남미의 화물 및 물류 시장 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

South America Freight And Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1687076

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

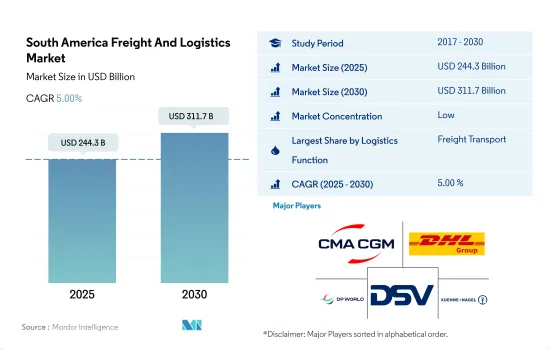

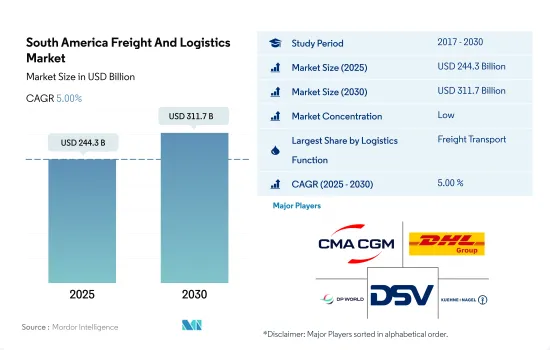

남미의 화물 및 물류 시장 규모는 2025년에 2,443억 달러로 추정되고, 2030년에는 3,117억 달러에 이를 것으로 예측되며, 예측 기간인 2025-2030년 CAGR 5.00%로 성장할 전망입니다.

전자상거래 산업과 인프라 투자, 이 지역의 화물 운송 시장 개척

브라질은 2024-2026년 신규 철도 및 고속도로 프로젝트에 약 1,800억 BRL(340억 3,000만 달러)의 민간투자를 유치하는 목표를 내걸고 있습니다. 이 움직임은 브라질의 도로 인프라를 현대화하고 확대하여 장거리 트럭 수송 능력을 강화하기 위한 광범위한 노력의 일환입니다. 주목할 만한 움직임으로 남북 아메리카 개발 은행(IDB)은 상파울루 주 고속도로 투자 프로그램에 대해 2023년에 4억 8,000만 달러의 융자를 승인했습니다. 이 이니셔티브는 동 주의 생산 체인 강화, 생산 능력 향상, 지역 통합의 촉진을 목적으로 하고 있습니다. 브라질은 2026년까지 620억 달러의 고속도로 투자를 확보하는 것을 목표로 하고 있습니다.

남미에서의 전자상거래의 급성장은 운송서비스 수요에 박차를 가하고 있습니다. 2023년에는 이 지역전자상거래 부문 매출이 583억 8,000만 달러에 달했으며, 2022년 517억 9,000만 달러에서 크게 증가했습니다. 예측에 따르면 2023-2027년 CAGR 13.50%로 성장할 전망이며, 2027년까지 수익은 968억 7,000만 달러에 이를 전망입니다. 사용자 기반도 확대되어 2025년에는 2억 4,410만 명에 이를 것이라는 기본 추정이 있습니다. 2022년 사용자 보급률은 54.0%로 2025년에는 58.7%까지 상승할 것으로 예측되고 있습니다.

남미의 화물 및 물류 성장과 변천

브라질은 아르헨티나, 칠레, 콜롬비아, 페루와 함께이 지역의 주요 경제 국가 중 하나입니다. 브라질은 지속가능한 수송을 목표로 트럭 차량에 클린 기술을 채용하고 있습니다. 예를 들어 Anheuser-Busch InBev가 소유한 브라질 양조회사 암베브는 전기 트럭 공급업체인 FNM과 협력해 2023년 말까지 약 1,000대의 전기 트럭을 도입했습니다. 브라질은 광업의 전기 트럭 채택을 보여주었습니다. 예를 들어, 2022년 10월, Vale는 미나스 제라이스 주의 아구아 림프에서 72톤의 오프하이웨이 트랙을 테스트한다고 발표했습니다. 이러한 중요한 기술 혁신 및 복수 분야에 걸친 화물 수송 수요의 증대를 가져왔습니다.

아르헨티나에서는 2023년 9월에 DHL Express가 마이애미와 부에노스아이레스를 연결하는 새로운 화물편을 취항하여 배송 효율성 향상을 도모했습니다. 이 항공편은 파나마의 DHL Aero Expreso가 관리하며 52톤의 적재 능력을 갖춘 B767-300 화물기를 사용합니다. 운항은 주 6편으로 마이애미 국제공항(MIA)에서 칠레의 산티아고(SCL)를 통해 부에노스아이레스(EZE)까지 왕복합니다. 이 노력을 통해 아르헨티나 도착 당일 통관을 10% 가속화하고 당일 배송을 50% 늘리는 것을 목표로 하고 있습니다.

