남미의 전기자동차용 전지 음극 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

South America Electric Vehicle Battery Anode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1636449

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

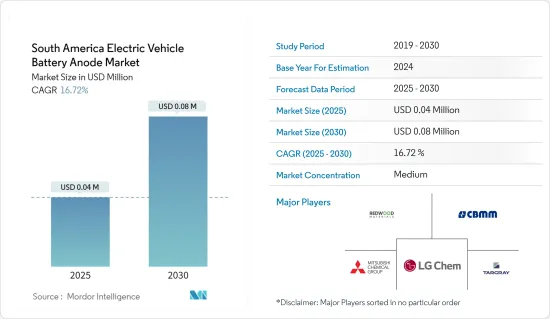

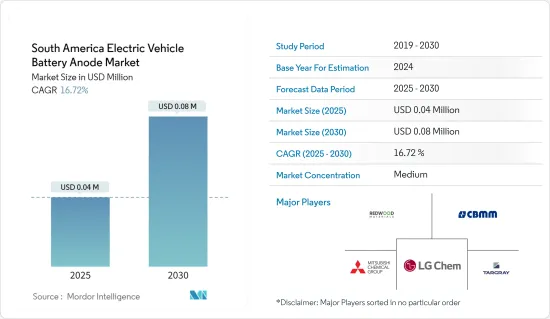

남미의 전기자동차용 전지 음극 시장 규모는 2025년에 4만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 16.72%로, 2030년에는 8만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

예측 기간 동안 전기차 보급 대수 증가, 정부 지원책, 리튬 이온 전지 가격 하락이 시장 성장을 뒷받침합니다.

그러나 동지역은 전지부품 수입에 크게 의존하고 있기 때문에 이는 향후 시장 확대에 과제가 되고 있습니다.

그러나 현재 진행중인 음극 재료와 효율적인 전해질에 대한 조사와 진보는 시장 성장의 유망한 기회를 제공합니다.

브라질은 자동차 부문의 음극재 수요 증가에 힘입어 시장을 선도하게 될 것으로 전망됩니다.

남미의 전기자동차 전지 음극 시장 동향

리튬 이온 전지가 큰 점유율을 차지할 전망

남미의 리튬 이온 전기자동차 전지 시장은 풍부한 리튬 자원을 배경으로 성장이 전망되고 있습니다. 아르헨티나, 볼리비아, 칠레의 일부에 걸쳐 있는 리튬 트라이앵글은 세계 리튬 매장량의 절반 이상을 차지하고 있으며, 세계 EV 공급망에서 남미가 매우 중요한 역할을 담당하고 있습니다.

이러한 방대한 매장량과 2023년 리튬 이온 전지 팩 가격의 14% 하락(139달러/kWh까지 하락)에 의해 전기자동차용 전지와 부품(양극 등)의 자국 내 제조 기회가 급증하고 있습니다.

이러한 개발을 바탕으로 많은 전지 제조업체들이 동지역의 리튬 매장량 탐사에 투자를 하고 있습니다. 이러한 탐사와 생산의 급증은 전기자동차용 리튬 이온 전지 수요를 증폭하고, 생산에 사용되는 전지용 음극의 필요성을 높일 것입니다.

예를 들어 2024년 7월 프랑스 광산그룹 에라메트와 중국의 Tsingshan은 전기자동차 산업 수요 증가에 대응하기 위해 아르헨티나의 살타에 리튬 생산 공장을 건설했습니다. 8억 7,000만 달러에 이르는 이 전략적 투자는 동지역의 중요성을 강조합니다.

향후 동지역의 풍부한 매장량을 바탕으로 리튬 이온 전지 제조에 대한 투자가 확대함에 따라 전기차용 리튬 이온 음극 시장도 확대 기조에 있습니다. 이 전망을 뒷받침하기 위해 볼리비아 대통령은 2024년 3월 EV용 전지를 포함한 전지 수출을 2026년부터 시작할 의향을 밝혔습니다.

전기차에 대한 리튬 이온 전지 도입이 증가하고 그 가격이 급락하고 있기 때문에 리튬 이온 전지 음극 부문은 향후 몇 년동안 크게 성장할 것입니다.

브라질이 큰 점유율을 차지할 전망

브라질은 남미 최대의 자동차 시장으로 수많은 세계 자동차 제조업체를 보유한 견고한 제조거점을 자랑합니다. 산업이 전기화로 전환하면서, 이러한 추세는 특히 전지 및 전지 음극와 같은 중요한 부품의 생산으로 원활하게 전환하고 있습니다.

