전기자동차 배터리 부품 시장 : 시장 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)

Electric Vehicle (EV) Battery Components Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1936512

리서치사:Global Market Insights Inc.

발행일:2026년 01월

페이지 정보:영문 254 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

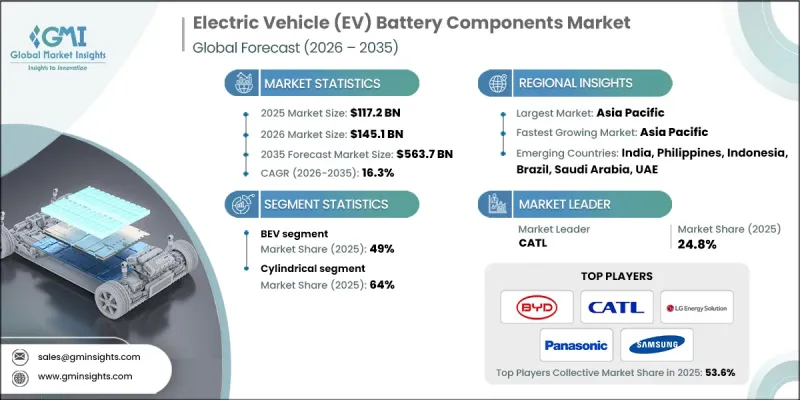

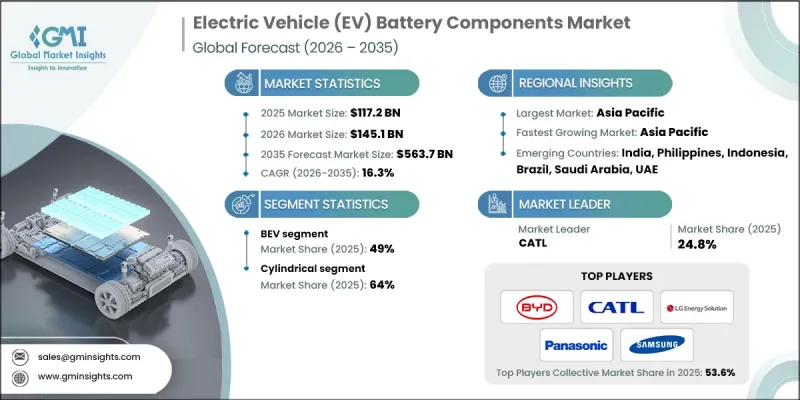

세계의 전기자동차 배터리 부품 시장은 2025년 1,172억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 16.3%로 성장할 전망이며, 5,637억 달러에 이를 것으로 예측됩니다.

세계 전기자동차의 급속한 보급은 자동차의 파워트레인 설계를 변화시키고 공급망을 재구성하도록 촉구하고 있습니다. 배터리 셀, 모듈, 캐소드, 애노드, 배터리 관리 시스템(BMS), 열 관리 솔루션 등의 부품은 현재 차량의 항속 거리, 성능, 안전성, 비용 효율성을 결정하는 핵심 요소가 되었습니다. 자동차 제조업체가 내연기관에서 전용 EV 아키텍처로 전환하는 동안 배터리 시스템은 개별 부품이 아닌 완전히 통합된 플랫폼으로 취급되는 경향이 강해졌으며 운영 가용성과 수명주기 경제성 모두에 영향을 미칩니다. 자동차 제조업체, 배터리 제조업체, 재료 공급업체, 반도체 기업 간 대규모 투자 및 전략적 제휴가 시장을 더욱 강화하고 있습니다. 자사 내에서의 배터리 조립, 현지에서의 셀 생산, 정극재 및 부극재의 합작 사업 등 수직 통합 전략에 의해 OEM 제조업체는 공급 확보, 비용 절감, 품질 향상을 실현하고 있습니다. 또한 광범위한 부품 테스트, 라이프사이클 최적화, 국제 안전 표준 준수는 제품의 신뢰성, 내구성 및 열 안전성을 향상시킵니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035년

시작 시 가치

1,172억 달러

예측 금액

5,637억 달러

CAGR

16.3%

배터리형 전기자동차(BEV) 부문은 2025년에 49%의 점유율을 차지했으며, 2035년까지 연평균 복합 성장률(CAGR) 17%를 나타낼 것으로 예측됩니다. BEV는 완전히 배터리 전력에 의존하기 때문에 장거리 주행, 급속 충전, 안정적인 성능을 보장하기 위해 대용량 셀, 모듈 및 관련 시스템에 대한 강한 수요가 발생하고 있습니다. 제로 방출 차량을 지원하는 세계 정책과 인센티브는 BEV의 보급을 더욱 가속화하고,이 부문을 시장의 주요 촉진요인으로 자리 매김하고 있습니다.

