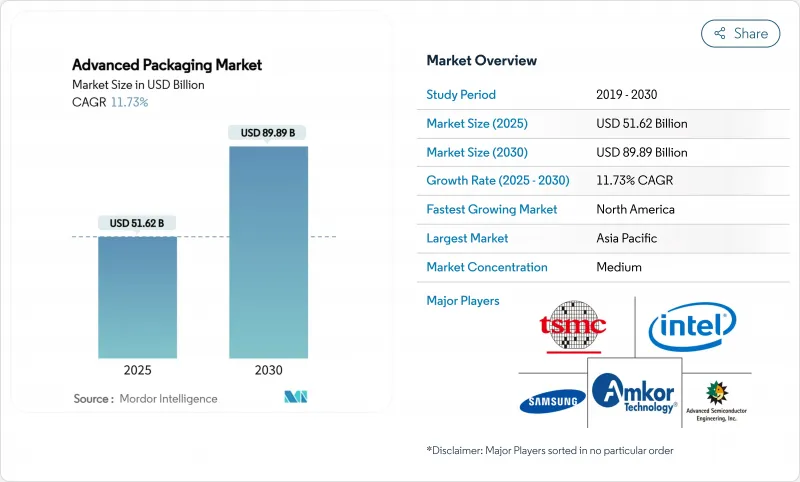

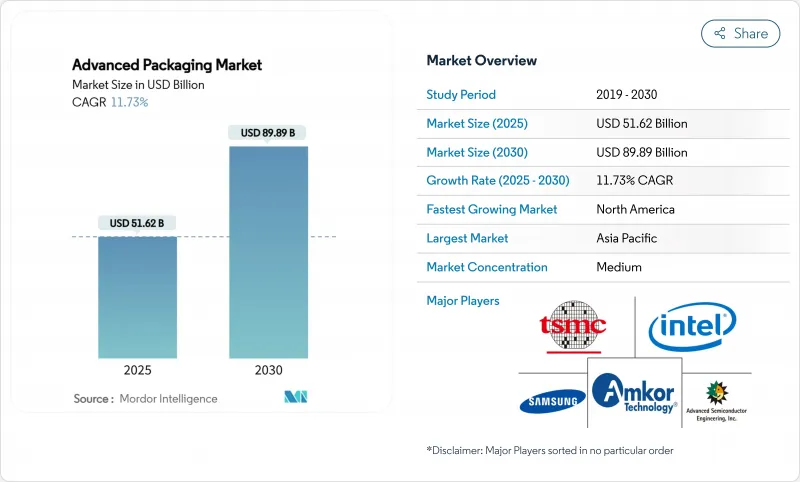

첨단 패키징 시장 규모는 2025년 516억 2,000만 달러로 추정되고, CAGR 11.73%로 확대될 전망이며, 2030년에는 898억 9,000만 달러에 이를 것으로 예측됩니다.

기존의 패키지에서는 열과 상호 연결의 한계를 넘는 인공지능(AI) 프로세서에 이기종 집적이 불가결해졌기 때문에 수요는 이전의 예측을 웃돌았습니다. 이에 따라 집적 디바이스 제조업체(IDMs)와 반도체 조립 및 테스트 아웃소싱(OSAT) 제공업체는 설비 투자를 가속화하면서 정부는 조립 능력을 현지화하기 위해 상당한 장려금을 계상했습니다. 첨단 패키징 시장은 또한 유리 코어 기판의 연구 개발, 패널 레벨 프로세싱의 테스트 운영, 하이퍼스케일 데이터센터에서의 코패키지 광학 부품의 급속한 채용으로부터 혜택을 받았습니다. 그러나 BT 레진기판 부족과 엔지니어 인력 부족은 적시에 생산 능력 증강을 방해해 공급은 여전히 핍박받고 있습니다. AI 공급망을 엔드 투 엔드로 관리하기 위해 주조 업체가 패키징을 내제화하고 기존 OSAT의 마진이 압박되어 전략적인 전문화가 촉진되어 경쟁이 격화되었습니다.

