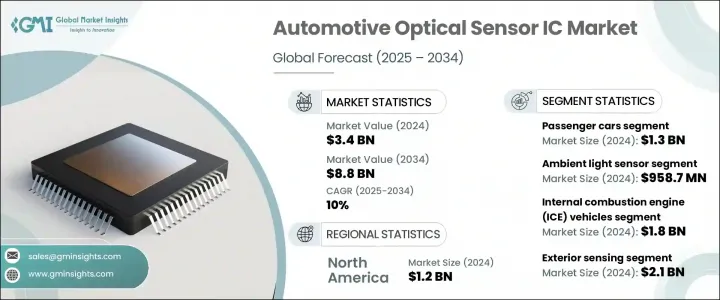

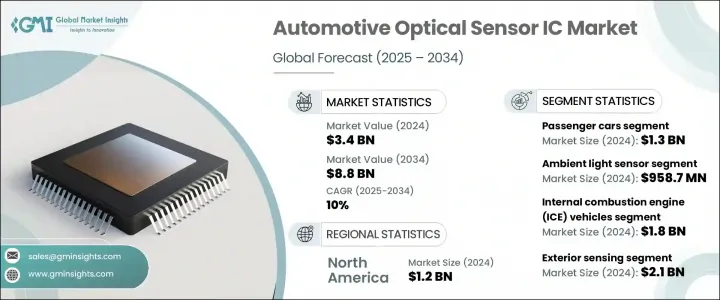

세계의 자동차용 광센서 IC 시장 규모는 2024년 34억 달러에 달했고, CAGR 10%로 성장하여 2034년까지 88억 달러에 이를 것으로 예측됩니다.

성장의 원동력은 급속한 기술 진보, ADAS(첨단 운전 지원 시스템) 수요 증가, 자율 주행 차량의 진화입니다. 수요는 주로, 안전성, 쾌적성, 성능 향상을 목적으로 한 자동차에 광학 센서의 채용 확대가 뒷받침하고 있습니다. 자동차 제조업체는 진화하는 규제의 안전 의무에 대응할 필요가 있습니다.

자동차 부문에서는 ADAS(첨단 운전 지원 시스템)를 강화하는 역할을 담당하는 광 센서 IC에 대한 주목이 높아지고 있습니다. 어댑티브 크루즈 컨트롤, 차선 유지, 사각 모니터링 등의 기능은 이러한 센서에 크게 의존합니다. 자동차 시스템의 복잡성과 보다 똑똑하고 안전하며 직관적인 운전 경험에 대한 소비자의 기대가 높아짐에 따라 고정밀하고 고성능 센서 기술에 대한 요구가 크게 증가하고 있습니다. 특히 광학 센서는 속도, 정밀도, 다양한 조명 및 환경 조건 하에서 효과적으로 기능하는 능력을 높이 평가합니다. 더 많은 OEM이 엄격한 안전 벤치마크를 충족하고 프리미엄 차량 경험을 제공하기 위해 광 센서 IC의 사용이 급속히 확대되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 34억 달러 |

| 예측 금액 | 88억 달러 |

| CAGR | 10% |

차종별로는 승용차 부문이 세계 시장을 선도했으며 2024년 시장 규모는 13억 달러였습니다. 이 부문은 안전성, 편안함, 실내 미관 향상 등 하이 엔드 기능에 대한 수요가 높아졌으며 자동차 제조업체가 광 센서 기반 시스템을 더 많이 통합 할 수 있습니다. 센서 IC는 자동화된 헤드라이트에서 차량 내 조명 조정에 이르기까지 광범위한 용도를 지원하기 위해 내장되어 있으며 스마트 모빌리티 솔루션에 대한 향상과 보조를 맞추고 있습니다. 전기자동차나 자율주행 승용차의 보급이 진행됨에 따라 광센서 IC에 대한 의존도가 크게 높아질 것으로 예측됩니다.

센서 유형별로 분류하면 환경광 센서가 최대 시장 점유율을 차지하고 2024년에는 9억 5,870만 달러에 달할 전망입니다. 이러한 센서는 차량의 내부 및 외부 조명을 실시간으로 조정하는 데 필수적이어서 시인성을 향상시키고 주의 산만을 줄이고 전반적인 운전의 편안함을 높입니다. 환경 변화에 적응하는 사용자 친화적인 조명 시스템에 대한 수요가 증가함에 따라 다양한 차종에서 환경 광 센서의 지속적인 채택을 촉진하고 있습니다.

용도별로 보면 자동차용 광센서 IC 시장은 인테리어 센싱과 외장 센싱으로 나눌 수 있습니다. 이 중 차외 센싱 분야는 2024년 시장 규모가 21억 달러로 압도적입니다. 외장 감지 기술은 주변 상황을 모니터링하고 주변 물체를 감지하고 도로 상황에 동적으로 대응하는 데 사용됩니다. 이러한 기능은 보행자 감지, 긴급 브레이크, 사각 인식 등의 시스템을 지원하는 데 매우 중요합니다. LiDAR, 적외선, 카메라 모듈과 같은 광학 센서는 이러한 기능의 핵심입니다. 특히 자동차 제조업체가 세계 안전 기준 및 신차 평가 프로그램(NCAP)을 준수하기 때문에 고성능 운전 지원 기능을 우선시하기 때문에 외부 용도를 위한 견고하고 내수성이 있는 고정밀 센서의 요구가 계속 증가하고 있습니다.

