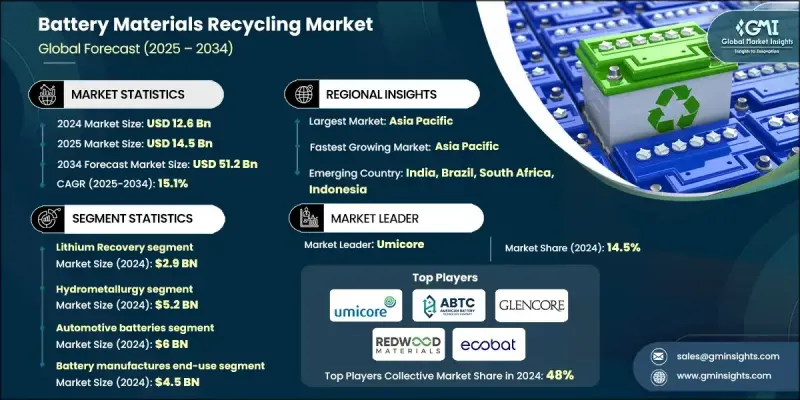

세계의 배터리 재료 재활용 시장 규모는 2024년에 126억 달러로 평가되었고, CAGR15.1%로 성장해 2034년에는 512억 달러에 이를 것으로 추정됩니다.

전기자동차 및 신재생에너지 분야가 확대됨에 따라 리튬, 코발트, 망간, 니켈 등 주요 배터리용 금속에 대한 수요가 급증하고 있습니다. 이러한 재료의 재활용은 전통적인 채굴에 대한 지속 가능한 대안으로 각광받고 있으며, 불안정한 원자재 가격, 지정학적 불확실성, 환경 악화에 대한 해결책을 제공합니다. 이 시장은 자원 순환을 장려하고 배터리 사용 후 제품 관리를 개선하기 위해 주요 지역에서 빠르게 진행되고 있는 규제 개혁에 의해 더욱 촉진되고 있습니다. 이러한 변화는 장기적인 성장 전망을 촉진하고 재활용 생태계에 대한 민간 및 공공 부문의 활발한 투자를 가능하게 하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 126억 달러 |

| 예측 금액 | 512억 달러 |

| CAGR | 15.1% |

지속 가능한 공급망에 대한 전 세계적인 관심이 높아지면서 에너지 저장 및 전기 이동성 분야에서 순환 경제에 대한 필요성이 커지고 있습니다. 재활용은 환경 친화적인 접근 방식일 뿐만 아니라 버진 소재 채취에 대한 의존도를 줄이기 위한 전략적 도구로 인식되고 있습니다. 산업을 재구성하는 중요한 트렌드 중 하나는 배터리 제조 공급망에 재활용 사업을 수직적으로 통합하는 것입니다. 이러한 통합을 통해 제조업체는 생산 라이프사이클 전반에 걸쳐 비용 효율성과 규제 준수를 개선하는 동시에 고부가가치 회수 재료의 안정적인 조달을 보장하고 루프를 닫을 수 있게 되었습니다.

리튬 회수 분야는 2024년 29억 달러 규모였으며, 2025년부터 2034년까지 13.9%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 리튬은 전기차, 휴대용 전자기기, 그리드 규모의 전력 저장 시스템에 사용되는 리튬 이온 배터리에 대한 높은 수요로 인해 리튬이 계속 우위를 점하고 있습니다. 리튬의 직접 추출 및 습식 야금 공정과 같은 기술의 발전으로 리튬 회수가 더욱 효율적이 되어 배터리 재료 재활용 시장에서 우위를 점할 수 있게 되었습니다. 이러한 기술의 사용이 증가함에 따라 추출 수율이 향상되고, 상업적 규모의 재활용이 점점 더 실용화되어 가고 있습니다.

자동차 배터리 분야는 2024년 60억 달러 규모로 평가되었고, 2034년까지 연평균 14.5%의 성장률을 보일 것으로 예측됩니다. 이 분야 성장의 원동력은 전 세계적으로 전기차 보급이 가속화되면서 엄청난 양의 사용 후 리튬 이온 배터리가 생산되고 있기 때문입니다. 자동차 제조업체와 배터리 공급업체들은 재활용업체와 전략적 제휴를 맺고 리튬, 코발트, 니켈 등의 금속을 재생하여 새로운 배터리 생산에 재사용하는 폐쇄형 루프 시스템을 구축하고 있습니다. 이러한 시스템은 EV의 성장에 따른 환경 영향을 줄이고 보다 견고한 공급망을 확보하는 데 중요한 역할을 하고 있습니다.

중국 배터리 재료 재활용 2024년 시장 규모는 30억 달러로 평가되었고, 2034년까지 15.3%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 중국은 엄격한 배터리 재활용 규제를 시행하고 있으며, 첨단 회수 기술의 성장을 뒷받침할 수 있는 산업 규모를 갖추고 있습니다. 한편, 인도는 새로운 규제와 투자로 재활용 역량을 강화하며 유망한 시장으로 빠르게 부상하고 있습니다. 호주, 인도네시아, 태국 등의 국가들도 전기차 및 전자 분야 확대에 따라 배터리 재료 회수를 지원하는 인프라 구축에 박차를 가하고 있습니다.

