인쇄회로기판(PCB) 산업 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2024-2029년)

Printed Circuit Board (PCB) Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

상품코드:1687833

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

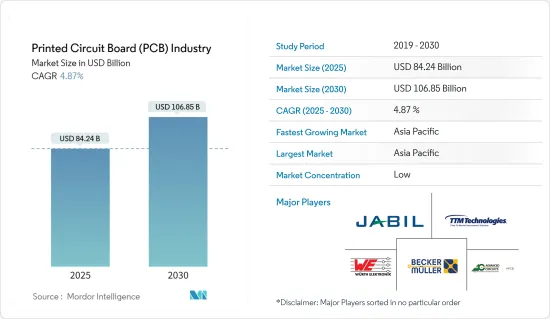

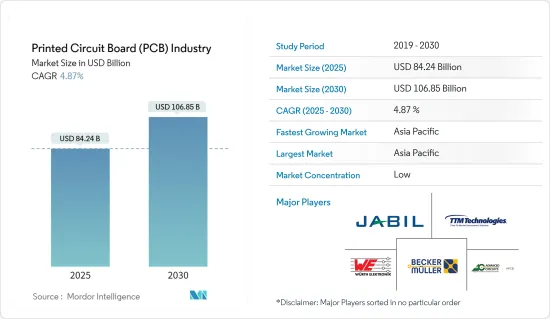

인쇄회로기판(PCB) 시장 규모는 2024년에 803억 3,000만 달러로 평가되었고, 2029년에는 965억 7,000만 달러 규모에 이를 전망입니다. 예측 기간 중(2024-2029년)의 CAGR은 4.87%를 나타낼 것으로 예측됩니다.

주요 하이라이트

저렴한 스마트폰 생산 증가로 휴대폰 PCB 생산 증가가 예상됩니다. 일본 전산에 의하면 스마트폰은 감소 경향에 있는 것으로, 세계에서 연간 13억대가 출하되고 있습니다. PCB는 마이크로프로세서, 메모리 칩, 센서, 기타 집적 회로 등 다양한 전자 부품을 연결하고 지원하는 중요한 휴대폰 부품이기 때문에 이러한 동향은 PCB에 큰 기회가 됩니다.

소비자용 PCB는 확실히 새로운 것은 아니지만, 일렉트로닉스용 PCB의 용도와 그 제조에 사용되는 재료는 잠시 동안 진화해 왔습니다. 이것은 특히 소형화의 동향에서 필연적인 일입니다. 게다가 현대의 전자기기나 컴퓨터 용도에서는 발생한 열을 방산할 수 있도록 열전도율이 높은 PCB가 필요합니다. 다양한 유형의 가전제품이 사용되기 때문에 다양한 PCB가 필요합니다. 예를 들어, 스마트 워치에 필요한 PCB와 컴퓨터에 필요한 PCB는 다릅니다.

PCB는 작고 가볍기 때문에 휴대용 가전에 매우 적합합니다. PCB 어셈블리 산업의 성장과 효율은 잘 설계되고 조립된 PCB에 가전제품이 크게 의존하기 때문입니다. 고성능 인쇄회로기판을 효과적으로 통합함으로써 다양한 소비자용 전자 기기를 최적화하고 일상 업무를 원활하게 수행할 수 있습니다. PCB가 필수적인 것은 스마트폰, 텔레비전, 노트북, 게임기 등 폭넓은 가전제품에 걸쳐 있으며, 그 컴팩트한 설계와 복잡한 회로를 수용하는 능력 때문입니다.

PCB 시장의 성장을 가속하는 한 가지 큰 동향은 5G와 같은 선진기술의 채택이 증가하고 있는데, 이는 다양한 정부기관과 민간조직으로부터의 투자 증가에 의해 크게 지지되고 있습니다.

