풍력 터빈 피치 및 요 제어 시스템 - 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Wind Turbine Pitch And Yaw Control System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1636230

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

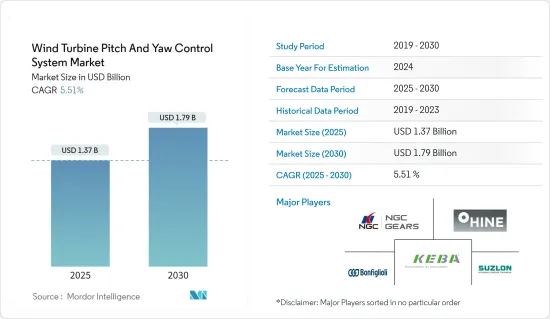

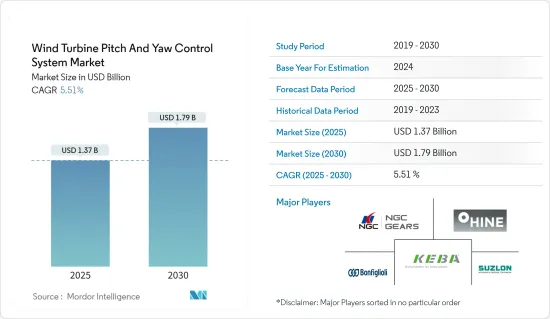

풍력 터빈 피치 및 요 제어 시스템 시장 규모는 2025년에 13억 7,000만 달러로 추정되며, 예측 기간(2025-2030년) 동안 5.51%의 CAGR로 2030년에는 17억 9,000만 달러에 달할 것으로 예상됩니다.

주요 하이라이트

장기적으로 풍력발전 프로젝트에 대한 투자 증가, 정부 지원 정책 및 인센티브는 예측 기간 동안 풍력 터빈의 피치 및 요 제어 시스템 시장을 견인할 것으로 예상되는 주요 요인입니다.

반면, 제어 시스템의 높은 비용과 다른 재생에너지 기술과의 경쟁은 예측 기간 동안 시장을 억제하는 요인으로 작용할 것입니다.

그러나 개선된 기술 시스템과의 하이브리드 시스템 통합과 해상 풍력발전 개발은 예측 기간 동안 풍력 터빈의 피치 및 요 제어 시스템 시장 진입 기업들에게 충분한 기회를 제공합니다.

풍력에너지 인프라 개발이 활발히 이루어지고 있는 유럽이 풍력 터빈의 피치&요 제어 시스템 시장을 독점할 것으로 예상됩니다.

풍력 터빈 피치 및 요 제어 시스템 시장 동향

해양 부문이 시장을 독점

깨끗하고 친환경적인 전력에 대한 수요가 증가함에 따라 주요 기업과 국가들은 재생에너지, 특히 풍력에너지와 해상 풍력에너지의 채택을 추진하고 있습니다. 첨단 기술을 통한 해상 풍력발전의 도입은 많은 국가와 기업을 끌어들이고 있으며, 투자 규모도 큽니다.

해상 풍력발전소 설치는 육지에 비해 풍속이 빠르기 때문에 유리한 시장으로 떠오르고 있습니다. 앞으로 해상 풍력발전의 도입은 유럽 그린딜을 실현하는 핵심이 될 것입니다. 유럽에는 광활한 해역이 있으며, 시속 10마일 이상의 풍속을 지원하는 지역도 있습니다.

해상 풍력발전 기술은 지난 5년 동안 풍속이 낮은 더 많은 지역을 커버하기 위해 설치된 메가 와트 용량당 발전량을 최대화하기 위해 발전해 왔습니다. 최근 몇 년 동안 풍력 터빈은 더 넓은 직경, 더 큰 풍력 터빈 블레이드, 더 높은 허브 높이를 가진 더 큰 규모의 풍력 터빈으로 발전하고 있습니다.

국제재생에너지기구(International Renewable Energy Agency)의 RE Capacity 2024에 따르면, 2023년 해상 풍력발전 용량은 1,696MW 증가하여 2022년 설치 용량과 비교하여 7만 2,663MW에 이르렀으며, 해상 풍력 산업이 크게 증가하였습니다. 해상 풍력 산업의 대폭적인 증가를 보여줍니다.

