북미의 전기자동차용 전지 음극 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

North America Electric Vehicle Battery Anode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1636448

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

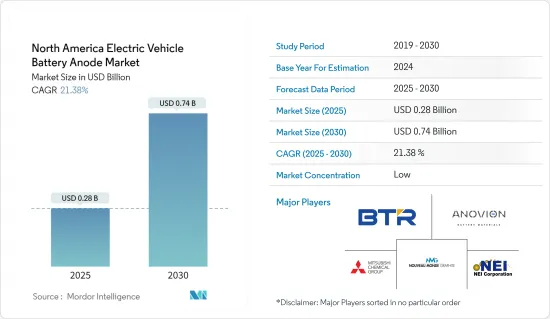

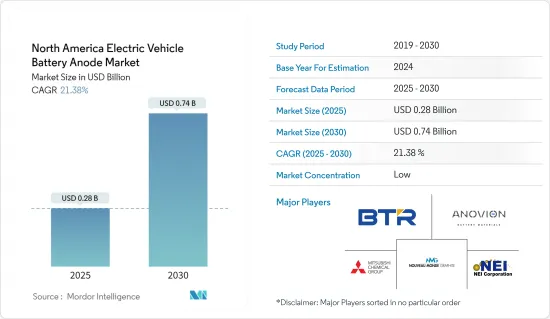

북미의 전기자동차용 전지 음극 시장 규모는 2025년에 2억 8,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 21.38%로, 2030년에는 7억 4,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

예측 기간 동안 전기차 보급 확대, 정부 지원책, 리튬 이온 전지 가격 하락이 시장 성장을 뒷받침합니다.

반대로 전지 부품의 자국 생산이 제한되어 시장은 과제에 직면할 수 있습니다.

그러나 현재 진행중인 음극 재료와 효율적인 전해질 연구 및 진보는 시장 확대의 유망한 기회를 제공합니다.

자동차 부문 수요가 증가하고 있는 미국은 음극 재료의 적용 확대로 시장을 선도하게 될 것으로 보입니다.

북미 전기자동차 전지 음극 시장 동향

리튬 이온 전지 유형이 큰 점유율을 차지할 전망

역사적으로 리튬 이온 전지는 휴대폰에서 컴퓨터에 이르기까지 소비자 전자 기기에 전력을 공급해 왔습니다. 그러나 그 역할은 확대되어 북미에서는 하이브리드 자동차나 완전 전기자동차(EV)의 전원으로 선호되고 있습니다. 이 변화는 주로 CO2나 질소산화물과 같은 온실가스를 배출하지 않는 EV의 환경적 이점 때문입니다.

북미에서는 리튬 이온 전지가 높은 용량 대 중량비로 인해 다른 유형의 전지보다 널리 보급됩니다. 리튬 이온 전지의 도입은 뛰어난 성능, 긴 수명, 비용 절감으로 더욱 가속화되고 있습니다. 높은 에너지 밀도와 긴 수명으로 리튬 이온 전지는 EV 제조업체에게 최적의 선택이 되었습니다. 북미 국가들이 EV 생산을 확대함에 따라 리튬 이온 기술에 맞춘 선진적 제조장치에 대한 수요가 높아지고, 이는 전지 음극재 수요를 견인하고 있습니다.

북미에서 리튬 이온 전지 시장 우위의 중요한 요소는 가격 하락입니다. 지난 10년간 기술 발전, 규모 경제, 정교한 제조 공정으로 인해 리튬 이온 전지의 비용이 크게 떨어졌습니다.

2023년에는 리튬 이온 전지 팩의 가격은 전년 대비 14% 하락하여 139달러/kWh입니다. 전지 가격이 하락함에 따라 EV는 합리적인 가격이 되어 전기자동차 보급과 시장 점유율 확대로 이어집니다. 이러한 수요의 급증은 음극을 포함한 전지 부품 소비량 증가를 촉진하고, 전지 성능을 향상시키기 위한 기술 진보를 촉진합니다.

향후, 동지역에서는 음극재나 양극재 등의 리튬 이온 전지 제조 부품 생산력 강화가 중시되기 때문에 리튬 이온 전지 음극 시장은 예측 기간 중에 성장할 것으로 예측됩니다.

예를 들어, 2024년 4월에는 호주에 본사를 둔 Sicona Battery Technologies가 미국 남동부에 최초의 실리콘-탄소 음극재 생산 시설을 설립할 예정입니다. 실리콘-탄소 음극은 전기자동차(EV) 전지 제조에 점점 더 많이 사용되고 있습니다. 전통적인 리튬 이온 전지는 일반적으로 흑연 음극을 사용하지만, 실리콘-탄소 음극은 특히 에너지 밀도면에서 여러가지 장점이 있습니다. 동사는 2030년까지 미국 내 생산량을 연간 2만 6,500톤으로 확대할 계획입니다.

