프랑스의 전기자동차용 전지 음극 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

France Electric Vehicle Battery Anode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1636421

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

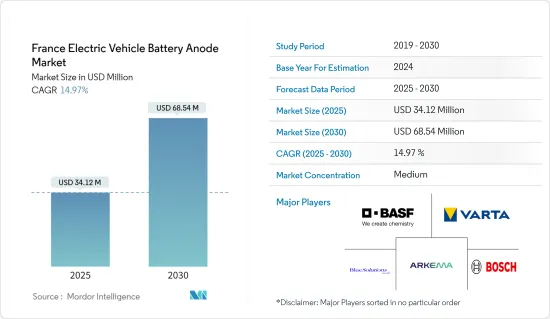

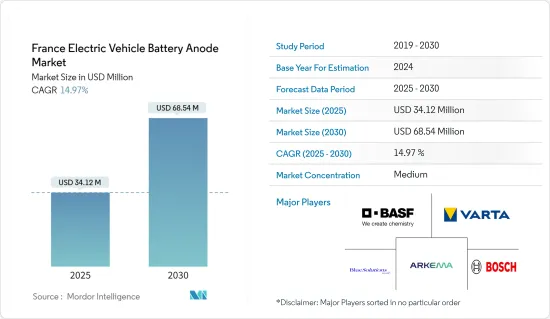

프랑스의 전기자동차 전지 음극 시장 규모는 2025년에 3,412만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 14.97%로, 2030년에는 6,854만 달러에 이를 것으로 예측됩니다.

주요 하이라이트

중기적으로는 전기자동차(EV) 보급의 확대와 음극재료의 기술진보가 예측 기간 동안 전기자동차 전지 음극 수요를 견인할 것으로 예상됩니다.

한편, 첨단 음극재, 특히 아직 실험 단계에 있는 음극재는 생산 비용이 높기 때문에 독일 전기자동차 전지 음극 시장의 성장을 크게 억제할 수 있습니다.

재활용과 순환 경제에 대한 관심 증가는 지속 가능한 음극재를 개발할 기회를 가져오고, 재활용 프로세스는 가까운 미래에 전기자동차 전지 음극 시장에 큰 기회를 가져올 것으로 예상됩니다.

프랑스 전기자동차 전지 음극 시장 동향

리튬 이온 전지 유형이 시장을 독점

독일에서는 특히 EV 부문의 리튬 이온 전지가 지속 가능한 운송으로의 전환에 필수적입니다. 자동차 산업의 세계 리더인 독일 정부는 리튬 이온 전지의 중요한 부품인 음극에 특히 중점을 두고 최첨단 EV용 전지 기술의 진보와 생산에 주력하고 있습니다.

음극은 리튬 이온 전지에 필수적이며 용량, 수명 및 충전 속도에 영향을 미칩니다. 또한, 이 전지의 비용은 전기자동차의 가격 설정에 크게 영향을 미칩니다. 따라서 독일 EV용 전지 음극 시장은 보다 넓은 리튬 이온 전지 시장에서 가장 중요합니다.

예를 들어 블룸버그 NEF의 보고서에 따르면 2023년 전지 가격은 139달러/kWh로 전년 대비 13% 하락했습니다. 지속적인 기술 발전과 제조 개선으로 인해 전지 팩의 가격이 더욱 감소하고 2025년에는 113달러/kWh, 2030년에는 80달러/kWh가 될 것으로 예상됩니다. 제조 효율 향상으로 리튬 이온 전지의 생산이 증가함에 따라, 전지 음극의 단가는 예측 기간 동안 감소할 것으로 예상됩니다.

게다가, 음극 재료의 기술 혁신이 리튬 이온 전지의 성능을 높이고, 종래의 내연 엔진 차량에 대한 EV의 경쟁을 점점 격화시키고 있습니다. 동지역 정부는 EV 전지의 혁신을 적극적으로 지지하고 있으며 대기업은 최근 EV 전지의 음극 재료를 강화하는 프로젝트에 착수하고 있습니다.

