ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

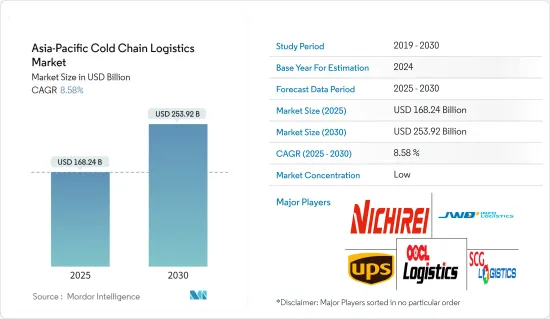

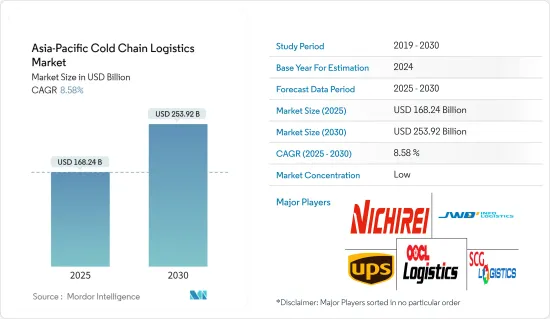

아시아태평양의 콜드체인 물류 시장 규모는 2025년에 1,682억 4,000만 달러, 2030년에는 2,539억 2,000만 달러에 달할 것으로 예측됩니다. 예측 기간(2025년-2030년) CAGR은 8.58%를 나타낼 전망입니다.

냉장 창고 증가와 의약품 분야 시장 개척 등의 요인이 아시아태평양의 콜드체인 물류 시장의 성장을 이끌 것으로 예상됩니다.

주요 하이라이트

콜드체인 물류는 아시아태평양에서 인기가 있습니다.이 지역은 세계 인구의 약 60%를 차지하는 대규모 소비자 기반을 가지고 있습니다. 이러한 제품의 수송도 중요합니다. 물론 COVID-19는 식품의 안전성에 대한 우려 증가 등 아시아의 콜드체인 사업에도 영향을 미치고 있습니다. 이미 소비자의 습관을 바꾸고 있어, 신선 식품이나 냉동 식품을 종래의 습식 시장이 아니고, 슈퍼마켓과 같은 조직화된 소매 채널로 구입하는 사람이 늘어나고 있습니다. 전자상거래와 온라인 식품 소매의 대두도 냉동 식품 수요를 촉진하고 있습니다.

일본은 콜드체인 물류의 성숙 시장으로 간주되고 있으며, 여러 기업이 우위를 차지하고 있습니다. 자동차, 무역 회사, 도매업체 등 다양한 업계의 고객이 이 회사의 저온 물류 서비스를 이용하고 있습니다.

콜드체인 용도용 RFID(Radio-Frequency Identification) 기술의 가용성과 콜드체인 물류용 자동화 소프트웨어의 채용은 시장 기업에게 유리한 성장 기회를 제공할 것으로 예측됩니다. 최근 몇 년간 국내 소비 호조, 전자상거래 산업의 확장, 현대 물류 시설의 발전으로 인해 아시아 태평양 지역에서 고품질 산업 및 물류 자산에 대한 수요가 견고하게 증가하고 있습니다. 가처분 소득 증가와 고령화에 의해 아시아태평양에는 헬스 케어 용품에 대한 방대한 소비자층이 존재합니다.

식생활 패턴의 변화에 따라 고기, 유제품, 어패류 등 온도에 민감하고 관리된 온도에서의 보관 및 수송이 필요한 고급품에 대한 수요가 높아지고 있습니다. 아시아 태평양 지역의 냉장 보관 시설에 대한 강력한 임대 수요에도 불구하고, 이 지역의 냉장 보관 용량은 선진 서구 시장에 비해 제한적입니다. 냉장 창고의 임대료는 드라이 창고보다 높습니다.그러나, 작업 순서, 시큐리티, 온도, 해충 방제에 관한 표준화가 진행되고 있지 않는 것, 운용 코스트 증가라고 하는 요인이, 시장의 성장을 억제하고 있습니다.

아시아태평양 콜드체인 물류 시장 동향

일본 국내 수상화물 운송량 감소

일본의 국내 화물 취급량은 매년 47억 톤을 넘습니다. 물, 철도, 항공, 도로 등 모든 수송 수단이 경제에서 중요한 역할을 하고 있습니다.

