자동차용 로보틱스 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)

Automotive Robotics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1666688

리서치사:Global Market Insights Inc.

발행일:2024년 12월

페이지 정보:영문 203 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

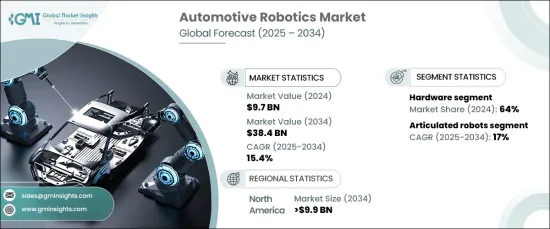

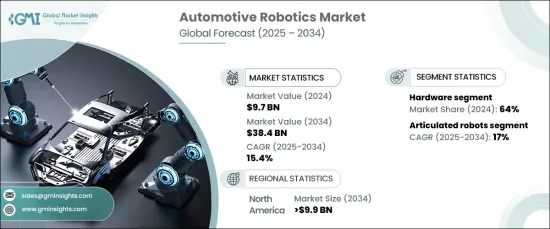

세계 자동차용 로보틱스 시장은 2024년 97억 달러로 평가되었고, 2025년부터 2034년까지 연평균 15.4%의 성장률을 나타낼 것으로 예상됩니다.

이러한 급격한 성장의 배경에는 자동차 제조의 합리화, 효율성 및 생산 품질 향상을 위한 자동화에 대한 의존도가 높아지고 있습니다. 로봇 공학의 산업 통합은 일관성을 보장하고, 오류를 줄이고, 생산성을 향상시키며, 조립, 용접, 자재 취급과 같은 주요 작업에서 자동화가 필수적인 요소로 자리 잡았습니다.

자동차용 로보틱스 수요를 촉진하는 주요 요인 중 하나는 제조의 정확성과 효율성을 향상시킬 필요가 있다는 것입니다. 최신 차량 설계, 특히 전기자동차 및 하이브리드 자동차의 설계에는 더 높은 정밀도가 요구됩니다. 용접, 도장, 조립 등의 작업을 수작업을 능가하는 정밀도로 수행하기 위해서는 로봇이 필수적입니다. 반복 작업의 자동화를 통해 생산 시간을 단축하고 처리 능력을 향상시키며 품질 기준을 유지합니다. 또한, 인더스트리 4.0 기술로 실현되는 IoT 및 스마트 제조와 로봇공학의 통합은 생산 워크플로우를 최적화하고 운영 비용을 절감합니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

97억 달러

예상 금액

384억 달러

CAGR

15.4%

자동차용 로보틱스 시장은 하드웨어, 소프트웨어, 서비스의 세 가지 주요 부문으로 나뉩니다. 이 중 하드웨어 분야가 가장 큰 비중을 차지하며 2024년 시장의 약 64%를 차지했습니다. 이 부문에는 로봇 팔, 센서, 액추에이터, 컨트롤러 등의 부품이 포함되며, 로봇 시스템의 정확성, 속도, 내구성을 높이는 데 매우 중요합니다. 보다 정교하고 가볍고 정밀한 하드웨어에 대한 수요가 증가함에 따라 자동차 생산의 복잡한 요구 사항을 충족시키기 위해 제조업체들은 첨단 기술에 지속적으로 투자하고 있습니다.

로봇의 유형에 있어서는 다관절 로봇이 다재다능함과 높은 정밀도로 인해 시장을 독점하고 있습니다. 특히 용접, 도장, 자재 취급 등의 작업에서 그 위력을 발휘합니다. 다축 동작과 실시간 조정 등 다관절 로봇의 고급 기능은 자동차 제조에 보급에 기여하고 있습니다. 다관절 로봇의 유연성은 대량 생산과 맞춤형 제조 요구에 모두 대응할 수 있어 자동차 부문의 자동화 전략에 없어서는 안 될 필수 요소로 자리 잡았습니다.

북미의 경우, 미국의 자동차용 로보틱스 시장은 2034년까지 99억 달러에 달할 것으로 예상됩니다. 이 분야의 성장은 첨단 제조 기술, 스마트 팩토리 도입, 전기자동차(EV)의 부상, AI와 협동로봇(cobot)의 통합을 포함한 유연한 자동화 시스템에 대한 관심이 향후 시장 형성에 중요한 역할을 할 것으로 예상됩니다.

