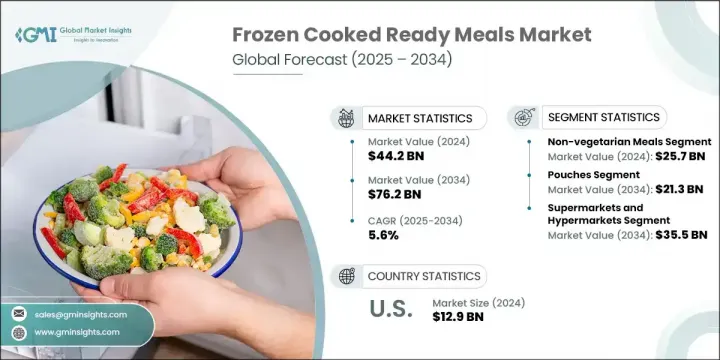

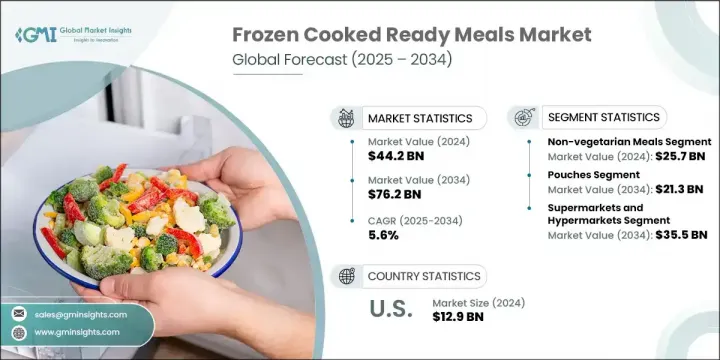

2024년 442억 달러로 평가되었고 CAGR 5.6%로 성장하여 2034년에는 762억 달러에 이를 것으로 추정됩니다.

편리하고 빠른 식사 솔루션에 대한 소비자의 선호도가 증가함에 따라 시장의 기세를 계속 견인하고 있습니다. 도시화, 공동 세대 증가, 일상생활의 페이스의 증대가, 진화하는 건강 기준에도 적합하는 퀵 조리식에 수요를 부추기고 있습니다. 고급 패키징 형식과 고급 저장 방법을 통해 브랜드는 신선한 맛과 영양을 보유한 냉동 식품을 제공할 수 있습니다. 동시에 전자상거래는 소비자의 쇼핑 방식을 바꾸어 이러한 식사를 보다 친숙하게 하고 있습니다.

식생활의 취향 변화, 제품 라인업 확대, 보다 건강하고 시간 절약으로 이어지는 식품 옵션에 대한 소비자의 지출 의욕이 높아지면서 세계 각지역에서 시장 규모는 2034년까지 거의 두배가 될 것으로 예측됩니다. 식물 기반의 식습관이 성장을 더욱 끌어주고 있으며, 지속 가능하고 고기를 사용하지 않는 선택을 요구하는 소비자가 늘고 있습니다. 각 브랜드는 고기 기반의 식사를 식물성 단백질 대체품으로 진화시켜 렌틸콩, 콩, 완두콩 등의 재료를 도입하여 윤리적이고 건강 지향적인 쇼핑객에게 어필하고 있습니다. 깨끗한 라벨, 빨리 먹을 수 있는 것, 버라이어티가 풍부한 세계의 요리에 대한 수요가 높아지고 있는 가운데, 냉동 조리 즉석식품 카테고리는 현대의 식사 계획과 식품 소비 패턴의 중심적 존재가 되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작금액 | 442억 달러 |

| 예측 금액 | 762억 달러 |

| CAGR | 5.6% |

비채식주의 냉동 식품 부문은 2024년에 257억 달러를 차지했고, 58.1%의 점유율을 차지했습니다. 이 부문은 단백질이 풍부하고 맛있는 식사 옵션에 대한 수요가 확산되기 때문에 여전히 지배적입니다. 채식 메뉴가 인기를 얻고 있는 것은 식물 유래의 식사와 건강에 대한 의식 증가가 주된 이유이지만, 비채식 음식은 확립된 소비자 기반과 다양성을 손상시키지 않고 편리성을 추구하는 식욕의 증가로부터 계속 이익을 얻고 있습니다. 소비자는 시간을 절약하면서 식사 요구를 충족시키는 식사에 매료되어 있으며, 이는 편의성이 우선하는 도시 환경에서 특히 그렇습니다. 건강 지향 증가는 각 브랜드가 더 깨끗하고 균형 잡힌 비 채식 음식을 제공하도록 촉구하고 성장을 더욱 향상시킵니다.

포장 혁신 부문은 2034년까지 213억 달러에 이르렀으며, 파우치는 사용 편의성, 운반성 및 저장 효율성을 제공합니다. 이 가벼운 옵션은 빠른 속도의 라이프 스타일을 지원하며 시장의 지속가능성으로의 전환과 일치합니다. 단열성, 재활용성 및 스마트 포장 기능을 향상시킨 새로운 파우치 형식은 제품을 보이는 방법과 보존 방법에 영향을 미칩니다.

