자동차 레이저 용접 시스템 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2025-2034년)

Automotive Laser Welding System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1876533

리서치사:Global Market Insights Inc.

발행일:2025년 11월

페이지 정보:영문 210 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

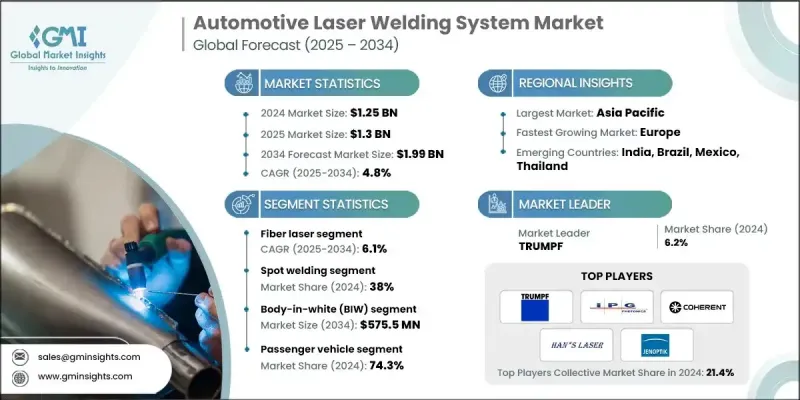

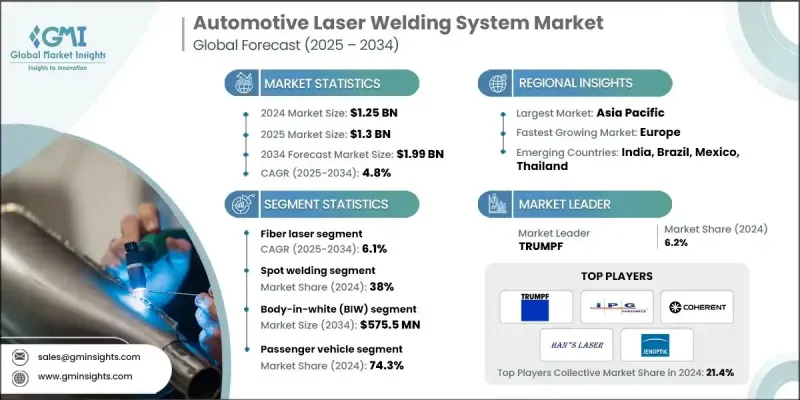

세계의 자동차 레이저 용접 시스템 시장은 2024년에 12억 5,000만 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 4.8%를 나타내 19억 9,000만 달러에 이를 것으로 예측됩니다.

자동차 부문의 꾸준한 확대는 차량 생산 증가와 신흥 경제국 수요 증가에 견인되어 첨단 제조 솔루션을 위한 강력한 기회를 창출하고 있습니다. 자동차 제조업체 각사는 진화하는 생산 기준을 충족하면서 보다 높은 정밀도, 생산성, 일관된 품질을 실현하기 위해 레이저 용접 기술에 적극적인 투자를 추진하고 있습니다. 알루미늄과 하이브리드 합금을 사용한 고성능의 경량 차량으로의 전환이 진행되는 동안 레이저 기반 용접 시스템에 대한 수요는 더욱 높아지고 있습니다. 레이저 용접은 탁월한 정밀도, 최소한의 열 변형, 우수한 강도 유지성을 제공하며 구조적 무결성을 손상시키지 않으면 서 얇은 재료와 이종 재료의 접합에 이상적입니다. 빔 제어, 적응형 센서 및 자동 모니터링 기술의 지속적인 혁신은 신뢰성을 높이고 제조상의 결함을 줄입니다. 이러한 발전은 생산 효율을 향상시킬 뿐만 아니라 대량 생산 환경 전체에서 균일한 품질과 재현성을 보장하며 현대 자동차 제조 공정에서 레이저 용접의 중요성을 더욱 강력하게 하고 있습니다. 시장의 진화는 자동차 생산의 자동화, 디지털화, 지속가능성에 대한 관심 증가에 의해 형성되고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 가치

12억 5,000만 달러

예측 금액

19억 9,000만 달러

CAGR

4.8%

파이버 레이저 부문은 2025년과 2034년 사이에 6.1%의 연평균 복합 성장률(CAGR)을 나타낼 것으로 예측됩니다. 뛰어난 빔 정확도, 에너지 효율, 경량 재료 및 이종 재료의 용접 능력으로 인해 파이버 레이저는 자동차 업계에서 매우 높은 평가를 받았습니다. 높은 용접 속도와 낮은 운영 비용을 포함한 성능 이점은 전기자동차 제조 및 고급 바디 구조의 채택을 촉진합니다. 자동차 제조업체가 정확성, 내구성 및 비용 효율성을 강조하는 동안 파이버 레이저 시스템은 차세대 생산 설비의 필수 구성 요소가 되고 있습니다.

