Plant-Based Protein Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1871090

리서치사:Global Market Insights Inc.

발행일:2025년 10월

페이지 정보:영문 230 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

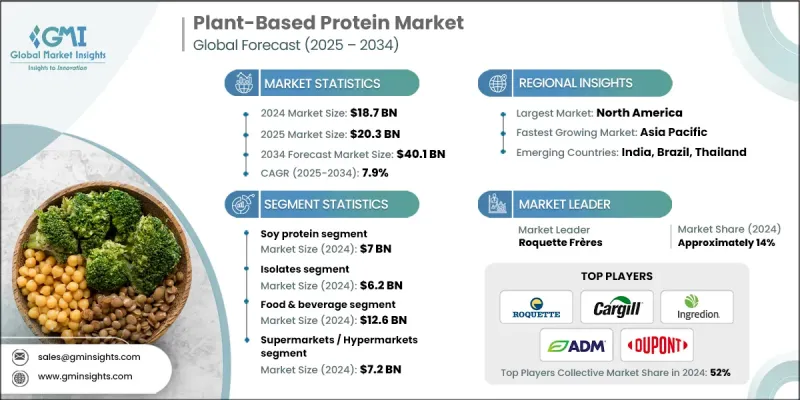

세계의 식물성 단백질 시장은 2024년에 187억 달러로 평가되었고 2034년까지 연평균 복합 성장률(CAGR)은 7.9%를 나타낼 것으로 예측되며 401억 달러에 달할 전망입니다.

지난 몇 년간 식물성 단백질은 건강, 지속가능성, 면역력 강화에 대한 소비자 관심 증가에 힘입어 틈새 시장에서 글로벌 주류 시장으로 전환되었습니다. 코로나19 팬데믹은 소비자들이 유통기한이 길고 영양가 높으며 육류가 포함되지 않은 단백질 옵션을 찾으면서 수요를 더욱 가속화했습니다. 특히 북미와 유럽은 적색육 및 가공육의 환경적 및 건강적 영향에 대한 인식이 높아지면서 특히 강한 성장을 보이고 있습니다. 플렉시테리언 식단의 인기 상승과 지속 가능한 식물성 식품에 대한 관심 증대는 브랜드들이 제품 포트폴리오를 다각화하도록 장려했습니다. 쉐이크, 단백질 풍부 식품, 유제품 대체품 등 육류 대체품이 널리 수용되면서 시장의 급속한 확장과 장기 성장 궤도가 강화되고 있습니다.

시장 범위

시작 연도

2024년

예측 기간

2025-2034년

시작 금액

187억 달러

예측 금액

401억 달러

CAGR

7.9%

콩 단백질 부문은 2024년 70억 달러를 기록했으며, 2025-2034년 연평균 7.2%의 성장률을 보일 것으로 예상됩니다. 콩, 완두콩, 밀 단백질은 높은 단백질 함량과 확립된 가공 네트워크로 인해 여전히 주요 원료로 자리 잡고 있습니다. 콩은 육류 대체품 및 유제품 프리 제품 생산에서 계속 선두를 유지하는 반면, 완두 단백질은 알레르기 유발 물질이 없고 비유전자변형(non-GMO)이라는 점으로 주목받고 있습니다. 밀 단백질은 제빵 제품 및 즉석 식품에 필수적인 질감 형태로 인해 여전히 인기가 높습니다.

분리 단백질 부문은 2024년 62억 달러 규모를 기록했으며, 높은 순도와 생체 이용률을 제공하여 스포츠 영양제, 건강 보조 식품, 단백질 음료 시장을 주도하며 2034년까지 연평균 8% 성장할 것으로 전망됩니다. 농축 단백질은 균형 잡힌 영양소와 비용 효율성으로 주류 식품 시장에서 입지를 유지하고 있습니다. 텍스처드 단백질은 식물성 고기와 즉석식에서 고기 유사 제품에 기대되는 씹는 맛과 질감을 구현함으로써 혁신을 주도합니다.

미국의 식물성 단백질 시장은 2024년에 45억 달러로 평가되었고, 2025-2034년 연평균 복합 성장률(CAGR)은 7.3%를 보일 것으로 예측됩니다. 단백질 강화 기능성 식품, 클린 라벨 보충제, 식물성 대체품의 광범위한 유통망 확장이 성장을 주도하고 있습니다. 성숙한 공급망과 강력한 브랜딩은 슈퍼마켓과 온라인 건강 플랫폼을 통한 신속한 시장 진출을 가능케 합니다. 기능성 식품에서 완두콩, 콩, 쌀 단백질에 대한 수요 증가로 식품 기술 기업들의 대규모 투자가 촉진되고 있습니다. FDA 기준을 준수하는 라벨 표기를 갖춘 고단백 포장 식품은 건강 혜택을 강조하는 마케팅 전략과 규제 체계의 혜택을 받고 있습니다.

