High Fat (>85%) Butter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1766207

리서치사:Global Market Insights Inc.

발행일:2025년 06월

페이지 정보:영문 220 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

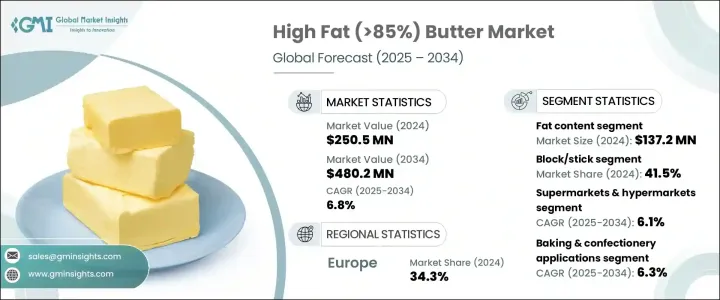

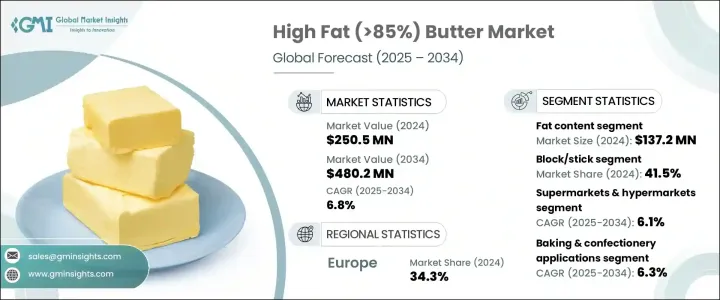

세계의 고지방(85% 이상) 버터 시장은 2024년에는 2억 5,050만 달러로 평가되었고, CAGR 6.8%를 나타내며 2034년에는 4억 8,020만 달러에 이를 것으로 추정됩니다.

이 꾸준한 성장의 원동력이 되고 있는 것은 보다 농후하고 자연스러운, 장인 기술이 빛나는 유제품에 대한 소비자의 기호의 높아입니다. 케토제닉·다이어트라고 하는 동향을 쫓는 건강 지향의 소비자의 사이에서 지지를 얻고 있습니다. 전통적인 교반(카쿠반) 방법으로 생산된, 클린 라벨, 유기 인증, 원산지 증명 첨부의 버터에 초점을 맞춘 프리미엄 부문도 출현하고 있습니다.

공급과 가격 변동에도 불구하고 호화스럽고 맛있는 유제품에 대한 수요는 여전히 강합니다. 또한 소매 전략의 진화, 신흥 시장에 대한 액세스 확대, 식품 전문점 및 전자상거래 플랫폼의 상승이 시장의 지속적인 성장을 지원합니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

2억 5,050만 달러

예측 금액

4억 8,020만 달러

CAGR

6.8%

제빵 및 제과 분야는 CAGR 6.3%를 나타내 보다 빠른 페이스로 성장할 것으로 예측됩니다. 고지방(85% 이상) 버터 시장 중에서는 고급 과자, 쿠키, 초콜릿에 있어서의 뛰어난 식감, 풍부한 풍미, 안정된 품질에 대한 수요 증가에 의해 제빵·과자류가 용도 동향을 지배하고 있습니다. 요리사가 소테나 소스, 풍미를 높이기 위해 고지방 버터를 선택하는 경향이 강해지고 있습니다. 사치스럽고 크림 같은 스프레드나 토핑을 요구하는 소비자가 이 수요를 한층 더 밀어 올리고 있는 한편, 케토식이나 고지방식 등의 영양 동향이 다이어트 용도에 있어서의 버터의 역할을 확대하고 있습니다.

2024년에는 블록과 스틱 부문이 41.5%의 점유율을 차지했고 CAGR 6.4%를 나타내 보다 폭넓은 소비자층을 끌어들일 것으로 예측됩니다. 도시의 건강 지향이 높은 소비자는 빵이나 크래커에 직접 칠할 수 있어 풍미를 손상시키지 않고 편리성을 겸비한, 이러한 소프트로 스프레드 가능한 포맷을 특히 높게 평가했습니다.

유럽의 고지방(85% 이상) 버터 시장은 2024년에 34.3%의 점유율을 차지했습니다. 이 이점은 전통적인 조리법과 미식 요리에서 버터가 중요한 역할을 하는 이 지역의 뿌리 깊은 요리 문화에 기인합니다. 유럽의 소비자들은 고품질의 유제품에 대한 이해가 발달하고 있으며, 진짜 지향, 풍부한 풍미, 장인적인 제조 방법을 우선하고 있습니다. 또한, 프리미엄 제품과 클린 라벨 제품에 관한 소비자 교육이 널리 침투하고 있는 것도 소매·외식 양 부문에 있어서의 고지방 버터의 안정된 수요를 뒷받침하고 있습니다. 유명한 유업 제조업체의 존재와 견고한 유통망은 이 시장에서 유럽의 주요 기업로서의 지위를 더욱 강화하고 소비자의 혀가 풍부한 기호를 충족시키는 특수 버터 제품의 지속적인 공급을 보장합니다.