예를 들어 HPQ Silicon Inc.는 2023년 12월 프랑스에 본사를 둔 계열사인 NOVACIUM SAS가 90,000유로(약 9만 9,000달러)의 French Tech Emergence Grant를 획득했다고 밝혔습니다. 이 보조금은 첨단 SiOx계 전지용 음극 재료의 밸류 체인 전체를 강화하는 프로젝트를 지원하는 것을 목적으로 하고 있습니다. 리튬 전지 영역에서 현저한 동향은 흑연 복합 전극에 5% 내지 10%의 산화규소(SiOx) 첨가제를 사용하는 것입니다. 이러한 진보는 동지역의 선진적 전지 생산을 뒷받침해 향후 몇 년간은 전지 제조에 있어서의 음극 수요를 높일 것으로 예상됩니다.

프랑스에서는 음극재의 주요 용도는 전기자동차(EV)용 리튬 이온 전지입니다. 이 전지는 승용차에서 상용차, 공공 운송에 이르기까지 다양한 EV에 전력을 공급합니다. 프랑스의 주요 기업은 모든 EV 카테고리에서 급증하는 수요에 대응하기 위해 여러 전지 제조 프로젝트를 시작하고 있습니다.

예를 들어 프랑스의 Blue Solutions는 2024년 5월 프랑스 동부에 약 20억 유로(21억 7,000만 달러)를 투자하는 기가팩토리 계획을 발표했습니다. 이 시설에서는 20분의 급속 충전 시간을 자랑하는 EV용 신형 고체 전지의 생산을 목표로 하고 있으며, 2030년까지 생산을 개시할 예정입니다. 이러한 노력은 청정 에너지 솔루션으로서 리튬 이온 전지의 채용을 촉진하고 예측 기간 동안 음극 재료 수요가 증가할 것으로 예상됩니다.

이러한 프로젝트와 기술 혁신은 동지역에서 리튬 이온 전지의 생산을 확대하고 향후 수년간 EV전지용 음극 수요를 급증시킬 것입니다.

EV 보급 확대가 시장을 견인

프랑스에서는 소비자의 기호의 변화와 규제의 의무화에 의해 전기자동차(EV) 수요가 급증하고 있어 EV전지용 음극 시장을 뒷받침하고 있습니다. 이 기세는 정부의 장려책과 전지 개발의 기술적 진보에 의해 더욱 뒷받침되어 지속적인 시장 확대의 무대를 제공하고 있습니다.

동지역의 전기자동차 판매량은 최근 급증하고 있습니다. 예를 들어 국제에너지기구(IEA)의 보고에 따르면 2023년 프랑스에서 판매된 전기차는 47만대로 2022년보다 38.2% 증가했습니다. 따라서 동지역 전체에서 전기자동차 판매량이 크게 증가하고 이에 따라 전지 음극재 수요도 증가할 것으로 예측합니다.

또한, 이산화탄소 배출을 억제하고 전기 이동성을 지지하는 것을 목표로 하는 프랑스 정부의 보조금과 인센티브는 시장을 추진하는데 중요한 역할을 하고 있습니다. 이러한 노력에는 EV 구매에 대한 재정적 지원, 세제 우대 정책, 충전 인프라에 대한 투자 강화 등이 포함됩니다. 이들을 총칭하여 전기자동차의 보급을 뒷받침할 뿐만 아니라 리튬 이온 전지의 생산에 필수적인 전지용 음극 수요도 높아지고 있습니다.

예를 들어, 2024년 5월 프랑스 정부는 최상급 자동차 제조업체와 협정을 맺고 2027년까지 전기차 판매량 80만대를 달성하는 야심찬 목표를 세웠습니다. 또한 정부는 다양한 이니셔티브를 통해 전기차 생산과 구매를 강화하기 위해 15억 유로(약 16억 달러)를 할당했습니다. 이러한 전략적인 동향은 전기자동차의 생산을 가속시킬 뿐만 아니라 전지 음극재 수요도 확대시킬 것입니다.

또한 전기자동차로의 전환은 순탄소 배출량 0이라는 목표를 실현하는데 매우 중요합니다. 동지역의 주요 기업은 전기자동차 생산을 강화하기 위해 적극적으로 투자하고 프로젝트를 시작하고 있습니다.