예를 들어, 2024년 3월, 에릭슨은 미국 연방 정부 전체에 5G 주도 디지털 변환을 실현하기 위한 전문 사업체를 새로 설립할 것이라고 발표했습니다. 이 발표는 5G 통신이 미국의 국가 안보와 경제 안보에 필수적이며 미국의 방어 근대화 프로그램의 중요한 구성 요소이기 때문에 5G 통신의 중요성이 높아지고 있음을 고려하여 이루어졌습니다.

인쇄 회로 기판(PCB)과 같은 전자 폐기물에 대한 우려 증가는 해결해야 할 심각한 환경 문제입니다. PCB에는 납, 수은 카드뮴, 브롬계 난연제 등 다양한 유해 물질이 포함되어 있습니다. 부적절하게 폐기되면 이러한 물질이 토양과 물에 녹아 사람의 건강과 환경에 위협을 줄 수 있습니다.

매립 및 소각과 같은 PCB의 부적절한 폐기는 환경에 심각한 결과를 초래할 수 있습니다. PCB가 매립지에 폐기되면 유해 물질이 토양으로 침투하여 지하수를 오염시킬 수 있습니다. PCB를 소각하면 독성 가스와 입자가 대기 중으로 방출되어 대기 오염의 원인이 됩니다.

또한 반도체 산업에서 대만의 중요성이 높아지고 반도체 제조 설비의 다양화의 중요성이 높아지는 요인이 향후 PCB의 수급 구조를 형성해 나갈 것으로 보입니다.

인쇄 회로 기판(PCB) 시장 동향

소비자 일렉트로닉스 부문이 가장 큰 최종 사용자 산업에

소비자 일렉트로닉스 산업에서 PCB 수요가 증가함에 따라 정부는 PCB 제조에 대한 인식을 넓히고 학생들에게 필요한 교육을 제공하기 위한 이니셔티브를 취하고 있습니다.

예를 들어, 2024년 2월 매사추세츠 대학 로웰은 PCB 설계 및 제조에서 학생과 산업 종사자의 훈련을 지원하기 위해 매사추세츠 전자 제조 진화(MEME) 연구소 설립을 발표했습니다. 이 프로젝트는 장비 구매를 위한 50만 달러의 매사추세츠 기술 자본 보조금으로 지원됩니다. 매사추세츠 주 워크포스 스킬 캐비닛은 자본 예산을 통해 주에서 자금을 지원하는 보조금 프로그램을 제공합니다.

PCB 프로토타이핑 시설은 미국, 인도, 중국 등 국가의 기업이들이 세계적으로 출시할 수 있는 최첨단 제품을 생산할 수 있게 해주는 현대 기술에 매우 중요한 요소입니다.

2023년 3월 인도 최대의 프로토타입 센터인 T-Works는 퀄컴과 제휴하여 최첨단 다층 PCB 제조 시설을 설립했습니다. 이 새로운 시설은 의료기기, 전기자동차, 가전제품, 산업용 자동화 제품 등 다양한 제품 개발을 지원할 것으로 기대됩니다.

가전 업계에서는 사용자의 스마트폰에 대한 의존도를 낮추기 위해 각 회사가 웨어러블 IoT 장치를 개발하고 있습니다. 이 장치는 스마트 시계 및 보온장치와 같은 1차적이고 저렴한 가젯부터 고급 스마트 홈 오토메이션 용도, 스마트 의류, 시계, 히어러블, 안경까지 다양합니다. 사용자의 업무, 커뮤니케이션, 일상 업무 수행 방법은 이러한 장치에 따라 변화하고 있습니다. 소비자를 위한 IoT 디바이스의 사용과 인기가 현저하게 증가하고 있으며, 이러한 추세는 사람들이 보다 저렴한, 빠르고, 고성능, 보다 안전한 IoT 디바이스를 요구하는 한 지속될 것으로 예상됩니다. 에릭슨에 따르면 스마트 가전과 같은 근거리 IoT 디바이스는 2027년까지 251억 5,000만대에 이를 것으로 예상되고 있으며, 이는 시장 성장을 견인할 것으로 보입니다.

