드라이브 바이 와이어(DBW) 시장(-2032년) : 유형(Steer by Wire, Brake by Wire, Shift by Wire, Park by Wire, Throttle by Wire), 자율주행차, 지역별

Drive By Wire Market by Type (Steer by Wire, Brake by Wire, Shift by Wire, Park by Wire, Throttle by Wire), Autonomous Vehicle, and Region - Global Forecast To 2032

상품코드:1950788

리서치사:MarketsandMarkets

발행일:2026년 02월

페이지 정보:영문 351 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

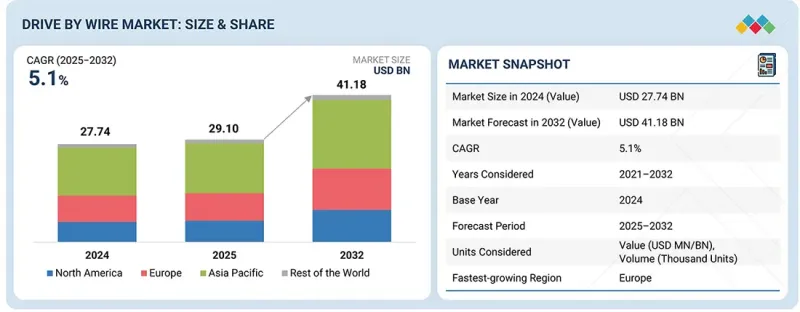

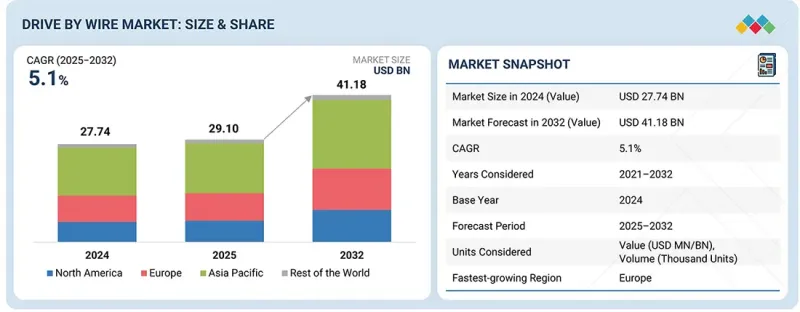

드라이브 바이 와이어(DBW) 시장 규모는 2025년 291억 달러에서 2032년까지 411억 8,000만 달러에 이를 것으로 예측되며, CAGR은 5.1%로 전망되고 있습니다.

시프트 바이 와이어와 스로틀 바이 와이어는 규정 준수 요구사항이 낮고 기능적, 비용적, 아키텍처 측면에서 즉각적인 이점을 제공하기 때문에 가장 널리 채택되는 드라이브 바이 와이어(DBW) 용도으로 남을 것으로 예측됩니다.

조사 범위

조사 대상 기간

2021-2032년

기준 연도

2024년

예측 기간

2025-2032년

단위

금액(달러), 수량

부문

Steer by Wire, Brake by Wire, Shift by Wire, Park by Wire, Throttle by Wire, Application

대상 지역

북미, 아시아태평양, 유럽, 기타 지역

스로틀 바이 와이어는 배출가스 규제 요건, 토크 관리, ADAS 통합, 전자식 파워트레인과의 호환성을 보장하기 위해 내연기관차, 하이브리드 자동차, 전기자동차에 모두 사용되고 있습니다. 자동변속기와 전기자동차가 시프트 바이 와이어의 채택을 주도하고 있습니다. 전자식 기어 선택은 컴팩트한 패키징, 간소화된 인테리어, 향상된 안전성, 자동 주차 기능 및 원격 제어 기능과의 완벽한 통합을 가능하게 합니다. 이러한 시스템은 OEM 제조업체에게 소프트웨어 정의 차량 개발 및 플랫폼 표준화를 위한 가장 빠른 경로를 제공하는 동시에 제조 비용 증가, 복잡한 안전 백업, 국가별 인증 획득과 같은 문제를 피할 수 있습니다.

