폴리우레탄 접착제 및 실란트 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

Polyurethane Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1641901

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

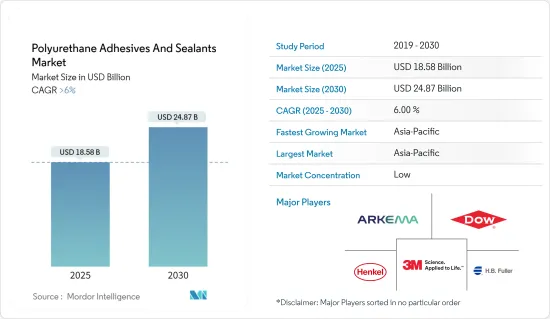

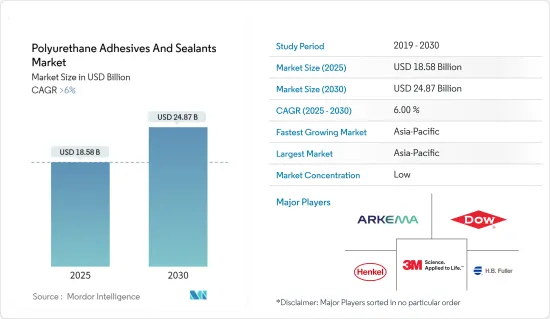

폴리우레탄 접착제 및 실란트 시장 규모는 2025년에 185억 8,000만 달러로 추정,예측되고, 2030년에는 248억 7,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2025-2030년)의 CAGR은 6%를 초과할 것으로 예측됩니다.

COVID-19 팬데믹은 세계의 폴리우레탄(PU) 접착제 및 실란트 시장에 큰 영향을 미쳤습니다. 봉쇄와 여행 제한은 원료와 완제품 공급망에 혼란을 일으켜 공급 부족과 가격 상승을 초래했습니다. 정부와 기업은 유행 기간 동안 의료 및 기타 필수적인 부문을 선호했으며, 이러한 제품에 크게 의존하는 건설, 자동차 및 기타 산업에 대한 투자 감소로 이어졌습니다. 그러나 시장은 COVID-19의 초기 영향에서 회복되었으며 장기적으로 완만한 속도로 성장을 계속하고 있습니다.

주요 하이라이트

아시아 지역에서는 도시화와 인프라 정비에 따른 건설활동 증가와 포장산업의 성장이 접착제 및 실란트 수요를 높일 것으로 예상됩니다.

그러나 휘발성 유기 화합물의 사용에 관한 정부의 엄격한 환경 규제가 시장 확대를 방해할 것으로 예상됩니다.

바이오 폴리우레탄(PU) 핫멜트 접착제에 대한 수요는 광범위한 PU 접착제 및 실란트 시장에서 꾸준히 증가하고 있으며, 세계 시장에 유리한 성장 기회를 창출할 것으로 예상됩니다.

아시아태평양은 가장 큰 시장이며 예측 기간 동안 가장 빠르게 성장하는 시장이 될 전망입니다. 이는 중국, 인도, ASEAN 국가의 소비 증가로 인한 것입니다.

폴리우레탄 접착제 및 실란트 시장 동향

건축 및 건설산업이 시장을 독점

접착제 및 실란트의 소비량이 가장 많은 것은 건설 부문입니다. 폴리우레탄 접착제 및 실란트는 탄성과 구조적 특성으로 인해 콘크리트, 목재, 플라스틱, 유리 등 많은 기판에 좋은 접착력을 발휘합니다. 지속적인 기술 진보와 함께 이러한 특성은 주택 건설에서 폴리 우레탄 접착제 및 실란트의 사용을 증가시키고 있습니다.

아시아태평양 건설 부문은 세계 최대입니다. 이 지역의 인구 증가, 중간 소득층 증가, 도시화로 인해이 부문은 견실한 성장률을 보여줍니다.

중국 정부는 14차 5개년 계획 기간 중(2021-2025년)에 건설 부문의 종합적인 개발 계획을 도입했습니다. 이 계획은 이 매우 중요한 산업을 보다 환경을 배려하고 기술적으로 선진적이고 안전한 궤도로 인도하는 것을 목표로 하고 있습니다. 주택,도시,농촌개발성이 정리한 가이드라인에 따르면 건설산업은 2025년 국내총생산(GDP)의 6%라는 공헌도를 유지할 전망입니다.

