자동차 도장 로봇 시스템 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2025-2034년)

Automotive Paint Robot System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1876544

리서치사:Global Market Insights Inc.

발행일:2025년 11월

페이지 정보:영문 230 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

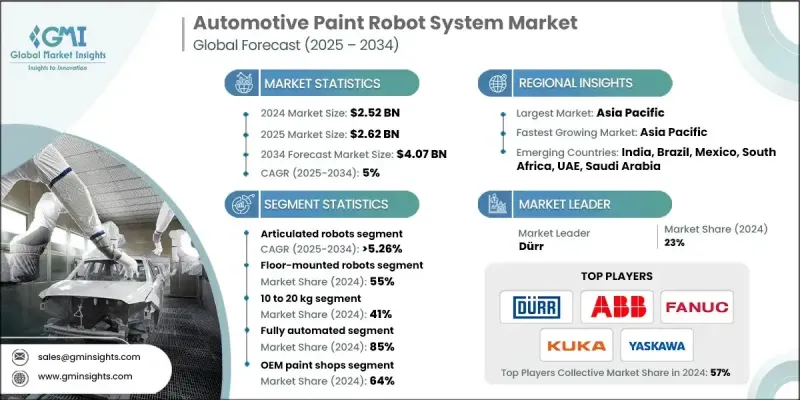

세계의 자동차 도장 로봇 시스템 시장은 2024년에 25억 2,000만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 5%를 나타내 40억 7,000만 달러에 이를 것으로 예측되고 있습니다.

자동차 생산시설에 있어서 자동화의 보급 확대가 본 시장의 성장을 견인하고 있어, 제조업체 각사는 차량 도장 공정에 있어서 정밀도, 균일성, 지속가능성의 향상을 추구하고 있습니다. 바디의 취급, 도장, 마무리를 자동화하는 자동차 도장 로봇 시스템은 현대의 차량 제조 라인에 있어서 필수적인 존재가 되고 있습니다. 세계 자동차 생산량 증가, 전기자동차로의 전환 가속화, 맞춤형 마감에 대한 수요 증가는 시장 확대의 주요 요인입니다. 로봇 코팅은 일관된 코팅 두께, 우수한 마감 품질, 최소한의 재료 손실을 실현하는 동시에 사이클 타임의 단축과 효율 향상을 보장합니다. 이러한 시스템은 배출가스 감소와 에너지 효율 향상을 통해 제조업체의 지속가능성 목표 달성을 지원합니다. 또한 환경 규제 강화, 운영 비용 절감 압력, 디지털화·녹색 제조에 대한 지속적인 동향이 자동 도장 공장에 대한 투자를 더욱 촉진하고 있습니다. 로봇 페인팅 기술은 재현성이 높은 결과를 제공하고 수작업과 관련된 편차를 제거하기 위해 자동차 제조업체는 생산 단계 전체에서 높은 생산성과 정확성을 달성하기 위해 고급 페인트 로봇을 우선적으로 도입하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 가치

25억 2,000만 달러

예측 금액

40억 7,000만 달러

CAGR

5%

관절식 로봇 부문은 2024년에 69%의 점유율을 차지했고 2025년부터 2034년에 걸쳐 CAGR 5.26%를 나타낼 것으로 예측됩니다. 이 이점은 다용도, 도달 범위의 넓이, 복잡한 차량 모양을 쉽게 처리할 수 있는 능력에 기인합니다. 복수의 관절과 보통 6축 이상을 갖춘 이 로봇은 인간의 팔과 같은 매끄럽고 정밀한 동작을 실현하여 정밀도와 적응성이 요구되는 자동차 도장 공정에 최적입니다. 복잡한 도장 각도와 윤곽을 관리하는 능력은 대규모 생산 라인에서 효율성을 유지하면서 전체 마감 품질을 향상시킵니다.

바닥 설치형 로봇 부문은 2024년에 55%의 점유율을 차지했으며, 2034년까지 연평균 복합 성장률(CAGR) 5.63%를 나타낼 것으로 전망되고 있습니다. 바닥 설치형은 안정성, 통합의 용이성, 기존 생산 레이아웃과의 호환성으로 인해 제조 시설에서 가장 널리 채택된 구성입니다. 이 로봇은 받침대와 공장 바닥에 직접 고정되어 로봇 암과 페인트 장비에 견고한 기반을 제공합니다. 이로 인해 고속 도장 사이클 중에도 정밀한 제어와 안정된 동작이 가능합니다. 견고한 구조와 적응성은 대규모 자동차 조립 라인의 필수 요소입니다.

아시아태평양의 자동차 도장 로봇 시스템 시장은 2024년에 50%의 점유율을 차지하며 12억 5,000만 달러 규모에 이르렀습니다. 이 지역의 견고한 지위는 급속한 산업화, 대규모 자동차 제조 및 자동화 기술에 대한 투자 증가로 지원됩니다. 중국, 일본, 한국, 인도 등 국가들은 스마트 제조, 로보틱스, 인더스트리 4.0의 도입을 촉진하는 전략적 이니셔티브를 통해 이 성장을 주도하고 있습니다. 정부 지원 프로그램과 첨단 기술 혁신을 통해 지역은 첨단 제조 및 자동화 개발의 주요 기지로 자리를 잡고 있습니다.

