Artificial Intelligence in Manufacturing Market by Processor (MPUS, GPUs, FPGA, ASICs), Software (On-premises, Cloud), Technology (Machine Learning, NLP, Context-aware Computing, Computer Vision, Generative Al), Application - Global Forecast to 2030

상품코드:1802923

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 335 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

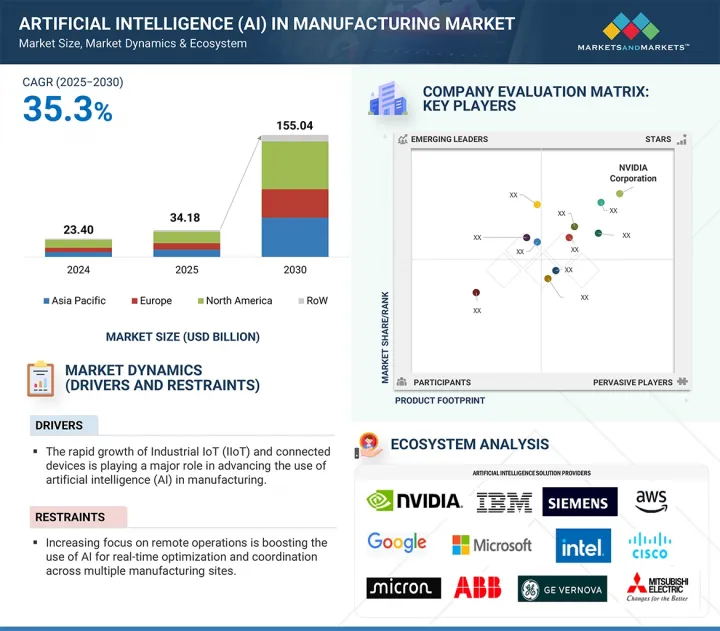

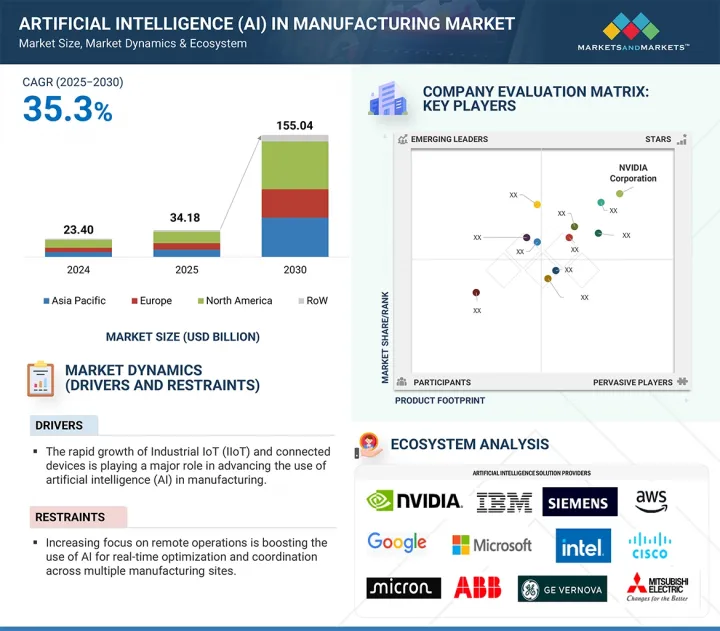

세계의 제조용 AI 시장은 2025년 341억 8,000만 달러에서 2030년까지 1,550억 4,000만 달러에 달할 것으로 예측되며, CAGR로 35.3%의 성장이 전망됩니다.

이러한 강력한 성장은 생산 워크플로우 간소화, 실시간 의사결정 강화, 다양한 제조 업무에 걸친 예지보전 지원을 위한 AI 기술의 급속한 채택에 기인하고 있습니다. 제조업계가 민첩성, 비용 효율성, 품질 보증을 향상시키기 위해 노력하고 있는 가운데, AI 솔루션은 새로운 차원의 비즈니스 인텔리전스와 생산성을 이끌어내는 데 중요한 역할을 하고 있습니다. 자동차, 전자, 항공우주, 소비재 등의 산업에서 머신러닝, 컴퓨터 비전, 자연 언어 처리를 활용하여 생산 스케줄링 최적화, 다운타임 감소, 공정 초기 단계의 이상 징후를 감지하고 있습니다.

