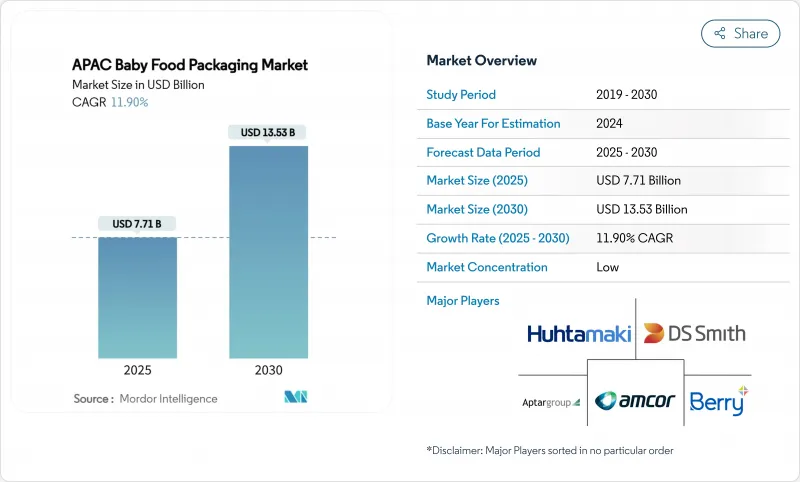

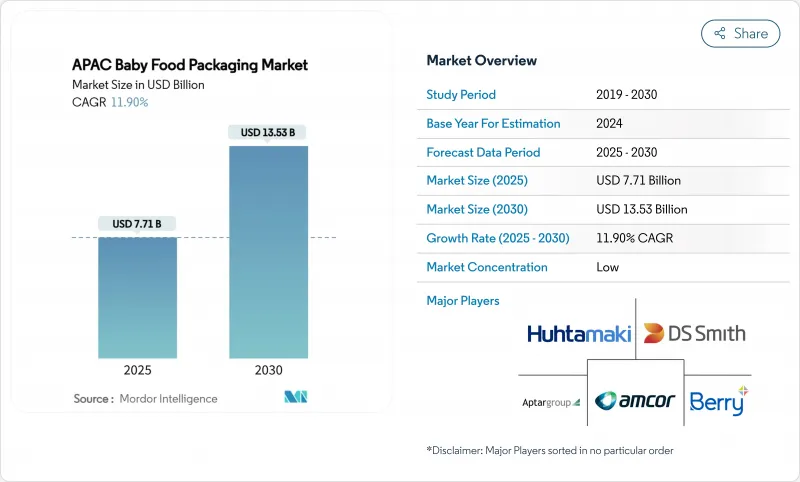

아시아태평양의 이유식 포장 시장 규모는 2025년에 77억 1,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 11.90%로, 2030년에는 135억 3,000만 달러에 달할 것으로 예상됩니다.

이 확장은 이 지역의 인구 역학 기세, 강력한 도시화, 고급 유아 영양에 대한 선호도 증가를 반영합니다. 중국의 추년에 출생 등록이 증가함에 따라 유아용 조제 분유의 초고급품 매출은 44.3% 증가했고 H&H 그룹은 이 가격대에서 15.6%의 점유율을 획득했습니다. 소재의 혁신도 성장의 기폭제입니다. 플라스틱은 2024년에 46.7%의 매출 점유율을 유지했지만, 바이오플라스틱이 CAGR 18.4%로 가장 빠르게 성장하고 있으며, 2025년에 예정된 네이처웍스의 태국에서 6억 달러의 Ingeo PLA 컴플렉스에 지지되고 있습니다. 편의용 파우치 점유율은 이미 33%를 차지하고 있으며 CAGR 15.9%를 나타낼 전망입니다. 지리적 집중은 여전히 눈에 띄고 중국은 35%의 점유율을 차지하는 반면 인도는 2030년까지 연평균 복합 성장률(CAGR)로 가장 빠른 14%로 성장을 지속하고 있습니다. 이유식용 포장의 E-Commerce 판매는 CAGR 19.4%로 가속해, 파손이나 치수 중량을 최소한으로 억제한, 출하를 견디는 경량 포맷에의 축족을 강요 받게 됩니다.

2024년 중국의 유아용 조제 분유 부문은 외국 브랜드가 8%의 매출 성장을 기록하고 슈퍼 프리미엄층이 37%의 점유율을 확보했기 때문에 바닥 견고함을 유지했습니다. APAC의 도시 부모는 안전, 보존 기간 연장, 우수한 영양을 보장하는 제품을 선호하고 다층 장벽 필름과 고급 마감에 대한 수요를 촉구합니다. 세대 간 부의 이동으로 밀레니얼 세대의 구매력은 수제 대체품보다 편의성과 인지된 품질을 우월합니다. 도시와 농촌의 격차는 여전히 남아 있지만, 대도시 중심부는 고밀도 수요 집적지가 되었습니다.