예측 기간 동안 정부의 노력과 해상 부문의 높은 풍력에너지 잠재력 등의 요인으로 인해 산업 투자가 증가함에 따라 해상 용량이 증가할 것으로 예상됩니다.

일본과 같은 국가들은 2030년까지 10GW, 2035년과 2040년까지 30-40GW의 해상 풍력발전 프로젝트 설치를 계획하고 있습니다. 또한 2024년 7월, 미국 청정전력협회(American Clean Power Association)는 미국의 해상 풍력에너지 산업에 2030년까지 약 650억 달러를 투자할 것이라고 발표했습니다.

이러한 계획으로 인해 예측 기간 동안 해상 부문이 풍력 터빈의 피치 및 요 제어 시스템 시장을 독점할 것으로 예상됩니다.

괄목할만한 성장세를 보이는 유럽

유럽은 해상 풍력발전의 선두주자이며, 세계 최대 규모의 풍력발전소가 운영되고 있습니다. 이 지역의 해상 및 육상 발전 용량은 유럽 주요 국가의 전력 수요를 충족시키기에 충분한 규모입니다.

이 지역은 풍력 터빈 부품 및 제어 시스템에서 가장 일찍부터 가장 큰 규모의 연구 개발이 이루어졌습니다. 풍력 터빈 피치 및 요 제어 시스템 시장의 상당수 기업이 유럽에 기반을 두고 있습니다.

국제재생에너지기구(International Renewable Energy Agency)의 RE Capacity 2024에 따르면 유럽의 풍력발전 용량은 2023년에 16,833MW 증가하여 2022년 설비용량 대비 25만 7,111MW에 달할 것으로 예상됩니다. 풍력 터빈의 설치 용량이 크게 증가하여 풍력 터빈의 피치 및 요 제어 시스템 시장 진입 기업을 크게 촉진하고 있음을 알 수 있습니다.

유리한 정부 정책도 풍력에너지 시장과 관련 부품에 기여하여 세계 2위의 풍력에너지 시장으로 성장하고 있으며, 2023년에 채택된 개정된 재생에너지 지침은 EU의 2030년 재생에너지 의무화 목표를 최소 42.5%로 상향 조정했습니다.

2023년 9월, RWE의 소피아 해상 풍력발전소가 정식으로 착공했습니다. 이는 영국의 넷 제로 목표에 크게 기여하는 기념비적인 재생에너지 프로젝트입니다. 소피아 해상 풍력발전소는 영국 에너지 인프라에 대한 RWE의 32억 달러가 넘는 대규모 투자이며, 재생에너지에 대한 RWE의 실질적 의지를 보여주는 것입니다.

2024년 1월, 프랑스의 초대형 에너지 기업 토탈 에너지 SE는 스웨덴, 덴마크, 핀란드 등 북유럽 3개국에서 해상 풍력발전 프로젝트를 개발하기 위해 유럽 에너지와 새로운 합의를 발표했습니다.

따라서 앞서 언급한 바와 같이, 풍력 터빈의 피치 및 요 제어 시스템 시장은 예측 기간 동안 유럽이 지배적일 것으로 예상됩니다.

풍력 터빈 피치 및 요 제어 시스템 산업 개요

풍력 터빈의 피치 및 요 제어 시스템 시장은 반통합형입니다. 이 시장에서 사업을 전개하는 주요 기업(순서에 관계없이)으로는 Bonfiglioli Transmissions Private Limited, SUZLON Energy Ltd, Nanjing High-Speed Gear Manufacturing, Dana SAC UK Ltd, Hine Group 등이 있습니다.