지역별로는 북미가 지배적인 시장으로 두드러지며 2024년에는 12억 달러를 차지했습니다. 이 지역은 자동차 안전을 지원하는 강력한 규제 프레임 워크와 자율 주행 차량 및 전기자동차 개발을 위한 첨단 생태계의 혜택을 받고 있습니다. 미국에서 시장은 2024년에 9억 1,040만 달러의 평가 금액에 도달하여 CAGR 10.5%로 성장했습니다. 국내 반도체 생산을 지원하는 정책 이니셔티브는 향후 몇 년 동안 자동차 센서 부품의 가용성과 비용 효율성에 큰 영향을 미치고 시장 확대를 더욱 강화할 것으로 예측됩니다.

자동차용 광센서 IC 시장에서 사업을 전개하는 주요 기업은 Panasonic Corporation, ON Semiconductor Corporation, Melexis NV, Autoliv Inc., Analog Devices, Inc., STMicroelectronics N.V., Omnivision Technologies, Inc., Broadcom Inc., NVIDIA Corporation, Infineon Technologies AG, Robert Bosch GmbH, Microchip Technology Inc., Continental AG, Aptiv PLC, ams-OSRAM AG, LeddarTech Inc., Texas Instruments Incorporated, NXP Semiconductors N.V., Hamamatsu Photonics K.K., Denso Corporation 등이 있습니다. 이 회사들은 센싱 기술 혁신, 칩 성능 향상, 자동차 제조업체와의 제휴에 주력하고 진화하는 상황에서 경쟁력을 유지하고 있습니다.

The Global Automotive Optical Sensor IC Market was valued at USD 3.4 billion in 2024 and is estimated to grow at a CAGR of 10% to reach USD 8.8 billion by 2034. The growth is driven by rapid technological advancement, increased demand for driver assistance systems, and the evolution of autonomous vehicles. The demand is primarily being fueled by the expanding adoption of optical sensors in automobiles for safety, comfort, and performance enhancements. Automakers are under increasing pressure to meet evolving regulatory safety mandates, which is contributing to the integration of sophisticated sensing components in modern vehicles.

The automotive sector is increasingly turning to optical sensor ICs due to their role in enhancing advanced driver assistance systems (ADAS). Features such as adaptive cruise control, lane keeping, and blind spot monitoring rely heavily on these sensors. The growing complexity of automotive systems and rising consumer expectations for smarter, safer, and more intuitive driving experiences have significantly increased the need for precise and high-performance sensor technologies. Optical sensors, in particular, are highly valued for their speed, accuracy, and ability to function effectively under diverse lighting and environmental conditions. As more OEMs aim to meet stringent safety benchmarks and offer premium vehicle experiences, the use of optical sensor ICs is rapidly expanding.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.4 Billion |

| Forecast Value | $8.8 Billion |

| CAGR | 10% |

In terms of vehicle type, the passenger cars segment led the global market and was valued at USD 1.3 billion in 2024. The increasing demand for high-end features in this segment, including enhanced safety, comfort, and interior aesthetics, is encouraging automakers to integrate more optical sensor-based systems. Sensor ICs are being embedded to support applications ranging from automated headlights to cabin light adjustments, aligning with the growing push towards smart mobility solutions. As electric and autonomous passenger cars continue to gain traction, the reliance on optical sensor ICs is anticipated to grow substantially.

When categorized by sensor type, ambient light sensors commanded the largest market share, reaching USD 958.7 million in 2024. These sensors are vital for adjusting both internal and external vehicle lighting in real-time, thereby improving visibility, reducing distractions, and enhancing overall driving comfort. The rising demand for user-friendly lighting systems that adapt to changing environments is fostering the continued adoption of ambient light sensors across various vehicle models.

By application, the automotive optical sensor IC market is divided into interior and exterior sensing. Among these, the exterior sensing segment dominated with a market value of USD 2.1 billion in 2024. Exterior sensing technologies are used to monitor surroundings, detect nearby objects, and respond dynamically to road conditions. These functions are crucial for supporting systems such as pedestrian detection, emergency braking, and blind spot recognition. Optical sensors, including LiDAR, infrared, and camera modules, are at the core of these capabilities. The need for robust, water-resistant, and accurate sensors for external applications continues to rise, especially as vehicle manufacturers prioritize high-performance driver assistance features to comply with global safety standards and New Car Assessment Programs (NCAP).

Regionally, North America stood out as the dominant market, accounting for USD 1.2 billion in 2024. The region benefits from a strong regulatory framework supporting vehicle safety and an advanced ecosystem for the development of autonomous and electric vehicles. In the United States, the market reached a valuation of USD 910.4 million in 2024, growing at a CAGR of 10.5%. Policy initiatives to support domestic semiconductor production are expected to significantly impact the availability and cost-efficiency of automotive sensor components in the coming years, further bolstering market expansion.

Key companies operating in the automotive optical sensor IC market include Panasonic Corporation, ON Semiconductor Corporation, Melexis NV, Autoliv Inc., Analog Devices, Inc., STMicroelectronics N.V., Omnivision Technologies, Inc., Broadcom Inc., NVIDIA Corporation, Infineon Technologies AG, Robert Bosch GmbH, Microchip Technology Inc., Continental AG, Aptiv PLC, ams-OSRAM AG, LeddarTech Inc., Texas Instruments Incorporated, NXP Semiconductors N.V., Hamamatsu Photonics K.K., and Denso Corporation. These players are focusing on innovations in sensing technology, improved chip performance, and partnerships with automotive OEMs to stay competitive in the evolving landscape.