스폿 용접 부문은 2024년에 38%의 점유율을 차지했습니다. 레이저 스폿 용접은 신속하고 견고하고 정확한 용접을 실현하는 차체 조립에서 중요한 공정으로 계속되고 있습니다. 스폿 용접에서 로봇 자동화와 고출력 파이버 레이저의 통합은 생산성 향상, 재료 폐기 최소화, 일관된 용접 품질 보장을 제공합니다. 이 기술적 진보는 경량 설계, 생산 사이클의 가속화, 제조 공정의 가동 중지 시간 절감에 주력하는 자동차 산업의 동향과 일치합니다.

미국의 자동차 레이저 용접 시스템 시장은 2024년 85.4%의 점유율을 차지했습니다. 이 국가는 최고 수준의 정확성과 신뢰성이 요구되는 용도를 위해 첨단 레이저 용접 기술의 채택에서 계속 주도적인 입장에 있습니다. 전기자동차의 상업화 확대, 견조한 연구개발 투자, 산업계와 연구기관의 강력한 연계가 미국 시장에서 레이저 용접 기술의 혁신을 지원하고 있습니다. 제조업체 각사는 고품질 생산과 자동화를 중시하고 있으며, 이에 따라 전국 자동차 공장의 기술 통합이 더욱 추진되고 있습니다.

세계의 자동차 레이저 용접 시스템 시장의 주요 기업으로는 TRUMPF, IPG Photonics, Coherent, Jenoptik, Han's Laser Technology, FANUC, Amada Weld Tech, Laserline, Golden Laser, Baison Laser 등이 있습니다. 자동차 레이저 용접 시스템 시장의 주요 기업은 기술 혁신, 생산 능력 확대, 전략적 제휴를 통해 시장에서의 지위를 강화하고 있습니다. 진화하는 제조 요구에 대응하기 위해 첨단 레이저 광원, 실시간 감시 솔루션, 에너지 절약 시스템 개발을 위한 연구 개발에 많은 투자를 하고 있습니다. 자동차 제조업체나 산업용 자동화 기기 프로바이더와의 제휴에 의해 전기자동차나 경량 소재용으로 최적화된 커스텀 용접 플랫폼의 창출이 가능해지고 있습니다. 또한 증가하는 세계적인 수요에 대응하기 위해 지리적 존재와 생산시설의 확대도 진행하고 있습니다.

목차

제1장 조사 방법

시장 범위와 정의

조사 설계

조사 접근

데이터 수집 방법

데이터 마이닝의 출처

세계

지역별/국가별

기본 추정치와 계산

기준연도 계산

시장 추정에서의 주요 동향

1차 조사 및 검증

1차 정보

예측

조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

원재료 공급자

부품 제조업체

시스템 통합자

OEM

최종 용도

업계에 미치는 영향요인

성장 촉진요인

자동차 생산 능력 확대

고정밀하고 경량인 재료에 대한 수요

에너지 절약형 제조 공정으로의 이행

레이저 빔 제어 및 감시 시스템의 진보

전기자동차 및 하이브리드 자동차의 보급 확대

업계의 잠재적 위험 및 과제

초기 투자비용 높이

숙련 레이저 용접 오퍼레이터의 부족

시장 기회

전기자동차 및 하이브리드 자동차 부문의 성장

배터리 모듈 및 파워트레인 용접 용도의 확대

인더스트리 4.0 및 스마트 제조 도입 확대

다재료 용접 솔루션의 기술적 진보

성장 가능성 분석

규제 상황

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신 동향

현행 기술

신흥기술

특허 분석

가격 동향 분석

구성 요소별

지역별

코스트 내역 분석

생산 통계

생산 거점

소비 거점

수출과 수입

지속가능성과 환경면

지속가능한 대처

폐기물 감축 전략

생산에 있어서 에너지 효율

환경에 배려한 대처

탄소발자국에 관한 고려 사항

향후의 동향

자동차 분야에서의 기술 로드맵과 혁신의 궤적

신흥 용도과 시장 확대의 기회

자율주행차에 미치는 영향과 부품요건

지속가능한 제조와 녹색기술의 통합

디지털 전환과 스마트 제조의 통합

자동차 고객의 요건과 업계 우선순위

자동차 품질에 대한 고정밀도 및 재현성의 요구

로봇 공학 및 자동화 통합 요건

EV 배터리용접 사양 및 기준

AWS D8.10 M : 2021 및 AIAG CQI-15 규격 준수

자동차 분야의 에너지 효율과 총 소유 비용

현지 서비스 네트워크와 기술 지원에 대한 기대

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 뉴스와 대처

인수 및 합병

파트너십 및 협력

신제품 발매

사업 확장 계획과 자금 조달

제5장 시장 추계·예측 : 레이저별(2021-2034년)

주요 동향

파이버 레이저

CO2 레이저

고체 레이저

다이오드 레이저

제6장 시장 추계·예측 : 용접별(2021-2034년)