목차

제1장 조사 방법과 조사 범위

시장 범위와 정의

기본 추정과 계산

예측 계산

데이터 소스

1차 데이터

2차 데이터

유료 정보원

공적 정보원

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

밸류체인에 영향을 미치는 요인

이익률 분석

파괴

향후 전망

제조업체

유통업체

공급업체 상황

이익률 분석

주요 뉴스

규제 상황

영향요인

성장 촉진요인

업계의 잠재적 리스크&과제

성장 가능성 분석

Porter의 Five Forces 분석

PESTEL 분석

제4장 경쟁 구도

서론

기업 점유율 분석

경쟁 포지셔닝 매트릭스

전략 전망 매트릭스

제5장 시장 추산·예측 : 컴포넌트별, 2021년-2034년

주요 동향

하드웨어

컨트롤러

로봇암

엔드 이펙터

센서

시각 센서

포스/토크 센서

기타

기타

소프트웨어

서비스

제6장 시장 추산·예측 : 로봇 유형별, 2021년-2034년

주요 동향

다관절 로봇

4-axis robots

6-axis robots

기타

스카라 로봇

직교 로봇

원통형 로봇

기타

제7장 시장 추산·예측 : 용도별, 2021년-2034년

주요 동향

자재관리

용접

스팟 용접

아크 용접

조립 및 분해

검사

절단 및 가공

물류 및 창고 자동화

기타

제8장 시장 추산·예측 : 페이로드 용량별, 2021년-2034년

주요 동향

16 kg까지

16-60킬로

60-225킬로

225kg 이상

제9장 시장 추산·예측 : 전개 유형별, 2021년-2034년

주요 동향

고정형 로봇

이동 로봇

무인운반차(AGV)

자율 이동 로봇(AMR)

제10장 시장 추산·예측 : 기술별, 2021년-2034년

주요 동향

머신러닝 및 인공지능(AI)

3D 비전 시스템

IoT 통합

클라우드 로보틱스

제11장 시장 추산·예측 : 지역별, 2021년-2034년

주요 동향

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

러시아

아시아태평양

중국

인도

일본

한국

호주

기타 아시아태평양

라틴아메리카

브라질

멕시코

기타 라틴아메리카

중동 및 아프리카

남아프리카공화국

사우디아라비아

아랍에미리트(UAE)

기타 중동 및 아프리카

제12장 기업 개요

ABB

Comau SpA

Denso Wave

Dürr AG

Fanuc Corporation

Harmonic Drive System

Kawasaki Heavy Industries

KUKA Robotics

Nachi-Fujikoshi Corp

Omron Corporation

Panasonic Welding Systems Co. Ltd.

Reis Gmbh &Co.

Rockwell Automation

Seiko Epson Corporation

Stäubli

Universal Robots

Yamaha Robotics

Yaskawa Electric Corporation

LSH

영문 목차

영문목차

The Global Automotive Robotics Market, valued at USD 9.7 billion in 2024, is expected to expand at a CAGR of 15.4% from 2025 to 2034. This surge is driven by the increasing reliance on automation to streamline automotive manufacturing, improve efficiency, and enhance production quality. The integration of robotics into the industry ensures greater consistency, reduces errors, and boosts productivity, with automation becoming essential in key operations such as assembly, welding, and material handling.

One of the primary factors fueling the demand for automotive robotics is the need for improved manufacturing precision and efficiency. Modern vehicle designs, especially those involving electric or hybrid models, demand a higher level of accuracy. Robots are critical in performing tasks like welding, painting, and assembly, all with a level of precision that surpasses manual labor. The automation of repetitive tasks reduces production times, increases throughput, and maintains high-quality standards. Additionally, the integration of robotics with IoT and smart manufacturing, enabled by Industry 4.0 technologies, optimizes production workflows and lowers operational costs.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$9.7 Billion

Forecast Value

$38.4 Billion

CAGR

15.4%

The automotive robotics market is divided into three key segments: hardware, software, and services. Among these, the hardware segment holds the largest share, accounting for approximately 64% of the market in 2024. This segment includes components like robotic arms, sensors, actuators, and controllers, which are crucial for enhancing the accuracy, speed, and durability of robotic systems. As the demand for more advanced, lightweight, and precise hardware increases, manufacturers continue to invest in cutting-edge technology to meet the complex demands of automotive production.

When it comes to robot types, articulated robots dominate the market due to their versatility and precision. They are particularly effective in performing tasks such as welding, painting, and material handling. The advanced capabilities of articulated robots, including multi-axis movement and real-time adjustments, contribute to their widespread use in automotive manufacturing. Their flexibility allows them to cater to both mass production and customized manufacturing needs, making them an essential part of the automotive sector's automation strategy.

In North America, the U.S. automotive robotics market is expected to exceed USD 9.9 billion by 2034. The country's growth in this sector is driven by advanced manufacturing technologies, the adoption of smart factories, and the rise of electric vehicles (EVs). The focus on flexible automation systems, including the integration of AI and collaborative robots (cobots), is expected to play a key role in shaping the market's future.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope & definitions

1.2 Base estimates & calculations

1.3 Forecast calculations

1.4 Data sources

1.4.1 Primary

1.4.2 Secondary

1.4.2.1 Paid sources

1.4.2.2 Public sources

Chapter 2 Executive Summary

2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Factor affecting the value chain

3.1.2 Profit margin analysis

3.1.3 Disruptions

3.1.4 Future outlook

3.1.5 Manufacturers

3.1.6 Distributors

3.2 Supplier landscape

3.3 Profit margin analysis

3.4 Key news & initiatives

3.5 Regulatory landscape

3.6 Impact forces

3.7 Growth drivers

3.7.1 Increased demand for automation

3.7.2 Surge in demand for electric and autonomous vehicles

3.7.3 Focus on safety and worker well-being

3.7.4 Rise of collaborative robots (cobots)

3.7.5 Ongoing technological advancements in robotics

3.8 Industry pitfalls & challenges

3.8.1 High Initial Investment

3.8.2 Skilled labor shortages for robotics operation