AI 워크로드는 기존의 패키징으로는 실현할 수 없었던 계산 밀도 및 메모리 대역폭이 필요합니다. TSMC의 CoWoS 플랫폼은 칩렛과 고대역폭 메모리를 단일 구조로 통합하여 주요 AI 가속기 공급업체 간에 빠르게 채택되고 있습니다. 삼성 SAINT 기술은 하이브리드 본딩을 사용하여 유사한 목표를 달성하고 향후 예정된 HBM4 스택을 지원함으로써 사내 첨단 패키징의 전략적 가치를 강조합니다. 열 인터페이스 재료, 특수 기판, 액티브 인터포저는 패키지 비용을 반도체 전체의 15-20%로 끌어올려 주류 CPU의 5-8%에서 상승시켰습니다. 그 결과, 첨단 패키징의 용량은 AI 시스템 시장 출시까지의 시간을 결정하는 데 있어서 최첨단 팹과 마찬가지로 매우 중요하게 되었습니다. 따라서 첨단 패키징 시장은 이전 단계의 전환을 늦추지 않고 오히려 연동하여 성장했습니다.

스마트폰, 웨어러블 단말기, 히어러블 단말기에서는 박형화 및 기능 밀도 향상이 항상 요구되고 있습니다. 팬아웃 웨이퍼 레벨 패키징(FOWLP)은 0.5mm 이하의 초박형 패키지에 여러 다이를 내장할 수 있어 열 성능을 저하시키지 않으면서 플래그쉽 모바일 프로세서를 지원합니다. 팬인 WLP에서 FOWLP로의 전환으로 인해 언더필, 와이어 본딩 및 라미네이트 기판이 더 이상 필요하지 않아 전체 시스템 비용이 최대 25% 절감되었습니다. 소형화는 또한 치수가 생명에 관련된 임베디드 의료용 전자기기로 진행되어 리드리스 페이스메이커는 WLP의 혜택을 받아 엄격한 신뢰성 목표를 충족하면서 디바이스 사이즈를 93% 삭감했습니다. 그 결과, 소비자 수요와 의료 수요는 PC 최종 시장의 주기적 변동으로부터 첨단 패키징 시장을 격리하는 경상적인 기준선을 만들었습니다.

2.5D 및 3D 프로세스용 툴링에는 챔버당 1,000만-1,500만 달러의 비용이 들고, 레거시 라인의 일반적인 300만 달러를 크게 웃돕니다. TSMC는 2025년 자본 지출에 420억 달러를 예산으로 기록하고 있으며, 그 중 중요한 점유율은 첨단 패키징 확장을 목표로 하고 있습니다. 따라서 소규모 OSAT는 급격히 축소되는 제품 수명주기에 걸쳐 투자를 상각하는 데 어려움을 겪어 틈새 전문화 및 방위적 합병을 촉구했습니다. 높은 장애율은 Tier One 공급자와 지역 추종자 간의 기술 격차를 넓혀 2024-2026년 첨단 패키징 시장에서 새로운 생산 능력을 감쇠시켰습니다.

플립칩 패키지는 2024년 매출액 49.0%로 선두를 유지했으며, 대량 생산되는 소비자용 및 산업 용도에 지지를 받고 있습니다. 그러나 2.5D/3D 구성은 AI 가속기가 플립 칩 한계를 초과하는 로직 메모리 간의 근접성을 요구하기 때문에 13.2%의 연평균 복합 성장률(CAGR) 전망을 달성하여 가장 빠른 성장을 보였습니다. 2.5D/3D 솔루션의 첨단 패키징 시장 규모는 2030년까지 341억 달러에 이를 전망이며, 전체 플랫폼 수익의 38%에 해당할 것으로 예측됩니다.

삼성의 SAINT 플랫폼은 10마이크로미터 이하의 하이브리드 본드를 달성했으며, 와이어 본드 스택에 비해 신호 대기 시간을 30% 줄이고, 열 헤드룸을 40% 확대했습니다. TSMC의 CoWoS는 2025년에 3개의 라인을 증설해 12개월의 백로그를 클리어했습니다. 임베디드 패키지는 공간에 제약이 있는 차량 탑재 영역에 적합하며, FOWLP(Fan-Out WLP)는 5G 기지국 및 mm 파 레이더 설계에 적합합니다. 이러한 역학을 종합하면 2.5D/3D 패키징이 차세대 디바이스의 로드맵 중심에 통합되어 첨단 패키징 시장에서 주요 가치 드라이버로서의 역할을 보장했습니다.

