울트라 크루즈 및 도심 자율주행 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)

Ultra Cruise and City-Street Autonomous Driving Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1959322

리서치사:Global Market Insights Inc.

발행일:2026년 02월

페이지 정보:영문 249 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

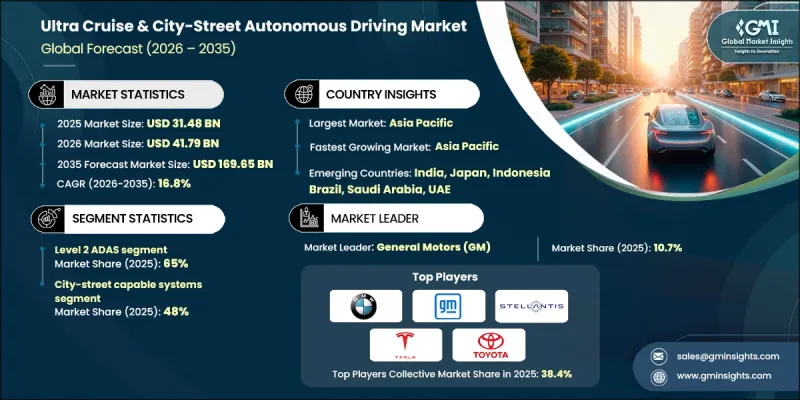

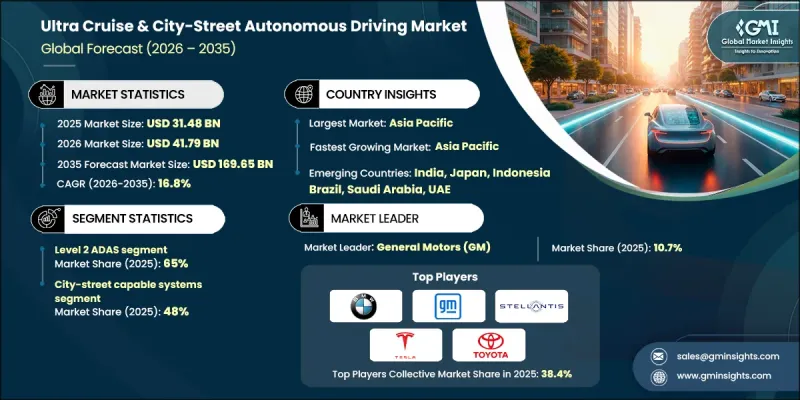

세계의 울트라 크루즈 및 도심 자율주행 시장은 2025년에 314억 8,000만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR)16.8%로 성장하여 1,696억 5,000만 달러에 이를 것으로 예측됩니다.

첨단 핸즈프리 운전과 도시 수준의 자동화의 통합은 차량 설계, 임베디드 소프트웨어 프레임워크, 차세대 모빌리티 솔루션을 재구성하고 있습니다. 자동차 제조업체들은 고립된 운전 지원 기능에서 인간의 감시를 유지하면서 단계적으로 고도화된 자율주행을 지원하는 적응형 소프트웨어 정의 주행 플랫폼으로 전환하고 있습니다. 교통체증, 예측 불가능한 도로 이용자, 고르지 못한 인프라 등 도심 주행 환경은 도심 자율주행 시스템에 높은 성능을 요구하고 있습니다. 이러한 솔루션은 교차로, 신호등, 차선 변경, 복잡한 교통 흐름을 관리하기 위해 고도의 센서 통합, 지속적인 환경 인식, 고속 컴퓨팅에 의존하고 있습니다. 이러한 기술은 차량이 정의된 운영 설계 영역 내에서 작동하기 때문에 제한된 접근 도로를 넘어 일상적인 도시 이용으로 자율주행을 확장하는 데 필수적입니다. 자동차 제조업체와 기술 제공업체들은 완전 자율주행의 도입보다는 소프트웨어 업데이트를 통한 안전과 신뢰성 확보, 단계적 기능 확장에 중점을 둔 확장 가능한 자율주행 스택에 많은 투자를 하고 있습니다. 이러한 단계적 접근 방식은 규제 준수, 소비자 신뢰 확보, 빠른 상용화를 돕습니다.

시장 범위

개시 연도

2025년

예측 연도

2026-2035년

개시 연도 가치

314억 8,000만 달러

예측 금액

1,696억 5,000만 달러

CAGR

16.8%

레벨 2 ADAS 부문은 2025년 65%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 16.5%의 성장률을 보일 것으로 전망됩니다. 이 부문이 선두를 달리고 있는 이유는 고도의 자동화 기능을 제공하면서도 운전자 모니터링을 유지할 수 있기 때문에 규제 당국의 승인과 시장 진출이 보다 현실적으로 가능해졌기 때문입니다. 기존의 안전 기준, 책임 프레임워크, 인증 프로세스는 모니터링이 가능한 자율주행을 강력하게 지지하고 있으며, 더 높은 수준의 자율 주행에 비해 더 빠른 도입을 가능하게 합니다.

도시 도로 대응 시스템 부문은 2025년에 48%의 점유율을 차지하며 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 17.8%를 나타낼 것으로 예측됩니다. 이러한 시스템이 주류가 된 이유는 차량 사용의 대부분이 발생하는 일상적인 운전 환경에 대응하기 때문입니다. 도심에서의 운전은 잦은 정차, 교차로, 취약한 도로 이용자, 혼잡한 교통상황을 수반하기 때문에 고속도로 전용 솔루션보다 도심 특화형 자율주행의 가치가 높아집니다. 도시 출퇴근, 주차, 단거리 이동에 대한 스트레스 감소를 원하는 소비자 수요 증가로 인해 도입이 가속화되고 있습니다.