조사 범위

조사 대상연도

2021-2030년

기준연도

2024년

예측 기간

2025-2030년

단위

10억 달러

부문

제공, 용도, 기술, 산업, 지역

대상 지역

북미, 유럽, 아시아태평양, 기타 지역

AI 지원 로봇, 디지털 트윈, 지능형 품질관리 시스템을 통해 제조업체는 정확하고 적응력 있게 생산을 확장할 수 있습니다. 또한 산업용 IoT 플랫폼과 클라우드 기반 데이터 분석에 AI를 통합하여 커넥티드 데이터베이스 생태계를 구현하고 스마트 팩토리로의 전환을 가속화합니다. 지속가능성, 경쟁 대응, 국제 경쟁력이 강조되는 가운데, AI는 차세대 제조 패러다임 형성에 있으며, 변혁적인 역할을 할 것입니다. 지능형 자동화 및 지속적인 프로세스 혁신에 대한 수요가 증가함에 따라 제조용 AI 시장은 모든 지역과 산업에서 지속적으로 확대될 것으로 예측됩니다.

"용도별로는 예지보전 부문이 2024년 가장 큰 시장 점유율을 차지했습니다. "

2024년, 장비 고장 최소화, 운영 중단 시간 단축, 자산 성능 최적화에 대한 관심이 높아지면서 예지보전 부문이 제조용 AI 시장의 주요 용도로 부상했습니다. 각 산업의 제조업체들은 센서 데이터 분석, 이상 감지, 장비 고장 사전 예측을 위해 AI를 활용한 예지보전 시스템 도입을 늘리고 있습니다. 이러한 접근 방식은 적시에 목표에 맞는 개입을 가능하게 하여 기업이 비용이 많이 드는 중단을 피하고 전반적인 생산 효율을 향상시키는 데 도움이 됩니다. 자동차, 중장비, 에너지 및 전력, 반도체 및 전자제품 제조 등 주요 부문은 특히 계획되지 않은 가동 중단이 큰 손실로 이어질 수 있는 대량 생산 및 자본 집약적 업무에서 예지보전을 우선시했습니다.

IoT 및 클라우드 플랫폼과 통합된 AI 알고리즘은 실시간 상태 모니터링 및 지능형 진단을 가능하게 하여 기존의 반응형 유지보수 및 시간 기반 유지보수 모델에 비해 분명한 우위를 점하고 있습니다. 고장을 예측하고, 유지보수 일정을 최적화하고, 예비 부품의 낭비를 줄이기 위해 AI를 통한 지식이 광범위하게 활용된 것이 이 부문의 우위에 크게 기여했습니다. 또한 장비 가동시간 향상, 자산 수명 연장, 인건비 절감을 통한 예지보전을 통한 투자 회수는 제조업체의 전략적 우선순위가 되고 있습니다. 공장이 더욱 스마트하고 데이터 중심적인 경영을 위해 계속 진화하는 가운데, 2024년에도 예지보전은 제조 분야에서 가장 영향력 있는 AI 활용 분야로 자리매김할 것으로 보입니다.

"기술별로는 머신러닝 분야가 가장 큰 시장 점유율을 차지했습니다. "

2024년, 머신러닝 부문이 제조용 AI 시장에서 가장 큰 점유율을 차지했습니다. 이는 산업 전반에 걸쳐 데이터베이스 의사결정, 프로세스 최적화, 적응형 자동화를 가능하게 하는 데 핵심적인 역할을 하고 있음을 반영합니다. 제조업체들은 센서, 기계, 기업 시스템에서 생성되는 대량의 업무 데이터를 분석하여 기존 방식으로는 감지할 수 없었던 패턴과 추세를 발견하기 위해 머신러닝 알고리즘에 대한 의존도를 높이고 있습니다. 이를 통해 기업은 생산 효율성을 높이고, 품질관리를 개선하며, 변화하는 시장 수요에 신속하게 대응할 수 있게 되었습니다. 자동차, 전자, 금속 및 중장비 제조 등의 산업에서 수요 예측 및 예지보전부터 이상 감지 및 공정 최적화까지 다양한 용도로 머신러닝을 활용하고 있습니다. 실시간 데이터를 기반으로 지속적으로 학습하고 모델을 개선하는 이 기술의 능력은 복잡한 경영 및 변동성이 크고 역동적인 환경에서 특히 유용하게 활용될 수 있습니다. 머신러닝이 산업용 IoT 플랫폼, 클라우드 컴퓨팅, 엣지 디바이스와 통합되면서 이산 제조와 공정 제조 모두에서 머신러닝의 활용이 크게 확대되었습니다. 의사결정을 자동화하고, 인적 오류를 줄이고, 숨겨진 비효율성을 발견하는 능력은 기초 AI 기술로서 머신러닝의 우위를 강화했습니다. 제조업이 더 높은 민첩성, 확장성, 경쟁 우위를 추구하는 가운데, 머신러닝은 제조용 AI 환경에서 가장 널리 도입되고 영향력 있는 기술로 부상했습니다.