중국의 건설 부문은 세계 최대의 건설 산업이며 5,300만 명 이상을 고용하고 있습니다. 국가 통계국에 따르면 중국의 건설 부문 생산량은 2021년 29조 3,100억 위안(약 4조 2,900억 달러)에 비해 2022년에는 31조 2,000억 위안(약 4조 5,700억 달러)으로 6% 성장을 기록했습니다. 중국 건설 산업은 2022년 GDP에 약 6.9% 기여했습니다.

주택도시농촌개발부의 예측에 따르면 중국의 건설 부문은 2025년 이후에도 GDP의 6%를 유지할 것으로 예상되고 있습니다.

국제무역기구에 따르면 중국은 세계에서 가장 큰 건설시장으로 세계에서 가장 도시화율이 높습니다. 미국 건축가 협회(AIA) 상하이 지부의 데이터에 따르면 중국은 2025년까지 1990년대 이후 뉴욕의 10개분에 해당하는 도시를 건설할 것으로 예상됩니다.

중국은 2030년까지 약 13조 달러를 건축물에 투입할 것으로 예상되고 있으며, 시장에는 밝은 전망이 열리고 있습니다. 이 나라는 세계 최대의 건설 시장으로 전 세계 건설 투자의 20%를 차지합니다.

미국 인구조사에 따르면 북미에서는 2022년에 약 1조 7,929억 달러가 건설에 소요되었으며, 이는 2021년 연간 건설 지출액을 10% 초과하는 상당한 금액입니다. 이는 이 지역의 건축 및 건설이 상승 경향에 있음을 나타냅니다.

또한 Eurostat에 따르면 EU 부흥 기금의 새로운 투자로 2022년 유럽 건설 부문은 2.5% 성장했습니다. 2022년 주요 건설 프로젝트는 비주택 건설(사무실, 병원, 호텔, 학교, 산업용 건물)이 전체의 31.3%를 차지합니다.

이러한 것들은 향후 수년간은 폴리우레탄 접착제와 실란트를 구입하고 싶은 사람이 늘어날 것으로 예상됩니다.

아시아태평양이 시장을 독점

아시아태평양은 세계 시장을 독점하고 있습니다. 중국, 인도, 일본 등의 국가에서의 포장, 건설, 자동차, 의료 등의 산업에서의 수요 증가가 조사된 시장을 견인하고 있습니다.

중국은 현재 진행 중인 도시화 경향을 적극적으로 추진,유지하고 있으며, 2030년까지 70%의 도시화를 목표로 하고 있습니다. 그 결과 중국과 같은 국가에서 건설 활동이 활발해지면서 이 지역에서 접착제 산업의 성장을 가속할 것으로 예상됩니다. 이러한 요인은 전체적으로 지역 전체의 접착제 수요 증가에 기여합니다.

Invest India에 따르면 인도 건설 산업은 2025년까지 1조 4,000억 달러에 이를 것으로 예상되며, 인도 건설 산업은 섹터 간 협력과 PMAY-U의 기술 제출 하에 확인된 54개 이상의 세계 혁신적인 건설 기술로 250개 서브섹터에 걸쳐 작동하며 인도 건설 부문의 새로운 시대를 시작할 것으로 예상됩니다.

폴리우레탄(PU) 접착제 및 실란트는 신발 산업에서 신발의 내구성, 편안함, 미관을 보장하는데 중요한 역할을 합니다. 어퍼와 밑창 접착에서 솔기 씰, 장식품 장착까지 신발 제조의 다양한 단계에서 사용됩니다.

중국은 세계 최대 PU 소비국이며 세계 최대 신발 생산국이기도 합니다. 중국은 세계 최대의 양말 제조수출국이며 세계를 석권하고 있습니다. 중국은 2022년에 130억 켤레 이상의 신발과 부츠를 출하했습니다.

한편, 중국은 세계 최대의 자동차 생산,구매국입니다. OICA에 따르면 중국은 세계 최대의 자동차 생산 거점이며, 2022년의 자동차 총 생산 대수는 2,702만대로, 작년의 2,608만대에 비해 3% 증가했습니다.

따라서 이러한 시장 동향은 예측 기간 동안 이 지역의 접착제 및 실란트 시장의 성장에 큰 영향을 미칠 것으로 예상됩니다.

