Pharmaceutical Contract Manufacturing Market by Service (Drug Development, Pharmaceutical (API, FDF - Parenteral, Tablet, Capsule), Biologics (API, FDF), Packaging & Labelling, Fill-finish), Molecule (Small, Large (ADC, CGT)) - Global Forecast to 2030

상품코드:1807080

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 522 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

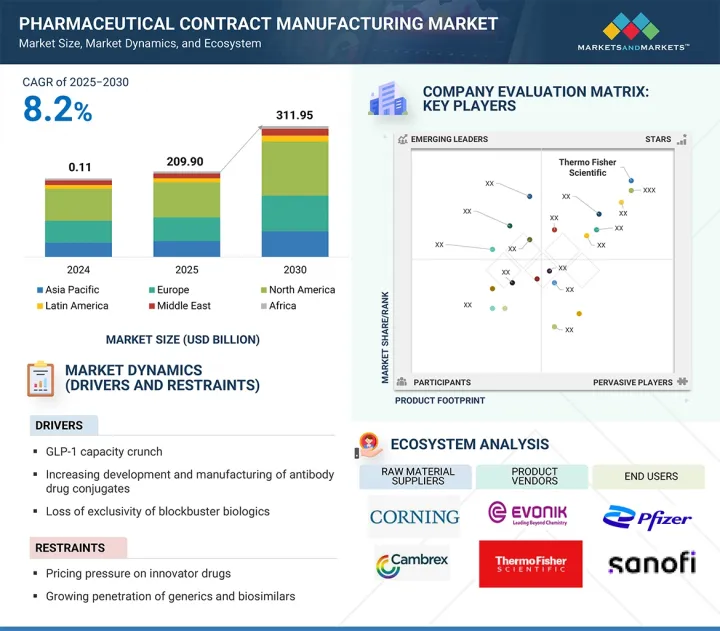

세계의 의약품 수탁 제조 시장 규모는 2025년부터 2030년까지 예측 기간 동안 CAGR 8.2%로 추이해, 2025년 2,099억 달러에서 2030년에는 3,119억 5,000만 달러에 달할 것으로 예측되고 있습니다.

조사 범위

조사 대상 연도

2024-2030년

기준 연도

2024년

예측 기간

2025-2030년

단위

금액(달러)

부문

서비스, 분자, 최종 사용자, 지역

대상 지역

북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카

의약품 수탁 제조 시장의 확대는 주로 GLP-1의 제조 및 개발에서 아웃소싱, ADC(항체 약물 복합체)의 승인 및 프로그램, 블록버스터 생물제제의 독점권 상실에 의해 견인되어 왔습니다. 그러나 제약기업에 의한 사내 제조능력 확대와 미국 및 유럽의 가격압력이 시장 성장을 억제하는 요인이 될 것으로 예측되고 있습니다.

서비스별로는 생물제제 FDF 제조 서비스 부문이 2024년 최대 CAGR을 기록

생물 제제 FDF 제조 서비스는 2025년부터 2030년까지의 예측 기간 동안 가장 빠른 성장률을 보일 것으로 예측됩니다. 이 강한 성장 전망은 단일클론항체, 재조합 단백질, 세포 및 유전자 치료, 백신 등 복잡하고 고부가가치 제품을 포함한 생물제제 수요의 급증에 의해 주로 견인되고 있습니다. 기존의 치료와 비교하여 보다 높은 효능과 부작용 감소를 제공하는 표적화된 약리 요법에 대한 관심 증가는 특수한 생산 능력에 대한 수요를 더욱 밀어 올리고 있습니다.