원통형 배터리 부문은 2025년에 64%의 점유율을 차지했으며, 2026-2035년 연평균 복합 성장률(CAGR) 15.7%로 성장할 것으로 예측됩니다. 이 배터리는 검증된 성능, 높은 에너지 밀도, 우수한 열 관리 및 긴 수명주기에 의해 지원됩니다. 모듈 설계와 표준화된 크기로 배터리 팩에 원활하게 통합할 수 있어 조립, 유지보수 및 재활용을 간소화합니다. 원통형 배터리는 향상된 안전성, 안정적인 방열성 및 고전류 부하 하에서의 내구성을 제공하므로 승용차 및 상용 EV 용도 모두에서 선호되는 옵션이 되었습니다.

중국의 전기자동차(EV)용 배터리 부품 시장은 2025년에 큰 점유율을 획득했습니다. 이 나라의 급속한 산업화, 견조한 국내 EV 수요 및 광범위한 공급망 통합은 시장의 강력한 확장을 지원합니다. 중국이 EV 생산의 주요 거점이기 때문에 전지 셀, 정극재, 부극재, 세퍼레이터, 전해액, 케이싱에 대한 수요가 지속적으로 발생하고 있습니다. 업스트림의 리튬 정제, 정극재 제조, 흑연 음극재 생산을 장악하고 있는 것으로, 비용 효율, 신속한 규모 확대, 안정 공급이 확보되고 있습니다. 생산 연동형 인센티브 및 장기적인 산업 계획을 통한 정책 지원에 의해 배터리 부품 부문 전체에서의 기술 도입과 생산 능력 확대가 더욱 가속화되고 있습니다.

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률 분석

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

전기승용차 및 상용차의 세계의 보급 확대

정부에 의한 인센티브, 보조금 및 EV 인프라 투자 증가

배터리 및 기가 공장의 확장과 지역별 생산 능력 확대

물류, 대중교통 및 플릿 차량에 있어서 전기화의 진전

업계의 잠재적 위험 및 과제

중요 배터리 원료의 고비용 및 가격 변동성

대규모 배터리 리사이클 및 사용후 배터리 처리 인프라의 부족

시장 기회

차세대 배터리 화학 기술 및 고체 배터리 부품의 채용 확대

전기차 및 배터리 현지화 정책에 의한 국내 제조 증가

첨단 배터리 관리 시스템 및 파워 일렉트로닉스에 대한 수요 급증

세컨드 라이프 및 리사이클 베이스의 배터리 부품 용도 분야에서의 성장

성장 가능성 분석

규제 상황

북미

미국-NHTSA 자율주행 시스템 안내 및 자율주행차 시험 이니셔티브

유럽

EU 배터리 규제(EU 규칙 2023/1542)

독일-배터리법(Batteriegesetz-BattG)

영국-배터리 및 축전지에 관한 규제

프랑스-배터리에 대한 확대 생산자 책임(EPR)

아시아태평양

중국-신에너지 차량용 파워 배터리의 안전성 및 재활용에 관한 규제

일본-경제산업성 리튬 이온 배터리의 안전 및 재활용에 관한 가이드라인

한국-전기전자기기 및 자동차의 자원순환에 관한 법률

싱가포르-환경 보호 및 관리(전지 폐기물)에 관한 규칙

라틴아메리카

브라질-국가 고형 폐기물 정책(배터리 역물류 규칙)

멕시코-공식 규격 NOM-212-SEMARNAT(배터리 폐기물 관리)

칠레-확대 생산자 책임법(법률 제20,920호)

중동 및 아프리카

아랍에미리트(UAE)-연방 통합 폐기물 관리법(전지 관련 규정)

