전기자동차 배터리 테스트 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)

Electric Vehicle Battery Testing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1928935

리서치사:Global Market Insights Inc.

발행일:2026년 01월

페이지 정보:영문 250 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

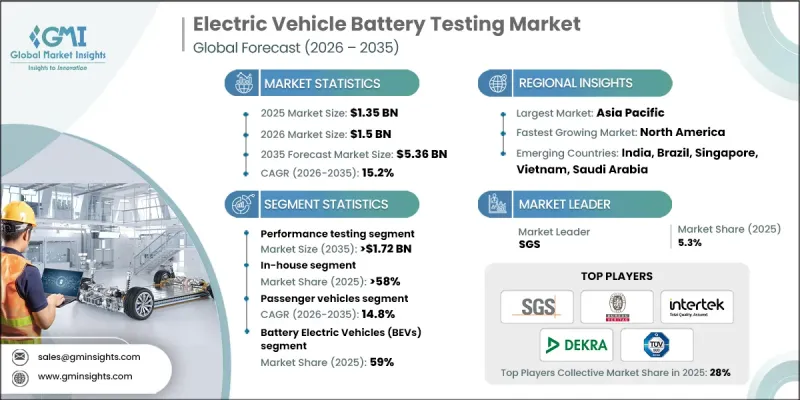

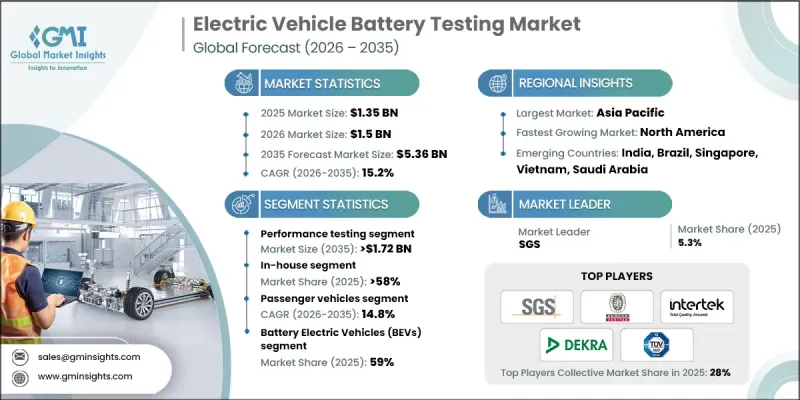

세계의 전기자동차 배터리 테스트 시장은 2025년에 13억 5,000만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 15.2%로 성장하여 53억 6,000만 달러에 이를 것으로 예측됩니다.

시장 확대는 전 세계 전기차 생산의 가속화와 밀접한 관련이 있으며, 이로 인해 배터리 제조업체와 공급업체는 안전성, 신뢰성, 성능을 확인하기 위한 첨단 테스트 솔루션을 도입해야 하는 상황에 직면해 있습니다. 배터리 설계가 고에너지 밀도, 소형화, 새로운 화학적 구성으로 진화함에 따라 고장에 따른 재정적, 안전적 위험은 계속 증가하고 있습니다. 제조업체는 대량 생산 시 제품의 일관성을 보장하기 위해 여러 작동 조건에서 종합적인 검증을 우선시합니다. 또한, 셀, 모듈, 팩의 각 레벨에서 장기 내구성, 열화 거동, 가혹한 조건 내성, 열 안정성에 대한 평가 요구가 테스트 수요를 촉진하고 있습니다. 배터리 교체 비용이 높아지는 상황에서 배터리 테스트는 위험 관리 전략의 필수 요소로 자리 잡았습니다. 과거에는 규제 준수를 위한 활동이었지만, 현재는 전기 모빌리티 생태계 전반에서 브랜드 가치 보호, 보증 리스크 감소, 전반적인 제품 품질 향상을 위한 전략적 투자로 인식되고 있습니다.

시장 범위

개시 연도

2025년

예측 연도

2026-2035년

개시 연도 가치

13억 5,000만 달러

예측 금액

53억 6,000만 달러

CAGR

15.2%

성능 테스트 부문은 2025년 38%의 점유율을 차지하며 2035년까지 17억 2,000만 달러에 이를 것으로 예측됩니다. 이 부문은 다양한 부하 조건과 작동 환경에서 배터리가 어떻게 효율적으로 전력을 공급할 수 있는지를 평가하는 데 중점을 두고 있습니다. 수명주기 평가는 기본 충전 주기를 넘어 가속 열화 테스트, 예측 열화 분석, 고급 배터리 건전성 모델링을 포함하여 차량의 더 긴 사용 기대치를 뒷받침하고 있습니다.

승용차 부문은 2034년까지 연평균 14.8%의 성장률을 보일 것으로 예측됩니다. 전기 승용차의 보급 확대에 따라 주행거리, 충전 성능, 내구성, 안전성에 대한 엄격한 요구 사항을 충족하는 배터리에 대한 수요가 지속적으로 증가하고 있습니다. 제조업체는 일관된 성능을 보장하고 신뢰성에 대한 소비자의 기대에 부응하기 위해 광범위한 테스트 프로토콜에 의존하고 있습니다.

미국 전기자동차 배터리 테스트 시장은 2025년 2억 3,220만 달러로 평가되었고, 2026년부터 2035년까지 견조한 성장세를 보일 것으로 예측됩니다. 안전 검증과 규제 준수에 대한 관심이 높아지면서 고급 테스트 서비스에 대한 수요가 증가하고 있습니다. 제조업체들은 증가하는 기술적 과제와 컴플라이언스 대응을 관리하면서 신속한 제품화를 지원하기 위해 사내 및 외부 위탁 시험 역량을 확대하고 있습니다.

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 상황

이익률 분석

비용 구조

각 단계 부가가치

밸류체인에 영향을 미치는 요인

파괴적 변화

업계에 대한 영향요인

성장 촉진요인

세계의 전기자동차 생산 성장

엄격한 배터리 안전기준 및 규제 기준

배터리 에너지 밀도 향상과 시스템 복잡성 증가

OEM 품질 보증과 보증 리스크 저감에의 주력

세계의 배터리 제조능력 확대

업계의 잠재적 리스크&과제

첨단시험 인프라 고액의 자본비용

긴 시험 사이클과 시장 투입까지 시간적 압력

시장 기회

제삼자에 의한 배터리 테스트 서비스 성장

디지털 및 자동화 시험 기술 진보

차세대 배터리 화학 부상

배터리 수명주기 확대와 세컨드 라이프 응용

성장 가능성 분석

규제 상황

북미

미국 : NHTSA 자동차 사이버 보안 베스트 프랙티스

캐나다 : 캐나다 자동차 안전기준(CMVSS)

유럽

영국 : UNECE 규칙 제13호 차량 제동·안정성 시스템

독일 : ISO 26262 도로 차량 전기 전자 시스템 기능 안전

프랑스 : UNECE 규칙 제79호 스티어링 및 차량 제어 시스템

이탈리아 : ISO 21434 도로 차량 사이버 보안 공학

스페인 : ISO 14001 환경 매니지먼트 시스템

아시아태평양

중국 : GB/T 38628전기자동차 배터리 테스트 및 OTA 갱신 보안 요건

일본 : ISO 26262 도로 차량 전기 전자 시스템 기능 안전

인도 : AIS 155 자동차 소프트웨어용 사이버 보안 및 OTA 요건

라틴아메리카

브라질 : ABNT NBR ISO 26262 도로 차량 기능 안전

멕시코 : NOM-194-SCFI 차량 안전성능기준

아르헨티나 : ISO 9001 품질 매니지먼트 시스템

중동 및 아프리카

아랍에미리트(UAE) : UNECE 규칙 제 155호 사이버 보안 및 사이버 보안 관리 시스템

남아프리카공화국 : ISO 26262 도로 차량 전기 전자 시스템 기능 안전

사우디아라비아 : SASO 자동차 기술 규제 사이버 보안과 소프트웨어

Porter의 Five Forces 분석

PESTEL 분석

기술과 혁신 동향

현재 기술 동향

신기술

비용 내역 분석

특허 분석

지속가능성과 환경면

지속가능한 실천

폐기물 감축 전략

생산 에너지 효율

친환경 이니셔티브

탄소발자국에 관한 고려사항

시험 기준과 프로토콜

배터리 테스트 기준과 프로토콜

인증 시험과 검증 시험과 형 식 승인 시험 비교

필수 시험 요건과 OEM 고유 시험 요건

배터리 화학 유형별 시험

배터리 화학 유형별 시험 요건

화학 조성별 열폭주 및 남용 시험 진화

수명주기 단계에 근거한 시험

디지털, AI 및 시뮬레이션 기반 시험

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

인수합병(M&A)

제휴·협력 관계

신제품 발매

사업 확대 계획과 자금조달

제5장 시장 추산·예측 : 시험별, 2022-2035

성능 테스트

안전성 시험

수명주기 시험

기타

제6장 시장 추산·예측 : 조달 방법별, 2022-2035

자사 조달

아웃소싱

제7장 시장 추산·예측 : 차량별, 2022-2035

승용차

해치백

세단

SUV

상용차

소형 상용차(LCV)

중형 상용차(MCV)

대형 상용차(HCV)

제8장 시장 추산·예측 : 추진력별, 2022-2035

배터리 전기자동차(BEV)

플러그인 하이브리드 전기자동차(PHEV)

하이브리드 전기자동차(HEV)

제9장 시장 추산·예측 : 컴포넌트별, 2022-2035

배터리 셀

배터리 모듈

배터리 팩

배터리 관리 시스템(BMS)

제10장 시장 추산·예측 : 최종 용도별, 2022-2035

자동차 제조업체

배터리 제조업체

연구개발 기관

제삼자 시험 서비스 제공 사업자

제11장 시장 추산·예측 : 지역별, 2022-2035

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

러시아

북유럽 국가

포르투갈

크로아티아

베네룩스

아시아태평양

중국

인도

일본

호주

한국

싱가포르

태국

인도네시아

베트남

라틴아메리카

브라질

멕시코

아르헨티나

콜롬비아

중동 및 아프리카

남아프리카공화국

사우디아라비아

아랍에미리트

튀르키예

제12장 기업 개요

세계 기업

ALS

Applus+

Bureau Veritas

DEKRA

DNV

Element Materials Technology

Eurofins

Intertek

SGS

TUV SUD

UL Solutions

지역 기업

AVL

CSA

FEV

Instron

KEMA Labs

Nemko

NTS(National Technical Systems)

Tektronix

VDE Testing and Certification

Emerging/Disruptor Players

Arbin Instruments

AVILOO

Bitrode

Chroma ATE

Digatron

Espec

Hioki

Keysight Technologies

Maccor

Weiss Technik

LSH

영문 목차

영문목차

The Global Electric Vehicle Battery Testing Market was valued at USD 1.35 billion in 2025 and is estimated to grow at a CAGR of 15.2% to reach USD 5.36 billion by 2035.

Market expansion is tied to the accelerating production of electric vehicles worldwide, which is pushing battery manufacturers and suppliers to adopt advanced testing solutions to confirm safety, reliability, and performance. As battery designs evolve toward higher energy density, compact form factors, and new chemical compositions, the financial and safety risks associated with failure continue to rise. Manufacturers are prioritizing comprehensive validation across multiple operating conditions to ensure product consistency during mass production. Testing demand is further strengthened by the need to evaluate long-term durability, degradation behavior, abuse tolerance, and thermal stability across cell, module, and pack levels. Battery testing has become an essential component of risk management strategies as the cost of battery replacement remains high. What was once a compliance-driven activity is now viewed as a strategic investment to protect brand reputation, reduce warranty exposure, and improve overall product quality across the electric mobility ecosystem.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$1.35 Billion

Forecast Value

$5.36 Billion

CAGR

15.2%

The performance testing segment held 38% share in 2025 and is projected to reach USD 1.72 billion by 2035. This segment focuses on assessing how efficiently batteries deliver power under varying load conditions and operating environments. Lifecycle evaluation has expanded beyond basic charge cycles to include accelerated aging, predictive degradation analysis, and advanced battery health modeling, supporting longer vehicle usage expectations.

The passenger vehicle segment is expected to grow at a CAGR of 14.8% throughout 2034. Rising adoption of electric passenger cars continues to increase demand for batteries that meet strict requirements related to driving range, charging performance, durability, and safety. Manufacturers depend on extensive testing protocols to ensure consistent performance and align with consumer expectations for reliability.

US Electric Vehicle Battery Testing Market was valued at USD 232.2 million in 2025 and is expected to record strong growth from 2026 to 2035. Increasing emphasis on safety validation and regulatory compliance is driving demand for advanced testing services. Manufacturers are expanding internal and outsourced testing capabilities to support faster commercialization while managing growing technical and compliance challenges.

Key companies active in the Global Electric Vehicle Battery Testing Market include SGS, UL Solutions, Intertek, TUV SUD, Bureau Veritas, DEKRA, Eurofins, DNV, Applus+, and Element. Companies operating in the Global Electric Vehicle Battery Testing Market are reinforcing their market position by expanding technical capabilities and service breadth. Investments in advanced testing infrastructure, automation, and simulation tools allow faster and more precise validation. Strategic partnerships with battery manufacturers and vehicle OEMs support long-term service agreements and recurring revenue. Many players are broadening global laboratory networks to serve customers across regions with consistent standards. A strong focus on safety, reliability, and time-to-market optimization helps testing providers differentiate their offerings while supporting the evolving requirements of next-generation electric vehicle batteries.

Table of Contents

Chapter 1 Methodology

1.1 Research approach

1.2 Quality commitments

1.2.1 GMI AI policy & data integrity commitment

1.3 Research trail & confidence scoring

1.3.1 Research trail components

1.3.2 Scoring components

1.4 Data collection

1.4.1 Partial list of primary sources

1.5 Data mining sources

1.5.1 Paid sources

1.6 Base estimates and calculations

1.6.1 Base year calculation

1.7 Forecast

1.8 Research transparency addendum

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2022 - 2035

2.2 Key market trends

2.2.1 Regional

2.2.2 Testing

2.2.3 Sourcing

2.2.4 Vehicle

2.2.5 Propulsion

2.2.6 Component

2.2.7 End use

2.3 TAM Analysis, 2026-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook & strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1.1 Growth drivers

3.2.1.2 Growth in global electric vehicle production

3.2.1.3 Stringent battery safety and regulatory standards

3.2.1.4 Increasing battery energy density and system complexity

3.2.1.5 OEM focus on quality assurance and warranty risk reduction

3.2.1.6 Expansion of global battery manufacturing capacity

3.2.2 Industry pitfalls and challenges

3.2.2.1 High capital cost of advanced testing infrastructure

3.2.2.2 Long testing cycles and time-to-market pressures

3.2.3 Market opportunities

3.2.3.1 Growth of third-party battery testing services

3.2.3.2 Advancements in digital and automated testing technologies

3.2.3.3 Emergence of next-generation battery chemistries

3.2.3.4 Expansion of battery lifecycle and second-life applications

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.1.1 United States: NHTSA Automotive Cybersecurity Best Practices

3.4.1.2 Canada: Canadian Motor Vehicle Safety Standards CMVSS

3.4.2 Europe

3.4.2.1 UK: UNECE Regulation No. 13 Vehicle Braking and Stability Systems

3.4.2.2 Germany: ISO 26262 Functional Safety of Electrical and Electronic Systems in Road Vehicles

3.4.2.3 France: UNECE Regulation No. 79 Steering and Vehicle Control Systems

3.4.2.4 Italy: ISO 21434 Road Vehicles Cybersecurity Engineering

3.4.2.5 Spain: ISO 14001 Environmental Management Systems

3.4.3 Asia Pacific

3.4.3.1 China: GB/T 38628 Electric Vehicle Battery Testing and OTA Update Security Requirements

3.4.3.2 Japan: ISO 26262 Functional Safety of Electrical and Electronic Systems in Road Vehicles

3.4.3.3 India: AIS 155 Cybersecurity and OTA Requirements for Automotive Software

3.4.4 Latin America

3.4.4.1 Brazil: ABNT NBR ISO 26262 Functional Safety for Road Vehicles

3.4.4.2 Mexico: NOM-194-SCFI Vehicle Safety and Performance Standards

3.4.4.3 Argentina: ISO 9001 Quality Management Systems

3.4.5 Middle East & Africa

3.4.5.1 UAE: UNECE Regulation No. 155 Cybersecurity and Cybersecurity Management Systems

3.4.5.2 South Africa: ISO 26262 Functional Safety of Electrical and Electronic Systems in Road Vehicles

3.4.5.3 Saudi Arabia: SASO Automotive Technical Regulations Cybersecurity and Software

3.5 Porter';s analysis

3.6 PESTEL analysis

3.7 Technology and innovation landscape

3.7.1 Current technological trends

3.7.2 Emerging technologies

3.8 Cost breakdown analysis

3.9 Patent analysis

3.10 Sustainability and environmental aspects

3.10.1 Sustainable practices

3.10.2 Waste reduction strategies

3.10.3 Energy efficiency in production

3.10.4 Eco-friendly initiatives

3.10.5 Carbon footprint considerations

3.11 Testing Standards & Protocols

3.11.1 Battery testing standards & protocols

3.11.2 Certification vs validation vs homologation testing

3.11.3 Mandatory vs OEM-specific test requirements

3.12 Battery Chemistry-Specific Testing

3.12.1 Testing requirements by battery chemistry

3.12.2 Thermal runaway & abuse testing evolution by chemistry