게다가, 특히 세포 및 유전자 치료에서 연구개발 활동 증가도 시장 확대에 크게 기여하고 있습니다. 이러한 첨단 치료 분야에서 파이프라인 후보 수 증가는 고도로 전문적인 제조 공정을 필요로 하고, 제약 기업에 필요한 전문 지식, 인프라, 규제 준수 능력을 갖춘 CDMO와의 제휴를 촉진하고 있습니다. 이러한 추세는 CDMO의 첨단 생물 제제 생산 기술, 능력 확장 및 품질 시스템에 대한 투자가 증가할 것으로 예측됩니다. 그 결과, FDF 제조 서비스 부문은 향후 수년간 상당한 성장을 이루고 있으며, 의약품 아웃소싱 분야에서 점점 중요한 역할을 할 것으로 기대되고 있습니다.

분자별로는 저분자 부문이 2024년 시장에서 지배적 위치를 차지

2024년에는 고활성 저분자, 올리고뉴클레오티드 및 합성 펩타이드, 방사성 의약품 등의 저분자 부문이 시장에서 가장 큰 점유율을 차지했습니다. 고활성 저분자, 특히 암 영역은 특수한 봉쇄 설비와 전문 지식을 필요로 하기 때문에 고급 시설을 가진 CDMO에 대한 수요를 견인하고 있습니다. 올리고뉴클레오티드 및 합성 펩티드는 정밀의료 및 표적 치료에서의 역할에서 기세를 늘리고 새로운 아웃소싱 기회를 제공합니다.

방사성 의약품은 진단 및 치료에 적용됨에 따라 핵 의학이 확대됨에 따라 관심이 커지고 있습니다. 다른 저분자는 심혈관 질환에서 감염에 이르는 많은 치료 분야에서 여전히 중요합니다. 저분자는 안정성, 경구 생체이용률 및 비용 효율적인 대량 생산성을 통해 혁신적인 의약품 및 제네릭 의약품 파이프라인 모두에서 매력적입니다. 만성 질환의 유병률이 증가하는 것 외에도 합성 화학 및 연속 생산의 지속적인 혁신이 시장에서의 입지를 강화하고 있습니다. 이러한 하위 범주에 특화된 전문 지식을 갖춘 CDMO는 속도, 유연성 및 비용 효율성을 요구하는 제약 기업의 강한 수요를 활용할 수 있으며, 저분자가 CDMO 산업 성장의 핵심 추진력임을 보장합니다.

지역별로는 북미가 가장 큰 점유율을 차지했습니다.

북미는 견고한 규제 프레임워크, 고급 제조 인프라, 주요 CDMO의 높은 집중도에 힘입어 2024년 시장을 지배했습니다. 이 지역은 확립된 제약 산업, 광범위한 R&D 능력, 비용 최적화 및 시장 진입 속도 향상을 위해 개발 및 제조를 아웃소싱하는 주요 제약 회사의 강력한 존재감의 혜택을 누리고 있습니다. 특히 미국 FDA를 중심으로 한 지원적인 규제 당국은 명확한 지침과 신속한 승인을 통해 혁신을 촉진하고, 연속 생산과 고활성 API 제조 등 선진적인 제조 기술에 대한 투자를 장려하고 있습니다. 북미는 또한 세포 및 유전자 치료에 대응하는 전문적인 CDMO 시설에 지지되어 생물 제제나 선진 치료의 제조에서도 주도적 지위를 차지하고 있습니다. 전략적 제휴, 합병 및 인수는 서비스 포트폴리오와 능력을 더욱 강화하고 있습니다. 이 지역의 견고한 벤처 캐피탈 에코시스템과 산학 협력은 혁신을 촉진하고 품질, 컴플라이언스 및 확장성에 중점을 둔 세계 고객을 끌어들이고 있습니다.