사우디아라비아-환경법 및 SASO EV 배터리 기술 규제

남아프리카-국가환경관리법-폐기물법(전지 컴플라이언스)

Porter's Five Forces 분석

PESTEL 분석

기술 및 혁신 동향

현재 기술 동향

신흥 기술

특허 분석

지속가능성 및 환경 영향 분석

지속가능한 실천

폐기물 감축 전략

생산에 있어서 에너지 효율화

환경에 배려한 대처

탄소발자국에 관한 고려 사항

전망 및 기회

OEM 도입 프레임워크

수직 통합의 동향

장기 공급 계약 및 부품 가격에 미치는 영향

우선 공급업체 모델 및 오픈 조달

공동 개발 및 합작 사업 모델

이용 사례 및 용도 시나리오

세계 생산 능력 및 가동률 분석

가동 완료 대 발표된 부품 생산 능력

지역별 가동률

과잉 생산 능력 및 공급 부족 위험 지역

부품의 병목 특정

제4장 경쟁 구도

서문

기업의 시장 점유율 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

합병 및 인수

제휴 및 협업

신제품 발매

사업 확대 계획 및 자금 조달

제5장 시장 추계 및 예측 : 배터리 형태별(2022-2035년)

원통형

파우치형

각형 배터리

제6장 시장 추계 및 예측 : 추진력별(2022-2035년)

BEV(배터리식 전기자동차)

PHEV

HEV

제7장 시장 추계 및 예측 : 차량별(2022-2035년)

승용차

세단

해치백

SUV

상용차

경상용차(LCV)

MCV

대형 상용차(HCV)

이륜차 및 삼륜차

제8장 시장 추계 및 예측 : 배터리 화학별(2022-2035년)

인산철 리튬

니켈, 코발트 및 알루미늄

니켈, 망간 및 코발트

리튬망간 산화물

기타

제9장 시장 추계 및 예측 : 컴포넌트별(2022-2035년)

셀 컴포넌트

음극

양극

전해질

기타

포장 부품

배터리 관리 시스템

열 관리 시스템

하우징 및 인클로저

기타

제10장 시장 추계 및 예측 : 지역별(2022-2035년)

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

러시아

벨기에

네덜란드

스웨덴

아시아태평양

중국

인도

일본

호주

한국

필리핀

인도네시아

싱가포르

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제11장 기업 프로파일

세계 기업

BASF SE

BYD

Contemporary Amperex Technology Co. Limited(CATL)

Johnson

LG Energy Solution

Panasonic

Samsung

Umicore

Arkema

지역 기업

Asahi Kasei

BTR New Energy Materials

Celgard

EVE Energy

Ganfeng Lithium

Gotion High-Tech

Huayou Cobalt

JFE Chemical

Mitsubishi Chemical

SK Innovation

Sumitomo Metal Mining

Toray Industries

신흥 기업

Amprius Technologies

Anovion Technologies

Ascend Elements

FREYR Battery

QuantumScape

Redwood Materials

AJY

영문 목차

영문목차

The Global Electric Vehicle Battery Components Market was valued at USD 117.2 billion in 2025 and is estimated to grow at a CAGR of 16.3% to reach USD 563.7 billion by 2035.

The rapid adoption of electric vehicles worldwide is transforming automotive powertrain design and reshaping supply chains. Components such as battery cells, modules, cathodes, anodes, battery management systems (BMS), and thermal management solutions are now central to determining vehicle range, performance, safety, and cost efficiency. As automakers shift from internal combustion engines to dedicated EV architectures, battery systems are increasingly treated as fully integrated platforms rather than individual parts, influencing both operational viability and lifecycle economics. The market is further boosted by large-scale investments and strategic collaborations among automakers, battery manufacturers, material suppliers, and semiconductor firms. Vertical integration strategies, including in-house battery assembly, localized cell production, and joint ventures for cathode and anode materials, are enabling OEMs to secure supplies, lower costs, and improve quality. Additionally, extensive component testing, lifecycle optimization, and adherence to global safety standards are enhancing product reliability, durability, and thermal safety.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$117.2 Billion

Forecast Value

$563.7 Billion

CAGR

16.3%

The battery electric vehicle (BEV) segment held 49% share in 2025 and is expected to grow at a CAGR of 17% through 2035. BEVs rely entirely on battery power, driving strong demand for high-capacity cells, modules, and associated systems to ensure long driving ranges, rapid charging, and consistent performance. Global policies and incentives supporting zero-emission vehicles further accelerate BEV adoption, positioning this segment as the primary growth driver for the market.