"BEV(배터리 전기차)가 드라이브 바이 와이어(DBW) 시스템에 대한 가장 큰 수요를 창출할 것으로 전망"

BEV는 엔진, 기계식 기어 링크 메커니즘, 진공식 브레이크 시스템이 필요하지 않기 때문에 전자 제어가 표준 선택이 될 것이며, 드라이브 바이 와이어(DBW) 시스템에 대한 수요가 가장 높을 것으로 예측됩니다. 스로틀 바이 와이어, Brake-by-wire, 시프트 바이 와이어는 내연기관 차량보다 평평한 바닥 구조와 중앙 집중식 전기 시스템에 통합하기가 더 쉽습니다. BEV의 기술적 진화는 드라이브 바이 와이어(DBW) 시스템에 대한 수요를 더욱 창출하고 있습니다. BEV 아키텍처는 완전 전자식 브레이크를 지원하며, 정밀한 브레이크 제어와 효율적인 회생 제동 조합을 가능하게 합니다. 이러한 차량에서 중앙 집중식 컴퓨팅과 구역별 E/E 아키텍처를 통해 조향, 브레이크, 스로틀, 변속 조작을 기계적인 링크가 아닌 소프트웨어 기능으로 제어해야 합니다. 또한, BEV는 소프트웨어 정의 플랫폼으로 개발되어 주행 모드, 에너지 관리, ADAS 기능 등이 무선으로 업데이트됩니다. 이는 바이와이어 시스템을 통해서만 가능한 일입니다. 이러한 플랫폼 수준의 변화는 기계식 제어가 BEV의 설계 목표와 양립할 수 없게 만들었고, 드라이브 바이 와이어(DBW)의 채택을 가속화하고 있습니다.

"유럽은 드라이브 바이 와이어(DBW) 시스템에서 가장 빠르게 성장하는 시장이 될 것으로 예측됩니다."

유럽은 규제 중심의 전동화 및 프리미엄 OEM의 리더십에 힘입어 예측 기간 동안 시장에서 가장 빠른 성장을 보일 것으로 예측됩니다. 이 지역에서 드라이브 바이 와이어(DBW)의 급속한 보급은 제약이 많은 패키징 환경 내에서 플랫폼 아키텍처 최적화의 필요성과 소프트웨어 정의 기능 안전 및 전자 제어 브레이크 시스템에 대한 강력한 제도적 준비에 의해 촉진되고 있습니다. 이 환경은 Brake-by-wire 아키텍처의 대규모 도입을 조기에 지원할 수 있습니다. 반면, 스티어 바이 와이어 도입은 패키징, 충돌 통합, 시스템 레벨의 이점이 추가 검증 및 중복성의 복잡성을 정당화할 수 있는 경우에만 선택적으로 진행됩니다. 시장 전망의 관점에서 볼 때, 유럽이 모듈형 차량 아키텍처와 소프트웨어 중심 안전 검증에서 선도적인 위치에 있기 때문에 드라이브 바이 와이어(DBW) 시스템은 중기적으로 평균보다 높은 성장률을 보일 것으로 예측됩니다. OEM의 투자는 Brake-by-wire 플랫폼을 기반 기술로 우선시할 가능성이 높으며, 이를 통해 대량 생산 부문의 대규모 도입이 가능해지고, 규제 준수 및 플랫폼 재사용이라는 목표도 달성할 수 있습니다.

세계의 드라이브 바이 와이어(DBW)(Drive-by-Wire) 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술 및 특허 동향, 법 및 규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별/지역별/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 바이와이야 기술 통합

제7장 기술 진보, AI의 영향, 특허, 혁신, 향후 응용

제8장 규제 상황

제9장 Brake-by-Wire : 추진 구분·컴포넌트별

제10장 Park by Wire : 추진 구분·컴포넌트별

제11장 Shift by Wire : 추진 구분·컴포넌트별

제12장 Steer-by-Wire : 추진 구분·컴포넌트별

제13장 Throttle by Wire : 추진 구분·컴포넌트별

제14장 자율주행차용 드라이브 바이 와이어(DBW) 시장 : 용도별

제15장 드라이브 바이 와이어(DBW) 시장 : 지역별

제16장 경쟁 구도

제17장 기업 개요

제18장 조사 방법

제19장 부록

LSH

영문 목차

영문목차

The drive by wire market is projected to reach USD 41.18 billion by 2032, from USD 29.10 billion in 2025, with a CAGR of 5.1%. Shift by wire and throttle by wire are expected to remain the most widely adopted drive by wire applications because they deliver immediate functional, cost, and architectural benefits with low regulatory compliance requirements.