남미의 화물 및 물류 시장 동향

남미 국가는 운송 부문을 개선하기 위해 인프라 개발에 많은 투자를 하고 있습니다.

2024년 6월, 아르헨티나 연방 정부는 914개 인프라 프로젝트를 주 당국으로 이관하여 주에 엄격한 재정적 과제가 발생했습니다. 유틸리티의 재개를 희망하고 있음에도 불구하고 주는 주요 수입원인 연방정부로부터 교부금의 상당한 삭감에 직면하고 있습니다. 주로의 연방세 이전액(CFI)은 2024년 6월에 전년 동월 대비 20% 감소하여, 2024년 6개월 중 5개월로 2자리 감소가 되었습니다. 기타 연방정부 이전(RON)도 6월 24.1% 감소했습니다.

2023년 브라질 정부는 고속도로, 철도, 항만, 공항 등 인프라 물류에 25억 9,000만 달러를 할당했습니다. 그 대부분 24억 2,000만 달러가 고속도로에 투입되었고, 철도는 3,025만 달러로 겸손한 배분이었습니다. 앞으로 정부는 2024년 6월까지 공공 부문과 민간부문의 자금을 결합하여 화물철도 프로젝트에 대한 투자를 확대하기 위한 대규모 국가 이니셔티브를 시작할 예정입니다. 야심찬 비전을 바탕으로 정부는 이 철도 프로젝트에 40억 달러를 투입할 예정입니다.

러시아와 우크라이나 전쟁이 세계 원유 가격에 미치는 영향으로 이 지역의 원유 가격이 크게 상승했습니다.

2024년 3월 계절 변동과 경기 감속의 징후로 브라질의 디젤 수요가 감소했습니다. 페트로브라스가 경유 가격 인하를 결정한 데다 바이오디젤 혼합률을 12%에서 14%로 의무화한 것도 기존 화석 경유 수요 감소에 박차를 가했다. 국내 시장은 세계 유가 변동과 이를 안정시키려는 정부의 노력에도 좌우되었습니다. 수중에 320만 배럴의 러시아산 경유가 과다하게 있었음에도 불구하고 브라질은 완전히 출하를 정지하지 않고 출하를 유지했습니다.

칠레는 2030년까지 지속 가능한 항공 연료(SAF)의 대규모 생산을 시작할 계획으로 2050년까지 항공 연료 수요의 절반을 유지, 생물학적 및 도시 폐기물 유래의 바이오연료로 충당하는 것을 목표로 하고 있습니다. 2040년까지 항공 교통량이 배증할 것으로 예측되는 가운데, 칠레는 SAF를 탈탄소화 전략에 있어서 지극히 중요한 요소로 생각하고 있습니다. 게다가 SAF는 기존 제트 연료와 혼합함으로써 엔진 개조 없이 배출가스를 최대 80% 줄일 수 있습니다. SAF는 칠레가 목표로 하는 탄소 배출 감축량의 절반 이상에 기여하고, 이 나라의 넷제로 목표에 있어 중요한 역할을 할 것으로 기대되고 있습니다.

남미의 화물 및 물류 산업 개요

남미의 화물 및 물류 시장은 세분화되어 있으며, CMA CGM Group(CEVA Logistics 포함), DHL Group, DP World, DSV A/S(De Sammensluttede Vognmaend af Air and Sea), Kuehne Nagel이 주요 5개사가 되고 있습니다.(알파벳순 정렬)

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 주요 요약 및 주요 조사 결과

제2장 보고서 제안

제3장 서문

조사 전제조건 및 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

인구동태

경제 활동별 GDP 분포

경제 활동별 GDP 성장률

인플레이션율

경제성과 및 프로파일

전자상거래 산업의 동향

제조업의 동향

운수 및 창고업의 GDP

수출 동향

수입 동향

연료 가격

트럭 운송 비용

유형별 트럭 보유 대수

물류 실적

주요 트럭 공급업체

모달 점유율

해상화물 운송 능력

정기선의 접속성

기항지 및 퍼포먼스

운임 동향

화물 톤수의 동향

인프라

규제 프레임워크(도로 및 철도)

아르헨티나

브라질

칠레

규제 프레임워크(해상 및 항공)