소비자용 전자기기는 2024년 출하의 40.0%를 흡수했지만, 그 성장은 1자리대에 정체했습니다. 이와는 대조적으로 자동차와 EV 수요는 CAGR 12.4%로 확대되어, 2030년까지 첨단 패키징 시장 점유율을 18%로 끌어올릴 것으로 예측되고 있습니다. 차량용 전자 제품의 첨단 패키징 시장 규모는 예측 기간 말까지 160억 달러 이상에 달할 것으로 예측됩니다.

EV 트랙션 인버터, 온보드 충전기 및 도메인 컨트롤러는 현재 자동차 등급 팬아웃, 더블 사이드 냉각 전원 모듈 및 오버몰드 시스템 인 패키지(SiP) 어셈블리를 지정합니다. 데이터센터 인프라스트럭처는 또 다른 고성장 틈새 분야가 되었습니다. AI 서버는 전력 밀도가 1,000W/cm2에 이르는 첨단 패키징을 이용하고 있으며, 혁신적인 서멀 리드와 언더필 케미스트리가 필요합니다. 반면 건강 관리는 생체 적합성 코팅과 밀폐형 인클로저를 필요로 하며, 그 특성으로 인해 평균 판매 가격이 비싸고 안정적인 교체 수요가 있습니다. 이러한 부문 동향은 수익원을 다양화하고 첨단 패키징 시장의 주기적인 스마트폰 리프레시 사이클에 대한 의존도를 줄이고 있습니다.

첨단 패키징 시장은 패키징 플랫폼별(플립칩, 임베디드 다이, 팬인 WLP 등), 최종 사용자 산업별(컨슈머 일렉트로닉스, 자동차 및 EV, 데이터센터 및 HPC 등), 디바이스 아키텍처별(2D IC, 2.5D 인터포저, 3D IC), 상호 연결 기술별(솔더 범프, 구리 기둥, 하이브리드 본드), 지역별(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)로 구분됩니다.

아시아태평양은 대만, 한국, 중국 본토가 프론트엔드 공장과 기판 공급업체의 대부분을 차지하기 때문에 2024년 매출의 75.0%를 창출했습니다. TSMC는 1,650억 달러의 미국 투자를 발표했는데, 이는 대만 기지 이전이 아닌 다각화 전략을 반영한 것이며, 아시아가 중기적으로 리더십을 유지할 수 있도록 보장합니다. 중국 국내 OSAT는 매출이 2자리 성장을 보이고 자동차 포장에도 진출했지만 극단 자외선(EUV) 툴의 규제가 엄격하여 최첨단 웨이퍼 팹 프로세스로의 진출은 제한되었습니다.

북미는 CHIPS법의 우대 조치로 CAGR 12.5%의 급성장 지역으로 부상했습니다. Amkor의 20억 달러 규모의 애리조나 거점은 2027년 전면 가동되면 범프, 웨이퍼 레벨, 패널 레벨 라인을 통합하고 미국 시스템 통합자 근처에서 최초의 대규모 아웃소싱 옵션을 제공할 예정입니다. 인텔, 애플, 엔비디아는 지정학적 공급 중단의 위험을 피하기 위해 이 생산 능력의 일부를 사전에 예약하고 지금까지 동아시아의 OSAT로 흐르고 있던 중요한 생산량을 전환했습니다. 그 결과 첨단 패키징 시장은 대량의 AI 제품을 지원할 수 있는 신뢰할 수 있는 북미 공급 노드를 포함하게 되었습니다.