일본에서는 자동화의 급속한 개발이 진행되고 있습니다.

트럭 운송과 내항해운은 연간 적재거리라는 점에서 일본의 물류업계를 지배하는 운송수단입니다.

냉장창고 증가

COVID-19의 유행은 공급망 전망에 큰 변화를 가져오고, 건강에 대한 우려와 함께 업무 효율을 달성하기 위한 디지털 하이엔드 기술의 이용 확대를 가능하게 했습니다.

콜드체인 시스템을 구성하는 일부 창고는 온도에 민감한 제품의 이상적인 보관 및 운송 조건을 보장하도록 설계되었습니다.

엔드 투 엔드 콜드체인 보안이 시스템의 약점이기 때문에 기업은 효과적이고 효율적이며 신뢰할 수있는 프로세스를 구축하기 위해 콜드체인 비즈니스에 수백만 달러를 투자했습니다. 또한 아시아태평양의 식품 및 의약품 수요가 급증함에 따라 냉장 창고의 수가 증가하고 있습니다.

아시아태평양 콜드체인 물류 산업 개요

아시아태평양의 콜드체인 시장은 매우 세분화되어 있으며 많은 세계 기업과 현지 기업이 수요 증가에 대응하고 있습니다. 과제는 방대한 에너지와 공간 소비, 막대한 설정 및 변경 비용입니다. 저장 온도나 작업 순서에 관한 표준화의 부족은 업계가 직면하는 더욱 중요한 과제입니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

분석 방법

조사 단계

제3장 주요 요약

제4장 시장 역학

현재의 시장 시나리오

시장 개요

시장 역학

성장 촉진요인

억제요인

기회

밸류체인, 서플라이체인 분석

Porter's Five Forces 분석

신규 참가업체의 위협

구매자 및 소비자의 협상력

공급기업의 협상력

대체품의 위협

경쟁 기업간 경쟁 관계

기술 동향과 자동화

정부의 규제와 대처

환경·온도 관리 보관에 대한 주목

배출 기준 및 규제가 콜드체인 업계에 미치는 영향

시장에 대한 COVID-19의 영향

제5장 시장 세분화

서비스별

보관

수송

부가가치 서비스(블라스트 동결, 라벨링, 재고 관리 등)

온도 유형별

칠드

냉동

용도별

원예(신선 과일, 야채)

유제품(우유, 아이스크림, 버터 등)

고기, 생선, 닭고기

가공식품

제약, 생명과학, 화학

기타 용도

국가별

중국

일본

인도

한국

인도네시아

태국

호주

필리핀

기타 아시아태평양

제6장 경쟁 구도

시장 집중도 개요

기업 프로파일

United Parcel Service of America

OOCL Logistics Ltd

JWD Infologistics Public Company Ltd

Nichirei Logistics Group Inc.

SCG Logistics Management Company Limited

X2 Logistics Network(X2 GROUP)

AIT Worldwide Logistics Inc.

CWT PTE. LIMITED(CWT International Ltd)

SF Express

CJ Rokin Logistics*

제7장 아시아태평양의 콜드체인 물류 시장의 장래성

제8장 부록

SHW

영문 목차

영문목차

The Asia-Pacific Cold Chain Logistics Market size is estimated at USD 168.24 billion in 2025, and is expected to reach USD 253.92 billion by 2030, at a CAGR of 8.58% during the forecast period (2025-2030).

Factors such as the increasing number of refrigerated warehouses and the development of the pharmaceutical sector are expected to drive the growth of the Asia-Pacific cold chain logistics market.

Key Highlights

Cold chain logistics are popular in the Asia Pacific. The region has a large consumer base, accounting for roughly 60% of the global population. Demand for premium products is increasing, driven by rising disposable incomes and a shift in dietary habits. Transportation for these products is also important. Of course, COVID-19 has had an impact on Asian cold chain operations, including increased concerns about food safety. This is already changing consumer habits, with more people buying fresh and frozen food from organized retail channels like supermarkets rather than traditional wet markets. The rise of e-commerce and online food retailing has also fueled demand for frozen foods. These trends have increased the demand for cold storage facilities in the region and bolstered further investments in infrastructure and transportation improvements.

Japan is regarded as a mature market for cold chain logistics, with several players dominating. Nichirei Logistics Group Inc., based in Tokyo, was founded in 1945 as Nippon Reizo Inc. Today, the company provides warehousing, cold storage, and transportation services in Japan and around the world. Customers in a variety of industries use its low-temperature logistics services, including restaurants, retail stores, food manufacturers, trading companies, and wholesalers. The 'upper limit on overtime hours in automobile driving operations' will be implemented in Japan in 2024, raising concerns about the impact on the transportation and logistics industries. Technological innovation is also expected to improve work efficiency, reduce workplace errors, and prevent accidents.