본 보고서에서는 세계의 의약품 수탁 제조 시장을 조사했으며, 시장 개요, 시장 성장에 대한 각종 영향요인 분석, 기술 및 특허 동향, 법규제 환경, 사례 연구, 시장 규모 추이와 예측, 각종 구분 및 지역/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

시장 역학

성장 촉진요인

억제요인

기회

과제

고객의 사업에 영향을 미치는 동향/혼란

가격 분석

밸류체인 분석

공급망 분석

생태계 분석

투자 및 자금조달 시나리오

기술 분석

특허 분석

2025-2026년 주요 회의 및 이벤트

규제 상황

Porter's Five Forces 분석

주요 이해관계자와 구매 기준

최종 사용자의 미충족 요구

단순화된 신약 신청(ANDA) 승인

AI/생성형 AI가 의약품 수탁 제조 시장에 미치는 영향

2025년 미국 관세가 의약품 수탁 제조 시장에 미치는 영향

제6장 의약품 수탁 제조 시장 : 서비스별

의약품 제조 서비스

의약품 API 제조 서비스

의약품 FDF 제조 서비스

의약품 개발 서비스

생물 제제 제조 서비스

생물 제제 API 제조 서비스

생물 제제 FDF 제조 서비스

포장 및 라벨 서비스

충전 마감 서비스

기타

제7장 의약품 수탁 제조 시장 : 분자별

저분자

고효력 저분자

올리고뉴클레오티드 및 합성 펩티드

방사성 의약품 분자

기타

고분자

단일클론항체

세포 및 유전자 치료

항체 약물 복합체

백신

치료용 펩타이드 및 단백질

기타

제8장 의약품 수탁 제조 시장 : 최종 사용자별

주요 의약품 기업

중소규모 의약품 기업

제네릭 의약품 기업

기타

제9장 의약품 수탁 제조 시장 : 지역별

북미

거시경제 전망

미국

캐나다

유럽

거시경제 전망

독일

영국

프랑스

이탈리아

스위스

폴란드

스페인

기타

아시아태평양

거시경제 전망

중국

일본

한국

인도

호주

기타

라틴아메리카

거시경제 전망

브라질

멕시코

기타

중동

거시경제 전망

GCC 국가

기타

아프리카

거시경제 전망

제10장 경쟁 구도

주요 진입기업의 전략 및 강점

수익 점유율 분석

시장 점유율 분석

기업 평가와 재무지표

브랜드 및 서비스 비교

기업 평가 매트릭스 : 주요 기업

기업 평가 매트릭스 : 스타트업 및 중소기업

경쟁 시나리오

제11장 기업 프로파일

주요 기업

THERMO FISHER SCIENTIFIC INC.

LONZA

CATALENT, INC.

WUXI APPTEC

WUXI BIOLOGICS

SAMSUNG BIOLOGICS

BOEHRINGER INGELHEIM INTERNATIONAL GMBH

EVONIK

FUJIFILM HOLDINGS CORPORATION

ABBVIE INC.

SIEGFRIED HOLDING AG

MERCK KGAA

ALMAC GROUP

CHARLES RIVER LABORATORIES

ASYMCHEM INC.

VETTER

ALCAMI CORPORATION

EUROFINS SCIENTIFIC

기타 기업

PIRAMAL PHARMA SOLUTIONS

SYNGENE INTERNATIONAL LIMITED

CAMBREX CORPORATION

JUBILANT PHARMANOVA LIMITED

YUHAN CORPORATION

PIERRE FABRE LABORATORIES

PFIZER CENTREONE

DELPHARM

FRONTAGE LABS

SHARP SERVICES, LLC

GRAND RIVER ASEPTIC MANUFACTURING

RECIPHARM AB

PCI PHARMA SERVICES

CURIA GLOBAL, INC.

SIMTRA BIOPHARMA SOLUTIONS

PORTON

MABPLEX INTERNATIONAL CO. LTD.

CELLARES

제12장 부록

JHS

영문 목차

영문목차

The global pharmaceutical contract manufacturing market is projected to reach USD 311.95 billion by 2030 from an estimated USD 209.90 billion in 2025, at a CAGR of 8.2% from 2025 to 2030.

Scope of the Report

Years Considered for the Study

2024-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD billion)

Segments

By Service, Molecule, End User, and Region

Regions covered

North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

The expansion of the pharmaceutical contract manufacturing market has been predominantly fueled by outsourcing for GLP-1 manufacturing & development, ADC approvals and programs, and loss of exclusivity for blockbuster biologics. However, expansion of in-house capacities by pharmaceutical companies and pricing pressure in the US and Europe are expected to restrict market growth.