세계 배터리 재료 재활용 시장의 혁신과 확장을 주도하는 주요 기업으로는 Stena Recycling, Redwood Materials, Ascend Elements, TES(SK Ecoplant의 일부), Umicore, LG Energy, RecycLiCo Battery Materials Inc.,Duesenfeld GmbH,Primobius GmbH(Neometals JV),Glencore plc,Ecobat,Neometals Ltd,Retriev Technologies,Elemental Strategic Metals(ESM), American Battery Technology Co. 등이 있습니다. 배터리 재료 재활용 시장에서의 입지를 굳히기 위해 각 업체들은 수직적 통합과 기술 혁신을 중심으로 한 전략을 추구하고 있습니다. 주요 기업들은 자동차 제조업체 및 배터리 제조업체와 제휴하여 사용한 배터리의 직접 조달을 촉진하는 폐쇄형 루프 생태계를 구축하고 있습니다. 또한, 재료의 회수율을 높이고 처리 비용을 절감하기 위해 첨단 습식 야금 기술과 직접 추출 기술에 대한 투자도 이루어지고 있습니다. 기업들은 지역 재활용 허브를 설치하거나 합작회사를 설립하여 회수 및 정제 작업을 현지화함으로써 전 세계에 진출하는 등 세계 입지를 확장하고 있습니다.

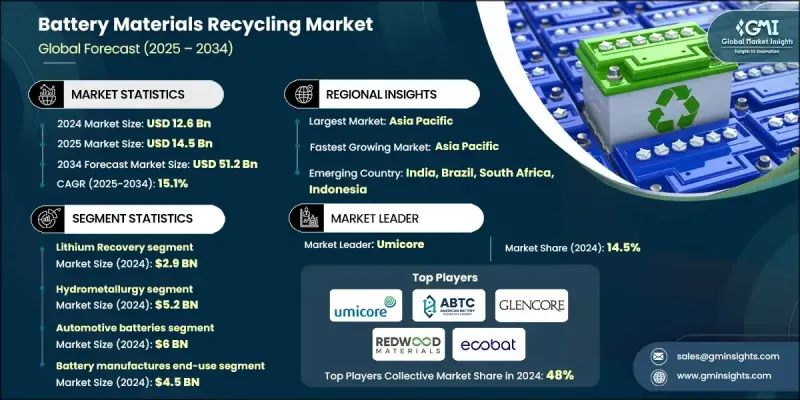

The Global Battery Materials Recycling Market was valued at USD 12.6 billion in 2024 and is estimated to grow at a CAGR of 15.1% to reach USD 51.2 billion by 2034.

Demand for key battery metals like lithium, cobalt, manganese, and nickel is surging as the electric vehicle and renewable energy sectors expand. Recycling these materials is gaining traction as a sustainable alternative to traditional mining, offering a solution to volatile raw material pricing, geopolitical uncertainty, and environmental degradation. The market is being further propelled by regulatory reforms, which are evolving rapidly across key regions to encourage resource circularity and improve battery end-of-life management. These changes are fostering long-term growth prospects and enabling robust private and public sector investments in recycling ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.6 Billion |

| Forecast Value | $51.2 Billion |

| CAGR | 15.1% |

Increasing global attention toward sustainable supply chains is reinforcing the need for circular economies in energy storage and electric mobility. Recycling is not only seen as an eco-conscious approach but also as a strategic tool for reducing dependency on virgin material extraction. One of the key trends reshaping the industry is the vertical integration of recycling operations into battery manufacturing supply chains. This integration is helping manufacturers close the loop, ensuring stable sourcing of high-value recovered materials while improving cost efficiency and regulatory compliance throughout production lifecycles.

The lithium recovery segment generated USD 2.9 billion in 2024 and is expected to grow at a CAGR of 13.9% from 2025 to 2034. Lithium continues to dominate due to its high demand in lithium-ion batteries used across EVs, portable electronics, and grid-scale storage systems. With advancements in techniques such as direct lithium extraction and hydrometallurgical processes, lithium recovery is becoming more efficient, further fueling its dominance within the battery materials recycling market. The rising use of these technologies enhances extraction yields, which is making recycling increasingly viable at a commercial scale.

The automotive battery segment generated USD 6 billion in 2024 and is projected to grow at a CAGR of 14.5% through 2034. The segment growth is fueled by the ongoing acceleration of global EV adoption, which is creating enormous volumes of spent lithium-ion batteries. Automakers and battery suppliers are forming strategic collaborations with recyclers to build closed-loop systems that reclaim metals such as lithium, cobalt, and nickel for reuse in new battery production. These systems are playing a key role in reducing the environmental impact of EV growth and ensuring more resilient supply chains.

China Battery Materials Recycling Market generated USD 3 billion in 2024 and is expected to grow at a CAGR of 15.3% through 2034. The country has implemented strict battery recycling regulations and possesses the industrial scale to support the growth of advanced recovery technologies. Meanwhile, India is quickly emerging as a promising market, with new regulations and investments strengthening its recycling capabilities. Countries like Australia, Indonesia, and Thailand are also accelerating infrastructure development to support battery material recovery as their EV and electronics sectors expand.

Leading companies driving innovation and expansion in Global Battery Materials Recycling Market include Stena Recycling, Redwood Materials, Ascend Elements, TES (part of SK Ecoplant), Umicore, LG Energy, RecycLiCo Battery Materials Inc., Duesenfeld GmbH, Primobius GmbH (Neometals JV), Glencore plc, Ecobat, Neometals Ltd, Retriev Technologies, Elemental Strategic Metals (ESM), and American Battery Technology Co. To strengthen their foothold in the battery materials recycling market, companies are pursuing strategies centered around vertical integration and technology innovation. Leading players are partnering with automakers and battery manufacturers to create closed-loop ecosystems that facilitate direct sourcing of spent batteries. Investments are also being made in advanced hydrometallurgical and direct extraction technologies to improve material recovery rates and reduce processing costs. Firms are expanding their global footprint by setting up regional recycling hubs and forming joint ventures to localize collection and refining operations.