Scope of the Report

Years Considered for the Study

2021-2032

Base Year

2024

Forecast Period

2025-2032

Units Considered

Value (USD MN/BN), Volume (Thousand Units)

Segments

Steer by Wire, Brake by Wire, Shift by Wire, Park by Wire, Throttle by Wire, Application

Regions covered

North America, Asia Pacific, Europe, Rest of the World

Throttle by wire is used across ICE, hybrid, and electric vehicles due to emission control requirements, torque management, ADAS integration, and to ensure compatibility with the electronic powertrain. Shift by wire adoption is led by automatic and electric vehicles, where electronic gear selection enables compact packaging, simplified interiors, improved safety, and seamless integration with autonomous parking and remote-control features. Together, these systems offer OEMs the fastest path to developing software-defined vehicles and platform standardization, while avoiding higher manufacturing costs, complex safety backups, and country-specific certifications.

"BEVs are expected to generate the highest demand for drive by wire systems."

BEVs are expected to generate the highest demand for drive by wire systems, as they lack engines, mechanical gear linkages, or vacuum-based brake systems, making electronic control the default choice for these vehicles. Throttle by wire, brake by wire, and shift by wire can be integrated easily into flat-floor architectures and centralized electrical systems than in ICE-derived vehicles. Technological changes in BEVs are further creating demand for drive by wire systems. BEV architectures support fully electronic braking, enabling accurate brake control and efficient regenerative braking blending. Centralized computing and zonal E/E architectures in these vehicles require steering, braking, throttle, and shifting to be controlled as software functions rather than mechanical linkages. Additionally, BEVs are developed as software-defined platforms, with drive modes, energy management, and ADAS features updated over the air, which is only feasible with by-wire systems. These platform-level changes make mechanical controls incompatible with BEVs' design goals, accelerating drive by wire adoption.

"Europe is expected to be the fastest-growing market for drive by wire systems."

Europe is expected to see the fastest growth in the drive by wire market during the forecast period, driven by regulation-driven electrification and premium OEM leadership. The region's rapid adoption of drive by wire is primarily driven by the need to optimize platform architectures within tightly constrained packaging environments and by strong institutional readiness for software-defined functional safety and electronically controlled braking systems. This environment supports earlier large-scale deployment of brake by wire architectures, with steer by wire adoption advancing selectively where packaging, crash integration, and system-level benefits justify the added validation and redundancy complexity. From a market-outlook perspective, Europe's leadership in modular vehicle architectures and software-centric safety validation is expected to translate into above-average growth rates for drive by wire systems over the medium term. OEM investments are likely to prioritize brake by wire platforms as a foundation technology, enabling large-scale deployment across high-volume segments while supporting regulatory compliance and platform reuse objectives.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and strategy directors, and executives from various key organizations operating in the drive by wire market.

By Company Type: Supply-side - 70%, Demand-side - 30%

By Designation: C level - 25%, Director Level - 30%, Others - 45%

By Region: Asia Pacific - 55%, Europe - 15%, North America - 20%, Rest of the World - 10%

Research Coverage

The report details the drivers, restraints, opportunities, and challenges in the drive by wire market and forecasts the market through 2032. It also provides a qualitative and quantitative description of different market segments. The report provides a detailed market overview across four regions: North America, Europe, Asia Pacific, and the Rest of the World.

Key Benefits of Buying this Report:

The report will help market leaders/new entrants with information on the closest approximations of revenue numbers for the overall drive by wire market and its subsegments.

This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies.