The biologics FDF manufacturing services segment reported the highest CAGR in 2024.

Based on biologics manufacturing service, the pharmaceutical contract manufacturing market is segmented into biologics API manufacturing services and biologics FDF Manufacturing Services. Among these, biologics FDF manufacturing services are projected to experience the fastest growth rate during the forecast period from 2025 to 2030. This strong growth outlook is primarily driven by the surging demand for biologics, which include complex and high-value products such as monoclonal antibodies, recombinant proteins, cell and gene therapies, and vaccines. The rising focus on targeted pharmacological therapies, which offer greater efficacy and reduced side effects compared to traditional treatments, is further boosting demand for specialized manufacturing capabilities. In addition, the increasing volume of research and development activities, particularly in cell and gene therapy, contributes significantly to market expansion. A growing number of pipeline candidates in these advanced therapeutic areas requires highly specialized manufacturing processes, encouraging pharmaceutical companies to partner with CDMOs possessing the necessary expertise, infrastructure, and regulatory compliance. This trend is expected to result in higher investment in advanced biologics production technologies, capacity expansion, and quality systems within CDMOs. Consequently, the FDF manufacturing services segment is well-positioned to achieve substantial growth and play an increasingly critical role in the pharmaceutical outsourcing landscape over the coming years.

The small molecules segment dominated the pharmaceutical contract manufacturing market in 2024.

The pharmaceutical contract manufacturing market is segmented by molecules into small molecules & large molecules. In 2024, small molecules, encompassing high-potency small molecules, oligonucleotides and synthetic peptides, radiopharmaceuticals, and other small molecules, hold the largest share of the pharmaceutical CDMO market by molecule segment. High-potency small molecules, particularly oncology, require specialized containment and expertise, driving demand for CDMOs with advanced facilities. Oligonucleotides and synthetic peptides have gained momentum due to their role in precision medicine and targeted therapies, offering new outsourcing opportunities. Radiopharmaceuticals, with applications in diagnostics and treatment, are seeing increased interest as nuclear medicine expands. The other small molecules category remains vital for numerous therapeutic areas, from cardiovascular to infectious diseases. Small molecules are favored for their stability, oral bioavailability, and cost-efficient mass production, making them attractive for both innovative and generic drug pipelines. The growing prevalence of chronic conditions, coupled with ongoing innovation in synthetic chemistry and continuous manufacturing, strengthens their market position. CDMOs with specialized expertise across these subcategories can leverage strong demand from pharmaceutical companies seeking speed, flexibility, and cost efficiency, ensuring that small molecules continue to be a core driver of the CDMO industry's growth.

North America accounted for the largest share in the global pharmaceutical contract manufacturing market from 2025 to 2030.

North America dominated the pharmaceutical CDMO market in 2024, driven by its strong regulatory framework, advanced manufacturing infrastructure, and high concentration of leading CDMO players. The region benefits from a well-established pharmaceutical industry, extensive R&D capabilities, and a strong presence of big pharmaceutical companies outsourcing development and manufacturing to optimize costs and speed to market. Supportive regulatory agencies, particularly the US FDA, promote innovation through clear guidelines and expedited approvals, encouraging investment in advanced manufacturing technologies such as continuous processing and high-potency API production. North America also leads in biologics and advanced therapies manufacturing, supported by specialized CDMO facilities catering to cell and gene therapies. Strategic collaborations, mergers, and acquisitions further enhance service portfolios and capacity. The region's robust venture capital ecosystem and academic-industry partnerships foster innovation, while its focus on quality, compliance, and scalability attracts global clients.