게다가, EV 전지 제조 부문에서 브라질의 지위 향상은 EV 전지 음극 시장을 변화시키고 있습니다. 브라질은 전지 생산 시설을 설치하기 위해 거액의 외국 투자를 모집하여 세계적인 파트너십을 맺고 있기 때문에 리튬 이온 전지에 불가결한 프리미엄 음극재 수요가 높아지고 있습니다.

예를 들어, 2023년 9월 중국 BYD가 브라질에서 최초의 전지 공장을 시작했습니다. BYD는 브라질에서 전기자동차(EV)뿐만 아니라 전기버스를 생산하고 현지에서 제조한 전지를 활용할 예정입니다. 이와 같은 전략적 움직임은 브라질의 EV용 전지 음극 시장 수요를 확대할 것으로 예상됩니다.

게다가 브라질에서 전기차 판매가 급증함에 따라 전지 제조업체는 현지 생산에 대한 투자를 늘리고 이는 EV 전지용 음극 수요를 더욱 촉진하고 있습니다. 국제에너지기구의 보고에 따르면 2023년 브라질의 EV 판매량은 5만 2,000대에 이르렀으며 2022년 1만 8,500대에서 크게 증가했습니다.

앞으로 EV 전지 부문에서 정부의 지지를 바탕으로 전지 음극 시장은 성장하는 태세가 갖추어지고 있습니다. 최근 브라질 정부의 시책 전환은 자동차 제조업체에 의한 새로운 투자의 물결을 가속화하고 있습니다. 설비의 현대화와 연구개발 강화를 목적으로 하는 이러한 투자는 지속가능성과 전기차와 하이브리드차의 생산에 중점을 두고 있습니다. 브라질 자동차 공업회는 2024년 투자액 220억 달러(2032년까지)라는 획기적인 헌신을 강조했습니다.

EV의 급속한 보급과 전지 제조의 급성장을 감안할 때, 브라질은 향후 수년간 시장을 선도할 것으로 예상됩니다.

남미의 전기자동차 전지 음극 산업 개요

남미의 전기자동차 전지 음극 시장은 중간정도의 시장집중도를 보이고 있습니다. 동시장의 주요 기업(순서부동)에는 Redwood Materials Inc., Mitsubishi Chemical Group Corporation, CBMM, LG Chem Ltd, Targray Industries Inc. 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 범위

시장의 정의

전제조건

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

서문

2029년까지 시장 규모와 수요 예측(단위 : 달러)

최근 동향과 개발

정부의 규제와 시책

시장 역학

촉진요인

전지 제조를 위한 정부의 시책과 투자

전지 원료 비용 저하

억제요인

전지 수입 부품에 의존

공급망 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 진입업자의 위협

대체품의 위협

경쟁 기업간 경쟁 관계

투자 분석

제5장 시장 세분화

전지 유형

리튬 이온

납축전지

기타 전지 유형

재료

리튬

흑연

실리콘

기타

지역

브라질

아르헨티나

콜롬비아

기타 남미

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 개요

Redwood Materials Inc.

Anovion LLC

Mitsubishi Chemical Group Corporation

CBMM

NEI Corporation

Targray Industries Inc.

Nexeon Lid.

LG Chem Ltd

Tokai Carbon Co., Ltd.

Resonac Holdings Corporation

시장 순위 분석

기타 유력 기업 목록

제7장 시장 기회와 앞으로의 동향

기타 음극 재료 연구개발 증가

CSM

영문 목차

영문목차

The South America Electric Vehicle Battery Anode Market size is estimated at USD 0.04 million in 2025, and is expected to reach USD 0.08 million by 2030, at a CAGR of 16.72% during the forecast period (2025-2030).

Key Highlights

In the forecast period, the market is poised for growth, driven by the rising adoption of electric vehicles, supportive government initiatives, and declining prices of lithium-ion batteries.

However, the region's heavy reliance on importing battery components poses a challenge to future market expansion.

Yet, ongoing research and advancements in anode materials and efficient electrolytes present promising opportunities for market growth.

Brazil is set to lead the market, fueled by the increasing demand for anode materials in the automotive sector.

South America Electric Vehicle Battery Anode Market Trends

Lithium-ion Battery is Expected to Have a Major Share

South America's lithium-ion EV battery market is poised for growth, thanks to the region's abundant lithium resources. The Lithium Triangle, spanning parts of Argentina, Bolivia, and Chile, harbors over half of the world's lithium reserves, cementing South America's pivotal role in the global EV supply chain.