게다가 IoT 도입 증가와 커넥티드 디바이스에 대한 수요 증가가 시장을 견인할 것으로 보입니다. IoT Analytics의 최신 보고서인 State of IoT-Spring 2023에서는 2022년 세계 IoT 연결 수가 18% 증가한 143억 액티브 IoT 엔드포인트에 도달했다고 발표했습니다.

2023년에는 세계 연결 IoT 디바이스 수가 16% 증가한 167억 액티브 엔드포인트가 되었습니다. 2023년의 성장률은 2022년을 약간 밑돌았으며, IoT 디바이스 연결은 수년간 계속 성장할 것으로 예상됩니다. 또한 아시아태평양에서 연결된 장치의 소유율은 중국, 태국, 베트남에 거주하는 사람들 사이에서 이미 높습니다.

아시아태평양은 대폭적인 성장이 예상된다.

중국의 일렉트로닉스 산업이 급속히 발전함에 따라, 많은 중국 PCB 제조업체들이 세계 PCB 시장의 선두주자로 부상하고 아시아태평양 시장 점유율을 얻고 있습니다. 이 제조업체들은 경쟁력있는 가격과 빠른 납기로 PCB 설계, 제조 및 조립을 포함한 광범위한 서비스와 능력을 제공합니다. 이 제조업체들은 JLCPCB, Graperain, Fulltronics, YMS PCB Assembly, Hitech Circuits 등을 포함합니다.

현재 중국 본토에는 약 2,500개의 PCB 제조업체가 있습니다. 중국의 PCB 산업은 주로 주강 델타, 장강 델타, 환 발해에 분포하고 있으며 대규모 부품 시장, 양호한 교통 조건, 물 및 전기 조건을 집계하고 있습니다.

중국 지역의 PCB 시장 성장을 가속하는 주된 이유는 전반적인 비용 감소와 경영 효율성 향상입니다. 첫째, 중국의 인구 보너스가 끝나고 있지만, 인건비는 일본, 한국, 대만보다 여전히 낮고 구미보다 훨씬 낮습니다. 둘째, 중국의 환경보호, 노동조합, 복지분야는 상대적으로 저비용입니다.

게다가 세계 최대의 제조국인 중국의 PCB 산업은 동박, 유리 섬유, 수지, 동장 적층판, PCB에 이르기까지 완전한 산업 체인을 가지고 있습니다. PCB는 최종 제품에 가깝고 많은 전자 장비도 중국에서 완성됩니다.

세계의 PCB 생산 능력을 중국으로 이전하고 다운스트림 전자 단말기 제품의 활발한 개발로 인해 중국의 PCB 산업은 급속한 발전 동향을 보이고 있습니다. 전자정보산업은 중국의 주요 발전을 위한 전략적, 필수적이고 선도적인 기둥이 되는 산업입니다. PCB산업은 전자정보산업의 발전의 초석으로서 중국이 장려하는 프로젝트의 하나가 되고 있습니다.

게다가 신뢰할 수 있는 산업단체의 실증 데이터는 대만이 세계 PCB 생산액에서 계속 우위를 차지하고 있으며 큰 시장 점유율을 차지하고 있음을 강조하고 있습니다. 주목할 점은 한국의 PCB 제조업체가 일본의 PCB 제조업체를 웃돌아 지역 규모로 3위의 지위를 확보하고 있다는 점입니다.

인쇄 회로 기판(PCB) 산업 개요

PCB(PCB) 시장은 세계 기업와 중소기업 모두가 존재하기 때문에 매우 단편화되고 있습니다. 시장의 주요 기업으로는 Jabil Inc., Wurth Elektronik Group(Wurth Group), TTM Technologies Inc., Becker & Muller Schaltungsdruck Gmbh, Advanced Circuits Inc. 등이 있습니다. 시장 기업은 제품 라인업을 강화하고 지속 가능한 경쟁 우위를 얻기 위해 파트너십 및 인수와 같은 전략을 채택합니다.

