오프 하이웨이 장비용 변속기 컴포넌트 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Off-Highway Equipment Transmission Component Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1858818

리서치사:Global Market Insights Inc.

발행일:2025년 10월

페이지 정보:영문 210 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

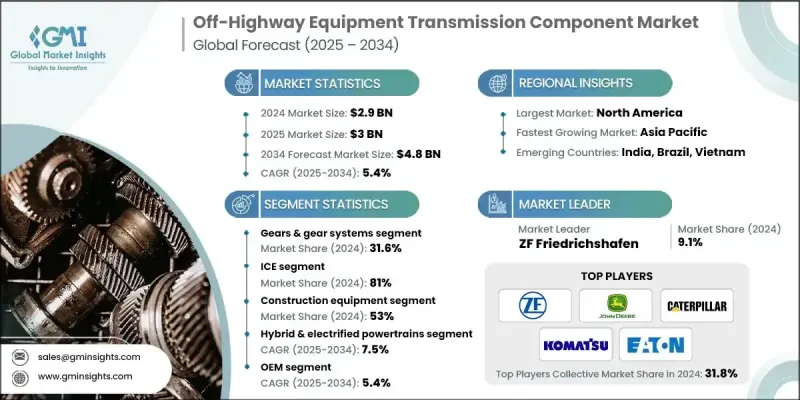

세계의 오프 하이웨이 장비용 변속기 컴포넌트 시장 규모는 2024년에 29억 달러로 평가되었고, CAGR 5.4%로 성장할 전망이며, 2034년에는 48억 달러에 이를 것으로 예측됩니다.

시장 성장의 원동력은 도로, 교량, 시장 개척 등 인프라 프로젝트에 대한 투자 증가입니다. 이러한 프로젝트에는 고부하를 장시간 처리할 수 있는 내구성 있는 변속기 시스템을 갖춘 건설 기계가 필요합니다. 또한 특히 아시아와 아프리카에서는 급속한 도시화가 진행되고 있기 때문에 오프 하이웨이 장비에 대한 수요도 높아지고 있습니다. 게다가, 특히 개발도상국의 농업 부문에서는 기계화가 진행되고 있으며, 트랙터, 수확기, 살포기에서는 선진적인 변속 시스템이 보편화되고 있습니다. 하이드로 스태틱 변속기 및 전기 유압 변속기와 같은 이러한 시스템은 효율성, 정확성 및 작동 편의성으로 인기를 얻고 있습니다. 마찬가지로 광업은 광물과 화석 연료에 대한 수요가 높아져 성장을 계속하고 있으며, 대형 기계에서 견고한 변속 장치에 대한 의존도가 높아지고 있습니다. 광산 기계의 전동화는 증가하는 경향이 있지만, 디젤 엔진 구동 기계는 까다로운 환경에서 효율적으로 작동하기 때문에 여전히 내구성이 높은 변속기에 의존하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시장 규모

29억 달러

예측 금액

48억 달러

CAGR

5.4%

기어 및 기어 시스템 분야는 2024년에 31.6%의 점유율을 차지했으며, 2034년까지 연평균 복합 성장률(CAGR) 6.1%로 성장할 것으로 예측됩니다. 이 부문은 오프 하이웨이 장비에서 보다 효율적이고 신뢰성이 높고, 공간 효율적이며, 컴팩트하고 높은 토크 솔루션을 제공하는 유성 기어 세트의 채용 증가로 혜택을 누리고 있습니다. 합금이나 복합재료 등의 경량 재료의 사용도 증가하고 있어 강도를 유지하면서 전체의 중량을 줄이는 데 도움이 되고 있습니다. 또한, 소음 및 진동 억제 기술의 발전은 운전자의 편안함과 기계 부품의 수명을 모두 향상시키기 위해 기어 시스템에 통합되고 있습니다.