With these vast reserves and a 14% drop in lithium-ion battery pack prices in 2023 (down to USD139/kWh), there's a burgeoning opportunity for domestic manufacturing of electric vehicle batteries and their components, such as anodes.

In light of these developments, many battery companies are channeling investments into exploring the region's lithium reserves. This surge in exploration and production is set to amplify the demand for lithium-ion batteries in electric vehicles, subsequently heightening the need for battery anodes in their production.

For example, in July 2024, French mining group Eramet and China's Tsingshan launched a lithium production plant in Salta, Argentina, addressing the electric car industry's rising demands. This strategic investment, amounting to USD 870 million, underscores the site's significance.

Looking ahead, as the region ramps up investments in lithium-ion battery manufacturing, buoyed by its rich reserves, the market for lithium-ion anodes in EVs is on an upward trajectory. Bolstering this outlook, Bolivia's President, in March 2024, unveiled ambitions to commence battery exports, including EV batteries, by 2026.

Given the rising adoption of lithium-ion batteries in electric vehicles and their plummeting prices, the lithium-ion battery anode segment is set for substantial growth in the coming years.

Brazil is Expected to have a Significant Share

Brazil stands as South America's largest automotive market, boasting a robust manufacturing base that hosts numerous global automakers. As the industry pivots towards electrification, this trend has seamlessly transitioned to the production of essential components, notably batteries and battery anodes.

Moreover, Brazil's rising stature in the EV battery manufacturing arena is shaping the trajectory of its EV battery anode market. With Brazil drawing substantial foreign investments and forging global partnerships to set up battery production facilities, there's a heightened demand for premium anode materials, vital for lithium-ion batteries.

For example, in September 2023, BYD, a Chinese firm, launched its first battery factory in Brazil. Beyond electric vehicles (EVs), BYD is set to produce electric buses in Brazil, leveraging batteries manufactured on-site. Such strategic moves are poised to amplify the demand for the country's EV battery anode market.

Furthermore, as electric vehicle sales surge in Brazil, battery manufacturers are increasingly investing in local production, further fueling the demand for EV battery anodes. The International Energy Agency reported that in 2023, Brazil's EV car sales reached 52,000 units, a significant jump from 18,500 units in 2022.

Looking ahead, bolstered by government backing in the EV battery sector, the battery anode market is poised for growth. Recent policy shifts by Brazil's government have ignited a wave of new investments from vehicle manufacturers. These investments, targeting facility modernization and enhanced R&D, emphasize sustainability and the production of electric and hybrid vehicles. The Brazilian Association of Vehicle Manufacturers highlighted a landmark commitment of USD 22 billion in 2024 investments, extending through 2032.

Given the surging adoption of EVs and the burgeoning battery manufacturing landscape, Brazil is set to lead the market in the coming years.

South America Electric Vehicle Battery Anode Industry Overview

The South America electric vehicle battery anode market is semi-concentrated. Some of the major players in the market (in no particular order) include Redwood Materials Inc., Mitsubishi Chemical Group Corporation, CBMM, LG Chem Ltd, and Targray Industries Inc., among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Government Policies and Investments towards battery manufacturing

4.5.1.2 Decline in cost of battery raw materials

4.5.2 Restraints

4.5.2.1 Dependence on Battery Imported Components

4.6 Supply Chain Analysis

4.7 Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

4.8 Investment Analysis

5 MARKET SEGMENTATION

5.1 Battery Type

5.1.1 Lithium-ion

5.1.2 Lead-Acid

5.1.3 Other Battery Types

5.2 Material

5.2.1 Lithium

5.2.2 Graphite

5.2.3 Silicon

5.2.4 Others

5.3 Geography

5.3.1 Brazil

5.3.2 Argentina

5.3.3 Colombia

5.3.4 Rest of South America

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 Redwood Materials Inc.

6.3.2 Anovion LLC

6.3.3 Mitsubishi Chemical Group Corporation

6.3.4 CBMM

6.3.5 NEI Corporation

6.3.6 Targray Industries Inc.

6.3.7 Nexeon Lid.

6.3.8 LG Chem Ltd

6.3.9 Tokai Carbon Co., Ltd.

6.3.10 Resonac Holdings Corporation.

6.4 Market Ranking Analysis

6.5 List of Other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 The Increasing Research and Development of Other Anode Materials