예를 들어 중국의 유명한 전기자동차 제조업체인 BYD는 2024년 6월 프랑스에 EV 생산 시설을 설립하고 플러그인 하이브리드 자동차(PHEV)를 전국에 도입할 계획을 발표했습니다. 이 시설은 내년 말부터 운영을 시작할 예정입니다. 이러한 노력은 EV의 생산을 뒷받침하고 나아가서는 전지와 음극 수요를 확대하게 됩니다.

정리하면 이러한 협조적인 노력과 전략에 의해 EV의 판매가 강화되고, 이에 따라 음극 전지재료 수요도 당분간 증가할 것으로 예상됩니다.

프랑스 전기자동차 전지 음극 산업 개요

프랑스 전기자동차 전지 음극 시장은 완만합니다. 주요 기업(순서부동)은 BASF SE, Varta AG, Blue Solutions, Arkema S.A., Robert Bosch GmbH 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사 범위

시장의 정의

전제조건

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

서문

2029년까지 시장 규모와 수요 예측(단위 : 달러)

최근 동향과 개발

정부의 규제와 시책

시장 역학

촉진요인

전기자동차 보급 확대

음극 재료의 진보

억제요인

높은 생산 비용

공급망 분석

PESTLE 분석

투자 분석

제5장 시장 세분화

전지 유형

리튬 이온 전지

납축전지

기타

재료 유형

리튬

흑연

실리콘

기타

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 개요

BASF SE

Varta AG

Blue Solutions

Arkema S.A.

Robert Bosch GmbH

TotalEnergies SE

STMicroelectronics

NAWA Technologies

Solvay S.A.

기타 유력 기업 목록

시장 순위 분석

제7장 시장 기회와 앞으로의 동향

순환형 경제와 재활용

CSM

영문 목차

영문목차

The France Electric Vehicle Battery Anode Market size is estimated at USD 34.12 million in 2025, and is expected to reach USD 68.54 million by 2030, at a CAGR of 14.97% during the forecast period (2025-2030).

Key Highlights

Over the medium term, the growing EV adoption and technological advancements in anode materials are expected to drive the demand for electric vehicle battery anode during the forecast period.

On the other hand, the high production costs of advanced anode materials, particularly those that are still in the experimental phase can significantly restrain the growth of the Germany electric vehicle battery anode market.

Nevertheless, the growing focus on recycling and the circular economy presents opportunities for developing sustainable anode materials and the recycling processe are expected to create significant opportunities for electric vehicle battery anode market in the near future.

France Electric Vehicle Battery Anode Market Trends

Lithium-Ion Battery Type Dominate the Market

In Germany, the lithium-ion battery, particularly in the electric vehicle (EV) sector, is crucial to the nation's transition towards sustainable transportation. As a global automotive leader, Germany's government is dedicated to advancing and producing state-of-the-art EV battery technologies, with a special focus on the anode, a vital component of lithium-ion batteries.

The anode is essential in lithium-ion batteries, influencing their capacity, lifespan, and charging speed. Moreover, the cost of these batteries significantly affects electric vehicle pricing. Consequently, the nation's EV battery anode market is of paramount importance in the broader lithium-ion battery landscape.

For example, a Bloomberg NEF report highlighted that in 2023, battery prices fell to USD 139/kWh, marking a 13% drop from the prior year. With ongoing technological advancements and manufacturing improvements, battery pack prices are projected to further decline, estimating costs at USD 113/kWh by 2025 and USD 80/kWh by 2030. As lithium-ion battery production ramps up due to enhanced manufacturing efficiencies, the unit cost of battery anodes is expected to decrease during the forecast period.

Moreover, innovations in anode materials are boosting lithium-ion battery performance, making EVs increasingly competitive against traditional internal combustion engine vehicles. Governments in the region are actively championing EV battery innovations, and major companies have recently embarked on projects to enhance anode materials in EV batteries.