식물성 단백질 시장의 주요 기업으로는 로켓 플레일사, ADM(아처 다니엘스 미첼사), 카길사, 잉글레디온사, 듀폰 뉴트리션사 등이 있습니다. 식물성 단백질 시장 기업들은 혁신, 전략적 파트너십, 글로벌 확장을 통해 시장 입지를 강화하고 있습니다. 연구 개발 투자는 단백질 기능성, 풍미, 영양 프로필 개선에 집중되어 주류 소비자에게 어필하고 있습니다. 식품 제조업체, 유통 체인, 온라인 플랫폼과의 파트너십은 더 넓은 유통망과 빠른 시장 진출을 보장합니다. 기업들은 소비자 가치와 규제 준수에 부합하기 위해 지속가능성과 클린 라벨 인증을 강조합니다. 육류 대체품, 기능성 음료, 유제품 대체품으로의 제품 다각화는 다양한 소비자 부문를 포착하는 데 도움이 됩니다. 건강상 이점, 알레르기 유발 물질이 없는 특성, 친환경 생산 방식을 강조하는 마케팅 캠페인은 브랜드 신뢰도를 구축하는 데 활용됩니다.

목차

제1장 조사 방법

시장 범위와 정의

조사 설계

조사 접근

데이터 수집 방법

데이터 마이닝 소스

세계

지역별/국가별

기본 추정치와 계산

기준연도 계산

시장 추정에서의 주요 동향

1차 조사 및 검증

1차 정보

예측 모델

조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

업계의 잠재적 억제요인 및 과제

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

가격 동향

지역별

장래 시장 동향

기술과 혁신의 상황

현재의 기술 동향

신흥기술

특허 상황

무역 통계(주 : 무역 통계는 주요 국가에서만 제공됨)

주요 수입국

주요 수출국

지속가능성과 환경적 측면

지속가능한 실천

폐기물 감축 전략

생산에서의 에너지 효율

환경에 배려한 대처

탄소발자국에 관한 고려 사항

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병 및 인수

제휴 및 협력관계

신제품 발매

사업 확대 계획

제5장 시장 추계 및 예측 : 유형별(2025-2034년)

주요 동향

콩 단백질

완두콩 단백질

밀 단백질

쌀 단백질

감자 단백질

카놀라 단백질

기타

제6장 시장 추계 및 예측 : 형태별(2025-2034년)

주요 동향

분리 단백질

농축물

텍스처드 단백질

가수분해물

제7장 시장 추계 및 예측 : 용도별(2025-2034년)

주요 동향

식품 및 음료

육류 대체품 및 유사품

유제품 대체품

베이커리 및 과자류

스포츠 및 영양 보조 식품

기능성 음료

동물사료(반려동물 식품, 가축 사료)

화장품 및 퍼스널케어

의약품

제8장 시장 추계 및 예측 : 유통 채널별(2025-2034년)

주요 동향

온라인 소매

슈퍼마켓 및 대형 슈퍼마켓

전문점

기업간 거래(B2B 공급)

제9장 시장 추계 및 예측 : 지역별(2025-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제10장 기업 프로파일

Roquette Freres

Cargill

Ingredion Inc.

ADM(Archer Daniels)

DuPont Nutrition

Kerry Group

Burcon NutraScience

Tate &Lyle

Glanbia Nutritionals

Puris

CHS Inc.

Farbest Brands

Beneo GmbH

Emsland Group

NOW Health Group

HBR

영문 목차

영문목차

The Global Plant-Based Protein Market was valued at USD 18.7 Billion in 2024 and is estimated to grow at a CAGR of 7.9% to reach USD 40.1 Billion by 2034.