공동 작업 가구는 당황한 일상을 지원하는 포장를 중시합니다. 파우치가 달린 파우치는 이동 중에 모유 수유, 간단한 재봉, 흩어짐을 줄이고 부모의 기대에 부합합니다. 한국과 싱가포르의 풍요로움은 프리미엄에서 물약 통제된 팩의 채택을 가속화하고 베트남과 인도네시아는 여성 노동 참여율이 증가함에 따라 이러한 경향을 반영하기 시작했습니다. 그 때문에 브랜드는 인간공학에 근거한 형상, 소프트 터치의 라미네이트 가공, 한 손으로 사용할 수 있는 퀵 오픈 클로저를 우선하고 있습니다.

인도에서는 2025년까지 많은 경질 카테고리에서 30%의 재활용 함량을 의무화하고 있으며, 연구개발과 인증주기의 가속화를 강요하고 있습니다. 생산자는 인증된 PCR 수지의 비용 증가와 마이그레이션 및 냄새에 대한 엄격한 사양에 직면합니다. 싱가포르와 인도네시아의 병행 조치는 다국적 공급망에 복잡성을 가져야 하며 다른 준수 기한을 양립시켜야 합니다.

2024년 아시아태평양의 이유식 포장 시장은 플라스틱이 46.7%의 매출 점유율을 차지했습니다. 그러나 바이오플라스틱은 태국의 투자촉진체제와 탄소중립에 관한 다국적 브랜드의 맹세에 힘입어 2030년까지의 CAGR이 18.4%로 성장을 지속하고 있습니다. 네이처웍스와 SKC의 생산능력이 석유계 폴리머와의 비용차이를 줄이기 때문에 바이오플라스틱의 아시아태평양의 이유식 포장 시장 규모는 가장 빠르게 성장할 것으로 예측됩니다. 태국과 베트남에서는 정부 보조금에 의해 자본금의 문턱이 내려가고, 바이오 베이스의 PLA와 PBAT 필름은 가공성의 향상에 의해 기존 플렉서블 플라스틱과 동등한 내열성과 씰성을 가지게 되었습니다.

일부 신흥 국가에서는 가격에 대한 민감성이 여전히 보급을 제한하고 있지만 프리미엄 브랜드와 유기농 이유식 브랜드는 브랜드 스토리로 컴포스터블 팩을 사용합니다. 유리 캔은 고급 선물에 사용되고 있지만, 그 무게와 깨지기 쉽기 때문에 전자상거래에서 경쟁력이 떨어지고 있습니다. 금속 캔 수요는 더 가벼운 장벽 라미네이트를 대체하고 있습니다. 판지는 종종 바이오 배리어 코팅과 결합되어 고급 2 차 팩의 틈새를 유지합니다.

2024년 아시아태평양의 이유식 포장 시장에서는 파우치가 33%의 점유율을 차지했습니다. CAGR은 15.9%로 예측되며 유아의 자립 수유를 지원하는 스파우트가 있는 디자인에 밀려있습니다. 따라서 파우치의 아시아태평양의 이유식 포장 시장 규모는 단단한 형식보다 빠르게 확대되고 있습니다. 플라스틱 병은 레이디 투 음료 밀크에 여전히 중요하지만, SIG와 테트라 시스템은 현재 더 낮은 탄소 발자국을 주장하는 단일 소재의 유연성과 경쟁하고 있습니다. 금속 캔은 무게 문제로 인해 선반에 늘어선 매력을 잃고 있으며, 클럽 매장에서는 비슷한 장벽 수준을 제공하는 휘트먼트 스탠드 업 파우치를 대체하고 있습니다.

제조업체는 파우치 물류의 이점을 높이 평가합니다. 소매업체는 소비자가 더 가벼운 형식을 받아들여 선반의 밀도를 높이고 셀 스루를 향상시킬 수 있습니다. 인도네시아와 필리핀에서는 지속가능성에 대한 우려보다 일회용의 편의성이 우선하기 때문에 파우치는 여전히 비용 효율적인 선택이 되고 있습니다. 병은 고급 유기농 퓌레용으로 존속하고 있지만, 유리제보다 경량의 PET제가 동향하고 있습니다.

아시아태평양의 이유식 포장 시장 보고서는 소재별(플라스틱, 판지, 금속, 유리, 바이오플라스틱), 포장 유형별(병, 금속캔, 카톤, 기타), 제품별(건조 이유식, 액체 우유, 분유, 기타), 연령층별(0-6개월, 6-12개월, 1-2세, 2-3세), 유통 채널별(슈퍼마켓 및 하이퍼마켓, 편의점, 기타), 지역별로 분류되어 있습니다.