기타 혜택

엑셀 형식의 시장 예측(ME) 시트

3개월간 애널리스트 지원

목차

제1장 소개

조사 범위

시장 정의와

조사 가정

제2장 조사 방법

조사 프레임워크

2차 조사

1차 조사

데이터 삼각측량과 인사이트 창출

제3장 실행 개요

제4장 시장 개요

소개

2029년까지 시장 규모와 수요 예측(단위 : 10억 달러)

최근 동향과 개발

정부 정책 및 규정

시장 역학

성장 촉진요인

풍력발전 프로젝트에 대한 투자 증가

정부 지원 시책과 인센티브

성장 억제요인

기타 재생에너지 기술과의 높은 경쟁

공급망 분석

Porter's Five Forces 분석

공급 기업의 교섭력

소비자의 협상력

신규 참여업체의 위협

대체품의 위협

경쟁 기업 간의 경쟁 관계

투자 분석

제5장 시장 세분화

요 제어 시스템별

액티브

패시브

용도별

육상

해상

지역별

북미

미국

캐나다

기타 북미

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

아랍에미리트

카타르

이집트

남아프리카공화국

나이지리아

기타 중동 및 아프리카

아시아태평양

중국

인도

일본

인도네시아

베트남

태국

말레이시아

기타 아시아태평양

유럽

영국

독일

프랑스

스페인

러시아

터키

북유럽

기타 유럽

제6장 경쟁 구도

M&A, 합작투자, 제휴, 협정

주요 기업의 전략

기업 개요

시장 진출 기업

Bonfiglioli Transmissions Private Limited

SUZLON Energy Ltd

Nanjing High-Speed Gear Manufacturing Co.

Dana SAC UK Ltd

Hine Group

OAT GmbH

ABM Greiffenberger Gmbh

Siemens AG

시장 순위 분석

기타 저명한 기업 리스트

제7장 시장 기회와 향후 동향

개선된 기술 시스템을 통한 하이브리드 시스템의 통합과 해상 풍력에너지 개발

ksm

영문 목차

영문목차

The Wind Turbine Pitch And Yaw Control System Market size is estimated at USD 1.37 billion in 2025, and is expected to reach USD 1.79 billion by 2030, at a CAGR of 5.51% during the forecast period (2025-2030).

Key Highlights

Over the long term, rising investments in wind power projects and supportive government policies and incentives are the major factors expected to drive the wind turbine pitch and yaw control system market during the forecast period.

On the other hand, the control systems' high costs and high competition from other renewable energy technologies will restrain the market during the forecast period.

However, hybrid systems integration with improved technological systems and offshore wind energy development will provide ample opportunities to the wind turbine pitch and yaw control system market players during the forecast period.

Due to greater wind energy infrastructure development activity, Europe is expected to dominate the wind turbine pitch and yaw control system market.

Wind Turbine Pitch and Yaw Control System Market Trends

The Offshore Segment to Dominate the Market

As the demand for clean, green electricity rises, major companies and countries are adopting renewable energy sources, especially wind energy and offshore wind energy, which can lead to tapping into huge unused potential. Adopting offshore wind energy with advanced technologies attracted many countries and companies with high investments.

The installation of wind farms in offshore areas is becoming a lucrative market because of the higher wind speed compared to onshore wind speed. In the future, deploying offshore wind energy is at the core of delivering the European Green Deal. Europe has vast offshore sea areas, with some regions supporting speeds of more than 10 miles per hour.

Offshore wind energy power generation technology evolved over the last five years to maximize the electricity produced per megawatt capacity installed to cover more sites with lower wind speeds. In recent years, wind turbines have become more extensive with broader diameters, larger wind turbine blades, and taller hub heights.

According to the International Renewable Energy Agency RE Capacity 2024, the offshore wind capacity increased by 10,696 MW in 2023. It reached 72,663 MW, compared to 2022 installed capacity, thus citing a major increase in the offshore wind industry.

During the forecast period, the offshore capacity is expected to increase due to rising investment in the industry due to factors like government initiatives and high wind energy potential in the offshore segment.

Countries like Japan plan to install 10GW of offshore wind projects by 2030 and 30-40 GW capacity by 2035 and 2040. Additionally, in July 2024, the American Clean Power Association announced an investment of approximately USD 65 billion by 2030 in the offshore wind energy industry in the United States.

Thus, with such plans, the offshore segment is expected to dominate the wind turbine pitch and yaw control system market during the forecast period.

Europe to Witness Significant Growth

Europe is a leader in offshore wind energy and is home to one of the biggest operational wind farms worldwide. The region's offshore and onshore capacity is large enough to meet the electricity needs of major European countries.