The report will also help stakeholders understand the market pulse and provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insight into the following pointers:

Analysis of key drivers (shift toward software-defined vehicle architectures, high operational accuracy and reduced mechanical losses, electrification of commercial and public transport fleets) restraints (legal liability in absence of mature fail-operational precedents, threat of cyberattacks and compliance costs), opportunities (Integration with AI, V2X, and OTA-enabled safety functions, advancements in autonomous vehicles), and challenges (integration challenges in off-highway equipment, electronic failures and rapid developments in automotive electronics)

Product Development/Innovation: Detailed insights into upcoming technologies and R&D activities in the drive by wire market

Market Development: Comprehensive information about lucrative markets across varied regions

Market Diversification: Exhaustive information about untapped geographies, recent developments, and investments in the drive by wire market

Competitive Assessment: In-depth assessment of market share, growth strategies, and product offerings of leading players, such as Robert Bosch GmbH (Germany), ZF Friedrichshafen AG (Germany), Continental AG (Germany), Nexteer Automotive (US), and Curtiss-Wright Corporation (US)

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 UNIT CONSIDERED

1.6 STAKEHOLDERS

1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

2.3 DISRUPTIVE TRENDS IN DRIVE BY WIRE MARKET

2.4 HIGH-GROWTH SEGMENTS

2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DRIVE BY WIRE MARKET

3.2 L2 AUTONOMOUS VEHICLE DRIVE BY WIRE MARKET, BY APPLICATION

3.3 THROTTLE BY WIRE MARKET, BY ICE VEHICLE TYPE

3.4 THROTTLE BY WIRE MARKET, BY EV TYPE

3.5 BRAKE BY WIRE MARKET, BY ICE VEHICLE TYPE

3.6 BRAKE BY WIRE MARKET, BY EV TYPE

3.7 STEER BY WIRE MARKET, BY ICE VEHICLE TYPE

3.8 STEER BY WIRE MARKET, BY EV TYPE

3.9 SHIFT BY WIRE MARKET, BY ICE VEHICLE TYPE

3.10 SHIFT BY WIRE MARKET, BY EV TYPE

3.11 PARK BY WIRE MARKET, BY ICE VEHICLE TYPE

3.12 PARK BY WIRE MARKET, BY EV TYPE

3.13 DRIVE BY WIRE MARKET, BY REGION

4 MARKET OVERVIEW

4.1 INTRODUCTION

4.2 MARKET DYNAMICS

4.2.1 DRIVERS

4.2.1.1 Transition to software-defined vehicle architectures

4.2.1.1.1 Shift toward zonal architectures

4.2.1.2 High operational accuracy and reduced mechanical losses

4.2.1.3 Electrification of public transport and commercial fleets

4.2.2 RESTRAINTS

4.2.2.1 Legal liability due to absence of mature fail-operational precedents

4.2.2.2 Threat of cyberattacks and compliance costs

4.2.3 OPPORTUNITIES

4.2.3.1 Integration with AI, V2X, and OTA-enabled safety functions

4.2.3.2 Advancements in autonomous vehicles

4.2.4 CHALLENGES