2024년 4월 - RF(Radio Frequency) 부품 및 첨단 인쇄 회로 기판과 같은 기술 솔루션의 세계 제조업체인 TTM Technologies는 2억 달러를 투자하여 말레이시아 페낭에 최초의 제조 공장을 개설했습니다. 이 회사에 따르면, 새로운 시설은 페낭 과학 공원 내에 건설되어 고도로 진보적이고 자동화 된 PCB 제조 능력을 갖추고 있습니다.

2023년 11월 - Jabil Inc.는 멕시코 치와와에 세 번째 생산 시설을 개설하여 이 지역으로의 지속적인 성장과 약속의 이정표로 자리잡았습니다. 이 공장은 250,000 평방 피트 이상의 넓이를 자랑합니다. 이 확장은 에너지, 자동차 및 운송, 건강 관리, 디지털 인쇄 및 소매 업계의 고객을 지원하는 데 매우 중요합니다. 이 새로운 시설은 업무 효율성과 유연성을 높이고 고품질 제품을 제공하는 능력을 강화합니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 및 지원

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

업계의 매력도 - Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

업계 밸류체인 분석

COVID-19의 부작용 및 기타 거시 경제 요인이 시장에 미치는 영향

제5장 시장 역학

시장 성장 촉진요인

기술 소형화에 대한 수요 증가

최종 사용자 산업에서의 수요 증가

시장 성장 억제요인

전자 폐기물에 대한 우려 증가

제6장 시장 세분화

제품 유형별

표준 다층 PCB

리지드 1-2면 PCB

HDI, 마이크로비아, 빌드업

유연한 PCB

리지드 플렉스 PCB

기타

최종 사용자 산업별

산업용 전자 기기

헬스케어

항공우주 및 방위

자동차

소비자 일렉트로닉스

기타 최종 사용자 산업

지역별

북미

유럽

아시아

호주 및 뉴질랜드

라틴아메리카

중동 및 아프리카

제7장 경쟁 구도

기업 프로파일

Jabil Inc.

Wurth elektronik group(Wurth group)

TTM Technologies Inc.

Becker & Muller Schaltungsdruck Gmbh

Advanced Circuits Inc.

Sumitomo Electric Industries Ltd(Sumitomo Corporation)

Murrietta Circuits

Unimicron Technology Corporation

Tripod Technology Corporation

AT&S Austria Technologie & Systemtechnik AG

Nippon Mektron Ltd(nok Group)

Zhen Ding Technology Holding Limited

제8장 벤더의 시장 점유율

제9장 투자 분석

제10장 시장 전망

SHW

영문 목차

영문목차

The PCB Market size is estimated at USD 80.33 billion in 2024, and is expected to reach USD 96.57 billion by 2029, growing at a CAGR of 4.87% during the forecast period (2024-2029).

Key Highlights

Increased production of budget smartphones means that phone PCB production is expected to increase. According to Nidec, despite the downfall, 1.3 billion smartphones are shipped annually worldwide. These trends largely represent real opportunities for the PCB, as it is a vital mobile phone component that connects and supports various electronic components such as microprocessors, memory chips, sensors, and other integrated circuits.

While consumer PCBs are certainly nothing new, the applications for PCBs for electronics and the materials used to make them have evolved over some time. This is inevitable, especially on account of the growing trend of miniaturization. Moreover, modern electronics and computer applications require PCBs with high thermal conductivity so that the heat generated can be dissipated. Different PCBs are needed for the many kinds of appliances in use. For example, the PCB needed to power a smartwatch is different from the PCB required for a computer.

PCBs are highly suitable for portable consumer electronics due to their small size and lightweight characteristics. The growth and efficiency of the PCB assembly industry can be attributed to the significant reliance of consumer electronic products on well-designed and assembled printed circuit boards. By incorporating high-performance PCBs effectively, various consumer electronic devices can be optimized to carry out everyday tasks seamlessly. The indispensability of PCBs extends to a wide range of consumer electronics, such as smartphones, televisions, laptops, and gaming consoles, owing to their compact design and capability to accommodate intricate circuitry.