따라서, 전기자동차에서 리튬 이온 전지 사용 증가 및 가격 감소로 인해, 리튬 이온 전지 음극 부문은 예측 기간 동안 크게 성장할 것으로 예상됩니다.

미국이 시장을 독점할 전망

최근 미국의 EV용 전지 음극 시장은 전기자동차 보급과 최첨단 전지 기술에 대한 수요 증가에 힘입어 급속도로 확대되고 있습니다.

미국에서 전기차 판매가 급증함에 따라 전지 제조업체는 미국 내 생산에 대한 투자를 늘리고 EV 전지용 음극에 대한 수요를 높이고 있습니다. 국제에너지기구(IEA)의 보고에 따르면 미국의 전기차 판매량은 2023년 139만대에 달했으며 2022년 99만대에서 현저하게 증가했습니다.

전지 제조업체는 정부의 강력한 지원을 받아 미국 내에 전기자동차(EV)를 위한 새로운 공장을 설립했습니다. 이 확장은 EV 생산에 사용되는 재료, 특히 전지 및 음극에 대한 수요를 크게 증가시킵니다. 예를 들어 미국 에너지부는 2024년 1월 EV용 전지와 충전 시스템 연구개발을 추진하는 프로젝트에 1억 3,100만 달러를 할당했습니다.

향후, EV의 보급이 진행됨에 따라, 전지 음극 시장은 전지 기술을 위한 국가 차원의 연구개발 노력에 뒷받침되어 성장하는 태세가 갖추어지고 있습니다. 특히 기존 흑연 음극보다 높은 에너지 밀도를 보장하는 혁신적인 실리콘-탄소 복합 음극은 EV의 항속 거리를 늘리는 데 매우 중요합니다. 파나소닉과 LG 에너지 솔루션 같은 대기업은 Sila Nanotechnologies와 같은 신흥 기업과 함께 음극의 성능과 안정성을 높이기 위한 연구개발에 자원을 투입하고 있습니다.

또한, Nouveau Monde Graphite는 캐나다 퀘벡주에서 급성장하는 리튬 이온 전지 및 연료전지 시장을 대상으로 탄소 중립 전지 음극재 개발에 선구적인 역할을 하고 있습니다.

EV 보급과 기술 진보의 동향을 고려하면 예측 기간 동안 미국이 시장을 선도하게 될 것으로 예상됩니다.

북미 전기자동차 전지 음극 산업 개요

북미의 전기자동차 전지 음극 시장은 양분화되어 있습니다. 동시장의 주요 기업(순서부동)에는 BTR New Material Group, Mitsubishi Chemical Group Corporation, Anovion LLC, Nouveau Monde Graphite Inc, NEI Corporation 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 범위

시장의 정의

전제조건

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

서문

2029년까지 시장 규모와 수요 예측(단위 : 달러)

최근 동향과 개발

정부의 규제와 시책

시장 역학

촉진요인

전지 제조를 위한 정부의 시책과 투자

전지 원료 비용 저하

억제요인

전지 부품 자국 제조 한계

공급망 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 진입업자의 위협

대체품의 위협

경쟁 기업간 경쟁 관계

투자 분석

제5장 시장 세분화

전지 유형

리튬 이온

납축전지

기타

재료

리튬

흑연

실리콘

기타

지역

미국

캐나다

기타 북미

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 개요

BTR 신재료 그룹

Anovion LLC

Mitsubishi Chemical Group Corporation

Nouveau Monde Graphite Inc

NEI Corporation

Targray Industries Inc.

Nexeon Lid.

LG Chem Ltd

Tokai Carbon Co., Ltd.

Nippon Carbon Co., Ltd.

시장 순위 분석

기타 유력 기업 일람

제7장 시장 기회와 앞으로의 동향

기타 전지화학 연구개발 증가

CSM

영문 목차

영문목차

The North America Electric Vehicle Battery Anode Market size is estimated at USD 0.28 billion in 2025, and is expected to reach USD 0.74 billion by 2030, at a CAGR of 21.38% during the forecast period (2025-2030).

Key Highlights

In the forecast period, the market is poised for growth, driven by the rising adoption of electric vehicles, supportive government initiatives, and declining prices of lithium-ion batteries.

Conversely, the market may face challenges due to the limited domestic manufacturing of battery components.

However, ongoing research and advancements in anode materials and efficient electrolytes present promising opportunities for market expansion.

With increasing demand from the automotive sector, the United States is set to lead the market, bolstered by its growing application of anode materials.

North America Electric Vehicle Battery Anode Market Trends

Lithium-ion Battery Type is Expected to Have a Major Share

Historically, lithium-ion batteries powered consumer electronics, from mobile phones to personal computers. However, their role has expanded, becoming the preferred power source for hybrid and fully electric vehicles (EVs) in North America. This shift is primarily attributed to the environmental benefits of EVs, which produce no CO2, nitrogen oxides, or other greenhouse gases.