세계의 제조용 AI 시장에 대해 조사분석했으며, 주요 촉진요인과 억제요인, 경쟁 구도, 향후 동향 등의 정보를 제공하고 있습니다.

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 중요 인사이트

제조용 AI기업에 매력적인 기회

제조용 AI 시장의 제공

제조용 AI 시장 : 기술별

제조용 AI 시장 : 산업별

제조용 AI 시장 : 용도별

제조용 AI 시장 : 국가별

제5장 시장 개요

서론

시장 역학

촉진요인

억제요인

기회

과제

밸류체인 분석

에코시스템 분석

고객 비즈니스에 영향을 미치는 동향/혼란

Porter's Five Forces 분석

주요 이해관계자와 구입 기준

사례 연구 분석

EASTMAN CHEMICAL COMPANY, GE VERNOVA가 제공하는 AI 드리븐 신뢰성 프로그램으로 기기 모니터링을 변혁

HARTING TECHNOLOGY GROUP, MICROSOFT와 SIEMENS의 AI를 활용한 엔지니어링으로 커넥터 설계를 가속

RENISHAW PLC, SIEMENS의 NX CAM 소프트웨어를 사용하여 정도를 향상하고, 스크랩을 삭감

MITSUBISHI MOTORS CORPORATION, IBM과 제휴하여 보다 효율적이고 민첩한 미래를 향해 업무 개혁을 시행

SHELL, MICROSOFT와 C3.AI가 제공하는 AI 솔루션을 활용하여 예지보전에서 운영 효율성과 확장성을 실현

기술 분석

주요 기술

보완 기술

인접 기술

가격결정 분석

주요 기업이 제공하는 프로세서의 평균 판매 가격 : 유형별(2024년)

주요 기업이 제공하는 프로세서의 가격대 : 유형별(2024년)

GPU의 평균 판매 가격 동향 : 지역별(2021-2024년)

FPGA의 평균 판매 가격 동향 : 지역별(2021-2024년)

투자와 자금조달 시나리오

무역 분석

수입 시나리오(HS 코드 8471)

수출 시나리오(HS 코드 8471)

특허 분석

주요 컨퍼런스와 이벤트(2025-2026년)

규제 상황

2025년 미국 관세의 영향 - 개요

서론

주요 관세율

가격의 영향 분석

국가/지역에 대한 영향

산업에 대한 영향

제조용 AI 채택의 전략적 로드맵(2024-2030년)

신규 지역의 핫스팟

제조용 AI의 미래

생성형 AI와 시뮬레이션 구동형 설계

자율형·협동형 로봇

디지털 트윈과 AI 드리븐 공장 계획

AI를 활용한 지속가능성과 에너지 효율

제조 에코시스템 전체에 걸친 AI의 확장

제6장 제조용 AI 시장 : 제공별

서론

하드웨어

프로세서

기억장치

네트워크 디바이스

소프트웨어

AI 솔루션

AI 플랫폼

서비스

배포·통합

지원·정비

제7장 제조용 AI 시장 : 기술별

서론

기계학습

심층학습

지도 학습

강화 학습

비지도 학습

기타

자연언어처리

상황 인식 컴퓨팅

컴퓨터 비전

생성형 AI

제8장 제조용 AI 시장 : 용도별

서론

재고 최적화

예지보전·기계 검사

생산계획

필드 서비스

레크라메이션

품질관리

사이버 보안

산업용 로봇

제9장 제조용 AI 시장 : 산업별

서론

자동차

에너지·전력

의약품

금속·중기

반도체·전자

식품 및 음료

기타 산업

제10장 제조용 AI 시장 : 지역별

서론

북미

북미의 미시경제 전망

미국

캐나다

멕시코

유럽

유럽의 미시경제 전망

독일

영국

프랑스

이탈리아

폴란드

스페인

북유럽

기타 유럽

아시아태평양

중국

일본

한국

인도

호주

말레이시아

태국

인도네시아

베트남

기타 아시아태평양

기타 지역

중동

아프리카

남미

제11장 경쟁 구도

개요

주요 참여 기업의 전략/강점(2023-2025년)