One major trend driving the growth of the PCB market is the increasing adoption of advanced technologies such as 5G, which is significantly favored by growing investment from various government and private organizations.

For instance, in March 2024, Ericsson announced the establishment of a dedicated entity for delivering a new dedicated entity to deliver 5G-driven digital transformation across the federal United States Government. This announcement was made taking the rising importance of 5G communication into consideration, as it is vital for US national and economic security and a key component of US defense modernization programs.

The growing concerns regarding electronic waste, like printed circuit boards (PCBs), are a significant environmental issue that needs to be addressed. PCBs contain various hazardous materials, including lead, mercury, cadmium, and brominated flame retardants. When improperly disposed of, these substances can leach into the soil and water, posing a threat to human health and the environment.

Improper disposal of PCBs, such as landfilling or incineration, can have serious environmental consequences. When PCBs end up in landfills, hazardous materials can seep into the soil and contaminate groundwater. Incineration of PCBs can release toxic gases and particles into the air, contributing to air pollution.

Furthermore, factors such as the growing importance of Taiwan in the semiconductor industry and the increasing importance of diversifying semiconductor manufacturing facilities are likely to shape the supply and demand structure of PCBs in the future.

PCB Market Trends

Consumer Electronics Segment to be the Largest End-user Industry

Owing to the growing demand for PCBs in the consumer electronics industry, the government is taking initiatives to spread awareness and provide essential training to students for PCB manufacturing.

For instance, in February 2024, UMass Lowell announced the establishment of the Massachusetts Electronics Manufacturing Evolution (MEME) laboratory to help train students and industry workers in designing and fabricating PCBs. The project is supported with a USD 500,000 Massachusetts Skills Capital Grant for purchasing equipment for the facility. The Massachusetts Workforce Skills Cabinet offers the grant program, which is funded by the state through its capital budget.

The PCB prototyping facility is a crucial component of modern technology, enabling entrepreneurs from countries such as the United States of America, India, and China to create cutting-edge products that can be launched globally.

In March 2023, T-Works, India's largest prototype center, partnered with Qualcomm to establish a state-of-the-art multilayer Printed Circuit Board (PCB) fabrication facility. This new facility is anticipated to support the development of a wide range of products, including medical devices, electric vehicles, consumer electronics, industrial automation products, and more.

Companies are developing wearable IoT devices in the consumer electronics industry to reduce users' reliance on smartphones. These devices can vary from primary and affordable gadgets like smartwatches and thermostats to advanced smart home automation applications, smart clothing, watches, hearables, and glasses. The way users work, communicate, and perform their daily tasks is being transformed by these devices. The usage and popularity of consumer IoT devices have grown significantly, and this trend is expected to continue as long as people demand IoT devices that are more affordable, faster, capable, powerful, and safer. According to Ericsson, short-range IoT devices like smart home appliances are expected to reach 25,150 million by 2027, which is expected to drive the market's growth.

Furthermore, the rising IoT deployments and increasing demand for connected devices are expected to drive the market. The latest IoT Analytics "State of IoT-Spring 2023" report presents that the number of global IoT connections grew by 18% in 2022 to 14.3 billion active IoT endpoints.

In 2023, the global number of connected IoT devices grew by 16% to 16.7 billion active endpoints. While 2023 growth was slightly lower than in 2022, IoT device connections are expected to continue to grow for many years. In addition, ownership of connected devices in the Asia-Pacific region is already high among those living in China, Thailand, and Vietnam.

Asia Pacific Region is Expected to Witness Significant Growth

With the rapid development of China's electronics industry, many Chinese PCB manufacturers have emerged as leading players in the global PCB market, capturing a market share in the Asia-Pacific region. These manufacturers offer a wide range of services and capabilities, including PCB design, fabrication, and assembly, with competitive pricing and fast turnaround times. They include JLCPCB, Graperain, Fulltronics, YMS PCB Assembly, and Hitech Circuits.