In North America, lithium-ion batteries are outpacing other battery types in popularity due to their favorable capacity-to-weight ratio. Their adoption is further fueled by superior performance, extended shelf life, and declining costs. With high energy density and long cycle life, lithium-ion batteries have become the go-to choice for EV manufacturers. As countries in North America ramp up EV production, there's a growing demand for advanced manufacturing equipment tailored to lithium-ion technology, thereby driving the demand for battery anode material.

A significant driver of lithium-ion batteries' market dominance in North America is their decreasing prices. Over the last decade, technological advancements, economies of scale, and refined manufacturing processes have led to a significant drop in lithium-ion battery costs.

In 2023, the price of lithium-ion battery packs decreased by 14% compared to the previous year to USD139/kWh. As battery prices drop, EVs become more affordable, leading to increased adoption and a larger market share for electric vehicles. This surge in demand will drive higher consumption of battery components, including the anode, and encourage technological advancements to improve battery performance.

In the future, due to the region's heightened emphasis on boosting the production of lithium-ion battery manufacturing components, such as anode and cathode materials, the market for lithium-ion battery anodes is projected to grow during the forecast period.

For instance, in April 2024, Sicona Battery Technologies, based in Australia, is set to establish its inaugural production facility for silicon-carbon anode materials in the Southeastern United States. Silicon-carbon anodes are increasingly being used in the manufacturing of electric vehicle (EV) batteries. Traditional lithium-ion batteries typically use graphite anodes, but silicon-carbon anodes offer several advantages, particularly in terms of energy density. By 2030, the company plans to expand its U.S. production to a total output of 26,500 tons annually.

Thus, owing to the increasing use of lithium-ion batteries in electric vehicles and decreasing prices, the lithium-ion battery anode segment is expected to grow significantly in the forecast period.

United States of America is Expected to Dominate the Market

In recent years, the United States EV battery anode market has rapidly expanded, fueled by the rising adoption of electric vehicles and the demand for cutting-edge battery technologies.

As electric vehicle sales surge in the United States, battery manufacturers are increasingly investing in domestic production, thereby driving up demand for EV battery anodes. The International Energy Agency reported that U.S. EV car sales reached 1.39 million units in 2023, a notable rise from 0.99 million in 2022.

With strong government support, battery manufacturers are setting up new plants for electric vehicles (EVs) in the United States. This expansion is set to significantly elevate the demand for materials, especially battery anodes, used in EV production. For example, in January 2024, the U.S. Department of Energy allocated USD 131 million to projects aimed at advancing research and development in EV batteries and charging systems.

Looking ahead, as EV adoption continues to rise, the battery anode market is poised for growth, bolstered by the nation's R&D efforts in battery technology. Notably, the innovative silicon-carbon composite anodes, which promise higher energy density than traditional graphite anodes, are pivotal for extending the EV range. Major players like Panasonic and LG Energy Solution, alongside newcomers like Sila Nanotechnologies, are pouring resources into R&D to boost anode performance and stability.

Moreover, Nouveau Monde Graphite is pioneering the development of a carbon-neutral battery anode material in Quebec, Canada, targeting the burgeoning lithium-ion and fuel cell markets.

Given the trajectory of EV adoption and technological advancements, the U.S. is poised to lead the market during the forecast period.

North America Electric Vehicle Battery Anode Industry Overview

The North America electric vehicle battery anode market is semi-fragmented. Some of the major players in the market (in no particular order) include BTR New Material Group Co., Ltd., Mitsubishi Chemical Group Corporation, Anovion LLC, Nouveau Monde Graphite Inc, and NEI Corporation, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Government Policies and Investments towards battery manufacturing

4.5.1.2 Decline in cost of battery raw materials

4.5.2 Restraints

4.5.2.1 Limited Domestic Manufacturing of Battery Components

4.6 Supply Chain Analysis

4.7 Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

4.8 Investment Analysis

5 MARKET SEGMENTATION

5.1 Battery Type

5.1.1 Lithium-ion

5.1.2 Lead-Acid

5.1.3 Other Battery Types

5.2 Material

5.2.1 Lithium

5.2.2 Graphite

5.2.3 Silicon

5.2.4 Others

5.3 Geography

5.3.1 United States

5.3.2 Canada

5.3.3 Rest of North America

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1

BTR New Material Group Co., Ltd

6.3.2 Anovion LLC

6.3.3 Mitsubishi Chemical Group Corporation

6.3.4 Nouveau Monde Graphite Inc

6.3.5 NEI Corporation

6.3.6 Targray Industries Inc.

6.3.7 Nexeon Lid.

6.3.8 LG Chem Ltd

6.3.9 Tokai Carbon Co., Ltd.

6.3.10 Nippon Carbon Co., Ltd.

6.4 Market Ranking Analysis

6.5 List of Other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 The Increasing Research and Development of Other Battery Chemistries