onsemi의 체코 거점은 차량 탑재 전원용 실리콘 카바이드 디바이스에 임해, 현지 OEM의 전동화 목표에 합치했습니다. 독일의 프라운호퍼 연구기구는 패널 수준의 연구를 주도했지만, 제조업체 각사는 그린필드의 메가사이트 헌신에 신중했습니다. 한편, 싱가포르는 허브의 역할을 강화했습니다. 마이크론의 HBM 공장과 KLA의 공정 제어 확장으로 AI 메모리와 측정을 하나의 관할하에 지원하는 수직적으로 일관된 생태계가 구축되었습니다. 인도에서는 50%의 자본 비용 부담 체계가 도입되어 중기적인 업사이드가 기대되는 반면, 인재 확보 나름이지만 첨단 패키징 파일럿의 제안이 모였습니다.

이러한 개척은 시스템 OEM의 지리적 위험을 분산시키고 첨단 패키징 시장의 균형을 조정했습니다. 그럼에도 아시아태평양은 2030년에 60% 이상의 점유율을 유지할 것으로 예측됩니다. 이는 기존 인프라, 공급 클러스터 및 규모의 경제가 여전히 신규 진출기업을 능가하기 때문입니다.

The advanced packaging market size was valued at USD 51.62 billion in 2025 and is forecast to expand at an 11.73% CAGR to reach USD 89.89 billion by 2030.

Demand outpaced earlier projections because heterogeneous integration became indispensable for artificial-intelligence (AI) processors that exceed the thermal and interconnect limits of conventional packages. In response, integrated-device manufacturers (IDMs) and outsourced semiconductor assembly and test (OSAT) providers accelerated capital spending, while governments earmarked large incentives to localize assembly capacity. The advanced packaging market also benefited from glass-core substrate R&D, panel-level processing pilots, and the rapid adoption of co-packaged optics in hyperscale data centers. Supply remained tight, however, as BT-resin substrate shortages and scarce engineering talent hindered timely capacity additions. Competitive intensity rose as foundries internalized packaging to secure end-to-end control of AI supply chains, squeezing traditional OSAT margins and prompting strategic specialization.

AI workloads require compute density and memory bandwidth unattainable with legacy packaging. TSMC's CoWoS platform integrates chiplets and high-bandwidth memory in a single structure, gaining rapid adoption among leading AI accelerator vendors. Samsung's SAINT technology achieved similar objectives using hybrid bonding that supports forthcoming HBM4 stacks, underscoring the strategic value of in-house advanced packaging. Thermal interface materials, specialized substrates, and active interposers raised package cost to 15-20% of the total semiconductor build-to-materials, up from 5-8% for mainstream CPUs. As a result, advanced packaging capacity became as critical as leading-edge fabs in determining time-to-market for AI systems. The advanced packaging market, therefore, grew in tandem with, rather than lagging, front-end process migrations.

Smartphones, wearables, and hearables consistently demand thinner profiles and higher functional density. Fan-out wafer-level packaging (FOWLP) enables multiple dies to be embedded in ultra-thin packages below 0.5 mm, supporting flagship mobile processors without compromising thermal performance. The shift from fan-in WLP to FOWLP reduced overall system cost by up to 25% because under-fill, wire-bonding, and laminate substrates were eliminated. Miniaturization also moved into implantable medical electronics, where dimensions are life-critical; leadless pacemakers benefited from WLP to cut device size by 93% while meeting stringent reliability targets. Consequently, consumer and medical demand created a recurring baseline that insulated the advanced packaging market from cyclical swings in PC end-markets.

Tooling for 2.5D and 3D processes can cost USD 10-15 million per chamber, vastly exceeding the USD 3 million typical for legacy lines. TSMC budgeted USD 42 billion in 2025 capital outlays, of which a material share targeted advanced packaging expansions. Smaller OSATs, therefore, struggled to amortize investments across rapidly shrinking product life cycles, prompting niche specialization or defensive mergers. The elevated hurdle rate widened the technological gap between tier-one providers and regional followers, dampening fresh capacity in the advanced packaging market during 2024-2026.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Flip-chip packages retained leadership with 49.0% revenue in 2024, anchored by high-volume consumer and industrial applications. Yet 2.5D/3D configurations delivered the fastest gains, achieving a 13.2% CAGR outlook as AI accelerators demanded logic-to-memory proximity beyond flip-chip limits. The advanced packaging market size for 2.5D/3D solutions is forecast to reach USD 34.1 billion by 2030, equal to 38% of total platform revenue.