폴리우레탄 접착제 및 실란트 산업 개요

폴리우레탄 접착제 및 실란트 시장은 세분화되어 있습니다. 주요 기업(특정 순서 없음)으로는 3M, HB Fuller Company, Arkema(Bostik), Dow, Henkel AG&Co.KGaA 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 성과

조사의 전제

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

아시아 지역의 건설 산업 수요 증가

포장 산업의 성장

기타 촉진요인

억제요인

유해물질에 관한 규제 강화와 환경 문제

원료 가격의 변동

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 진입업자의 위협

대체품의 위협

경쟁도

제5장 시장 세분화(금액 베이스 시장 규모)

기술

물베이스

용제 베이스

핫멜트

기타 기술(바이오베이스, 나노 PU 접착제 등)

최종 사용자 산업

건축 및 건설

의료

자동차 및 운송

포장

양말 피혁

전기 및 전자

기타 최종 사용자 산업(목공·가구, 소비재 등)

지역

아시아태평양

중국

인도

일본

한국

인도네시아

말레이시아

태국

베트남

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

스페인

러시아

터키

북유럽 국가

기타 유럽

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

카타르

아랍에미리트(UAE)

이집트

알제리

기타 중동?아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

시장 점유율(%)**/랭킹 분석

주요 기업의 전략

기업 프로파일

3M

Arkema

Beijing Comens New materials Co. Ltd

Dow

HBFuller Company

Henkel AG & Co.KGaA

Hubei Huitian New Materials Co. Ltd

Huntsman International LLC

Jowat SE

Kangada New Materials(Group) Co. Ltd

MAPEI SpA

NANPAO RESINS CHEMICAL GROUP

Pidilite Industries Ltd

Sika AG

Soudal Holding NV

제7장 시장 기회와 앞으로의 동향

바이오베이스 PU 핫멜트 접착제에 대한 수요 증가

SHW

영문 목차

영문목차

The Polyurethane Adhesives And Sealants Market size is estimated at USD 18.58 billion in 2025, and is expected to reach USD 24.87 billion by 2030, at a CAGR of greater than 6% during the forecast period (2025-2030).

The COVID-19 pandemic had a significant impact on the global polyurethane (PU) adhesives and sealants market. Lockdowns and travel restrictions caused disruptions in the supply chain for raw materials and finished products, leading to shortages and price increases. Governments and businesses prioritized healthcare and other essential sectors during the pandemic, leading to reduced investment in construction, automotive, and other industries that rely heavily on these products. However, the market has recovered from the initial impact of COVID-19 and continues to grow at a moderate pace in the long run.

Key Highlights

Increased construction activities in the Asian region, driven by urbanization and infrastructure development, along with the growth in the packaging industry, are expected to propel the demand for adhesives and sealants.

However, strict environmental regulations set by the government on the use of volatile organic compounds are anticipated to hamper the expansion of the market studied.

The demand for bio-based polyurethane (PU) hot-melt adhesives is steadily rising within the broader PU adhesives and sealants market, which is expected to create lucrative growth opportunities in the global market.

The Asia-Pacific region represents the largest market and is also expected to be the fastest growing market over the forecast period. This is due to the increase in consumption from China, India, and ASEAN Countries.

Polyurethane Adhesives And Sealants Market Trends

Building and Construction Industry to Dominate the Market

The construction sector has the highest consumption of adhesives and sealants. Polyurethane adhesives and sealants offer good adhesion to numerous substrates, such as concrete, wood, plastic, and glass, due to their elasticity and structural properties. Together with ongoing technical advancement, these characteristics have increased the use of polyurethane adhesive and sealant in residential construction.

The construction sector in the Asia-Pacific region is the largest in the world. The sector is growing at a healthy rate due to the region's rising population, increase in middle-class incomes, and urbanization.

As per the Government of China, China introduced a comprehensive development blueprint for its construction sector during the 14th Five-Year Plan period (2021-2025). This plan aims to steer the pivotal industry towards a more environmentally responsible, technologically advanced, and safer trajectory. As per the guidelines outlined by the Ministry of Housing and Urban-Rural Development, the construction industry is expected to uphold its contribution at 6 percent of the nation's GDP through 2025.

China's construction sector is the largest construction industry in the world, employing more than 53 million people. According to the National Bureau of Statistics, the Chinese construction sector output was CNY 31.20 trillion (~USD 4.57 trillion) in 2022, compared to CNY 29.31 trillion (~USD 4.29 trillion) in 2021, registering a 6% growth. China's construction industry contributed around 6.9% to its GDP in 2022.

As per the Ministry of Housing and Urban-Rural Development forecast, China's construction sector is expected to maintain a 6% share of the country's GDP moving into 2025.

According to the International Trade Organization, China is the world's largest construction market, with the highest urbanization rate globally. According to data from the American Institute of Architects (AIA) Shanghai, by 2025, China will have built a city equivalent to 10 in New York since the 1990s.

China is expected to spend nearly USD 13 trillion on buildings by 2030, creating a positive outlook for the market. The country has the largest construction market in the world, encompassing 20% of all construction investments globally.

