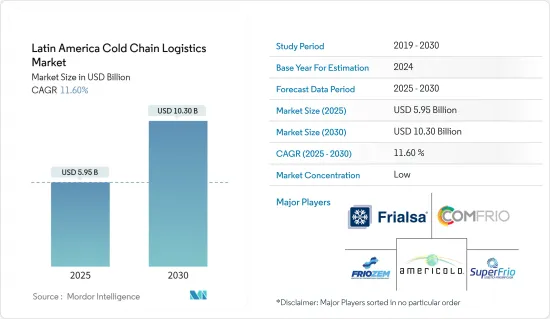

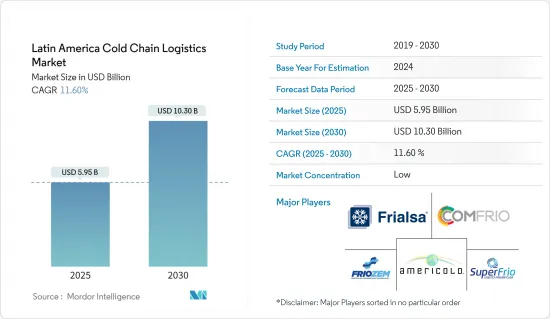

라틴아메리카의 콜드체인 물류 시장 규모는 2025년에는 58억 7,000만 달러로 추정되고, 2030년에는 101억 5,000만 달러에 달할 것으로 예측되고, 예측 기간(2025-2030년)의 CAGR은 11.60%를 나타낼 전망입니다.

라틴아메리카 국가들은 다양한 제품을 전 세계로 수출하고 있으며, 많은 제품이 자연 상태 그대로 소비자에게 전달되며 품질을 중시합니다. 육류, 생선, 과일, 유제품을 포함한 이러한 제품은 중단 없는 콜드 체인에 크게 의존합니다. 북미, 유럽, 심지어 라틴아메리카가 주요 목적지이지만, 코로나19 백신과 같은 특정 제품, 특히 의약품은 아프리카와 남미로 향하고 있습니다.

특히 Pfizer/Biontech의 코로나19 백신과 같이 초저온 보관이 필요한 의약품에 대한 수요가 급증하면서 라틴아메리카의 콜드 체인 부문은 혁신과 확장을 추진했습니다. 하지만 노동력 부족과 인프라 미비로 인해 정치, 사회, 재정적 통합 노력이 필요한 등 여전히 과제가 남아 있습니다.

라틴아메리카의 백신 무역은 냉동 식품 및 유제품에 대한 수요 증가와 맞물려 시장을 견인하는 중추적인 역할을 하고 있습니다. 브라질이 선두를 달리고 있으며 멕시코, 아르헨티나, 콜롬비아가 그 뒤를 따르고 있습니다.

라틴아메리카의 부패하기 쉬운 식품 공급망은 인력 부족과 최대 용량 창고와 같은 문제에도 불구하고 여전히 탄력적입니다. 이러한 장애물로 인해 기존 지역 업체들은 이 지역의 냉장 공간 부족 문제를 해결하기 위해 기술력을 강화하고 있습니다.

2022년 10월, 우루과이의 몬테비데오에 본사를 둔 Frigorifico Modelo(Frimosa)는 이 회사의 냉장 창고 사업을 Emergent Cold LatAm에 매각한다고 발표했습니다. Cold LatAm은 파라과이의 아순시온에 있는 8,400팔레트의 창고를 구입할 예정입니다.

결론적으로 라틴아메리카의 콜드 체인 부문은 의약품 및 부패하기 쉬운 식품에 대한 수요 증가로 인해 상당한 성장을 경험하고 있습니다. 인력 부족과 인프라 격차 등의 문제에 직면해 있지만, 기술 발전과 전략적 투자를 통해 이 분야는 더욱 발전할 준비가 되어 있습니다.

신선식품의 국제 무역이 증가함에 따라 신뢰할 수 있는 콜드 체인에 대한 필요성이 증가하고 있습니다. 이 시장에서 활동하는 기업은 국제적으로 제품의 품질과 안전성을 보장해야 합니다. 신선 식품의 국제 무역이 증가함에 따라 강력한 콜드 체인에 대한 수요가 높아졌습니다.