고지방(85% 이상) 버터 시장의 혁신과 유통을 견인하는 주요 기업으로는 Ornua Co-operative Limited(Kerrygold), Arla Foods amba(Lurpak), Lactalis Group(President), Fonterra Co-operative Group(Anchor), Gujarat Cooperative Milk Marketing Federation Ltd.(Amul) Danone SA, Nestle SA, The JM Smucker Company(Eagle Brand), Arla Foods, and Friesland Campina NV 등이 있습니다. 콘덴스 우유와 에바밀크 분야에서 영향력 있는 역할을 하고 있습니다.

시장 포지션을 강화하기 위해 고지방 버터 부문의 기업은 제품의 혁신을 우선하고 투명성과 품질에 대한 소비자의 요구 증가에 부응하기 위해 깨끗한 라벨과 유기농 인증에 주력하고 있습니다. 부문을 캡처하기 위해 허브, 향신료 및 프로바이오틱스를 배합한 인퓨즈드 버터를 도입하여 맛 포트폴리오를 확대하고 있습니다. 선택을 요구하는 소비자를 캡처하기 위해 제품의 본격적이고 장인적인 성격을 강조하고 있습니다. 지속 가능한 조달과 생산 관행에 대한 투자는 환경 문제에 대한 관심을 따라 브랜드의 명성을 향상시키고 있습니다.

The Global High Fat (>85%) Butter Market was valued at USD 250.5 million in 2024 and is estimated to grow at a CAGR of 6.8% to reach USD 480.2 million by 2034. This steady growth is driven by a rising consumer preference for richer, more natural, and artisanal dairy products. High-fat butter, once limited to niche segments such as gourmet baking and fine dining, has now gained traction among health-conscious consumers following trends like low-carb and ketogenic diets. There is an emerging premium segment focused on clean-label, organically certified, and origin-verified butter produced through traditional churning methods.

Despite fluctuations in supply and price, the demand for indulgent, flavorful dairy items remains strong. Innovations in product offerings, increased awareness of fat's functional benefits, and growing global populations with high standards for quality and authenticity are all contributing to the market's expansion. Additionally, evolving retail strategies, greater access to emerging markets, and the rise of specialty food stores and e-commerce platforms support ongoing market growth.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$250.5 Million

Forecast Value

$480.2 Million

CAGR

6.8%

The baking and confectionery segment is projected to grow at a faster pace, with a CAGR of 6.3%. Within the high-fat (>85%) butter market, baking and confectionery dominate application trends thanks to growing demand for superior texture, rich flavor, and consistent quality in premium pastries, cookies, and chocolates. Culinary uses are also on the rise, as chefs increasingly choose high-fat butter for sauteing, sauces, and boosting flavor profiles. Consumers seeking indulgent, creamy spreads and toppings are further driving this demand, while nutritional trends like keto and high-fat diets are expanding butter's role in dietary applications.

In 2024, the blocks and sticks segment accounted for a 41.5% share and is projected to grow at a CAGR of 6.4%, attracting a broader consumer base. These formats continue to dominate, especially in Western regions, due to their convenience, familiarity, and ease of measurement for cooking and baking. Urban health-conscious consumers particularly appreciate these soft, spreadable formats for their direct application on bread and crackers, combining convenience without compromising flavor.

Europe High Fat (>85%) Butter Market held a 34.3% share in 2024. This dominance is driven by the region's deep-rooted culinary heritage, where butter plays a vital role in traditional recipes and gourmet cooking. European consumers have a well-developed appreciation for high-quality dairy, prioritizing authenticity, rich flavor, and artisanal production methods. Additionally, widespread consumer education around premium and clean-label products fuels steady demand for high-fat butter across both retail and food service sectors. The presence of established dairy producers and a robust distribution network further strengthens Europe's position as a key player in this market, ensuring continuous availability of specialty butter products that meet the discerning tastes of its consumers.

Key players driving innovation and distribution in the High Fat (>85%) Butter Market include Ornua Co-operative Limited (Kerrygold), Arla Foods amba (Lurpak), Lactalis Group (President), Fonterra Co-operative Group (Anchor), and Gujarat Cooperative Milk Marketing Federation Ltd. (Amul). Danone S.A., Nestle S.A., The J.M. Smucker Company (Eagle Brand), Arla Foods, and Friesland Campina N.V. play influential roles in the condensed and evaporated milk segments.

To strengthen their market position, companies in the high-fat butter sector are prioritizing product innovation, focusing on clean-label and organic certifications to meet growing consumer demands for transparency and quality. They are expanding their flavor portfolios by introducing infused butter with herbs, spices, and probiotics to capture niche culinary and health-focused segments. Marketing efforts emphasize the authentic, artisanal nature of their products, connecting with consumers seeking premium, natural dairy options. Strategic partnerships with specialty retailers and online platforms enhance accessibility and consumer reach. Furthermore, investments in sustainable sourcing and production practices are improving brand reputation while aligning with environmental concerns. These combined strategies allow companies to build loyalty and tap into expanding global markets.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Product

2.2.3 End Use

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier Landscape

3.1.2 Profit Margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.2 Industry pitfalls and challenges

3.2.3 Market opportunities

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.6.1 Technology and innovation landscape

3.6.2 Current technological trends

3.6.3 Emerging technologies

3.7 Price trends

3.7.1 By region

3.7.2 By product

3.8 Future market trends

3.9 Technology and innovation landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent Landscape

3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and environmental aspects

3.12.1 Sustainable practices

3.12.2 Waste reduction strategies

3.12.3 Energy efficiency in production

3.12.4 Eco-friendly Initiatives

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Million) (Kilo Tons)