매출 분석(2020-2024년)

시장 점유율 분석(2024년)

기업의 평가와 재무 지표

브랜드의 비교

기업 평가 매트릭스 : 주요 기업(2024년)

기업 평가 매트릭스 : 스타트업/중소기업(2024년)

경쟁 시나리오

제12장 기업 개요

주요 기업

NVIDIA CORPORATION

IBM

SIEMENS

ABB

HONEYWELL INTERNATIONAL INC.

GE VERNOVA

GOOGLE LLC

MICROSOFT

MICRON TECHNOLOGY, INC.

INTEL CORPORATION

AMAZON WEB SERVICES, INC.

ROCKWELL AUTOMATION

SAP SE

ORACLE

MITSUBISHI ELECTRIC CORPORATION

PTC

SCHNEIDER ELECTRIC

기타 기업

CISCO SYSTEMS, INC.

HEWLETT PACKARD ENTERPRISE DEVELOPMENT LP

DASSAULT SYSTEMES

PROGRESS SOFTWARE CORPORATION

ZEBRA TECHNOLOGIES CORP.

UBTECH ROBOTICS CORP LTD

AQUANT

BRIGHT MACHINES, INC.

AVATHON

SIGHT MACHINE

제13장 부록

KSA

영문 목차

영문목차

With a CAGR of 35.3%, the global AI in manufacturing market is anticipated to rise from USD 34.18 billion in 2025 to USD 155.04 billion by 2030. This robust growth is being driven by the rapid adoption of AI technologies to streamline production workflows, enhance real-time decision making, and support predictive maintenance across diverse manufacturing operations. As manufacturers strive for greater agility, cost efficiency, and quality assurance, AI solutions are becoming instrumental in unlocking new levels of operational intelligence and productivity. Industries such as automotive, electronics, aerospace, and consumer goods are leveraging machine learning, computer vision, and natural language processing to optimize production scheduling, reduce downtime, and detect anomalies early in the process.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Billion)

Segments

By Offering, Application, Technology, Industry, and Region

Regions covered

North America, Europe, APAC, RoW

The use of AI-enabled robots, digital twins, and intelligent quality control systems allows manufacturers to scale output with precision and adaptability. Additionally, AI integration with industrial IoT platforms and cloud-based data analytics accelerates the transition to smart factories by enabling connected, data-driven ecosystems. With growing emphasis on sustainability, customization, and global competitiveness, AI is set to play a transformative role in shaping next-generation manufacturing paradigms. As the demand for intelligent automation and continuous process innovation intensifies, the AI in manufacturing market is poised for sustained expansion across all regions and industry verticals.

"By Application, Predictive Maintenance Segment Held the Largest Market Share in 2024."

In 2024, the predictive maintenance segment emerged as the leading application in the AI in manufacturing market, driven by the growing emphasis on minimizing equipment failures, reducing operational downtime, and optimizing asset performance. Manufacturers across industries increasingly adopted AI-powered predictive maintenance systems to analyze sensor data, detect anomalies, and forecast equipment failures before they occurred. This approach enabled timely and targeted interventions, helping companies avoid costly disruptions and improve overall production efficiency. Key sectors such as automotive, heavy machinery, energy & power, and semiconductor & electronics manufacturing prioritized predictive maintenance, particularly in high-volume and capital-intensive operations where unplanned outages could result in significant losses.

AI algorithms, integrated with IoT and cloud platforms, enabled real-time condition monitoring and intelligent diagnostics, offering a clear advantage over traditional reactive or time-based maintenance models. The widespread use of AI-driven insights to anticipate failures, optimize maintenance schedules, and reduce spare part wastage contributed significantly to the segment's dominance. Additionally, the return on investment from predictive maintenance through improved equipment uptime, extended asset life, and reduced labor costs made it a strategic priority for manufacturers. As factories continued to evolve toward smarter, data-centric operations, predictive maintenance firmly held its position as the most impactful AI application in the manufacturing sector in 2024.

"By Technology, the Machine Learning Segment Held the Largest Market Share."