4.2.4.1 Integration challenges in off-highway equipment

4.2.4.2 Electronic failures and rapid developments in automotive electronics

4.3 UNMET NEEDS AND WHITE SPACES

4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

5.1 ECOSYSTEM ANALYSIS

5.1.1 RAW MATERIAL SUPPLIERS

5.1.2 ACTUATOR AND SENSOR MANUFACTURERS

5.1.3 TIER-1 SUPPLIERS/COMPONENT MANUFACTURERS

5.1.4 DISTRIBUTORS

5.1.5 OEMS

5.2 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.3 CASE STUDY ANALYSIS

5.3.1 FKA'S STEER BY WIRE SYSTEMS

5.3.2 CONTINENTAL'S MK C1 INTELLIGENT BRAKING SYSTEM

5.3.3 NEXTEER AUTOMOTIVE'S STEER BY WIRE SYSTEM

5.4 PRICING ANALYSIS

5.5 SUPPLY CHAIN ANALYSIS

5.6 COST-BENEFIT ANALYSIS

5.6.1 THROTTLE BY WIRE

5.6.2 SHIFT BY WIRE

5.6.3 PARK BY WIRE

5.6.4 BRAKE BY WIRE

5.6.5 STEER BY WIRE

5.7 KEY CONFERENCES AND EVENTS

6 INTEGRATION OF BY-WIRE TECHNOLOGIES

6.1 SMART ACTUATORS

6.1.1 OVERVIEW

6.1.2 KEY SUPPLIERS

6.2 ELECTRIC MOTORS

6.2.1 OVERVIEW

6.2.2 KEY SUPPLIERS

6.3 INTEGRATED CHASSIS SYSTEMS

6.3.1 OVERVIEW

6.3.2 KEY SUPPLIERS

6.4 SYNERGIES WITH ADAS/AUTONOMY

6.5 TRADITIONAL SYSTEMS VS. BY-WIRE SYSTEMS

6.6 FEATURE ANALYSIS OF BY-WIRE TECHNOLOGIES

7 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

7.1 KEY TECHNOLOGIES

7.1.1 ADVANCED SENSOR TECHNOLOGIES

7.1.2 ELECTRICAL/ELECTRONIC ARCHITECTURES

7.1.3 CYBERSECURITY IN DRIVE BY WIRE NETWORKS

7.2 IMPACT OF AI/GEN AI

7.3 PATENT ANALYSIS

7.4 FUTURE APPLICATIONS

7.4.1 INTEGRATION WITH ADAS AND AUTONOMOUS DRIVING PLATFORMS

8 REGULATORY LANDSCAPE

8.1 REGIONAL REGULATIONS AND COMPLIANCE

8.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

8.1.2 DRIVE BY WIRE STANDARDS, BY COUNTRY

9 BRAKE BY WIRE, BY PROPULSION AND COMPONENT

9.1 INTRODUCTION

9.2 TYPES

9.2.1 PEDAL-BASED BRAKE BY WIRE

9.2.2 ELECTRO-HYDRAULIC BRAKE BY WIRE

9.2.3 ELECTRO-MECHANICAL BRAKE BY WIRE

9.3 CONVENTIONAL BRAKING SYSTEMS VS. BRAKE BY WIRE SYSTEMS

9.4 KEY FEATURES

9.5 MARKET UPTAKE - BY OEM

9.6 MARKET SIZING AND FORECAST

9.6.1 BY ICE VEHICLE TYPE

9.6.1.1 Passenger car

9.6.1.2 Light commercial vehicle

9.6.1.3 Truck

9.6.1.4 Bus

9.6.2 BY EV TYPE

9.6.2.1 BEV

9.6.2.2 PHEV

9.6.2.3 FCEV

9.6.3 BY SENSOR TYPE

9.6.3.1 Brake pedal sensor

9.6.4 BY COMPONENT

9.6.4.1 Actuator

9.6.4.2 ECU

9.7 PRIMARY INSIGHTS

10 PARK BY WIRE, BY PROPULSION AND COMPONENT

10.1 INTRODUCTION

10.2 TYPES

10.2.1 TRANSMISSION PARK BY WIRE

10.2.2 REDUNDANT PARK BY WIRE

10.2.3 ELECTRIC PARKING BRAKE

10.3 CONVENTIONAL PARKING SYSTEMS VS. PARK BY WIRE SYSTEMS

10.4 KEY FEATURES

10.5 MARKET UPTAKE - BY OEM

10.6 MARKET SIZING AND FORECAST

10.6.1 BY ICE VEHICLE TYPE

10.6.1.1 Passenger car

10.6.1.2 Light commercial vehicle

10.6.1.3 Truck

10.6.1.4 Bus

10.6.2 BY EV TYPE

10.6.2.1 BEV

10.6.2.2 PHEV

10.6.2.3 FCEV