국가 간 고객을 위한 원활한 엔드투엔드 연결을 지원하는 것은 전략적인 움직임일 뿐만 아니라 상당한 경제적 이점도 제공합니다. 이러한 접근 방식은 공급망 운영을 간소화하여 운영 효율성을 향상시킵니다. 경제적으로는 비용 절감과 시장 점유율 확대를 통한 수익성 향상으로 이어져 더욱 가치 있는 물류 파트너로 자리매김할 수 있습니다.

온도관리된 창고와 물류의 선두 공급자인 Emergent Cold LatAm은 타르카와노에 칠레 최대의 냉동 식품 창고를 개설했습니다.이 마일스톤은 라틴아메리카에서의 에머전트 콜드의 가장 큰 확대를 의미합니다.

29만 4,000m3, 3만 7,000팔레트의 보관 능력을 자랑하는 이 시설은 150명의 직접 고용과 추정 500명의 간접 고용 기회를 창출하여 지역 경제를 강화합니다.

현지 및 해외 투자자들의 지원을 받아 이 지역을 위한 전용 투자 수단이 설립되었습니다.

브라질은 시장 수요 증가, 기술 발전, 보다 효율적이고 광범위한 콜드 체인 물류 네트워크에 대한 시급한 필요성에 힘입어 라틴아메리카 전역에서 콜드 스토리지 투자 급증의 선두를 달리고 있습니다.

결론적으로 Emergent Cold LatAm의 신규 시설로 대표되는 라틴아메리카의 콜드 체인 인프라 확장은 글로벌 신선식품 시장에서 라틴아메리카의 중요성이 커지고 있음을 보여줍니다.

최근 몇 년 동안 브라질 콜드체인 물류 시장은 부패하기 쉬운 상품에 대한 수요 증가와 급성장하는 제약 부문에 힘입어 눈에 띄게 확장되었습니다.

이들 소비자의 25%는 한 달에 4-5회, 30%는 2회 이상, 40%는 월 1회 이상 냉동식품을 구매하는 등 주목할 만한 구매 패턴을 보입니다. 특히 여성이 냉동식품 구매의 73%를 차지하며 이 시장을 지배하고 있습니다. 냉동 식품 중 가장 선호하는 제품은 육류(39%), 피자(33%), 라자냐(10%)입니다.

냉동식품 시장은 주로 중상류층(42%)과 중하류층(29%)에 의해 형성되고 있습니다.

브라질에는 700개 이상의 냉동 식품 기업이 운영 중이며, 대부분(90% 이상)이 소규모 기업으로 분류됩니다.

냉동 식품 분야에서 두각을 나타내고 있지만 브라질의 현재 냉장 저장 용량은 600만 입방미터로 약 30% 부족합니다. 이러한 부족은 냉동 식품 시장에 심각한 영향을 미칩니다.

증가하는 수요를 충족하기 위해 브라질은 콜드 체인 인프라 확장에 우선순위를 두고 투자해야 합니다. 과일, 육류, 설탕, 대두의 주요 수출국으로서 브라질은 특히 글로벌 육류 시장에서 성장 전망이 밝습니다.

브라질 콜드체인 시장은 성장이 가속화될 것으로 보입니다. 이는 브라질의 냉장 제품 수출 증가, 현대 기술 및 자동화 도입 급증, 육류, 해산물, 과일, 채소에 대한 선호도 증가, 인프라 시설의 현저한 개선 등 여러 가지 요인에 기인합니다.

결론적으로 브라질 콜드체인 물류 시장은 부패하기 쉬운 상품에 대한 수요 증가와 인프라의 발전으로 인해 견고한 성장 궤도에 올라서고 있습니다. 이러한 성장을 지속하기 위해서는 현재의 냉장 보관 용량 부족 문제를 해결하고 최신 기술을 활용하는 것이 중요합니다. 특히 육류 수출을 중심으로 글로벌 시장에서 브라질의 역할이 계속 확대됨에 따라 콜드체인 물류 부문은 상품의 효율적이고 안전한 운송을 보장하는 데 중추적인 역할을 할 것입니다.