The availability of Radio-frequency identification (RFID) technologies for cold chain applications and the adoption of automated software for cold chain logistics is projected to offer lucrative growth opportunities for the market players. Recent years have seen robust demand for high-quality industrial and logistics assets in Asia-Pacific due to strong domestic consumption, the e-commerce industry's expansion, and the development of modern logistics facilities. Due to the rising disposable income and ageing population, Asia-Pacific has a vast consumer base for healthcare supplies. There are increasing concerns over food safety and a continuous shift in consumer habits to buy fresh and frozen food products from organized retail channels, such as supermarkets, compared to traditional wet markets.

The shift in dietary patterns is increasing the demand for premium products, including meat, dairy, and seafood, which are temperature-sensitive and need to be stored and transported at controlled temperatures. Despite robust leasing demand for cold storage facilities in Asia-Pacific, cold storage capacity in the region is limited compared to that in developed western markets. Cold storage facilities command higher rental premiums than dry warehouses. However, factors such as lack of standardization about operating procedures, security, temperature, pest control, and increased operational costs restrain the market's growth.

Asia Pacific Cold Chain Logistics Market Trends

Decreasing Volume of Domestic Water Freight Transport in Japan

Japan handles more than 4.7 billion tons of domestic freight every year. Every mode of transport, including water, rail, air, and road, fulfills a crucial role in the economy. While cargo transport relies primarily on demand created by manufacturing industries and consumption, transportation creates demand for trucks and vehicles of any kind, including drones.

Rapid developments in automation are taking place in Japan. The Japanese logistics industry suffers labor shortages, and the existing drivers are rapidly aging, thereby threatening to increase the fraction of transport costs in the sale of goods.

Trucking and coastal shipping are the Japanese logistics industry's dominant modes of transport in terms of yearly payload distance. Railway and air transport are also used for transporting goods. However, despite the railway network being highly efficient for the transport of people, most logistics facilities, warehouses, and factories are better connected to roads.

Increased Number of Refrigerated Warehouses

The COVID-19 pandemic has resulted in a significant change in the supply chain outlook, enabling the growing usage of digital high-end technologies to attain operational efficiency along with health concerns. The changing logistics industry outlook, requirement for substantial cost optimization, and optimum inventory management are anticipated to support the growth of the Asia-Pacific cold chain logistics market.

Several warehouses comprising cold chain systems are designed to ensure the ideal storage and transportation conditions for temperature-sensitive products. Multiple export industries are now dependent on the vital links provided by cold chain solutions.

Businesses are investing millions of dollars in their cold chain operations to create effective, efficient, and reliable processes, as end-to-end cold chain security is the weak link in the system. Moreover, the number of refrigerated warehouses is increasing due to a surge in demand for food and pharmaceutical products in the Asia-Pacific region. Therefore, an increase in refrigerated warehouses is anticipated to boost the growth of the Asia-Pacific cold chain logistics market.

Asia Pacific Cold Chain Logistics Industry Overview

The Asia-Pacific cold chain market is highly fragmented, with many global and local players catering to the growing demand. UPS, OOCL Logistics, and JWD are some of the major players in the market. Critical challenges faced by the cold chain industry are enormous energy and space consumption and huge setup and modification costs. Lack of standardization related to storage temperature and operating procedures are a few more significant challenges the industry faces. The quality and flexibility of available cold warehousing space are a considerable concern.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

2.1 Analysis Method

2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS DYNAMICS

4.1 Current Market Scenario

4.2 Market Overview

4.3 Market Dynamics

4.3.1 Drivers

4.3.2 Restraints

4.3.3 Opportunities

4.4 Value Chain / Supply Chain Analysis

4.5 Porters Five Forces Analysis

4.5.1 Threat of New Entrants

4.5.2 Bargaining Power of Buyers/Consumers

4.5.3 Bargaining Power of Suppliers

4.5.4 Threat of Substitute Products

4.5.5 Intensity of Competitive Rivalry

4.6 Technological Trends and Automation

4.7 Government Regulations and Initiatives

4.8 Spotlight on Ambient/Temperature-controlled Storage

4.9 Impact of Emission Standards and Regulations on Cold Chain Industry