Over the past several years, plant-based protein has transitioned from a niche segment to a mainstream global market, driven by growing consumer focus on health, sustainability, and immune support. The COVID-19 pandemic further accelerated demand as consumers sought shelf-stable, nutritious, and meat-free protein options. North America and Europe are witnessing particularly strong growth due to rising awareness around the environmental and health impacts of red and processed meat. The increasing popularity of flexitarian diets and growing interest in sustainable, plant-based foods have encouraged brands to diversify their offerings. Meat-free alternatives, including shakes, protein-rich foods, and dairy substitutes, have become widely accepted, reinforcing the market's rapid expansion and long-term growth trajectory.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$18.7 Billion

Forecast Value

$40.1 Billion

CAGR

7.9%

The soy protein segment generated USD 7 Billion in 2024 and is expected to grow at a CAGR of 7.2% between 2025 and 2034. Soy, pea, and wheat proteins remain the dominant sources due to high protein content and established processing networks. Soy continues to lead in the production of meat alternatives and dairy-free products, while pea protein is gaining traction for being allergen-free and non-GMO. Wheat protein remains popular for its textured forms, which are essential for bakery products and ready meals.

The isolates segment reached USD 6.2 Billion in 2024 and is forecasted to grow at 8% CAGR through 2034, as isolates provide high purity and bioavailability, dominating sports nutrition, dietary supplements, and protein beverages. Concentrates remain cost-effective with balanced nutrition, sustaining their presence in mainstream food products. Textured proteins drive innovation in plant-based meats and ready-to-eat meals by delivering the chew and texture expected in meat analogues.

U.S. Plant-Based Protein Market was valued at USD 4.5 Billion in 2024 and is projected to grow at a CAGR of 7.3% from 2025 to 2034. Growth is driven by protein-enriched functional foods, clean-label supplements, and broad retail distribution of plant-based alternatives. A mature supply chain and strong branding enable rapid market penetration through supermarkets and online health platforms. Increasing demand for pea, soy, and rice proteins in functional foods has spurred significant investments by food technology companies. High-protein packaged foods with FDA-compliant label claims benefit from marketing strategies and regulatory frameworks that emphasize health benefits.

Major players operating in the Plant-Based Protein Market include Roquette Freres, ADM (Archer Daniels), Cargill, Ingredion Inc., and DuPont Nutrition. Companies in the Plant-Based Protein Market are leveraging innovation, strategic partnerships, and global expansion to strengthen their market position. Investment in research and development focuses on improving protein functionality, flavor, and nutritional profiles to appeal to mainstream consumers. Partnerships with food manufacturers, retail chains, and online platforms ensure wider distribution and faster market penetration. Companies emphasize sustainability and clean-label certifications to align with consumer values and regulatory compliance. Product diversification into meat alternatives, functional beverages, and dairy substitutes helps capture multiple consumer segments. Marketing campaigns highlighting health benefits, allergen-free attributes, and eco-friendly production practices are used to build brand credibility.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Type

2.2.3 Form

2.2.4 Application

2.2.5 Distribution Channel

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier Landscape

3.1.2 Profit Margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.2 Industry pitfalls and challenges

3.2.3 Market opportunities

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Price trends

3.7.1 By region

3.8 Future market trends

3.9 Technology and Innovation landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent Landscape

3.11 Trade statistics (Note: the trade statistics will be provided for key countries only)

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and Environmental Aspects

3.12.1 Sustainable Practices

3.12.2 Waste Reduction Strategies

3.12.3 Energy Efficiency in Production

3.12.4 Eco-friendly Initiatives

3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New Product Launches

4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2025 - 2034 (USD Million, Kilo Tons)

5.1 Key trends

5.2 Soy Protein

5.3 Pea Protein

5.4 Wheat Protein

5.5 Rice Protein

5.6 Potato Protein

5.7 Canola Protein

5.8 Others

Chapter 6 Market Estimates and Forecast, By Form, 2025 - 2034 (USD Million, Kilo Tons)

6.1 Key trends

6.2 Isolates

6.3 Concentrates

6.4 Textured Proteins

6.5 Hydrolysates

Chapter 7 Market Estimates and Forecast, By Application, 2025 - 2034 (USD Million, Kilo Tons)

7.1 Key trends

7.2 Food & Beverage

7.2.1 Meat Substitutes & Analogues

7.2.2 Dairy Alternatives

7.2.3 Bakery & Confectionery

7.2.4 Sports & Nutritional Supplements

7.2.5 Functional Beverages

7.3 Animal Feed (Pet Food, Livestock Feed)

7.4 Cosmetics & Personal Care

7.5 Pharmaceuticals

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2025 - 2034 (USD Million, Kilo Tons)

8.1 Key trends

8.2 Online Retail

8.3 Supermarkets/Hypermarkets

8.4 Specialty Stores

8.5 Business-to-Business (B2B Supply)

Chapter 9 Market Estimates and Forecast, By Region, 2025 - 2034 (USD Million, Kilo Tons)