라틴아메리카의 콜드체인 물류 산업은 현지 업체와 글로벌 업체가 혼재되어 있는 세분화된 산업으로 두드러집니다. 이러한 다양성은 한 기업이 독주하지 않는 치열한 경쟁 환경을 강조합니다. 이 분야의 주요 경쟁업체로는 Frialsa Frigorificos SA, Comfrio Solucoes Logisticas, Friozem Armazens Frigorificos, Superfrio Armazens Gerais, Americold Logistics 등이 있습니다.

이 기업들은 IoT, RFID, 클라우드 스토리지, 전자 데이터 교환과 같은 첨단 기술을 도입하여 콜드 체인 물류의 효율성을 높이고 있습니다. 시장 입지를 강화하려는 기업들의 인수합병이 증가하고 있습니다.

The Latin America Cold Chain Logistics Market size is estimated at USD 5.87 billion in 2025, and is expected to reach USD 10.15 billion by 2030, at a CAGR of 11.60% during the forecast period (2025-2030).

Latin American nations export a diverse range of products globally, with many reaching consumers in their natural state, emphasizing quality. These products, including meat, fish, fruits, and dairy, rely heavily on an uninterrupted cold chain. While North America, Europe, and even Latin America itself are primary destinations, certain products, notably pharmaceuticals like the Covid-19 vaccines, have found their way to Africa and South America.

The surge in demand for medicines, notably those requiring ultra-low temperatures like Pfizer/Biontech's Covid-19 vaccine, has propelled the cold chain sector in Latin America to innovate and expand. Yet, challenges persist, with labor shortages and inadequate infrastructure necessitating a unified political, social, and financial effort.

Latin America's vaccine trade, coupled with a rising appetite for frozen foods and dairy, has been pivotal in propelling the market. Brazil leads the pack, trailed by Mexico, Argentina, and Colombia. Projections suggest a significant uptick in processed food sales until 2025, presenting a lucrative opportunity for cold chain logistics and warehousing firms. Peru, poised for a 15.16% growth rate from 2020 to 2026, is set to join the region's leading cold chain players.

Despite challenges like workforce shortages and full-capacity warehouses, Latin America's perishable food supply chain remains resilient. These hurdles are prompting established regional players to bolster their technological prowess, aiming to combat the region's refrigerated space deficit.

In a notable move in October 2022, Uruguay's Montevideo-based Frigorifico Modelo (Frimosa) announced the sale of its cold storage operations to Emergent Cold Latin America (Emergent Cold LatAm). Emergent Cold LatAm, a key player in refrigerated storage and logistics in the region, will acquire Frimosa's primary facility in Polo Oeste, boasting 22,000 cold storage pallets, a bonded warehouse, and ample room for expansion. Additionally, Emergent Cold LatAm is set to purchase an 8,400-pallet warehouse in Asuncion, Paraguay.

In conclusion, the cold chain sector in Latin America is experiencing significant growth driven by increased demand for pharmaceuticals and perishable foods. Despite facing challenges such as labor shortages and infrastructure gaps, the sector is poised for further development through technological advancements and strategic investments. The ongoing consolidation and expansion efforts by key players like Emergent Cold LatAm highlight the region's potential to overcome these obstacles and meet the growing market demands.

The increase in international trade in fresh food has led to an increase in the need for reliable cold chains. Companies operating in these markets must ensure the quality and safety of their products during internationaThe rise in global trade of fresh food has heightened the demand for robust cold chains. Companies in this space must prioritize effective cold chain management to guarantee product quality and safety during international transit.

Enabling seamless end-to-end connections for customers across nations is not just a strategic move but also a significant economic advantage. This approach streamlines supply chain operations, enhancing operational efficiency. Economically, it can lead to heightened profitability through cost savings and an expanded market share, positioning the company as a more valuable logistics partner.

Emergent Cold Latin America (Emergent Cold LatAm), the leading provider of temperature-controlled storage and logistics in the region, unveiled Chile's largest frozen food warehouse in Talcahuano. This milestone marks Emergent Cold's most substantial expansion in Latin America. Given Talcahuano's global reputation for seafood and fruit exports, this warehouse stands as a pivotal addition to the local cold chain infrastructure.