In 2024, the machine learning segment accounted for the largest share of the AI in manufacturing market, reflecting its central role in enabling data-driven decision making, process optimization, and adaptive automation across the industry. Manufacturers increasingly relied on machine learning algorithms to analyze large volumes of operational data generated by sensors, machines, and enterprise systems, uncovering patterns and trends that traditional methods could not detect. This allowed companies to enhance production efficiency, improve quality control, and respond swiftly to changing market demands. Industries such as automotive, electronics, and metals & heavy machinery manufacturing have adopted machine learning to drive a range of applications, from demand forecasting and predictive maintenance to anomaly detection and process optimization. The technology's ability to continuously learn and refine models based on real-time data made it especially valuable in dynamic environments with complex operations and high variability. The integration of machine learning with industrial IoT platforms, cloud computing, and edge devices significantly expanded its use across both discrete and process manufacturing. The ability to automate decision-making, reduce human error, and uncover hidden inefficiencies reinforced machine learning's dominance as a foundational AI technology. As manufacturers pursued greater agility, scalability, and competitiveness, machine learning emerged as the most widely implemented and impactful technology within the AI in manufacturing landscape.

"By Region, Europe Recorded Significant Growth in the AI in Manufacturing Market During the Forecast Period."

Europe is expected to witness significant growth in the AI in manufacturing market, supported by a strong focus on industrial modernization, digital innovation, and automation-led competitiveness. Manufacturers will continue to embrace AI technologies to improve productivity, reduce operational inefficiencies, and meet evolving regulatory and sustainability standards. Government-led initiatives across various European nations have played a significant role in accelerating AI integration within the manufacturing sector. Investments in research and development, along with supportive policies for smart factory development, have created a favorable environment for AI adoption.

Additionally, the presence of a highly skilled workforce, advanced industrial infrastructure, and well-established digital ecosystems has enabled faster deployment of AI solutions across the region. European manufacturers are increasingly leveraging AI to enhance production intelligence, implement real-time monitoring, and support autonomous decision-making. The emphasis on quality, precision, and traceability has further driven the demand for AI technologies that enable continuous improvement and adaptive control. As the region balances the goals of industrial innovation and environmental responsibility, AI adoption is expected to remain a key enabler of its manufacturing transformation, reinforcing Europe's position as a major contributor to the global AI in manufacturing market.

Breakdown of primaries

A variety of executives from key organizations operating in the AI in manufacturing market, including CEOs, marketing directors, and innovation and technology directors, were interviewed in depth.

By Company Type: Tier 1 - 45%, Tier 2 - 35%, and Tier 3 - 20%

By Designation: Directors - 45%, C-level - 30%, and Others - 25%

By Region: North America - 45%, Europe - 25%, Asia Pacific - 20%, and RoW - 10%

Note: Other designations include sales and product managers and project engineers. The three tiers of the companies are defined based on their total revenue in 2024: Tier 1 - revenue >= USD 1 billion; Tier 2 - revenue USD 100 million-USD 1 billion; and Tier 3 revenue < USD 100 million.

Major players profiled in this report are as follows:

Siemens (Germany), NVIDIA Corporation (US), IBM (US), Intel Corporation (US), GE Vernova (US), Google (US), Micron Technology, Inc (US), Microsoft (US), Amazon Web Services, Inc (US), Rockwell Automation (US), ABB (Switzerland), Honeywell International Inc. (US), Cisco Systems, Inc. (US), Hewlett Packard Enterprise Development LP (US), SAP SE (Germany), Mitsubishi Electric Corporation (Japan), Oracle (US), Dassault Systemes (France), Sight Machine ( US), Progress Software Corporation (US), Aquant (US), Bright Machines, Inc. (US), Avathon, Inc. (US), and Zebra Technologies Corp. (US).

The study provides a detailed competitive analysis of these key players in the AI in manufacturing market, presenting their company profiles, most recent developments, and key market strategies.

Study Coverage

In this report, the AI in manufacturing market has been segmented based on offering, technology, application, industry, and region. The offering segment includes hardware, software, & services. The technology segment comprises machine learning, natural language processing, context-aware computing, computer vision, and generative AI. The application segment comprises inventory optimization, predictive maintenance & machinery inspection, production planning, field services, reclamation, quality control, cybersecurity, and industrial robots. The industry segment comprises semiconductor & electronics, energy & power, pharmaceuticals, automotive, metals & heavy machinery, food & beverages, and other industries. The market has been segmented into four regions - North America, Asia Pacific, Europe, and Rest of the World (RoW).