10.6.3 BY SENSOR TYPE

10.6.3.1 Park sensor

10.6.4 BY COMPONENT

10.6.4.1 Actuator

10.6.4.2 ECU

10.6.4.3 Parking pawl

10.7 PRIMARY INSIGHTS

11 SHIFT BY WIRE, BY PROPULSION AND COMPONENT

11.1 INTRODUCTION

11.2 TYPES

11.2.1 ELECTRONIC GEAR SELECTOR

11.2.2 PUSH-BUTTON SHIFT BY WIRE

11.2.3 LEVER-BASED SHIFT BY WIRE

11.3 CONVENTIONAL SHIFTING SYSTEMS VS. SHIFT BY WIRE SYSTEMS

11.4 KEY FEATURES

11.5 MARKET UPTAKE - BY OEM

11.6 MARKET SIZING AND FORECAST

11.6.1 BY ICE VEHICLE TYPE

11.6.1.1 Passenger car

11.6.1.2 Light commercial vehicle

11.6.1.3 Truck

11.6.1.4 Bus

11.6.2 BY EV TYPE

11.6.2.1 BEV

11.6.2.2 PHEV

11.6.2.3 FCEV

11.6.3 BY SENSOR TYPE

11.6.3.1 Gear shift position sensor

11.6.4 BY COMPONENT

11.6.4.1 Actuator

11.6.4.2 ECU

11.6.4.3 ETCU

11.7 PRIMARY INSIGHTS

12 STEER BY WIRE, BY PROPULSION AND COMPONENT

12.1 INTRODUCTION

12.2 TYPES

12.2.1 PINION

12.2.2 COLUMN

12.2.3 RACK

12.3 CONVENTIONAL STEERING SYSTEMS VS. STEER BY WIRE SYSTEMS

12.4 KEY FEATURES

12.5 MARKET UPTAKE - BY OEM

12.6 MARKET SIZING AND FORECAST

12.6.1 BY ICE VEHICLE TYPE

12.6.1.1 Passenger car

12.6.1.2 Light commercial vehicle

12.6.1.3 Truck

12.6.1.4 Bus

12.6.2 BY EV TYPE

12.6.2.1 BEV

12.6.2.2 PHEV

12.6.2.3 FCEV

12.6.3 BY SENSOR TYPE

12.6.3.1 Hand wheel angle sensor

12.6.3.2 Pinion angle sensor

12.6.4 BY COMPONENT

12.6.4.1 Actuator

12.6.4.2 ECU

12.6.4.3 Feedback motor

12.7 PRIMARY INSIGHTS

13 THROTTLE BY WIRE, BY PROPULSION AND COMPONENT

13.1 INTRODUCTION

13.2 TYPES

13.2.1 PEDAL-BASED THROTTLE BY WIRE

13.2.2 MOTOR-TORQUE THROTTLE BY WIRE

13.2.3 DRIVE-MODE ADAPTIVE THROTTLE BY WIRE

13.3 CONVENTIONAL THROTTLE SYSTEMS VS. THROTTLE BY WIRE SYSTEMS

13.4 KEY FEATURES

13.5 MARKET UPTAKE - BY OEM

13.6 MARKET SIZING AND FORECAST

13.6.1 BY ICE VEHICLE TYPE

13.6.1.1 Passenger car

13.6.1.2 Light commercial vehicle

13.6.1.3 Truck

13.6.1.4 Bus

13.6.2 BY EV TYPE

13.6.2.1 BEV

13.6.2.2 PHEV

13.6.2.3 FCEV

13.6.3 BY SENSOR TYPE

13.6.3.1 Throttle pedal sensor

13.6.3.2 Throttle position sensor

13.6.4 BY COMPONENT

13.6.4.1 Actuator

13.6.4.2 ECU

13.6.4.3 ECM

13.6.4.4 ETCM

13.7 PRIMARY INSIGHTS

14 AUTONOMOUS VEHICLE DRIVE BY WIRE MARKET, BY APPLICATION

14.1 INTRODUCTION

14.2 L2 AUTONOMOUS VEHICLE

14.3 L3 AUTONOMOUS VEHICLE

14.4 L4/L5 AUTONOMOUS VEHICLE

14.5 PRIMARY INSIGHTS

15 DRIVE BY WIRE MARKET, BY REGION

15.1 INTRODUCTION

15.2 ASIA PACIFIC

15.2.1 CHINA

15.2.1.1 Growing popularity of electronic vehicle control to drive market

15.2.2 INDIA

15.2.2.1 Rising penetration of automatic transmissions to drive market

15.2.3 JAPAN

15.2.3.1 Product innovations by domestic manufacturers to drive market

15.2.4 SOUTH KOREA

15.2.4.1 Regulatory and technology alignment to drive market

15.2.5 THAILAND