The primary interviews conducted for this report can be categorized as follows:

By Respondent: Supply Side- 70% and Demand Side- 30%

By Designation: Managers- 45%, CXO and Directors- 30%, and Executives- 25%

By Region: North America- 30%, Europe- 30%, Asia Pacific- 30%, Latin America- 5%, and the Middle East & Africa- 5%

Key Companies

Key players in the pharmaceutical contract manufacturing market include Thermo Fisher Scientific Inc. (US), Lonza (Switzerland), WuXi AppTec (China), WuXi Biologics (China), AbbVie Inc. (US), Catalent, Inc. (Novo Holdings) (US), Samsung Biologics (South Korea), Evonik (Germany), FUJIFILM Holding Corporation (Japan), Siegfried Holding AG (Switzerland), and Boehringer Ingelheim International GmbH (Germany). Other notable companies are Merck KGaA (Germany), Almac Group (UK), Charles River Laboratories (US), Asymchem Inc. (China), Vetter (Germany), and Alcami Corporation (US).

Research Coverage

This research report categorizes the pharmaceutical contract manufacturing market, by service {drug development services, pharmaceutical manufacturing services [pharmaceutical API manufacturing services, pharmaceutical FDF manufacturing services (parenteral, tablet, capsule, oral liquid, semi-solid, other formulations), biologics manufacturing services (biologics API manufacturing services, biologics FDF manufacturing services)], packaging & labelling services, fill-finish services, other services}, molecule [small molecules (high-potency small molecules, oligonucleotide & synthetic peptides, radiopharmaceutical, and other molecules) large molecules (mAbs, CGT, ADC, vaccines, therapeutic peptides & proteins, and other large molecules)], end user (big pharmaceutical companies, small & mid-sized pharmaceutical companies, generic pharmaceutical companies, other end users), and by region (North America, Europe, Asia Pacific, Latin America, Middle East, and Africa). The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the pharmaceutical contract manufacturing market. A detailed analysis of the key industry players has been done to provide insights into their business overview, solutions, key strategies, collaborations, partnerships, and agreements. New launches, collaborations, acquisitions, and recent developments associated with the pharmaceutical contract manufacturing market.

Reasons to buy this report

The report will help market leaders and new entrants by providing them with closest approximations of the revenue numbers for the overall pharmaceutical contract manufacturing market and its subsegments. It will also help stakeholders better understand the competitive landscape and gain more insights to better positioning their businesses and make suitable go-to-market strategies. This report will enable stakeholders to understand the market's pulse and provide them with information on the key market drivers, restraints, opportunities, and challenges.

The report provides insights into the following pointers:

Analysis of key drivers (GLP-1 capacity crunch, increasing development and manufacturing of antibody drug conjugates, loss of exclusivity of blockbuster biologics, increasing complexity of injectable drug formats) restraints (pricing pressure on innovator drugs, growing penetration of generics and biosimilars, strict regulatory compliance, risk in advanced therapies pipeline), opportunities (Rising demand for cell and gene therapies, growing inclination toward one-stop-shop model, market expansion in emerging countries, booming radiopharmaceutical and nuclear medicine segment), and challenges (global trade instability and insourcing) influencing the growth of pharmaceutical contract development and manufacturing market.

Service Development/Innovation: Thorough investigation of recently launched services available in the pharmaceutical contract manufacturing market.

Market Development: Utilizing analysis of regional market trends, the study offers comprehensive knowledge on profitable markets.

Market Diversification: Comprehensive information on new services, underdeveloped areas, present developments, and pharmaceutical contract manufacturing sector investments is what market diversification is based on.

Competitive Assessment: A comprehensive evaluation of the market shares, growth strategies, and service offerings of prominent companies such as Thermo Fisher Scientific Inc. (US), Catalent, Inc. (US), Lonza (Switzerland), AbbVie Inc. (US), WuXi AppTec (China), and others in the pharmaceutical contract development and manufacturing market.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 STAKEHOLDERS

1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key objectives of secondary research

2.1.1.2 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Breakdown of primaries

2.1.2.2 Key objectives of primary research

2.2 MARKET SIZE ESTIMATION

2.2.1 GLOBAL MARKET ESTIMATION

2.2.1.1 Company revenue analysis (Bottom-up approach)