미국 냉동 조리 즉석식품 시장은 80.1%의 점유율을 차지하며, 2024년에는 129억 달러를 창출했습니다. 이 지역은 성숙한 소매 인프라와 제품 다양성 혁신을 요구하는 소비자의 일관된 수요로 인해 강력한 성장을 보여줍니다. 공동 작업 가구 증가와 시간에 제약이 있는 소비자와 같은 라이프 스타일의 변화가 시장을 계속 확대하는 편리성의 문화를 만들어 냈습니다. 전통적인 식료품점과 대형 소매점은 여전히 필수적인 채널이지만, 온라인 식료품 택배 플랫폼은 냉동 식품의 인지도와 접근성을 크게 향상시키고 있습니다. 소비자의 식생활이 건강과 웰빙으로 이동하는 동안 미국의 각 브랜드는 주요 제품인 육류를 보완하는 식물성 식품의 선택을 꾸준히 늘리고 있습니다.

세계의 냉동 조리 즉석식품 시장을 형성하는 주요 기업으로는 Dr. Oetker, General Mills, Frosta, Kerry Group, Conagra Brands 등이 있습니다. 냉동 조리 즉석식품 시장에서 경쟁력을 확보하기 위해 선도적인 브랜드는 다양한 소비자 요구를 목표로 하는 지속적인 제품 혁신에 주력하고 있습니다. 각 회사는 건강 지향 및 유연한 지향 소비자에게 호소하기 위해 식물 유래 및 클린 라벨 포트폴리오를 확대하고 있습니다. R&D에 투자함으로써 인공적인 보존제를 사용하지 않고 미각 프로파일을 개선하고 유통 기한을 연장할 수 있습니다. 현지 공급업체와의 전략적 파트너십은 신속한 제품 출시와 원료 관리를 가능하게 합니다. 재활용 가능한 파우치와 전자레인지 대응 용기 등 패키징 솔루션의 강화도 우선 과제가 되고 있습니다. 각 브랜드는 온라인 식료품 플랫폼과 소비자 직접 판매 채널을 중시하는 옴니 채널 소매 전략을 통해 시장의 발자취를 더욱 강화하고 있습니다.

8.3.1 독일

The Global Frozen Cooked Ready Meals Market was valued at USD 44.2 billion in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 76.2 billion by 2034. Rising consumer preference for convenient and fast meal solutions continues to drive market momentum. Urbanization, increasing dual-income households, and the growing pace of everyday life are fueling the demand for quick-prep meals that also meet evolving health standards. Enhanced packaging formats and advanced preservation methods are enabling brands to deliver fresher-tasting, nutrient-retaining frozen meals. Simultaneously, e-commerce is reshaping how consumers shop, making these meals more accessible.

Across global regions, market volumes are expected to nearly double by 2034, supported by changing dietary preferences, expanded product offerings, and growing consumer willingness to spend more on healthier, time-saving food options. Plant-based eating habits are further propelling growth, with more consumers seeking sustainable, meat-free choices. Brands are evolving meat-based meals into plant protein alternatives, incorporating ingredients like lentils, soy, and peas to appeal to ethical and health-conscious shoppers. With demand rising for clean-label, ready-to-serve, and varied global cuisines, the frozen cooked ready meals category is becoming a central part of modern meal planning and food consumption patterns.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $44.2 Billion |

| Forecast Value | $76.2 Billion |

| CAGR | 5.6% |

The non-vegetarian frozen meals segment accounted for USD 25.7 billion in 2024, capturing 58.1% share. This segment remains dominant due to the widespread demand for protein-rich and flavorful meal options. While vegetarian options are gaining traction, largely because of increased awareness around plant-based diets and health, non-vegetarian meals continue to benefit from an established consumer base and growing appetite for convenience without compromising variety. Consumers are drawn to meals that meet dietary needs while saving time, and this is especially true in urban environments where convenience is a priority. The rise in health consciousness is pushing brands to offer cleaner, better-balanced non-veg meals, further boosting growth.

Packaging innovation segment will reach USD 21.3 billion by 2034, pouches offer ease of use, portability, and better storage efficiency. These lightweight options cater to fast-paced lifestyles and align with the market's shift toward sustainability. New pouch formats with improved insulation, recyclability, and smart-packaging features are influencing how products are presented and preserved.

U.S. Frozen Cooked Ready Meals Market held 80.1% share and generated USD 12.9 billion in 2024. The region shows strong growth thanks to mature retail infrastructure and consistent consumer demand for innovation in product variety. Lifestyle changes such as the growth of dual-income homes and time-constrained consumers have created a culture of convenience that continues to expand the market. Traditional grocery stores and large-format retailers remain essential channels, though online grocery delivery platforms have significantly boosted visibility and accessibility of frozen meals. As consumer diets shift toward health and wellness, brands in the U.S. are steadily adding plant-based options to complement their core meat-based lines.

The key players shaping the Global Frozen Cooked Ready Meals Market include Dr. Oetker, General Mills, Frosta, Kerry Group, and Conagra Brands. To secure a competitive position in the frozen cooked ready meals market, leading brands are focusing on continuous product innovation, targeting diverse consumer needs. Companies are expanding their plant-based and clean-label portfolios to appeal to health-conscious and flexitarian consumers. Investing in R&D helps improve taste profiles and extend shelf life without artificial preservatives. Strategic partnerships with local suppliers allow faster product launches and better control over ingredients. Enhanced packaging solutions, including recyclable pouches and microwave-safe containers, are also a priority. Brands are further strengthening their market footprint through omnichannel retail strategies, emphasizing online grocery platforms and direct-to-consumer channels.

8.3.1 Germany