15.2.5.1 Surge in EV sales and localization of electronics to drive market

15.2.6 REST OF ASIA PACIFIC

15.3 EUROPE

15.3.1 GERMANY

15.3.1.1 Strong premium vehicle base and presence of major by-wire suppliers to drive market

15.3.2 FRANCE

15.3.2.1 High demand for premium vehicles and stringent emission rules to drive market

15.3.3 RUSSIA

15.3.3.1 Rise of premium vehicle sales to drive market

15.3.4 SPAIN

15.3.4.1 Increasing consumer demand for luxury brands to drive market

15.3.5 UK

15.3.5.1 Mature automotive R&D ecosystem to drive market

15.3.6 TURKEY

15.3.6.1 Expanding presence of foreign luxury automakers to drive market

15.3.7 ITALY

15.3.7.1 Ongoing technology partnerships to drive market

15.3.8 REST OF EUROPE

15.4 NORTH AMERICA

15.4.1 CANADA

15.4.1.1 Elevated demand for premium and advanced vehicles to drive market

15.4.2 MEXICO

15.4.2.1 Robust cross-border supply chains to drive market

15.4.3 US

15.4.3.1 Strong technology adoption to drive market

15.5 REST OF THE WORLD

15.5.1 BRAZIL

15.5.1.1 Localization of advanced components and export-oriented production to drive market

15.5.2 IRAN

15.5.2.1 Preference for manual transmissions to impede market

15.5.3 ARGENTINA

15.5.3.1 Reduced import duties to drive market

15.5.4 SOUTH AFRICA

15.5.4.1 New premium vehicle launches to drive market

15.5.5 OTHERS

16 COMPETITIVE LANDSCAPE

16.1 INTRODUCTION

16.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

16.3 MARKET SHARE ANALYSIS, 2024

16.4 REVENUE ANALYSIS, 2020-2024

16.5 COMPANY VALUATION AND FINANCIAL METRICS

16.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

16.6.1 STARS

16.6.2 EMERGING LEADERS

16.6.3 PERVASIVE PLAYERS

16.6.4 PARTICIPANTS

16.6.5 COMPANY FOOTPRINT

16.6.5.1 Company footprint

16.6.5.2 Region footprint

16.6.5.3 Component footprint

16.6.5.4 Application footprint

16.7 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2024

16.7.1 PROGRESSIVE COMPANIES

16.7.2 RESPONSIVE COMPANIES

16.7.3 DYNAMIC COMPANIES

16.7.4 STARTING BLOCKS

16.7.5 COMPETITIVE BENCHMARKING

16.7.5.1 List of start-ups/SMEs

16.7.5.2 Competitive benchmarking of start-ups/SMEs

16.8 COMPETITIVE SCENARIO

16.8.1 PRODUCT LAUNCHES/DEVELOPMENTS

16.8.2 DEALS

16.8.3 EXPANSIONS

16.8.4 OTHER DEVELOPMENTS

17 COMPANY PROFILES

17.1 KEY PLAYERS

17.1.1 ROBERT BOSCH GMBH

17.1.1.1 Business overview

17.1.1.2 Products offered

17.1.1.3 Recent developments

17.1.1.3.1 Product launches/developments

17.1.1.3.2 Deals

17.1.1.3.3 Other deveopments

17.1.1.4 MnM view

17.1.1.4.1 Key strengths/Right to win

17.1.1.4.2 Strategic choices

17.1.1.4.3 Weaknesses and competitive threats

17.1.2 CONTINENTAL AG

17.1.2.1 Business overview

17.1.2.2 Products offered

17.1.2.3 Recent developments

17.1.2.3.1 Product launches/developments

17.1.2.3.2 Deals

17.1.2.3.3 Expansions