내연기관(ICE) 부문은 2024년에 81%의 점유율을 차지했으며, 2034년까지 CAGR 5.2%로 성장이 예상됩니다. 전동화의 동향은 높아지고 있는 반면, ICE는 그 신뢰성과 높은 파워로부터, 오프 하이웨이 용도에서는 여전히 선호되고 있습니다. 제조업체는 엄격한 환경 기준을 충족하기 위해 연료 효율을 높이고 배출 가스를 줄이는 데 주력하고 있습니다.

미국의 오프 하이웨이 장비용 변속기 컴포넌트 2024년 시장 점유율은 86.1%로 7억 2,890만 달러에 달했습니다. 이 나라의 급속한 도시화, 가처분 소득 증가, 고급차 수요 증가가 이 우위성의 요인이 되고 있습니다. 미국에서 하이드로 스태틱 변속기는 유연성, 효율성 및 부드러운 동력 전달을 통해 오프 하이웨이 기계에 널리 사용되고 있습니다. 이러한 시스템은 건설 기계 및 농업 기계와 같은 가변 속도 제어가 필요한 용도 분야에서 특히 유용합니다.

세계의 고속도로 장비용 변속기 부품 시장을 선도하는 주요 기업으로는 Allison Transmission, BorgWarner, Bosch Rexroth, Caterpillar, CNH Industrial, Eaton Corporation, John Deere, Komatsu, and ZF Friedrichshafen 등이 있습니다. 오프 하이웨이 장비용 변속기 컴포넌트 시장의 기업은 그 지위를 강화하기 위해, 기술을 혁신하고 제품 다양화에 주력하고 있습니다. 대부분은 오프 하이웨이 기계의 효율, 내구성 및 에너지 성능을 향상시키기 위해 정유압 솔루션 및 전동 유압 솔루션과 같은 고급 변속기 시스템 개발에 투자하고 있습니다. 또한 각 회사는 OEM과 전략적 파트너십을 맺고 자체 변속기 기술을 차세대 오프 하이웨이 장비에 직접 통합하려고 합니다. 게다가 이러한 기업들은 특히 북미와 아시아와 같은 인프라 요구가 증가하는 지역에서 제조 능력을 확대하고 있습니다.