The region has seen the earliest and most expansive research and development in wind turbine components and control systems. A significant number of companies in the wind turbine pitch and yaw control system market are based in Europe.

According to the International Renewable Energy Agency RE Capacity 2024, wind energy capacity in Europe increased by 16,833 MW in 2023. It reached 257,111 MW compared to the 2022 installed capacity, indicating a significant increase in wind turbine installed capacity and a major boost to the wind turbine pitch and yaw control system market players.

Favorable government policies have also contributed to the wind energy market and related components, making it the second-largest wind energy market globally. Adopted in 2023, the revised Renewable Energy Directive raised the European Union's binding renewable energy target for 2030 to a minimum of 42.5%, earlier set at 32% in 2018.

In September 2023, construction officially commenced at RWE's Sofia Offshore Wind Farm, a monumental renewable energy project set to contribute significantly to the UK's net-zero targets. The Sofia Offshore Wind Farm represents an impressive investment of over USD 3.2 billion in the UK's energy infrastructure by RWE, marking a substantial commitment to renewable energy.

In January 2024, Total Energies SE, the French Supermajor Energy company, announced its new agreement with European Energy to develop offshore wind projects in three Nordic countries: Sweden, Denmark, and Finland.

Thus, based on the aforementioned points, Europe will dominate the wind turbine pitch and yaw control system market during the forecast period.

Wind Turbine Pitch and Yaw Control System Industry Overview

The wind turbine pitch and yaw control system market is semi-consolidated. Some major players operating in the market (in no particular order) include Bonfiglioli Transmissions Private Limited, SUZLON Energy Ltd, Nanjing High-Speed Gear Manufacturing Co. Ltd, Dana SAC UK Ltd, and Hine Group.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition and

1.3 Study Assumptions

2 RESEARCH METHODOLOGY

2.1 Research Framework

2.2 Secondary Research

2.3 Primary Research

2.4 Data Triangulation and Insight Generation

3 EXECUTIE SUMMARY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD billion, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Rising Investments in Wind Power Projects

4.5.1.2 Supportive Government Policies and incentives

4.5.2 Restraints

4.5.2.1 High Competition from Other Renewable Energy Technologies

4.6 Supply Chain Analysis

4.7 Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

4.8 Investment Analysis

5 MARKET SEGMENTATION

5.1 By Yaw Control System

5.1.1 Active

5.1.2 Passive

5.2 By Application

5.2.1 Onshore

5.2.2 Offshore

5.3 Geography

5.3.1 North America

5.3.1.1 United States

5.3.1.2 Canada

5.3.1.3 Rest of North America

5.3.2 South America

5.3.2.1 Brazil

5.3.2.2 Argentina

5.3.2.3 Colombia

5.3.2.4 Rest of South America

5.3.3 Middle East and Africa

5.3.3.1 Saudi Arabia

5.3.3.2 United Arab Emirates

5.3.3.3 Qatar

5.3.3.4 Egypt

5.3.3.5 South Africa

5.3.3.6 Nigeria

5.3.3.7 Rest of Middle East and Africa

5.3.4 Asia-Pacific

5.3.4.1 China

5.3.4.2 India

5.3.4.3 Japan

5.3.4.4 Indonesia

5.3.4.5 Vietnam

5.3.4.6 Thailand

5.3.4.7 Malaysia

5.3.4.8 Rest of Asia-Pacific

5.3.5 Europe

5.3.5.1 United Kingdom

5.3.5.2 Germany

5.3.5.3 France

5.3.5.4 Spain

5.3.5.5 Russia

5.3.5.6 Turkey

5.3.5.7 NORDIC

5.3.5.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 Market Players

6.3.1.1 Bonfiglioli Transmissions Private Limited

6.3.1.2 SUZLON Energy Ltd

6.3.1.3 Nanjing High-Speed Gear Manufacturing Co.

6.3.1.4 Dana SAC UK Ltd

6.3.1.5 Hine Group

6.3.1.6 OAT GmbH

6.3.1.7 ABM Greiffenberger Gmbh

6.3.1.8 Siemens AG

6.4 Market Ranking Analysis

6.5 List of Other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Hybrid systems integration with improved technological systems and offshore Wind Energy development