세계의 자동차 도장 로봇 시스템 시장에서 주요 기업으로는 KUKA, FANUC, ABB, Durr, Comau, Kawasaki Heavy Industries, Staubli Robotics, Yaskawa Electric, Omron 등을 들 수 있습니다. 자동차 도장 로봇 시스템 시장의 주요 기업은 혁신, 협업, 기술 능력 확대를 통해 경쟁력을 강화하고 있습니다. 보다 높은 정밀도, 에너지 효율, 디지털 통합을 갖춘 지능형 로봇 도장 솔루션의 도입을 위한 연구 개발에 주력하고 있습니다. 자동차 제조업체와의 제휴를 통해 특정 생산 요구 사항을 충족하도록 설계된 맞춤형 자동화 시스템이 가능합니다. 또한 신흥 시장 수요 증가에 대응하기 위해 각사는 제조능력과 서비스 네트워크의 확대에도 노력하고 있습니다.

목차

제1장 조사 방법

시장 범위와 정의

조사 설계

조사 접근

데이터 수집 방법

데이터 마이닝의 출처

세계

지역별/국가별

기본 추정치와 계산

기준연도 계산

시장 추정에서의 주요 동향

1차 조사 및 검증

1차 정보

예측

조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률 분석

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

파괴적 혁신

업계에 미치는 영향요인

성장 촉진요인

자동차 커스터마이징에 대한 수요 증가

대량 생산 차량의 생산 요건

인건비 삭감의 압력

환경규제

로보틱스 분야에서의 기술적 진보

제조업체에 의한 지속가능성 이니셔티브

업계의 잠재적 위험 및 과제

초기 투자비용 높이

복잡한 유지보수 요건

시장 기회

신흥 시장에서의 사업 확대

전기자동차 생산 확대

협동 로봇 개발

AI와 IoT의 통합

성장 가능성 분석

특허 분석

Porter's Five Forces 분석

PESTEL 분석

코스트 내역 분석

기술 동향

현재의 기술 동향

신흥기술

규제 상황

가격 동향

지역별

로봇에 의한

생산 통계

생산 거점

소비 거점

수출과 수입

지속가능성과 환경면

지속가능한 실천

폐기물 감축 전략

생산에 있어서 에너지 효율

환경에 배려한 대처

탄소발자국에 관한 고려 사항

투자 및 공급망 분석

투자 및 자금 조달 동향의 분석

공급망 동향과 원재료의 영향

업무 효율화, 지속가능성 및 노동력 관리

품질 기준과 성능 벤치마킹

환경 영향과 지속가능성에 대한 노력

노동력에 미치는 영향과 기술 요건 분석

연수·인재육성 프로그램의 평가

벤더 및 리스크 관리

벤더 평가 기준과 선정 프레임워크

리스크 평가 및 경감 전략

자동화가 고사양 계약 획득에 미치는 영향

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

인수 및 합병

파트너십 및 협업

신제품 발매

확대계획과 자금조달

제5장 시장 추계·예측 : 로봇별(2021-2034년)

주요 동향

관절식 로봇

직교 로봇

스칼라 로봇

협동 로봇

제6장 시장 추계·예측 : 설치 방법별(2021-2034년)

주요 동향

바닥 장착형 로봇

벽면 장착형 로봇

레일 장착형 로봇

제7장 시장 추계·예측 : 페이로드별(2021-2034년)

주요 동향

5kg 이하

5-10kg

10-20kg

20kg 이상

제8장 시장 추계·예측 : 자동화 수준별(2021-2034년)

주요 동향

완전 자동화

반자동화

제9장 시장 추계·예측 : 최종 용도별(2021-2034년)

주요 동향

OEM 도장 공장

Tier 1 공급업체 시설

애프터마켓 및 충돌 수리 센터

특수 차량 제조

제10장 시장 추계·예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

북유럽 국가

러시아

아시아태평양

중국

인도

일본

호주

인도네시아

필리핀

태국

한국

싱가포르

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

제11장 기업 프로파일

세계의 기업

ABB

Comau

Denso

Durr

Epson Robots

FANUC

Kawasaki Heavy Industries

KUKA

Mitsubishi Electric

Nachi-Fujikoshi

Omron

Panasonic

Staubli Robotics

Yaskawa Electric

지역 기업

11.2.1. 3M 그룹

Doosan Robotics

Elite Robots

Hyundai Robotics

Reis Robotics

Universal Robots

신흥기업/혁신기업

Franka Emika

Precise Automation

Rethink Robotics

Standard Bots

Techman Robot

KTH

영문 목차

영문목차

The Global Automotive Paint Robot System Market was valued at USD 2.52 billion in 2024 and is estimated to grow at a CAGR of 5% to reach USD 4.07 billion by 2034.