Boasting a storage capacity of 294,000 m3 and 37,000 pallets, this facility is set to create 150 direct jobs and an estimated 500 indirect job opportunities, bolstering the regional economy.

Backed by both local and international investors, a dedicated investment vehicle was established for the region. Historically, Latin America, barring a few exceptions in Brazil and Mexico, lacked a unified warehouse network. The primary aim was to create a pan-Latin American network, transcending individual borders, and offering a holistic food supply chain solution.

Brazil spearheads the surge in cold storage investments across Latin America, driven by rising market demands, technological progress, and the pressing need for more efficient and expansive cold chain logistics networks.

In conclusion, the expansion of cold chain infrastructure in Latin America, exemplified by Emergent Cold LatAm's new facility, highlights the region's growing importance in the global fresh food market. As investments continue to pour in, the region is poised to become a critical hub for temperature-controlled logistics, ensuring the safe and efficient transport of perishable goods across borders.

In recent years, the Brazil cold chain logistics market has seen notable expansion, primarily fueled by a rising appetite for perishable goods and the burgeoning pharmaceutical sector. Notably, Brazil's frozen food sector is buoyed by the purchases of its upper and middle-class consumers.

These consumers exhibit a noteworthy buying pattern: 25% purchase frozen food 4-5 times a month, 30% do so at least twice, and 40% make the purchase at least once monthly. Women, in particular, dominate this market, accounting for 73% of frozen food purchases. Among the frozen food offerings, meat (39%), pizzas (33%), and lasagnas (10%) stand out as the most favored.

The market is largely shaped by the high middle class (42%) and the low middle class (29%). The rise of Brazil's middle class, combined with the time constraints faced by working families, is a key driver behind the frozen food market's growth.

The industry boasts over 700 frozen food businesses in operation, with the majority (over 90%) classified as small enterprises. Brazil's role as a frozen meat exporter is substantial, offering a diverse range that includes frozen beef tripe, tenderloins, and various beef cuts.

Despite its prominence in the frozen food arena, Brazil's current cold storage capacity of 6 million cubic meters falls short by about 30%. This shortfall bears significant consequences for the frozen food market. Inadequate cold storage and transportation facilities can result in substantial product wastage, potentially affecting the supply and affordability of frozen foods.

To meet the escalating demand, Brazil must prioritize investments in expanding its cold chain infrastructure. Given its status as a leading exporter of fruits, meat, sugar, and soybeans, Brazil holds promising growth prospects, particularly in the global meat market.

The Brazil cold chain market is poised for accelerated growth. This is attributed to several factors, including the country's increased exports of refrigerated products, a surge in the adoption of modern technologies and automation, a rising appetite for meat, seafood, fruits, and vegetables, and notable improvements in infrastructure facilities. Furthermore, the market share of cold transport is expected to witness a rise, thanks to these enhanced infrastructure facilities.

In conclusion, the Brazil cold chain logistics market is on a robust growth trajectory, driven by the increasing demand for perishable goods and advancements in infrastructure. Addressing the current shortfall in cold storage capacity and leveraging modern technologies will be crucial for sustaining this growth. As Brazil continues to expand its role in the global market, particularly in meat exports, the cold chain logistics sector will play a pivotal role in ensuring the efficient and safe transportation of goods.

In Latin America, the cold chain logistics sector stands out for its fragmentation, hosting a mix of local and global players. This diversity underlines a fiercely competitive landscape, where no single entity reigns supreme. Key contenders in this arena include Frialsa Frigorificos SA, Comfrio Solucoes Logisticas, Friozem Armazens Frigorificos, Superfrio Armazens Gerais, and Americold Logistics.

These companies are pivoting towards cutting-edge technologies like IoT, RFID, cloud storage, and electronic data interchange, amplifying the efficiency of their cold chain logistics. Mergers and acquisitions are on the rise, as firms seek to bolster their market foothold. For instance, Emergent Cold Latin America's acquisition of Frigorifico Modelo's operations in Uruguay and a new warehouse in Paraguay underscores this trend.