Samsung's SAINT platform attained sub-10 µm hybrid bonds, reducing signal latency by 30% and extending thermal headroom by 40% relative to wire-bonded stacks. TSMC's CoWoS ramped three additional lines in 2025 to clear a 12-month backlog. Embedded-die and fan-out WLP progressed as complementary options: embedded packages suited space-constrained automotive domains, while fan-out WLP captured 5G base-station and mmWave radar designs. Collectively, these dynamics embedded 2.5D/3D packaging at the center of next-generation device roadmaps, guaranteeing its role as the prime value driver inside the advanced packaging market.

Consumer electronics absorbed 40.0% of 2024 shipments, but its growth plateaued at single digits. In contrast, automotive and EV demand is projected to expand at a 12.4% CAGR, lifting its share of the advanced packaging market to 18% by 2030. The advanced packaging market size for automotive electronics is estimated to surpass USD 16 billion by the end of the forecast period.

EV traction inverters, on-board chargers, and domain controllers now specify automotive-grade fan-out, double-side cooled power modules, and over-molded system-in-package (SiP) assemblies. Data-center infrastructure provided another high-growth niche: AI servers utilize advanced packages with power densities reaching 1,000 W/cm2, dictating innovative thermal lid and under-fill chemistries. Healthcare, meanwhile, requires biocompatible coatings and hermetic enclosures, attributes that carry premium average selling prices and stable replacement demand. Cumulatively, these segment trends diversified revenue streams and reduced dependence on cyclical smartphone refresh cycles within the advanced packaging market.

Advanced Packaging Market is Segmented by Packaging Platform (Flip-Chip, Embedded Die, Fan-In WLP, and More), End-User Industry (Consumer Electronics, Automotive and EV, Data Center and HPC, and More), Device Architecture (2D IC, 2. 5D Interposer, and 3D IC), Interconnect Technology (Solder Bump, Copper Pillar, and Hybrid Bond), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa).

Asia-Pacific generated 75.0% of 2024 revenue because Taiwan, South Korea, and mainland China house the bulk of front-end fabs and substrate suppliers. TSMC announced a USD 165 billion U.S. investment, reflecting a diversification strategy rather than the displacement of its Taiwan base, ensuring Asia retains leadership in the medium term. China's domestic OSATs delivered double-digit sales gains and expanded into automotive packaging, but tight controls on extreme-ultraviolet (EUV) tools limited their move into leading-edge wafer-fab processes.

North America emerged as the fastest-growing region at a 12.5% CAGR thanks to the CHIPS Act incentives. Amkor's USD 2 billion Arizona site will combine bump, wafer-level, and panel-level lines once fully ramped in 2027, providing the first large-scale outsourced option near U.S. system integrators. Intel, Apple, and NVIDIA pre-booked a portion of this capacity to de-risk geopolitical supply interruptions, redirecting meaningful volumes that historically flowed to East Asian OSATs. Consequently, the advanced packaging market now includes a credible North American supply node capable of high-volume AI product support.

Europe pursued specialization rather than volume leadership. onsemi's Czech facility addressed silicon-carbide devices for automotive power, aligning with local OEM electrification targets. Germany's Fraunhofer institutes led panel-level research, but manufacturers stayed cautious on green-field megasite commitments. Meanwhile, Singapore strengthened its hub role; Micron's HBM plant and KLA's process-control expansion created a vertically coherent ecosystem that supports AI memory and metrology under one jurisdiction. India introduced a 50% capital cost-sharing scheme, attracting proposals for advanced packaging pilots that promise medium-term upside yet remain contingent on talent availability.

Collectively, these developments diversified geographic risk for system OEMs and rebalanced the advanced packaging market. Even so, Asia-Pacific is forecast to maintain more than 60% share in 2030 because existing infrastructure, supply clusters, and economies of scale still surpass new regional entrants.