미국의 울트라 크루즈 및 도심 자율주행 시장은 2025년 85%의 점유율을 차지하며 92억 달러 규모에 달할 것으로 예측됩니다. 첨단 운전 보조 시스템 및 모니터링이 가능한 자율주행 솔루션의 지속적인 혁신과 주요 자동차 제조업체의 대규모 투자로 미국 시장은 견조한 성장세를 유지하고 있습니다. 고도로 발달한 소프트웨어 정의 차량 생태계를 통해 제조업체는 핸즈프리 운전 기능을 관리되는 고속도로 환경에서 복잡한 도시 환경으로 확장할 수 있습니다. 이러한 발전은 인공지능 기반 인식 시스템, 고정밀 디지털 매핑, 기능, 안전 및 운전 성능의 지속적인 개선을 가능하게 하는 무선 소프트웨어 업데이트에 의해 뒷받침되고 있습니다.

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 자율 레벨별, 2022-2035

제6장 시장 추산 및 예측 : 운영 설계 영역별, 2022-2035

제7장 시장 추산 및 예측 : 센서 기술별, 2022-2035

제8장 시장 추산 및 예측 : 용도별, 2022-2035

제9장 시장 추산 및 예측 : 차량별, 2022-2035

제10장 시장 추산 및 예측 : 지역별, 2022-2035

제11장 기업 개요

LSH

영문 목차

영문목차

The Global Ultra Cruise & City-Street Autonomous Driving Market was valued at USD 31.48 billion in 2025 and is estimated to grow at a CAGR of 16.8% to reach USD 169.65 billion by 2035.

The integration of advanced hands-free driving and city-level automation is reshaping vehicle design, embedded software frameworks, and next-generation mobility solutions. Automakers are moving away from isolated driver-assistance features toward adaptive, software-defined driving platforms that support progressively higher autonomy while retaining human supervision. Urban driving conditions, including congestion, unpredictable road users, and inconsistent infrastructure, are placing higher performance demands on city-street autonomous systems. These solutions rely on sophisticated sensor integration, continuous environment perception, and high-speed computing to manage intersections, traffic signals, lane changes, and complex traffic flows. Because vehicles operate within defined operational design domains, such technologies are essential for extending autonomy beyond limited-access roads into everyday urban use. Automakers and technology providers are heavily investing in scalable autonomy stacks that emphasize safety, reliability, and gradual feature expansion through software updates rather than full automation deployment. This step-by-step approach supports regulatory alignment, consumer trust, and faster commercialization.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$31.48 Billion

Forecast Value

$169.65 Billion

CAGR

16.8%

The Level 2 ADAS segment held a 65% share in 2025 and is projected to grow at a CAGR of 16.5% through 2035. This segment leads due to its ability to deliver advanced automated functionality while maintaining driver oversight, making regulatory approval and market rollout more practical across regions. Existing safety standards, liability frameworks, and certification processes strongly favor supervised autonomy, enabling faster adoption compared to higher autonomy levels.

The city-street capable systems segment held 48% share in 2025 and is expected to register a CAGR of 17.8% between 2026 and 2035. These systems dominate because they address everyday driving environments where most vehicle usage occurs. Urban operation involves frequent stops, intersections, vulnerable road users, and mixed traffic conditions, making city-focused automation more valuable than highway-only solutions. Growing consumer demand for stress reduction in urban commuting, parking, and short-distance travel continues to accelerate adoption.

United States Ultra Cruise & City-Street Autonomous Driving Market held an 85% share, generating USD 9.2 billion in 2025. Market expansion in the U.S. remains strong, driven by continuous innovation in advanced driver assistance and supervised autonomy solutions, along with substantial investment from major automakers. A well-developed software-defined vehicle ecosystem is enabling manufacturers to extend hands-free driving capabilities beyond controlled highway environments into complex urban settings. This progress is supported by artificial intelligence-based perception systems, high-precision digital mapping, and over-the-air software updates that allow ongoing improvements in functionality, safety, and driving performance.

Key participants active in the Global Ultra Cruise & City-Street Autonomous Driving Market include NVIDIA, Toyota Motor, Continental, Mobileye, General Motors, Stellantis, BMW, Nissan Motor, and Mercedes-Benz Group. Companies in the ultra cruise and city-street autonomous driving market are strengthening their foothold through sustained investment in software-centric vehicle architectures and artificial intelligence-driven perception systems. Automakers are prioritizing modular autonomy platforms that allow features to scale across vehicle models and price segments. Strategic partnerships with semiconductor firms and software developers help accelerate processing performance and algorithm refinement. Many players emphasize over-the-air update capabilities to enhance system reliability and functionality post-sale. Extensive real-world data collection is used to improve urban driving accuracy and safety validation.

Table of Contents

Chapter 1 Methodology

1.1 Research approach

1.2 Quality commitments

1.2.1 GMI AI policy & data integrity commitment

1.3 Research trail & confidence scoring

1.3.1 Research trail components

1.3.2 Scoring components

1.4 Data collection

1.4.1 Partial list of primary sources

1.5 Data mining sources

1.5.1 Paid sources

1.6 Base estimates and calculations

1.6.1 Base year calculation

1.7 Forecast model

1.8 Research transparency addendum

Chapter 2 Executive Summary

2.1 Industry 360° synopsis, 2022 - 2035

2.2 Key market trends

2.2.1 Regional

2.2.2 Autonomy Level

2.2.3 Operational Design Domain

2.2.4 Vehicle

2.2.5 Sensor Technology

2.2.6 End use

2.3 TAM Analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising Demand for Hands-Free & Convenience-Driven Mobility

3.2.1.2 Advancements in AI, Sensor Fusion & Onboard Compute