Reasons to buy the report

The report will help the leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall market and the sub-segments. It will also help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the AI in manufacturing market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

Key Benefits of Buying the Report

Analysis of key drivers (The proliferation of industrial IoT and connected devices is enabling seamless integration of AI across factory ecosystems. Data-driven decision making and process intelligence are becoming central to modern manufacturing strategies, allowing companies to uncover inefficiencies, optimize production schedules, and reduce variability through AI-powered insights. Enhanced human-machine collaboration, or augmented intelligence, is improving shop floor productivity by empowering workers with AI-assisted tools and systems), restraints (Data quality and availability challenges continue to limit the full potential of AI in manufacturing. The complexity in scaling AI from pilot projects to full-scale production environments presents a significant hurdle), opportunities (Increasing focus on remote operations is boosting the use of AI for real-time optimization and coordination across multiple manufacturing sites. Growing demand for personalized products is driving AI adoption to enable flexible, small-batch production tailored to individual customer needs), and challenges (Difficulty in managing real-time AI decision feedback loops limits responsiveness and disrupts tightly synchronized production workflows. Frequent changes in materials, processes, or demand patterns challenge the ability to keep AI models updated, reducing their accuracy and long-term effectiveness in dynamic manufacturing environments) influencing the growth of the AI in manufacturing market is available in the report.

Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, new product launches in the AI in manufacturing market are available.

Market Development: Comprehensive information about lucrative markets - the report analyses the AI in manufacturing market across regions.

Market Diversification: Exhaustive information about new products/services, untapped geographies, recent developments, and investments in the AI in manufacturing market.

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as NVIDIA Corporation (US), IBM (US), Siemens (Germany), Intel Corporation (US), Amazon Web Services, Inc. (US), and others.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 STAKEHOLDERS

1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY AND PRIMARY RESEARCH

2.1.2 SECONDARY DATA

2.1.2.1 List of secondary sources

2.1.2.2 Key data from secondary sources

2.1.3 PRIMARY DATA

2.1.3.1 List of participants in primary interviews

2.1.3.2 Key data from primary sources

2.1.3.3 Key industry insights

2.1.3.4 Breakdown of primaries

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.1.1 Approach to estimate market size using bottom-up analysis (demand side)

2.2.2 TOP-DOWN APPROACH

2.2.2.1 Approach to estimate market size using top-down analysis (supply side)

2.3 DATA TRIANGULATION

2.4 RESEARCH ASSUMPTIONS

2.5 RESEARCH LIMITATIONS

2.6 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ARTIFICIAL INTELLIGENCE IN MANUFACTURING MARKET

4.2 ARTIFICIAL INTELLIGENCE IN MANUFACTURING MARKET, BY OFFERING

4.3 ARTIFICIAL INTELLIGENCE IN MANUFACTURING MARKET, BY TECHNOLOGY

4.4 ARTIFICIAL INTELLIGENCE IN MANUFACTURING MARKET, BY INDUSTRY

4.5 ARTIFICIAL INTELLIGENCE IN MANUFACTURING MARKET, BY APPLICATION

4.6 ARTIFICIAL INTELLIGENCE IN MANUFACTURING MARKET, BY COUNTRY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Increasing adoption of IIoT and connected devices across manufacturing plants

5.2.1.2 Growing inclination toward AI-enabled decision-making in manufacturing

5.2.1.3 Growing role of augmented intelligence in enhancing workforce productivity

5.2.2 RESTRAINTS

5.2.2.1 Poor data integrity and data availability gaps in legacy systems

5.2.2.2 Barriers to enterprise-wide AI deployment in manufacturing

5.2.3 OPPORTUNITIES

5.2.3.1 Emerging trend of managing global plants remotely with AI

5.2.3.2 Shifting focus from mass production to smart customization

5.2.4 CHALLENGES

5.2.4.1 Complexities in aligning AI output with dynamic manufacturing environments

5.2.4.2 Sustaining AI accuracy in dynamic production environments

5.3 VALUE CHAIN ANALYSIS

5.4 ECOSYSTEM ANALYSIS

5.5 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.6 PORTER'S FIVE FORCES ANALYSIS