The APAC Baby Food Packaging Market size is estimated at USD 7.71 billion in 2025, and is expected to reach USD 13.53 billion by 2030, at a CAGR of 11.90% during the forecast period (2025-2030).

This expansion reflects the region's demographic momentum, strong urbanization and the growing preference for premium infant nutrition. Rising birth registrations during China's Year of the Dragon lifted super-premium infant formula sales by 44.3%, while H&H Group captured 15.6% share of that price tier. Material innovation is another growth catalyst. Plastic retained 46.7% revenue share in 2024, yet bioplastics are climbing fastest at 18.4% CAGR, supported by NatureWorks' USD 600 million Ingeo PLA complex in Thailand scheduled for 2025. Convenience-led pouches already hold 33% share and are growing at 15.9% CAGR, reshaping packaging line investments and retail shelf layouts. Geographic concentration remains evident as China commands 35% share, while India is registering the quickest 14% CAGR through 2030. E-commerce sales of baby food packaging accelerate at 19.4% CAGR, forcing a pivot toward shipping-robust, lighter formats that minimize breakage and dimensional weight.

China's infant formula segment stayed resilient in 2024 as foreign brands logged 8% sales growth, with the super-premium tier securing 37% share. Parents in urban APAC favor products that guarantee safety, extended shelf life and superior nutrition, prompting demand for multi-layer barrier films and premium finishes. Generational wealth transfer brings millennial purchasing power that privileges convenience and perceived quality over homemade alternatives. Urban-rural divides remain, yet metropolitan centers have become high-density demand clusters.

Households with two earners value packaging that supports hectic routines. Spouted pouches enable on-the-go feeding, easy resealability and reduced mess, aligning with parental expectations. Affluence in South Korea and Singapore accelerates adoption of premium, portion-controlled packs, while Vietnam and Indonesia are beginning to mirror the trend as female labor participation rises. Brands are therefore prioritizing ergonomic shapes, soft-touch laminates and quick-open closures suitable for one-hand use.

India mandates 30% recycled content by 2025 in many rigid categories, forcing accelerated R&D and qualification cycles. Producers face added costs for certified PCR resin and tighter specifications on migration and odor. Parallel measures in Singapore and Indonesia add complexity for multinational supply chains that must juggle differing compliance deadlines.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Plastic dominated the APAC baby food packaging market in 2024 with 46.7% revenue share. Bioplastics, however, are charting an 18.4% CAGR to 2030, supported by Thailand's pro-investment regime and multinational brand pledges on carbon neutrality. The APAC baby food packaging market size for bioplastics is expected to grow the fastest as capacity from NatureWorks and SKC reduces cost differentials with petro-based polymers. Government subsidies in Thailand and Vietnam lower capital thresholds, while improved processability allows bio-based PLA and PBAT films to match heat resistance and sealing integrity of conventional flexibles.

Price sensitivity still limits uptake in several emerging economies, yet premium and organic baby food brands are using compostable packs as a brand story. Glass maintains relevance in luxury gifting, yet its weight and fragility reduce competitiveness in e-commerce. Metal can demand is retreating in favor of lighter barrier laminates. Paperboard, often coupled with bio-barrier coatings, retains a niche for premium secondary packs.

Pouches held 33% share of the APAC baby food packaging market in 2024. They are forecast to expand at 15.9% CAGR, propelled by spouted designs that support independent toddler feeding. The APAC baby food packaging market size for pouches is therefore widening more quickly than rigid formats. Bottles stay important for ready-to-drink formula, but SIG and Tetra systems now compete with mono-material flexibles that claim lower carbon footprints. Metal cans are losing shelf appeal due to weight penalties and are being displaced in club stores by stand-up pouches with fitments that offer similar barrier levels.

Manufacturers appreciate the logistics benefits of pouches, which reduce inbound freight volumes and warehouse space. Retailers gain faced-up shelf density and improved sell-through as consumers embrace the lighter format. Sachets remain a cost-effective option in Indonesia and the Philippines, where single-use affordability trumps sustainability concerns. Jars persist for premium organic purees but are trending toward lightweight PET rather than glass.

APAC Baby Food Packaging Market Report is Segmented by Material (Plastic, Paperboard, Metal, Glass, Bioplastics), Package Type (Bottles, Metal Cans, Cartons, and More), Product (Dried Baby Food, Liquid Milk Formula, Powder Milk Formula and More), Age Group (0-6 Months, 6-12 Months, 1-2 Years, 2-3 Years), Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores and More), and Geography.