아르헨티나

브라질

칠레

밸류체인 및 유통채널 분석

제5장 시장 세분화

최종 사용자 산업별

농업, 어업 및 임업

건설업

제조업

석유 및 가스, 광업, 채석업

도매 및 소매업

기타

물류 기능별

쿨리에, 익스프레스 및 소포(CEP)

목적지별

국내

국제

화물 수송

수송 모드별

항공

해상 및 내륙 수로

기타

화물 수송

수송 수단별

항공

파이프라인

철도

도로

해상 및 내륙 수로

창고 보관

온도 관리

온도관리 없음

온도 관리

기타

국가별

아르헨티나

브라질

칠레

기타 남미

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

Agunsa

Alonso Group

Americold

CMA CGM Group(CEVA Logistics 포함)

Deutsche Bahn AG(DB Schenker 포함)

DHL Group

DP World

DSV A/S(De Sammensluttede Vognmaend af Air and Sea)

Kuehne Nagel

Romeu

SAAM

TASA Logistica

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Porter's Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(시장 성장 촉진요인, 억제요인 및 기회)

기술의 진보

정보원 및 참고문헌

도표 목록

주요 인사이트

데이터 팩

용어집

환율

AJY

영문 목차

영문목차

The South America Freight And Logistics Market size is estimated at 244.3 billion USD in 2025, and is expected to reach 311.7 billion USD by 2030, growing at a CAGR of 5.00% during the forecast period (2025-2030).

E-commerce industry and infrastructure investments, developing the freight transport market in the region

Brazil has set a target of attracting around BRL 180 billion (USD 34.03 billion) in private investments for new rail and highway projects from 2024 to 2026. This move is part of Brazil's broader efforts to modernize and expand its road infrastructure, which would bolster its long-haul trucking capabilities. In a notable development, the Inter-American Development Bank (IDB) sanctioned a USD 480 million loan in 2023 for the State of Sao Paulo Highway Investment Program. The initiative aims to enhance the state's production chains, improve production capacity, and foster regional integration. Brazil has set its sights on securing USD 62 billion in highway investments by 2026.

The rapid growth of e-commerce in South America is fueling the demand for transportation services. In 2023, the region's e-commerce sector generated revenues of USD 58.38 billion, marking a significant increase from USD 51.79 billion in 2022. Projections indicate a CAGR of 13.50% from 2023 to 2027, with revenues expected to reach USD 96.87 billion by 2027. The user base is also set to expand, with estimates pegging it at 244.1 million by 2025. In 2022, the user penetration rate stood at 54.0%, and it is projected to rise to 58.7% by 2025.

Growth and transition in South America's freight and logistics

Brazil is one of the major economies in the region, along with Argentina, Chile, Colombia, and Peru. Brazil is working toward sustainable transport and adopting clean technologies for truck fleets. For instance, Ambev, a Brazilian brewing company owned by Anheuser-Busch InBev, collaborated with electric truck supplier FNM to receive around 1,000 electric trucks by the end of 2023. Brazil witnessed the adoption of electric trucks in mining. For instance, in October 2022, Vale announced testing 72-tonne off-highway trucks at Agua Limpa in Minas Gerais. These significant technological innovations and growing demand for freight transport across several sectors.

In Argentina, in September 2023, DHL Express launched new freighter flights between Miami and Buenos Aires to improve delivery efficiency. These flights, managed by DHL Aero Expreso in Panama, use a B767-300 freighter with a 52-ton capacity. Operating six times weekly, the service goes from Miami International Airport (MIA) to Buenos Aires (EZE) via Santiago, Chile (SCL), and back. This initiative aims to speed up customs clearance in Argentina by 10% on the same day as arrival and increase same-day deliveries by 50%.

South America Freight And Logistics Market Trends

South American countries are investing heavily in infrastructure development to improve the transportation sector

In June 2024, Argentina's federal government transferred 914 infrastructure projects to provincial authorities, creating a tough financial challenge for the provinces. Despite wanting to resume public works, provinces have faced deep cuts to federal transfers, their main source of income. Federal tax transfers (CFI) to provinces dropped 20% YoY in June 2024 and have decreased by double digits in five out of the six months of 2024. Other federal transfers (RON) also fell 24.1% in June.

In 2023, the Brazilian government allocated USD 2.59 billion to infrastructure logistics, encompassing highways, railways, ports, and airports. A significant portion, approximately USD 2.42 billion, was funneled into highways, while railways received a modest allocation of USD 30.25 million. Looking ahead, by June 2024, the government is set to launch a major national initiative aimed at amplifying investments in freight rail projects, leveraging a blend of public and private sector funding. With an ambitious vision, the government plans to inject a substantial USD 4 billion into these rail projects.