5.6.1 BARGAINING POWER OF SUPPLIERS

5.6.2 BARGAINING POWER OF BUYERS

5.6.3 THREAT OF NEW ENTRANTS

5.6.4 THREAT OF SUBSTITUTES

5.6.5 INTENSITY OF COMPETITIVE RIVALRY

5.7 KEY STAKEHOLDERS AND BUYING CRITERIA

5.7.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.7.2 BUYING CRITERIA

5.8 CASE STUDY ANALYSIS

5.8.1 EASTMAN CHEMICAL COMPANY TRANSFORMS EQUIPMENT MONITORING WITH AI-DRIVEN RELIABILITY PROGRAM OFFERED BY GE VERNOVA

5.8.2 HARTING TECHNOLOGY GROUP ACCELERATES CONNECTOR DESIGN WITH AI-POWERED ENGINEERING FROM MICROSOFT AND SIEMENS

5.8.3 RENISHAW PLC IMPROVES PRECISION AND REDUCES SCRAP USING NX CAM SOFTWARE OF SIEMENS

5.8.4 MITSUBISHI MOTORS CORPORATION TRANSFORMS OPERATIONS WITH IBM FOR MORE EFFICIENT AND AGILE FUTURE

5.8.5 SHELL ACHIEVES OPERATIONAL EXCELLENCE AND SCALABILITY IN PREDICTIVE MAINTENANCE WITH AI SOLUTIONS OFFERED BY MICROSOFT AND C3.AI

5.9 TECHNOLOGY ANALYSIS

5.9.1 KEY TECHNOLOGIES

5.9.1.1 Reinforcement learning

5.9.1.2 Augmented reality, virtual reality, and mixed reality

5.9.2 COMPLEMENTARY TECHNOLOGIES

5.9.2.1 Internet of Things (IoT)

5.9.2.2 Edge computing

5.9.3 ADJACENT TECHNOLOGIES

5.9.3.1 Additive manufacturing

5.9.3.2 Digital twin

5.10 PRICING ANALYSIS

5.10.1 AVERAGE SELLING PRICE OF PROCESSORS OFFERED BY KEY PLAYERS, BY TYPE, 2024

5.10.2 PRICING RANGE OF PROCESSORS OFFERED BY KEY PLAYERS, BY TYPE, 2024

5.10.3 AVERAGE SELLING PRICE TREND OF GPU, BY REGION, 2021-2024

5.10.4 AVERAGE SELLING PRICE TREND OF FPGA, BY REGION, 2021-2024

5.11 INVESTMENT AND FUNDING SCENARIO

5.12 TRADE ANALYSIS

5.12.1 IMPORT SCENARIO (HS CODE 8471)

5.12.2 EXPORT SCENARIO (HS CODE 8471)

5.13 PATENT ANALYSIS

5.14 KEY CONFERENCES AND EVENTS, 2025-2026

5.15 REGULATORY LANDSCAPE

5.15.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.16 IMPACT OF 2025 US TARIFF - OVERVIEW

5.16.1 INTRODUCTION

5.16.2 KEY TARIFF RATES

5.16.3 PRICE IMPACT ANALYSIS

5.16.4 IMPACT ON COUNTRIES/REGIONS

5.16.4.1 US

5.16.4.2 Europe

5.16.4.3 Asia Pacific

5.16.5 IMPACT ON INDUSTRIES

5.16.5.1 Semiconductor & electronics

5.16.5.2 Automotive

5.17 STRATEGIC ROADMAP FOR AI ADOPTION IN MANUFACTURING (2024-2030)

5.18 EMERGING REGIONAL HOTSPOTS

5.19 FUTURE OF AI IN MANUFACTURING

5.19.1 GENERATIVE AI AND SIMULATION-DRIVEN DESIGN

5.19.2 AUTONOMOUS AND COLLABORATIVE ROBOTICS

5.19.3 DIGITAL TWINS AND AI-DRIVEN FACTORY PLANNING

5.19.4 AI-DRIVEN SUSTAINABILITY AND ENERGY EFFICIENCY

5.19.5 SCALING AI ACROSS MANUFACTURING ECOSYSTEM

6 ARTIFICIAL INTELLIGENCE IN MANUFACTURING MARKET, BY OFFERING

6.1 INTRODUCTION

6.2 HARDWARE

6.2.1 PROCESSORS

6.2.1.1 Rising need for faster and more energy-efficient computation to boost demand