At present, there are about 2,500 PCB manufacturers in mainland China. The PCB industry in China is mainly distributed in the Pearl River Delta, the Yangtze River Delta, and the Bohai Rim, where they centralize the large component markets, good transportation conditions, and water and electricity conditions.

Major reasons driving the growth of the PCB market in the Chinese region include lower overall cost and higher management efficiency. First, although China's demographic dividend is ending, labor costs are still lower than those of Japan, South Korea, and Taiwan and even lower than those of Europe and the United States. Second, China's environmental protection, trade unions, and welfare sectors are relatively low-cost.

In addition, as the world's largest manufacturing country, China's PCB industry has a complete industrial chain from copper foil, glass fiber, resin, copper-clad laminates, and PCBs. PCB is close to the final products, and a great number of electronics are also finished in China.

Benefiting from the transfer of global PCB production capacity to China and the vigorous development of downstream electronic terminal products, China's PCB industry shows a rapid development trend. The electronic information industry is a strategic, essential, and leading pillar industry for China's key development. The PCB industry, as the cornerstone of the development of the electronic information industry, has become one of the projects encouraged by China.

Furthermore, empirical data from reputable industry associations underscores Taiwan's continued dominance in global PCB production values, with a major market share. Notably, South Korean PCB manufacturers have surpassed their Japanese counterparts, securing the third position on a regional scale.

PCB Industry Overview

The PCB market is highly fragmented due to the presence of both global players and small and medium-sized enterprises. Some of the major players in the market are Jabil Inc., Wurth Elektronik Group (Wurth group), TTM Technologies Inc., Becker & Muller Schaltungsdruck Gmbh, and Advanced Circuits Inc. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

April 2024 - TTM Technologies Inc., a global manufacturer of technology solutions such as radio frequency ("RF") components and advanced printed circuit boards, opened its first manufacturing plant in Penang, Malaysia, with an investment of USD 200 million. According to the company, the new facility is built in Penang Science Park and has highly advanced and automated PCB manufacturing capabilities.

November 2023 - Jabil Inc. opened its third production facility in Chihuahua, Mexico, marking a milestone in its continued growth and commitment to the region. The plant spans more than 250,000 square feet. This expansion will be critical in supporting customers across the energy, automotive and transportation, healthcare, digital print, and retail industries. This new facility will enhance operational efficiency, flexibility, and the ability to deliver high-quality products.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitute Products

4.2.5 Intensity of Competitive Rivalry

4.3 Industry Value Chain Analysis

4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Rising Demand for Miniaturization of Technology

5.1.2 Increasing Demand from End-user Industries

5.2 Market Restraints

5.2.1 Growing Concern Regarding Electronic Waste

6 MARKET SEGMENTATION

6.1 By Product Type

6.1.1 Standard Multilayer PCBs

6.1.2 Rigid 1-2 Sided PCBs

6.1.3 HDI/Micro-via/Build-up

6.1.4 Flexible PCBs

6.1.5 Rigid-flex PCBs

6.1.6 Others

6.2 By End-user Industry

6.2.1 Industrial Electronics

6.2.2 Healthcare

6.2.3 Aerospace and Defense

6.2.4 Automotive

6.2.5 Consumer Electronics

6.2.6 Other End-user Industries

6.3 By Geography

6.3.1 North America

6.3.2 Europe

6.3.3 Asia

6.3.4 Australia and New Zealand

6.3.5 Latin America

6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

7.1 Company Profiles

7.1.1 Jabil Inc.

7.1.2 Wurth elektronik group (Wurth group)

7.1.3 TTM Technologies Inc.

7.1.4 Becker & Muller Schaltungsdruck Gmbh

7.1.5 Advanced Circuits Inc.

7.1.6 Sumitomo Electric Industries Ltd (Sumitomo Corporation)

7.1.7 Murrietta Circuits

7.1.8 Unimicron Technology Corporation

7.1.9 Tripod Technology Corporation

7.1.10 AT&S Austria Technologie & Systemtechnik AG