of vehicles in European countries is expected to grow tremendously in the next few years. The efforts of the governments in the regions for decarbonization are expected to drive the electric commercial vehicle market in Europe. For instance, in January 2022, the transport minister of Germany announced a goal to put 15 million electric vehicles on the road by 2030. Such factors are expected to increase the sales of electric vehicles during the 2024-2030 period in European countries.

Europe Light Commercial Vehicles Industry Overview

The Europe Light Commercial Vehicles Market is moderately consolidated, with the top five companies occupying 62.47%. The major players in this market are Fiat Chrysler Automobiles N.V, Ford Motor Company, Groupe Renault, Peugeot S.A. and Volkswagen AG (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Population

4.2 GDP Per Capita

4.3 Consumer Spending For Vehicle Purchase (cvp)

4.4 Inflation

4.5 Interest Rate For Auto Loans

4.6 Impact Of Electrification

4.7 EV Charging Station

4.8 Battery Pack Price

4.9 New Xev Models Announced

4.10 Logistics Performance Index

4.11 Fuel Price

4.12 Oem-wise Production Statistics

4.13 Regulatory Framework

4.14 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)