17.1.2.3.4 Other deveopments

17.1.2.4 MnM view

17.1.2.4.1 Key strengths/Right to win

17.1.2.4.2 Strategic choices

17.1.2.4.3 Weaknesses and competitive threats

17.1.3 ZF FRIEDRICHSHAFEN AG

17.1.3.1 Business overview

17.1.3.2 Products offered

17.1.3.3 Recent developments

17.1.3.3.1 Product launches/developments

17.1.3.3.2 Deals

17.1.3.3.3 Other deveopments

17.1.3.4 MnM view

17.1.3.4.1 Key strengths/Right to win

17.1.3.4.2 Strategic choices

17.1.3.4.3 Weaknesses and competitive threats

17.1.4 NEXTEER AUTOMOTIVE

17.1.4.1 Business overview

17.1.4.2 Products offered

17.1.4.3 Recent developments

17.1.4.3.1 Product launches/developments

17.1.4.3.2 Deals

17.1.4.3.3 Expansions

17.1.4.4 MnM view

17.1.4.4.1 Key strengths/Right to win

17.1.4.4.2 Strategic choices

17.1.4.4.3 Weaknesses and competitive threats

17.1.5 HITACHI, LTD.

17.1.5.1 Business overview

17.1.5.2 Products offered

17.1.5.3 Recent developments

17.1.5.3.1 Product launches/developments

17.1.5.3.2 Deals

17.1.5.4 MnM view

17.1.5.4.1 Key strengths/Right to win

17.1.5.4.2 Strategic choices

17.1.5.4.3 Weaknesses and competitive threats

17.1.6 HL MANDO CORP.

17.1.6.1 Business overview

17.1.6.2 Products offered

17.1.6.3 Recent developments

17.1.6.3.1 Deals

17.1.6.3.2 Other developments

17.1.7 JTEKT CORPORATION

17.1.7.1 Business overview

17.1.7.2 Products offered

17.1.7.3 Recent developments

17.1.7.3.1 Product launches/developments

17.1.7.3.2 Deals

17.1.7.3.3 Expansions

17.1.7.3.4 Other developments

17.1.8 THYSSENKRUPP AG

17.1.8.1 Business overview

17.1.8.2 Products offered

17.1.8.3 Recent developments

17.1.8.3.1 Deals

17.1.9 FICOSA INTERNATIONAL SA

17.1.9.1 Business overview

17.1.9.2 Products offered

17.1.10 KONGSBERG AUTOMOTIVE

17.1.10.1 Business overview

17.1.10.2 Products offered

17.1.10.3 Recent developments

17.1.10.3.1 Other developments

17.1.11 CURTISS-WRIGHT CORPORATION

17.1.11.1 Business overview

17.1.11.2 Products offered

17.1.11.3 Recent developments

17.1.11.3.1 Product launches/developments

17.1.11.3.2 Deals

17.1.11.3.3 Expansions

17.1.11.3.4 Other deveopments

17.2 OTHER PLAYERS

17.2.1 SCHAEFFLER TECHNOLOGIES AG & CO. KG

17.2.2 KSR INTERNATIONAL INC.

17.2.3 CTS CORPORATION

17.2.4 HYUNDAI MOBIS

17.2.5 FORVIA

17.2.6 NIDEC CORPORATION

17.2.7 NISSAN CORPORATION

17.2.8 INFINEON TECHNOLOGIES AG

17.2.9 BREMBO S.P.A.

17.2.10 DENSO CORPORATION

17.2.11 NXP SEMICONDUCTORS NV

17.2.12 SNT MOTIV CO., LTD.

17.2.13 LEM EUROPE GMBH

17.2.14 ALLIED MOTION TECHNOLOGIES INC.

17.2.15 DURA AUTOMOTIVE SYSTEMS

18 RESEARCH METHODOLOGY

18.1 RESEARCH DATA

18.1.1 SECONDARY DATA

18.1.1.1 List of secondary sources

18.1.1.2 Key data from secondary sources

18.1.2 PRIMARY DATA

18.1.2.1 Primary interviewees from demand and supply sides