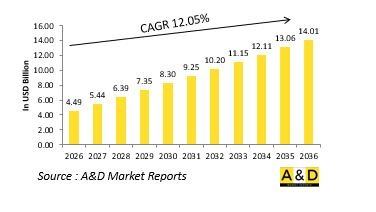

세계의 방위용 로봇 및 자율주행차 시장 규모는 2026년에 44억 9,000만 달러로 추정되며, 2026년부터 2036년까지 예측 기간에 CAGR 12.05%로 성장하여 2036년까지 140억 1,000만 달러에 달할 전망입니다.

방위용 로봇 및 자율주행차 시장 개요

방위용 로봇 및 자율 주행 차량 시장은 최소한의 인위적 개입으로 복잡한 군사 임무를 수행하도록 설계된 무인 시스템을 포함합니다. 이들 시스템은 공중, 육상, 해상 영역에서 운용되며 정찰, 군수지원, 감시, 폭발물 처리, 전투작전 등의 임무를 수행합니다. 분쟁 지역이나 위험한 환경에서 위험한 임무를 수행하여 부대 보호를 강화하고, 인원의 위험을 줄입니다. 국방 작전에 로봇과 자율성을 통합하는 것은 디지털화, 네트워크화, 정밀화를 지향하는 전쟁 형태로의 광범위한 전환을 반영합니다. 전 세계 국방 기관은 작전 효율성 향상, 상황 인식 유지, 인력 도달 범위 확대를 위해 로봇 플랫폼의 도입을 가속화하고 있습니다. 인공지능(AI)과 머신러닝이 성숙해짐에 따라 자율방위 시스템은 원격 조종 도구에서 독립적인 임무 수행 능력을 갖춘 지능형 의사결정 지원 자산으로 진화하며 현대 군사 전략의 본질을 재정의하고 있습니다.

인공지능, 첨단 센서, 기계 자율성 분야의 혁신으로 국방 로봇 및 자율 주행 차량 시장에 큰 변화를 가져오고 있습니다. AI 기반 내비게이션 및 인지 기술의 혁신으로 인해 이러한 시스템은 복잡하고 역동적인 환경에서도 자율적으로 작동할 수 있게 되었습니다. 향상된 센서 융합은 시각, 열 감지 및 레이더 데이터를 원활하게 통합하여 뛰어난 상황 인식 능력과 목표물 식별을 실현합니다. 엣지 컴퓨팅과 실시간 데이터 처리를 통해 자율 플랫폼은 외부 통신 링크에 의존하지 않고 임무 수행 중 즉각적인 판단을 내릴 수 있게 되었습니다. 로봇 설계의 발전으로 경량화, 기동성 향상, 에너지 절약, 다양한 지형과 임무 프로파일에 적응할 수 있는 플랫폼이 실현되고 있습니다. 군집 지능과 협동 로봇 공학이 새로운 트렌드로 부상하고 있으며, 여러 자율 시스템이 협력하여 동기화된 작전 행동을 가능하게 합니다. 사이버 보안과 안전한 통신 프로토콜도 필수적이며, 전자전 및 방해공작에 대한 내성을 보장합니다. 이러한 기술 발전으로 로봇공학과 자율성은 정밀성, 적응성, 작전적 확장성을 실현하는 미래 국방 능력의 근간으로 자리매김하고 있습니다.

방위용 로봇 및 자율 주행 차량 시장의 성장은 현대전에서 상황 인식 능력 강화, 부대 보호 및 작전 효율성 향상에 대한 필요성에 의해 주도되고 있습니다. 전장의 복잡성, 도심 전투 환경, 비대칭 위협 증가는 고위험 임무를 수행할 수 있는 무인 시스템의 가치를 부각시키고 있습니다. 국방기관은 인명피해 감소, 임무 연속성 향상, 병참 및 정찰 임무의 최적화를 목적으로 자동화를 우선적으로 추진하고 있습니다. 감시, 전투 지원, 의사결정 과정에서 AI와 자율성의 활용이 확대되면서 도입이 더욱 가속화되고 있습니다. 각국 정부는 또한 현대화 계획의 일환으로 기술 자립과 로봇 시스템의 국내 개발을 중시하고 있습니다. 전자전의 부상과 더 빠른 데이터 기반 대응 능력에 대한 수요가 증가함에 따라 지능화 및 네트워크화된 로봇 플랫폼에 대한 투자가 촉진되고 있습니다. 또한, 민수용 로봇 기술 혁신과 방위용 로봇의 융합이 진전되면서 도입 속도가 빨라지고 있으며, 무인 자율 군사 작전의 새로운 시대가 열리고 있습니다.

방위용 로봇 및 자율주행차 시장의 지역별 동향은 각 지역의 전략적 목표와 기술 역량의 차이를 반영하고 있습니다. 북미는 무인 지상, 항공, 해상 시스템에 대한 지속적인 투자로 선도적인 위치에 있으며, 첨단 자율기술과 AI를 통합한 통합부대 작전을 전개하고 있습니다. 유럽에서는 감시, 후방 지원 및 전투 임무를 위한 상호 운용 가능한 시스템 개발을 목표로 하는 협동형 국방 로봇 프로그램에 집중하고 있습니다. 아시아태평양에서는 국방 예산 증가와 국경 보안 및 해상 감시 강화를 위한 국산 로봇 개발의 중요성이 강조되면서 급속한 성장세를 보이고 있습니다. 중동에서는 지역 안보 이슈에 대응하기 위해 정보 수집 및 기지 방어를 위한 자율 시스템에 대한 투자가 진행되고 있습니다. 라틴아메리카와 아프리카에서는 파트너십과 기술 이전을 통해 국경 감시 및 평화 유지 임무를 위한 무인 시스템 도입이 점차 진행되고 있습니다. 모든 지역에서 자립형 방어 능력의 구축, 디지털 혁신, 차세대 전투 태세로의 추진은 로봇 기술과 자율 시스템의 주류 군사 작전에의 통합을 가속화하고 있습니다.

미 육군은 국방혁신부(DIU)와 협력하여 자율주행 수송차량 시스템(ATV-S) 프로토타입 개발을 추진하기 위해 카네기 로보틱스와 포터라를 선정했습니다. 당초 2023년 12월 육군은 3개 업체(Robotics Research Autonomous Industries(현 Forterra), Neya Systems, Carnegie Robotics)와 총 1,480만 달러 규모의 시제품 개발 계약을 체결했습니다. 미화 1,480만 달러에 수주하였습니다. 이번 신규 계약의 세부 내용(금액, 조건 등)은 아직 공개되지 않았으나, 이번 선정은 1차 심사를 통과한 시제품을 정식 육군 시험평가 단계로 전환하는 것입니다.

지역별

용도별

플랫폼별

10년간 방위용 로봇 및 자율주행차 시장 분석으로는 방위용 로봇 및 자율주행차 시장 성장, 변화하는 동향, 기술 채택 개요 및 전체적인 시장의 매력 상세한 개요가 나타나 이 장으로 설명되고 있습니다.

이 부문에서는 이 시장에 영향을 미치는으로 예상되는 상위 10기술과 이러한 기술이 시장 전체에 미칠 가능성이 있는 영향에 대해 설명합니다.

이 시장 10년간 방위용 로봇 및 자율주행차 시장 예측은 상기 부문 전체에 걸쳐서 상세하게 커버되고 있습니다.

이 부문에서는 지역별 방위용 로봇 및 자율주행차 시장 동향, 촉진요인, 제약 요인, 과제, 그리고 정치, 경제, 사회, 기술이라고 하는 측면을 망라하고 있습니다. 또한 지역별 시장 예측과 시나리오 분석도 상세하게 채택하고 있습니다.지역 분석 마지막에는 주요 기업 프로파일링, 공급업체 상황, 기업 벤치마킹가 포함되어 있습니다.현재 시장 규모는 통상 시나리오에 근거하고 추정되고 있습니다.

북미

성장 촉진요인, 억제요인, 과제

PEST

주요 기업

공급업체 Tier 상황

기업 벤치마킹

유럽

중동

아시아태평양

남미

이 장에서는 이 시장 주요 방위 프로그램을 채택해 이 시장에서 신청된 최신 뉴스나 특허에 대해도 해설합니다. 또한 국가 레벨 10년간 시장 예측과 시나리오 분석에 대해도 해설합니다.

미국

방위 프로그램

최신 뉴스

특허

이 시장에서의 현재 기술 성숙도

캐나다

이탈리아

프랑스

독일

네덜란드

벨기에

스페인

스웨덴

그리스

호주

남아프리카공화국

인도

중국

러시아

한국

일본

말레이시아

싱가포르

브라질

기회 매트릭스는 독자가 이 시장 기회 높은 부문을 이해하는데 도움이 됩니다.

이 시장 가능성 있는 분석에 관한 당사 전문가 의견을 정리했습니다.

The Global Defense Robots and Autonomous Vehicles market is estimated at USD 4.49 billion in 2026, projected to grow to USD 14.01 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 12.05% over the forecast period 2026-2036.

Introduction to Defense Robots and Autonomous Vehicles Market

The defense robots and autonomous vehicles market encompasses unmanned systems designed to perform complex military tasks with minimal human intervention. These systems operate across air, land, and sea domains, executing missions such as reconnaissance, logistics support, surveillance, explosive ordnance disposal, and combat operations. They enhance force protection by performing dangerous tasks in contested or hazardous environments, reducing the risk to human personnel. The integration of robotics and autonomy into defense operations reflects a broader shift toward digitized, networked, and precision-oriented warfare. Defense organizations worldwide are increasingly adopting robotic platforms to boost operational efficiency, maintain situational awareness, and extend the reach of human forces. As artificial intelligence and machine learning continue to mature, autonomous defense systems are evolving from remote-controlled tools to intelligent, decision-supporting assets capable of independent mission execution, redefining the nature of modern military strategy.

Technology is profoundly transforming the defense robots and autonomous vehicles market through innovations in artificial intelligence, advanced sensors, and machine autonomy. Breakthroughs in AI-driven navigation and perception enable these systems to operate independently in complex and dynamic environments. Enhanced sensor fusion allows seamless integration of visual, thermal, and radar data for superior situational awareness and target identification. Edge computing and real-time data processing empower autonomous platforms to make split-second decisions during missions without relying on external communication links. Robotics design advancements have led to lighter, more agile, and energy-efficient platforms adaptable to multiple terrains and mission profiles. Swarm intelligence and collaborative robotics are emerging trends that allow multiple autonomous systems to coordinate actions in synchronized operations. Cybersecurity and secure communication protocols are also integral, ensuring resilience against electronic warfare and interference. These technological developments are positioning robotics and autonomy as the cornerstone of future defense capabilities, enabling precision, adaptability, and operational scalability.

The growth of the defense robots and autonomous vehicles market is driven by the need for enhanced situational awareness, force protection, and operational efficiency in modern warfare. Increasing battlefield complexity, urban combat environments, and asymmetric threats have underscored the value of unmanned systems capable of performing high-risk missions. Defense agencies are prioritizing automation to reduce human casualties, increase mission persistence, and optimize logistics and reconnaissance tasks. The expanding use of AI and autonomy in surveillance, combat support, and decision-making processes further fuels adoption. Governments are also emphasizing technological self-reliance and indigenous development of robotic systems as part of modernization programs. The rise of electronic warfare and the demand for faster, data-driven response capabilities encourage investment in intelligent and connected robotic platforms. Moreover, the growing convergence between civilian robotics innovations and defense applications is accelerating the pace of adoption, shaping a new era of unmanned and autonomous military operations.

Regional trends in the defense robots and autonomous vehicles market reflect varied strategic objectives and technological capabilities. North America leads through sustained investments in unmanned ground, aerial, and maritime systems, integrating advanced autonomy and AI into joint-force operations. Europe focuses on collaborative defense robotics programs aimed at developing interoperable systems for surveillance, logistics, and combat missions. The Asia-Pacific region is experiencing rapid growth, driven by rising defense budgets and emphasis on indigenous robotic development to enhance border security and maritime surveillance. The Middle East is investing in autonomous systems for intelligence gathering and base protection, addressing regional security challenges. Latin America and Africa are gradually adopting unmanned systems for border monitoring and peacekeeping missions through partnerships and technology transfers. Across all regions, the push toward self-reliant defense capabilities, digital transformation, and next-generation combat readiness is accelerating the integration of robotics and autonomy into mainstream military operations.

The U.S. Army, in collaboration with the Defense Innovation Unit (DIU), has chosen Carnegie Robotics and Forterra to advance prototyping efforts for the Autonomous Transport Vehicle System (ATV-S). Initially, in December 2023, the Army awarded development and prototyping contracts to three vendors-Robotics Research Autonomous Industries (now Forterra), Neya Systems, and Carnegie Robotics-valued at $14.8 million for four prototypes each. While the specifics of the new contract, including its value and terms, have not been disclosed, this award represents a first down selection, moving the chosen prototypes into formal Army Test and Evaluation.

By Region

By Application

By Platform

The 10-year Defense Robots And Autonomous Vehicles Market analysis would give a detailed overview of Defense Robots And Autonomous Vehicles Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

The 10-year Defense Robots And Autonomous Vehicles Market forecast of this market is covered in detailed across the segments which are mentioned above.

The regional Defense Robots And Autonomous Vehicles Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Hear from our experts their opinion of the possible analysis for this market.