The cylindrical cells segment held 64% share in 2025, with projected growth at a CAGR of 15.7% from 2026 to 2035. These cells are favored for their proven performance, high energy density, superior thermal management, and long lifecycle. Their modular design and standardized sizes allow seamless integration into battery packs, simplifying assembly, maintenance, and recycling. Cylindrical cells also provide enhanced safety, reliable heat dissipation, and durability under high current loads, making them a preferred choice for both passenger and commercial EV applications.

China Electric Vehicle (EV) Battery Components Market reached a significant share in 2025. The country's rapid industrialization, strong domestic EV demand, and extensive supply chain integration support robust market expansion. China's dominant EV production base drives ongoing demand for battery cells, cathodes, anodes, separators, electrolytes, and casings. Control over upstream lithium refining, cathode manufacturing, and graphite anode production ensures cost efficiency, rapid scaling, and stable supply. Policy support through production-linked incentives and long-term industrial planning further accelerates technology adoption and capacity expansion across battery component segments.

Key players shaping the Global Electric Vehicle Battery Components Market include CATL, BYD, Panasonic, Blue Line Battery, Johnson Matthey, Mitsubishi Chemical, LG Energy Solution, Samsung SDI, Sumitomo Metal Mining, and Umicore. Leading companies in the Electric Vehicle Battery Components Market are adopting multiple strategies to strengthen their market presence and competitive position. These include forming strategic alliances with automakers and material suppliers to secure raw material access, investing in localized manufacturing to reduce costs and improve supply chain resilience, and expanding R&D efforts to develop next-generation high-capacity, fast-charging, and longer-lasting battery systems. Companies are also enhancing production scalability, integrating advanced thermal management and battery management technologies, and pursuing mergers or joint ventures to enter new geographic markets. Focused testing, lifecycle optimization, and adherence to global safety and environmental standards further improve product reliability, building trust among OEMs and fleet operators and solidifying long-term market foothold.

Table of Contents

Chapter 1 Methodology

1.1 Research approach

1.2 Quality commitments

1.2.1 GMI AI policy & data integrity commitment

1.3 Research trail & confidence scoring

1.3.1 Research trail components

1.3.2 Scoring components

1.4 Data collection

1.4.1 Partial list of primary sources

1.5 Data mining sources

1.5.1 Paid sources

1.6 Base estimates and calculations

1.6.1 Base year calculation

1.7 Forecast model

1.8 Research transparency addendum

Chapter 2 Executive Summary

2.1 Industry 360° synopsis, 2022 - 2035

2.2 Key market trends

2.2.1 Regional

2.2.2 Battery Form

2.2.3 Propulsion

2.2.4 Vehicle

2.2.5 Battery Chemistry

2.2.6 Component

2.3 TAM Analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising global adoption of electric passenger and commercial vehicles

3.2.1.2 Increase in government incentives, subsidies, and EV infrastructure investments

3.2.1.3 Expansion of battery giga factories and localized manufacturing capacity

3.2.1.4 Growing electrification of logistics, public transport, and fleet vehicles

3.2.2 Industry pitfalls and challenges

3.2.2.1 High cost and price volatility of critical battery raw materials

3.2.2.2 Limited large-scale battery recycling and end-of-life infrastructure

3.2.3 Market opportunities

3.2.3.1 Rise in adoption of next-generation battery chemistries and solid-state components

3.2.3.2 Increase in domestic manufacturing supported by EV and battery localization policies

3.2.3.3 Surge in demand for advanced battery management systems and power electronics

3.2.3.4 Growth in second life and recycling-based battery component applications

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.1.1 United States: NHTSA ADS Guidance & AV TEST Initiative.

3.4.2 Europe

3.4.2.1 EU Battery Regulation (Regulation (EU) 2023/1542)