Crude oil prices in the region rose significantly owing to the impact of the Russia-Ukraine War on global crude oil

In March 2024, seasonal fluctuations and signs of an economic slowdown led to a decline in Diesel demand in Brazil. Petrobras' decision to reduce Diesel prices, coupled with the mandated increase in biodiesel blending from 12% to 14%, further fueled this drop in demand for conventional fossil Diesel. The domestic market was also swayed by global fluctuations in crude oil prices and government efforts to stabilize them. Even with an excess of 3.2 million barrels of Russian Diesel on hand, Brazil maintained its shipments without a complete halt.

By 2030, Chile plans to launch large-scale production of sustainable aviation fuel (SAF) and aims for these biofuel sources derived from oils, fats, and both biological and municipal waste to satisfy half of its aviation fuel needs by 2050. With projections of air traffic doubling by 2040, Chile views SAF as a pivotal element in its decarbonization strategy. Moreover, SAF can be blended with traditional jet fuel to reduce emissions by up to 80% without engine modifications. It is expected to contribute over half of Chile's targeted carbon emissions reductions, playing a key role in the country's net-zero goals.

South America Freight And Logistics Industry Overview

The South America Freight And Logistics Market is fragmented, with the major five players in this market being CMA CGM Group (including CEVA Logistics), DHL Group, DP World, DSV A/S (De Sammensluttede Vognmaend af Air and Sea) and Kuehne+Nagel (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Demographics

4.2 GDP Distribution By Economic Activity

4.3 GDP Growth By Economic Activity

4.4 Inflation

4.5 Economic Performance And Profile

4.5.1 Trends in E-Commerce Industry

4.5.2 Trends in Manufacturing Industry

4.6 Transport And Storage Sector GDP

4.7 Export Trends

4.8 Import Trends

4.9 Fuel Price

4.10 Trucking Operational Costs

4.11 Trucking Fleet Size By Type

4.12 Logistics Performance

4.13 Major Truck Suppliers

4.14 Modal Share

4.15 Maritime Fleet Load Carrying Capacity

4.16 Liner Shipping Connectivity

4.17 Port Calls And Performance

4.18 Freight Pricing Trends

4.19 Freight Tonnage Trends

4.20 Infrastructure

4.21 Regulatory Framework (Road and Rail)

4.21.1 Argentina

4.21.2 Brazil

4.21.3 Chile

4.22 Regulatory Framework (Sea and Air)

4.22.1 Argentina

4.22.2 Brazil

4.22.3 Chile

4.23 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes 1. Market value in USD for all segments 2. Market volume for select segments viz. freight transport, CEP (courier, express, and parcel) and warehousing & storage 3. Forecasts up to 2030 and analysis of growth prospects)

5.1 End User Industry

5.1.1 Agriculture, Fishing, and Forestry

5.1.2 Construction

5.1.3 Manufacturing

5.1.4 Oil and Gas, Mining and Quarrying

5.1.5 Wholesale and Retail Trade

5.1.6 Others

5.2 Logistics Function

5.2.1 Courier, Express, and Parcel (CEP)

5.2.1.1 By Destination Type

5.2.1.1.1 Domestic

5.2.1.1.2 International

5.2.2 Freight Forwarding

5.2.2.1 By Mode Of Transport

5.2.2.1.1 Air

5.2.2.1.2 Sea and Inland Waterways

5.2.2.1.3 Others

5.2.3 Freight Transport

5.2.3.1 By Mode Of Transport

5.2.3.1.1 Air

5.2.3.1.2 Pipelines

5.2.3.1.3 Rail

5.2.3.1.4 Road

5.2.3.1.5 Sea and Inland Waterways

5.2.4 Warehousing and Storage

5.2.4.1 By Temperature Control

5.2.4.1.1 Non-Temperature Controlled

5.2.4.1.2 Temperature Controlled

5.2.5 Other Services

5.3 Country

5.3.1 Argentina

5.3.2 Brazil

5.3.3 Chile

5.3.4 Rest of South America

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

6.4.1 Agunsa

6.4.2 Alonso Group

6.4.3 Americold

6.4.4 CMA CGM Group (including CEVA Logistics)

6.4.5 Deutsche Bahn AG (including DB Schenker)

6.4.6 DHL Group

6.4.7 DP World

6.4.8 DSV A/S (De Sammensluttede Vognmaend af Air and Sea)

6.4.9 Kuehne+Nagel

6.4.10 Romeu

6.4.11 SAAM

6.4.12 TASA Logistica

7 KEY STRATEGIC QUESTIONS FOR FREIGHT AND LOGISTICS CEOS