For instance, in December 2023, HPQ Silicon Inc. revealed that its affiliate, NOVACIUM SAS, based in France, obtained a French Tech Emergence Grant of EUR 90,000 (around USD 99,000). This grant is intended to support projects that enhance the entire value chain of advanced SiOx-based anode materials for batteries. A notable trend in the lithium battery domain is the use of 5% to 10% silicon oxide (SiOx) additives in graphite composite electrodes. Such advancements are poised to boost sophisticated battery production in the region and elevate the demand for anodes in battery manufacturing in the years ahead.

In France, the primary use of anode materials is in lithium-ion batteries for electric vehicles (EVs). These batteries power a range of EVs, from passenger cars to commercial vehicles and public transport. Leading French companies have initiated multiple battery manufacturing projects to meet the surging demand across all EV categories.

For example, in May 2024, Blue Solutions, a French firm, unveiled plans for a gigafactory in eastern France, with an investment of about 2 billion euros (USD 2.17 billion). This facility aims to produce a new solid-state battery for EVs, boasting a rapid 20-minute charging time, with production slated to commence by 2030. Such initiatives are set to bolster the adoption of lithium-ion batteries as a clean energy solution and heighten the demand for anode materials in the forecast period.

Thus, these projects and innovations are poised to amplify lithium-ion battery production in the region and escalate the demand for EV battery anodes in the coming years.

Growing EV adoption drives the Market

In France, the surging demand for electric vehicles (EVs), driven by changing consumer preferences and regulatory mandates, is propelling the EV battery anode market. This momentum is further bolstered by government incentives and technological strides in battery development, setting the stage for continued market expansion.

Sales of electric vehicles in the region have seen a meteoric rise in recent years. For instance, the International Energy Agency (IEA) reported that in 2023, France sold 0.47 million electric vehicles, marking a 38.2% increase from 2022. Projections indicate a substantial uptick in electric vehicle sales across the region, subsequently amplifying the demand for battery anode materials.

Moreover, the French government's subsidies and incentives, aimed at curbing carbon emissions and championing electric mobility, play a crucial role in propelling the market. These initiatives encompass financial backing for EV purchases, tax incentives, and bolstered investments in charging infrastructure. Collectively, they not only boost electric vehicle adoption but also heighten the demand for battery anodes essential for lithium-ion battery production.

For example, in May 2024, the French government inked a deal with top car manufacturers, setting an ambitious target of 800,000 electric vehicle sales by 2027, a significant leap from 200,000 in 2022. Additionally, the government allocated a substantial 1.5 billion euros (approximately USD 1.6 billion) to bolster electric vehicle production and purchases through diverse initiatives. Such strategic moves are poised to not only accelerate EV production but also amplify the demand for battery anode materials.

Furthermore, the transition to electric vehicles is pivotal in realizing net-zero carbon emission aspirations. Major companies in the region are actively investing and launching projects to bolster electric vehicle production.

For instance, in June 2024, BYD Company, a prominent Chinese electric vehicle manufacturer, declared its plans to establish an EV production facility in France, with intentions to introduce plug-in hybrid vehicles (PHEVs) nationwide. This facility is slated to commence operations by the end of next year. Such endeavors are set to boost EV production and, in turn, escalate the demand for battery anodes.

In summary, these concerted efforts and strategies are anticipated to bolster EV sales and subsequently elevate the demand for anode battery materials in the foreseeable future.

France Electric Vehicle Battery Anode Industry Overview

The France electric vehicle battery anode market is moderate. Some of the key players (not in particular order) are BASF SE, Varta AG, Blue Solutions, Arkema S.A., Robert Bosch GmbH, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Growing Adoption of Electric Vehicles

4.5.1.2 Advancements in Anode Materials

4.5.2 Restraints

4.5.2.1 High Production Costs

4.6 Supply Chain Analysis

4.7 PESTLE Analysis

4.8 Investment Analysis

5 MARKET SEGMENTATION

5.1 Battery Type

5.1.1 Lithium-Ion Batteries

5.1.2 Lead-Acid Batteries

5.1.3 Others

5.2 Material Type

5.2.1 Lithium

5.2.2 Graphite

5.2.3 Silicon

5.2.4 Others

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements