승용차용 디지털 트윈 시장 : 시장 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)

Passenger Car Digital Twin Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1936504

리서치사:Global Market Insights Inc.

발행일:2026년 01월

페이지 정보:영문 250 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

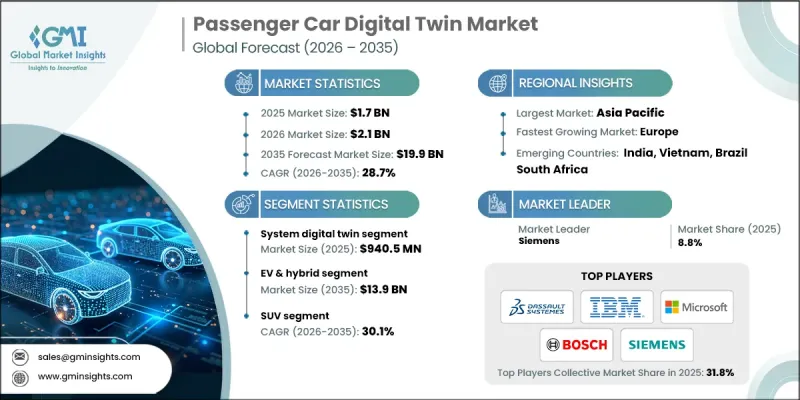

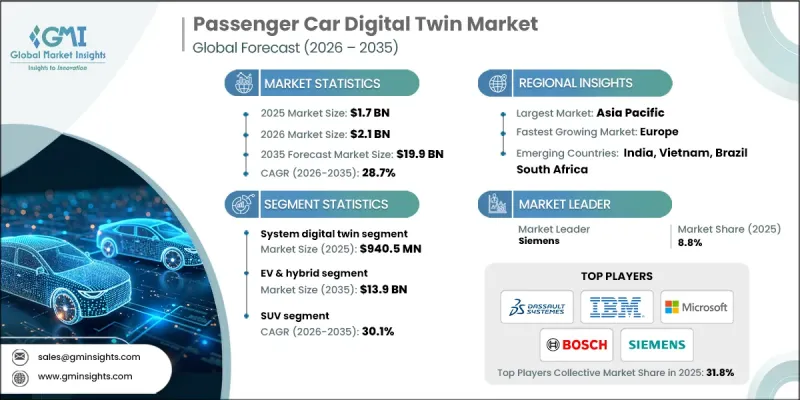

세계의 승용차용 디지털 트윈 시장은 2025년에 17억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 28.7%로 성장할 전망이며, 199억 달러에 이를 것으로 예측됩니다.

자동차 생산에는 개발 사이클의 단축, 수복의 최소화, 프로토타입 비용 절감, 설비 및 부품의 고장 방지를 실현하는 첨단 기술이 요구되고 있습니다. 디지털 트윈 플랫폼은 물리적 생산을 시작하기 전에 차량 수명주기 전반에 걸쳐 가상 검증을 가능하게 함으로써 이러한 요구를 충족시킵니다. 제조업체는 이러한 시스템을 활용하고 설계, 제조 및 운영 거동을 실시간으로 시뮬레이션함으로써 의사 결정과 비용 관리를 크게 개선하고 있습니다. 인공지능(AI)과 머신러닝은 조기 고장 검출, 성능 검증, 예측 고장 분석을 가능하게 함으로써 디지털 트윈의 가치를 더욱 향상시킵니다. 이러한 기능을 통해 제조업체와 공급업체는 차량이 시장에 나가기 전에 문제를 파악할 수 있습니다. 데이터 구동형 제조, 커넥티드 팩토리, 소프트웨어 정의 차량으로의 전환이 진행되고 있는 가운데, 현대의 자동차 생산 전략의 핵심 추진력으로서 디지털 트윈에 대한 의존도는 계속 증가하고 있습니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035년

시작 시 가치

17억 달러

예측 금액

199억 달러

CAGR

28.7%

시스템 수준의 디지털 트윈 부문은 2025년에 55.2%의 점유율을 차지하여, 약 9억 4,050만 달러를 창출했습니다. 이 부문의 이점은 상호 연결된 차량 시스템의 종합적인 시뮬레이션에 대한 수요가 증가하고 있기 때문입니다. 시스템 디지털 트윈을 통해 제조업체는 전원 공급, 안전 아키텍처, 디지털 인터페이스와 같은 서브시스템 간 복잡한 상호작용을 분석할 수 있습니다. 이러한 모델은 실시간 시스템 모니터링 및 예측 유지 보수를 지원하여 생산 및 운영 단계 전반에 걸쳐 신뢰성을 향상시키고 다운타임을 줄입니다.

전기자동차 및 하이브리드 자동차 부문은 2025년에 64.6%의 점유율을 차지하였고, 2035년까지 139억 달러에 이를 것으로 예측됩니다. 이 차량은 디지털 트윈 플랫폼과 원활하게 작동하는 고급 전자 부품 및 센서를 통합합니다. 디지털 트윈은 전기자동차 및 하이브리드 플랫폼에 중요한 요소인 배터리의 노후화, 열 성능, 전력 효율 및 소프트웨어 동작 시뮬레이션을 제조업체에 제공합니다. 이 기능을 통해 디지털 트윈은 차세대 차량 아키텍처를 최적화하는 필수 도구로 자리를 잡고 있습니다.

미국의 승용차용 디지털 트윈 시장은 2025년 3억 4,820만 달러에 달했습니다. 제조업체가 스마트 제조 이니셔티브의 일환으로 디지털 트윈을 도입하고 생산 라인 최적화, 운영 중단 감소, 공급망 복잡성 대응을 추진함에 따라 채용이 확대되고 있습니다. 제조 환경의 실시간 디지털 복제를 통해 문제 해결을 가속화하고 지속적인 성능을 향상시킬 수 있습니다. 클라우드 기반 플랫폼과 연결 시스템은 생산 및 생산 후 분석에서 디지털 트윈의 채택을 더욱 지원합니다.

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

소프트웨어 정의 차량(SDV)의 보급 확대

승용차 아키텍처의 복잡성 증가

가상 프로토타이핑 및 시뮬레이션에 대한 수요 증가

OEM에 있어서 시장 투입 기간의 단축에 대한 주력

업계의 잠재적 위험 및 과제

높은 도입 및 통합 초기 비용

사이버 보안 및 데이터 프라이버시에 대한 우려 사항

시장 기회

차량 라이프 사이클 각 단계에서의 디지털 트윈 도입

가동 중 차량 모니터링을 위한 실시간 디지털 트윈

디지털 트윈에 의해 강화된 사용량 베이스 보험(UBI) 모델

컴포넌트 검증을 위한 디지털 트윈 솔루션 공동 개발

성장 가능성 분석

규제 상황

북미

미국 도로교통안전국(NHTSA)

FMVSS(연방 자동차 안전 기준)

EPA(환경보호청)

캐나다 자동차 안전 기준(운수성)

유럽

유럽위원회(EC)

UNECE(유엔 유럽 경제위원회)

EU 일반 데이터 보호 규칙(GDPR(EU 개인정보보호규정))

아시아태평양

JASIC(일본 자동차 규격 국제화 센터)

SAE 중국(중국 자동차 기술자 협회)

KATS(한국자동차기술연구원)

AIS(자동차 산업 표준)

라틴아메리카

전국 자동차 제조업자 협회

국립 계량 표준화 산업 규격 연구소(INMETRO)

라틴아메리카의 차량 안전 규제

중동 및 아프리카

GCC 표준화 기구(GSO)

남아프리카 표준국(SABS)

사우디아라비아 규격, 계량 및 품질 기구(SASO)

Porter's Five Forces 분석

PESTEL 분석

기술 및 혁신 동향

현재 기술 동향

신흥 기술

비용 내역 분석

지속가능성 및 환경에 미치는 영향

환경 영향 평가

사회적 영향 및 지역 사회에 대한 이익

거버넌스 및 기업의 사회적 책임

지속 가능한 금융 및 투자 동향

디지털 트윈을 위한 데이터 아키텍처

실시간 데이터 스트리밍 아키텍처

센서 데이터 관리 및 처리

데이터 품질 및 거버넌스의 틀

상호 운용성 및 데이터 교환 프로토콜

사이버 보안 및 프라이버시의 틀

디지털 트윈 사이버 보안 위협 상황

데이터 암호화 및 액세스 제어 메커니즘

제로 트러스트 아키텍처 도입

프라이버시 보호 기술

컴플라이언스 프레임 워크

사례 연구

전망 및 기회

제4장 경쟁 구도

서문

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

합병 및 인수

제휴 및 협업

신제품 발매

사업 확대 계획 및 자금 조달

제5장 시장 추계 및 예측 : 컴포넌트별(2022-2035년)

하드웨어

IoT 센서 및 디바이스

엣지 컴퓨팅 하드웨어

데이터 수집 시스템

연결성 인프라

소프트웨어

서비스

전문 서비스

시스템 통합

연수 및 컨설팅

지원 및 유지 보수

매니지드 서비스

제6장 시장 추계 및 예측 : 디지털 트윈별(2022-2035년)

시스템 및 디지털 트윈

제품 디지털 트윈

프로세스 및 디지털 트윈

제7장 시장 추계 및 예측 : 도입 형태별(2022-2035년)

클라우드 기반

온프레미스

하이브리드

제8장 시장 추계 및 예측 : 차량별(2022-2035년)

해치백

세단

SUV

제9장 시장 추계 및 예측 : 추진력별(2022-2035년)

내연기관(ICE)

전기자동차(EV) 및 하이브리드 자동차

배터리식 전기자동차(BEV)

플러그인 하이브리드 전기자동차(PHEV)

하이브리드 전기자동차(HEV)

연료전지 전기자동차(FCEV)

제10장 시장 추계 및 예측 : 용도별(2022-2035년)

제품 설계 및 개발

예지보전 및 성능 모니터링

제조 및 공정 최적화

가동중의 운용 및 플릿 관리

제11장 시장 추계 및 예측 : 최종 용도별(2022-2035년)

OEM

1단계 및 2단계 공급업체

자동차용 소프트웨어 및 기술 기업

이동성 서비스 제공업체

보험사

애프터마켓 및 서비스 센터

제12장 시장 추계 및 예측 : 지역별(2022-2035년)

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

러시아

체코 공화국

벨기에

네덜란드

아시아태평양

중국

인도

일본

한국

호주

싱가포르

말레이시아

인도네시아

베트남

태국

라틴아메리카

브라질

멕시코

아르헨티나

콜롬비아

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제13장 기업 프로파일

세계 기업

ANSYS

Autodesk

Dassault

GE Vernova

Hexagon

IBM

Microsoft

NVIDIA

PTC

Robert Bosch

SAP

Siemens

지역 기업

ABB

AVEVA

Emerson

Honeywell

Oracle

Rockwell

Schneider

TCS

신흥 기업

Amazon Web Services

Lauterbach

Toobler

Unity

Valeo

AJY

영문 목차

영문목차

The Global Passenger Car Digital Twin Market was valued at USD 1.7 billion in 2025 and is estimated to grow at a CAGR of 28.7% to reach USD 19.9 billion by 2035.

Automotive production demands advanced technologies that reduce development cycles, minimize rework, lower prototype costs, and prevent equipment or component failures. Digital twin platforms address these needs by enabling virtual validation across the vehicle lifecycle before physical production begins. Manufacturers rely on these systems to simulate design, manufacturing, and operational behavior in real time, significantly improving decision-making and cost control. Artificial intelligence and machine learning further enhance digital twin value by enabling early fault detection, performance validation, and predictive failure analysis. These capabilities allow manufacturers and suppliers to identify issues before vehicles reach the market. The shift toward data-driven manufacturing, connected factories, and software-defined vehicles continues to increase reliance on digital twins as a core enabler of modern automotive production strategies.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$1.7 Billion

Forecast Value

$19.9 Billion

CAGR

28.7%

The system-level digital twins segment held a 55.2% share in 2025, generating approximately USD 940.5 million. This segment dominates due to the rising demand for holistic simulation of interconnected vehicle systems. System digital twins allow manufacturers to analyze complex interactions between subsystems such as power delivery, safety architecture, and digital interfaces. These models support real-time system monitoring and predictive maintenance, improving reliability and reducing downtime across production and operational stages.

The electric and hybrid vehicles segment held 64.6% share in 2025 and is projected to reach USD 13.9 billion by 2035. These vehicles integrate advanced electronic components and sensors that connect seamlessly with digital twin platforms. Digital twins help manufacturers simulate battery aging, thermal performance, power efficiency, and software behavior, which are critical factors for electric and hybrid platforms. This capability positions digital twins as essential tools for optimizing next-generation vehicle architectures.

United States Passenger Car Digital Twin Market reached USD 348.2 million in 2025. Adoption grows as manufacturers deploy digital twins within smart manufacturing initiatives to optimize production lines, reduce operational disruptions, and address supply chain complexity. Real-time digital replicas of manufacturing environments enable faster issue resolution and continuous performance improvement. Cloud-based platforms and connected systems further support digital twin adoption across production and post-production analytics.

Key companies active in the Global Passenger Car Digital Twin Market include Siemens, NVIDIA, SAP, Dassault, PTC, Microsoft, ANSYS, IBM, GE Vernova, and Robert Bosch. Companies in the passenger car digital twin market strengthen their competitive position by investing in AI-driven simulation, cloud-native platforms, and scalable digital engineering solutions. Many focus on integrating digital twins across design, manufacturing, and after-sales operations to deliver end-to-end lifecycle value. Strategic partnerships with automakers and suppliers accelerate platform adoption and customization. Continuous innovation in predictive analytics, real-time monitoring, and system interoperability enhances differentiation. Vendors emphasize compatibility with connected factory infrastructure and vehicle software ecosystems.

Table of Contents

Chapter 1 Methodology

1.1 Research approach

1.2 Quality commitments

1.2.1 GMI AI policy & data integrity commitment

1.3 Research trail & confidence scoring

1.3.1 Research trail components

1.3.2 Scoring components

1.4 Data collection

1.4.1 Partial list of primary sources

1.5 Data mining sources

1.5.1 Paid sources

1.6 Base estimates and calculations

1.6.1 Base year calculation

1.7 Forecast model

1.8 Research transparency addendum

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Component

2.2.3 Digital Twin

2.2.4 Deployment Mode

2.2.5 Vehicle

2.2.6 Propulsion

2.2.7 Application

2.2.8 End-Use

2.3 TAM analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising adoption of software-defined vehicles (SDVs)

3.2.1.2 Increasing complexity of passenger car architectures

3.2.1.3 Growing demand for virtual prototyping and simulation

3.2.1.4 OEM focus on reducing time-to-market

3.2.2 Industry pitfalls and challenges

3.2.2.1 High initial implementation and integration costs

3.2.2.2 Cybersecurity and data privacy concerns

3.2.3 Market opportunities

3.2.3.1 Digital twin deployment across vehicle lifecycle phases

3.2.3.2 Real-time digital twins for in-use vehicle monitoring

3.2.3.3 Usage-based insurance (UBI) models enhanced by digital twins

3.2.3.4 Co-development of digital twin solutions for component validations

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.1.1 National Highway Traffic Safety Administration (NHTSA)

3.4.1.2 FMVSS (Federal Motor Vehicle Safety Standards)

3.4.1.3 EPA (Environmental Protection Agency)

3.4.1.4 Canadian Motor Vehicle Safety Standards (Transport Canada)

3.4.2 Europe

3.4.2.1 European Commission (EC)

3.4.2.2 UNECE (United Nations Economic Commission for Europe)

3.4.2.3 EU General Data Protection Regulation (GDPR)