In North America, according to the US Census, around USD 1,792.9 billion was spent on construction in 2022, a considerable amount and 10% higher than the annual spending on construction in 2021. This indicates an upward trend for buildings and construction in the region.

Furthermore, according to Eurostat, the European construction sector grew by 2.5% in 2022 due to new investments from the EU Recovery Fund. The major construction projects in 2022 accounted for non-residential construction (offices, hospitals, hotels, schools, and industrial buildings), accounting for 31.3% of total activity.

All of these things are likely to make more people want to buy polyurethane adhesives and sealants over the next few years.

Asia-Pacific to Dominate the Market

The Asia-Pacific region dominated the global market. The increasing demand from industries such as packaging, construction, automotive, healthcare, etc., in countries such as China, India, and Japan is driving the market studied.

China is actively promoting and sustaining an ongoing urbanization trend, aiming for an anticipated rate of 70% by the year 2030. Consequently, the heightened construction activities in countries such as China are expected to propel growth in the adhesive industry within the region. These factors collectively contribute to an elevated demand for adhesives across the region.

As per Invest India, the Indian construction industry is expected to reach USD 1.4 trillion by 2025, and the construction industry in India works across 250 sub-sectors with linkages across sectors and over 54 global innovative construction technologies identified under a Technology Sub-Mission of PMAY-U to start a new era in the Indian construction sector.

Polyurethane (PU) adhesives and sealants play a crucial role in the footwear industry, ensuring the durability, comfort, and aesthetic appeal of shoes. They are used in various stages of shoe manufacturing, from bonding the upper to the sole to sealing seams and attaching embellishments.

China is the largest consumer of PU and the largest producer of footwear globally. China is the world's largest footwear manufacturer and exporter, dominating worldwide. China shipped more than 13 billion pairs of shoes and boots in 2022.

On the other hand, China is the world's greatest producer and purchaser of automobiles. According to OICA, China has the largest automotive production base in the world, with a total vehicle production of 27.02 million units in 2022, registering an increase of 3% compared to 26.08 million units produced last year.

Hence, such market trends are expected to significantly impact the growth of the adhesives and sealants market in the region during the forecast period.

Polyurethane Adhesives and Sealants Industry Overview

The polyurethane adhesives and sealants market is fragmented in nature. The major players (not in any particular order) include 3M, H.B. Fuller Company, Arkema (Bostik), Dow, and Henkel AG & Co. KGaA, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Deliverables

1.2 Study Assumptions

1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Rising Demand from the Construction Industry in the Asian Region

4.1.2 Growth in the Packaging Industry

4.1.3 Other Drivers

4.2 Restraints

4.2.1 Stricter Regulations on Hazardous Materials and Environmental Concerns

4.2.2 Fluctuating Raw Material Prices

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

5.1 Technology

5.1.1 Water-based

5.1.2 Solvent-based

5.1.3 Hot-melt

5.1.4 Other Technologies (Bio-based, Nano-PU adhesives, etc.)

5.2 End-user Industry

5.2.1 Building and Construction

5.2.2 Healthcare

5.2.3 Automotive and Transportation

5.2.4 Packaging

5.2.5 Footwear and Leather

5.2.6 Electrical and Electronics

5.2.7 Other End-user Industries (Woodworking and Furniture, Consumer Goods, etc.)

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Indonesia

5.3.1.6 Malaysia

5.3.1.7 Thailand

5.3.1.8 Vietnam

5.3.1.9 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 France

5.3.3.4 Italy

5.3.3.5 Spain

5.3.3.6 Russia

5.3.3.7 Turkey

5.3.3.8 NORDIC Countries

5.3.3.9 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Colombia

5.3.4.4 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Qatar

5.3.5.4 United Arab Emirates

5.3.5.5 Egypt

5.3.5.6 Algeria

5.3.5.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 3M

6.4.2 Arkema

6.4.3 Beijing Comens New materials Co. Ltd

6.4.4 Dow

6.4.5 H.B.Fuller Company

6.4.6 Henkel AG & Co.KGaA

6.4.7 Hubei Huitian New Materials Co. Ltd

6.4.8 Huntsman International LLC

6.4.9 Jowat SE

6.4.10 Kangada New Materials (Group) Co. Ltd

6.4.11 MAPEI SpA

6.4.12 NANPAO RESINS CHEMICAL GROUP

6.4.13 Pidilite Industries Ltd

6.4.14 Sika AG

6.4.15 Soudal Holding NV

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Rising Demand for Bio-based PU Hot-melt Adhesives