주요 동향

스폿 용접

이음매 용접

하이브리드 용접

원격 용접

제7장 시장 추계·예측 : 용도별(2021-2034년)

주요 동향

차체 본체(BIW)

파워트레인 부품

배터리 제조(전기자동차용)

배기 시스템

섀시 및 구조 부품

제8장 시장 추계·예측 : 차량별(2021-2034년)

주요 동향

승용차

SUV

해치백

세단

상용차

LCV

MCV

대형 상용차(HCV)

제9장 시장 추계·예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

북유럽 국가

네덜란드

러시아

아시아태평양

중국

인도

일본

ANZ

싱가포르

태국

베트남

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제10장 기업 프로파일

세계의 기업

Bystronic Laser

Coherent

FANUC

Han's Laser Technology

IPG Photonics

Jenoptik

TRUMPF

지역 기업

Amada Weld Tech

HGTECH

Laser Photonics

Laserax

Precitec

Prima Power

Sino-Galvo Technology

Emerson Electric(Branson Ultrasonics)

신흥기업 및 혁신기업

ALPHA LASER

Baison Laser

Control Laser

Golden Laser

KEYENCE

Laserline

LaserStar Technologies

Miyachi Unitek

Perfect Laser

Sahajanand Laser Technology

KTH

영문 목차

영문목차

The Global Automotive Laser Welding System Market was valued at USD 1.25 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 1.99 billion by 2034.

The steady expansion of the automotive sector, driven by rising vehicle production and growing demand in developing economies, is creating strong opportunities for advanced manufacturing solutions. Automakers are actively investing in laser welding technologies to achieve higher precision, productivity, and consistent quality while meeting evolving production standards. The increasing shift toward high-performance, lightweight vehicles made from aluminum and hybrid alloys is further amplifying the demand for laser-based welding systems. Laser welding offers exceptional accuracy, minimal thermal distortion, and superior strength retention, making it ideal for joining thin or dissimilar materials without compromising structural integrity. Continued innovation in beam control, adaptive sensors, and automated monitoring technologies enhances reliability and reduces manufacturing defects. These advancements not only improve production efficiency but also ensure uniform quality and repeatability across mass-production environments, reinforcing the importance of laser welding in modern automotive manufacturing processes. The market's evolution is being shaped by a growing focus on automation, digitalization, and sustainability in vehicle production.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$1.25 Billion

Forecast Value

$1.99 Billion

CAGR

4.8%

The fiber laser segment is anticipated to register a CAGR of 6.1% between 2025 and 2034. Its superior beam precision, energy efficiency, and ability to weld lightweight and mixed materials make fiber lasers highly favored in the automotive industry. Their performance benefits, including high welding speed and lower operating costs, are driving adoption in electric vehicle manufacturing and advanced body structures. As automakers emphasize precision, durability, and cost-effectiveness, fiber laser systems are becoming essential components of next-generation production facilities.

The spot welding segment accounted for a 38% share in 2024. Laser spot welding remains a critical process in vehicle body assembly, offering rapid, strong, and accurate welds. The integration of robotic automation and high-powered fiber lasers in spot welding enhances productivity, minimizes material waste, and ensures consistent weld quality. This technological progress aligns with the automotive industry's increasing focus on lightweight design, faster production cycles, and reduced downtime in manufacturing operations.

U.S. Automotive Laser Welding System Market held a share of 85.4% in 2024. The country continues to lead in adopting advanced laser welding technologies for applications demanding maximum precision and reliability. The growing commercialization of electric vehicles, robust R&D investments, and strong collaboration between industry and research institutions are sustaining innovation in laser welding within the U.S. market. Manufacturers are emphasizing high-quality production and automation, further driving technological integration in automotive plants nationwide.

Key companies operating in the Global Automotive Laser Welding System Market include TRUMPF, IPG Photonics, Coherent, Jenoptik, Han's Laser Technology, FANUC, Amada Weld Tech, Laserline, Golden Laser, and Baison Laser. Leading companies in the Automotive Laser Welding System Market are strengthening their market position through technological innovation, capacity expansion, and strategic partnerships. They are investing extensively in R&D to develop advanced laser sources, real-time monitoring solutions, and energy-efficient systems that meet evolving manufacturing needs. Collaborations with automotive OEMs and industrial automation providers are enabling the creation of customized welding platforms optimized for electric vehicles and lightweight materials. Companies are also expanding their geographic presence and production facilities to meet increasing global demand.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Laser

2.2.2 Welding

2.2.3 Application

2.2.4 Vehicle

2.2.5 Region

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.1.1 Raw material suppliers

3.1.1.2 Component manufacturers

3.1.1.3 System integrators

3.1.1.4 OEM

3.1.1.5 End use

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Expansion of automotive production capacity

3.2.1.2 Demand for high precision and lightweight materials