목차

제1장 조사 방법

시장 범위 및 정의

조사 디자인

조사 접근

데이터 수집 방법

데이터 마이닝의 출처

지역 및 국가

기본 추정 및 계산

기준 연도의 산출

시장 추계의 주요 동향

1차 조사 및 검증

1차 정보

예측 모델

조사의 전제조건 및 한계

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률 분석

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

밸류체인 분석

업스트림 밸류체인

미드스트림 밸류 체인

다운스트림 밸류체인

업계에 미치는 영향요인

성장 촉진요인

건설 및 광산 기계 수요 증가

전동화 및 하이브리드 파워트레인으로의 시프트

변속기 시스템의 기술적 진보

신흥 시장에서의 성장

업계의 잠재적 위험 및 과제

전동화 시스템을 위한 고액 설비 투자

원재료 가격 변동

복잡한 유지보수 요건

신흥 시장의 인프라 한계

시장 기회

애프터마켓 서비스 확대

자율 주행 기기 및 스마트 기기의 채용

정부 보조금 및 인센티브

특수 기기의 새로운 용도

성장 가능성 분석

규제 상황

EPA 제4차 최종 기준의 실시

EU 스테이지 V 배출 가스 적합 요건

지역별 규제 틀의 차이

향후 배출 가스 규제의 전개

Porter's Five Forces 분석

PESTEL 분석

기술 및 혁신의 전망

차세대 변속기 기술

풀 장비의 전동화 타임라인

자율주행 기기의 통합

디지털 트윈 및 시뮬레이션 기술

지속 가능한 제조 동향

가격 동향

자동차

지역

특허 분석

생산 통계

생산 거점

소비 거점

수출 및 수입

비용 내역 분석

지속가능성 및 환경 측면

지속가능한 실천

폐기물 감축 전략

생산에서의 에너지 효율

환경 친화적인 노력

탄소발자국

OEM 및 애프터마켓의 경쟁 관계

오리지널 기기 통합 전략

애프터마켓 서비스 및 교환 모델

재제조 및 순환경제 동향

채널 분쟁 및 파트너십 관리

기기의 자동화 및 커넥티비티의 통합

자율주행 기기의 전송 요건

IoT 및 텔레매틱스의 통합

예지보전 및 진단

원격 감시 및 제어 시스템

제조 및 생산의 과제

지역별 제조 전략

생산 능력 및 확장성

품질 관리 및 시험 기준

린 생산 방식 및 공정 최적화

기기의 라이프 사이클 및 서비스에 관한 인사이트

컴포넌트의 내구성 및 신뢰성 요건

서비스 간격 최적화

현장 서비스 및 지원 전략

사용한 부품 관리

기기의 전동화 및 기술 이행

송전 기술의 채용

하이브리드 파워트레인 통합의 과제

배터리 기술 및 파워 매니지먼트

기존 시스템 및 전기 시스템의 비교

제4장 경쟁 구도

서문

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

합병 및 인수

파트너십 및 협업

신제품 발표

확장 계획 및 자금 조달

제5장 시장 추계 및 예측 : 컴포넌트별(2021-2034년)

주요 동향

기어 및 기어 시스템

클러치 및 브레이크

토크 컨버터

유압 부품

제어 시스템

송전 부품

제6장 시장 추계 및 예측 : 추진력별(2021-2034년)

주요 동향

ICE

전기

배터리 전기자동차(BEV)

하이브리드 자동차(HEV)

플러그인 하이브리드 자동차(PHEV)

하이브리드

제7장 시장 추계 및 예측 : 차량별(2021-2034년)

주요 동향

건설 기계

굴삭기 및 백호

불도저 및 스크레이퍼

휠 로더 및 스키드 스티어

모터 그레이더 및 콤팩터

농업 기계

트랙터 및 유틸리티 차량

콤바인 및 하베스터

분무기 및 어플리케이터

경운기 및 이식기

광산 기계

운반 트럭 및 덤프 트럭

드래그 라인 및 굴삭기

지하 설비

파쇄 및 가공기기

임업 기계

수확기 및 가공기

포워더 및 스키더

펠러 번처

로그 로더 및 델린버

자재 관리 기기

지게차 및 텔레핸들러

러프테레인 크레인

고소 작업차

컨테이너 핸들러

제8장 시장 추계 및 예측 : 기술별(2021-2034년)

주요 동향

메카니컬 트랜스미션 시스템

하이드로 스태틱 및 하이드로 메카니컬 시스템

하이브리드 및 전동 파워트레인

제어 및 액추에이션 기술

제9장 시장 추계 및 예측 : 판매 채널별(2021-2034년)

주요 동향

OEM

애프터마켓

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

러시아

북유럽 국가

폴란드

아시아태평양

중국

인도

일본

한국

뉴질랜드

베트남

싱가포르

인도네시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제11장 기업 프로파일

세계 리더

ZF Friedrichshafen

Allison Transmission

Eaton

Bosch Rexroth

Parker Hannifin

Caterpillar

John Deere

CNH Industrial

BorgWarner

지역 챔피언

Komatsu

Volvo

Liebherr

Doosan

Hitachi

SANY

XCMG

JCB

신흥 기업

Carraro

Twin Disc

Bondioli & Pavesi

Hydro-Gear

Poclain

Brevini

Rexnord

AJY

영문 목차

영문목차

The Global Off-Highway Equipment Transmission Component Market was valued at USD 2.9 billion in 2024 and is estimated to grow at a CAGR of 5.4% to reach USD 4.8 billion by 2034.