The growing adoption of automation across automotive production facilities is driving this market, as manufacturers seek enhanced precision, uniformity, and sustainability in vehicle painting operations. Automotive paint robot systems, designed to automate body handling, coating, and finishing, have become essential to modern vehicle manufacturing lines. Rising global vehicle output, the accelerating transition toward electric vehicles, and increasing demand for customized finishes are major factors contributing to market expansion. Robotic painting offers consistent coating thickness, superior finish quality, and minimal material waste while ensuring faster cycle times and higher efficiency. These systems also support manufacturers' sustainability goals by reducing emissions and improving energy efficiency. Moreover, stricter environmental regulations, pressure to reduce operational costs, and the ongoing trend toward digital and green manufacturing are further fueling investments in automated paint shops. With robotic painting technology delivering repeatable results and eliminating inconsistencies associated with manual operations, automakers are prioritizing advanced paint robotics to achieve higher productivity and precision in every production stage.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$2.52 billion

Forecast Value

$4.07 billion

CAGR

5%

The articulated robots segment held 69% share in 2024 and is projected to grow at a CAGR of 5.26% from 2025 to 2034. This dominance is attributed to their versatility, extended reach, and ability to handle complex vehicle geometries with ease. These robots, equipped with multiple joints and typically six or more axes, provide smooth and precise motion like that of a human arm, making them ideal for automotive paint applications that demand accuracy and adaptability. Their capability to manage intricate painting angles and contours enhances the overall finish quality while maintaining efficiency on large-scale production lines.

The floor-mounted robots segment held a 55% share in 2024 and is expected to grow at a CAGR of 5.63% through 2034. Floor-mounted configurations remain the most adopted setup in manufacturing facilities due to their stability, ease of integration, and compatibility with existing production layouts. These robots are fixed directly onto pedestals or plant floors, providing a solid base for the robotic arm and paint applicator, which allows for precise control and steady operation during high-speed painting cycles. Their robust structure and adaptability make them an essential part of large automotive assembly lines.

Asia Pacific Automotive Paint Robot System Market held a 50% share and generated USD 1.25 billion in 2024. The region's strong position is supported by rapid industrialization, large-scale automotive manufacturing, and rising investment in automation technologies. Countries including China, Japan, South Korea, and India are leading this growth through strategic initiatives that promote smart manufacturing, robotics, and Industry 4.0 adoption. These government-backed programs and high levels of technological innovation have positioned the region as a major hub for advanced manufacturing and automation development.

Key players operating in the Global Automotive Paint Robot System Market include KUKA, FANUC, ABB, Durr, Comau, Kawasaki Heavy Industries, Staubli Robotics, Yaskawa Electric, and Omron. Leading companies in the Automotive Paint Robot System Market are strengthening their competitive position through innovation, collaboration, and expansion of technological capabilities. They are focusing on research and development to introduce intelligent robotic painting solutions with higher accuracy, energy efficiency, and digital integration. Partnerships with automotive manufacturers are enabling tailored automation systems designed to meet specific production requirements. Companies are also expanding their manufacturing capacity and service networks to cater to rising demand in emerging markets.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Regional

2.2.2 Robot

2.2.3 Mounting

2.2.4 Pay load

2.2.5 Automation level

2.2.6 End use

2.3 TAM analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future-outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factors affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising demand for automotive customization

3.2.1.2 High-volume vehicle production requirements

3.2.1.3 Labor cost reduction pressures

3.2.1.4 Environmental regulations

3.2.1.5 Technological advancements in robotics

3.2.1.6 Sustainability initiatives by manufacturers

3.2.2 Industry pitfalls and challenges

3.2.2.1 High initial investment costs

3.2.2.2 Complex maintenance requirements

3.2.3 Market opportunities

3.2.3.1 Expansion in emerging markets

3.2.3.2 Electric vehicle production growth

3.2.3.3 Collaborative robotics development

3.2.3.4 Integration of AI and IoT

3.3 Growth potential analysis

3.4 Patent analysis

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Cost breakdown analysis

3.8 Technology landscape

3.8.1 Current technological trends

3.8.2 Emerging technologies

3.9 Regulatory landscape

3.9.1 North America

3.9.2 Europe

3.9.3 Asia Pacific

3.9.4 Latin America

3.9.5 Middle East and Africa

3.10 Price trends

3.10.1 By region

3.10.2 By robot

3.11 Production statistics

3.11.1 Production hubs

3.11.2 Consumption hubs

3.11.3 Export and import

3.12 Sustainability and environmental aspects

3.12.1 Sustainable practices

3.12.2 Waste reduction strategies

3.12.3 Energy efficiency in production

3.12.4 Eco-friendly initiatives

3.13 Carbon footprint considerations

3.14 Investment and supply chain analysis

3.14.1 Investment and funding trends analysis

3.14.2 Supply chain dynamics and raw material impact

3.15 Operational excellence, sustainability, and workforce management

3.15.1 Quality standards and performance benchmarking

3.15.2 Environmental impact and sustainability initiatives

3.15.3 Workforce impact and skills requirements analysis

3.15.4 Training and development programs assessment

3.16 Vendor and risk management

3.16.1 Vendor evaluation criteria and selection framework

3.16.2 Risk assessment and mitigation strategies

3.17 Impact of Automation on Securing High-Specification Contracts