The market growth is driven by increasing investments in infrastructure projects, including roads, bridges, and housing developments. These projects require construction equipment equipped with durable transmission systems capable of handling heavy loads for extended periods. The demand for off-highway machinery is also rising due to rapid urbanization, particularly in Asia and Africa. Moreover, the agriculture sector, especially in developing countries, is embracing mechanization, with advanced transmission systems becoming more common in tractors, harvesters, and sprayers. These systems, such as hydrostatic and electro-hydraulic transmissions, are gaining popularity because of their efficiency, precision, and ease of operation. Similarly, the mining industry continues to grow as demand for minerals and fossil fuels remains high, leading to greater reliance on robust transmission systems in heavy-duty machinery. Although the electrification of mining equipment is a growing trend, diesel-powered machinery still relies on durable transmissions to function efficiently in challenging environments.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$2.9 Billion

Forecast Value

$4.8 Billion

CAGR

5.4%

The gears & gear systems segment accounted for a 31.6% share in 2024 and is expected to grow at a CAGR of 6.1% through 2034. This segment is benefiting from the increasing adoption of planetary gear sets, which provide compact, high-torque solutions that are more efficient, reliable, and space-efficient in off-highway machinery. The use of lightweight materials such as alloys and composites is also growing, helping to reduce overall weight while maintaining strength. Additionally, advancements in noise and vibration suppression technologies are being integrated into gear systems to improve both operator comfort and the longevity of machine parts.

The internal combustion engine (ICE) segment held an 81% share in 2024 and is expected to grow at a CAGR of 5.2% through 2034. Despite the growing trend toward electrification, ICEs are still preferred in off-highway applications due to their reliability and power. Manufacturers are focusing on improving fuel efficiency and reducing emissions to meet stringent environmental standards.

U.S. Off-Highway Equipment Transmission Component Market held 86.1% in 2024, with USD 728.9 million. The country's rapid urbanization, growing disposable incomes, and increasing demand for premium vehicles are all contributing factors to this dominance. In the U.S., hydrostatic transmissions are becoming more widely used in off-highway machinery due to their flexibility, efficiency, and smooth power delivery. These systems are particularly beneficial in applications that require variable speed control, such as construction and agricultural machinery.

Key companies leading the Global Off-Highway Equipment Transmission Component Market include Allison Transmission, BorgWarner, Bosch Rexroth, Caterpillar, CNH Industrial, Eaton Corporation, John Deere, Komatsu, and ZF Friedrichshafen. To strengthen their position, companies in the Off-Highway Equipment Transmission Component Market are focusing on technological innovation and product diversification. Many are investing in the development of advanced transmission systems, such as hydrostatic and electro-hydraulic solutions, to improve the efficiency, durability, and energy performance of off-highway machinery. Companies are also forming strategic partnerships with OEMs to integrate their transmission technologies directly into new-generation off-highway equipment. Furthermore, these players are expanding their manufacturing capabilities, particularly in regions with growing infrastructure needs, like North America and Asia.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Regional

2.2.2 Component

2.2.3 Propulsion

2.2.4 Vehicle

2.2.5 Technology

2.2.6 Sales channel

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Value chain analysis

3.2.1 Upstream value chain

3.2.2 Midstream value chain

3.2.3 Downstream value chain

3.3 Industry impact forces

3.3.1 Growth drivers

3.3.1.1 Increasing Demand for Construction and Mining Equipment

3.3.1.2 Shift Towards Electrification and Hybrid Powertrains

3.3.1.3 Technological Advancements in Transmission Systems

3.3.1.4 Growth in Emerging Markets

3.3.2 Industry pitfalls and challenges

3.3.2.1 High Capital Investment for Electrified Systems

3.3.2.2 Volatility in Raw Material Prices

3.3.2.3 Complex Maintenance Requirements

3.3.2.4 Infrastructure Limitations in Emerging Markets

3.3.3 Market opportunities

3.3.3.1 Expansion of Aftermarket Services

3.3.3.2 Adoption of Autonomous and Smart Equipment

3.3.3.3 Government Subsidies and Incentives

3.3.3.4 Emerging Applications in Specialty Equipment

3.4 Growth potential analysis

3.5 Regulatory landscape

3.5.1 EPA Tier 4 Final Standards Implementation

3.5.2 EU Stage V Emissions Compliance Requirements