RTD(Ready-To-Drink) 차 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)

RTD Tea Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1750518

리서치사:Global Market Insights Inc.

발행일:2025년 05월

페이지 정보:영문 210 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

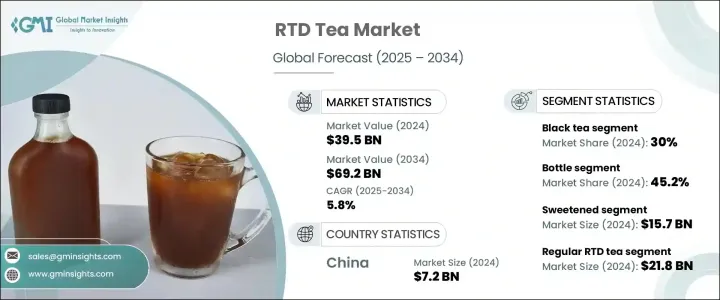

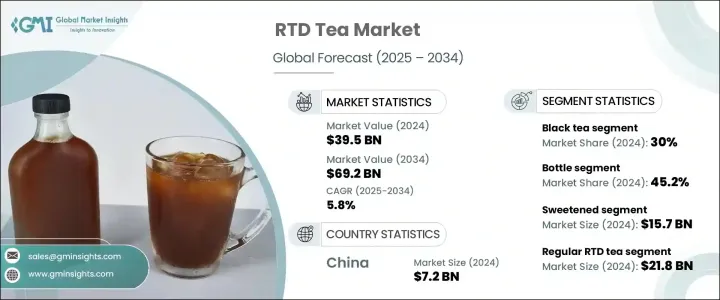

세계의 RTD 차 시장 규모는 2024년에 395억 달러로 평가되었고, 소비자의 건강 의식 증가와 편리한 음료 옵션에 대한 수요 증가에 의해 2034년까지는 692억 달러에 달할 것으로 추정되며, CAGR 5.8%로 성장할 전망입니다.

더 많은 사람들이 단 음료의 건강한 대안을 찾게 되면서, RTD 차는 녹차, 홍차, 허브차와 같은 천연 성분으로 인기를 얻고 있습니다. 클린 라벨 제품에 대한 선호도가 높아지고 있으며, 소비자들은 항산화제, 프로바이오틱스, 강장제 등 건강에 추가적인 효능을 제공하는 음료를 찾고 있습니다. 지속 가능성도 중요한 역할을 하고 있으며, 재활용 가능한 포장재가 구매 결정의 핵심 요인이 되고 있습니다.

RTD 차는 탄산음료나 설탕이 많은 주스보다 건강에 좋고 칼로리가 낮은 옵션으로, 사무직 종사자, 운동선수, 건강을 중시하는 소비자들에게 인기입니다. 슈퍼마켓, 편의점, 자판기, 온라인 플랫폼을 통해 널리 접근 가능해 모든 연령층을 대상으로 합니다. 제품 유형에 따라 RTD 차는 다양한 건강 혜택을 제공합니다. 녹차와 홍차는 정신 집중력을 높여주고, 허브나 콤부차 제품은 소화를 돕습니다. 휴대성, 다양한 맛, 건강 혜택은 맛있고 편리한 음료를 찾는 소비자에게 이상적인 선택입니다.

시장 범위

시작 연도

2024년

예측 연도

2025년-2034년

시작금액

395억 달러

예측 금액

692억 달러

CAGR

5.8%

병 포장 부문은 RTD 차 시장에서 가장 큰 비중을 차지하며, 2024년에는 45.2%의 상당한 점유율을 차지하고 2034년까지 6%의 CAGR로 꾸준히 성장할 것으로 예상됩니다. 병 포장 RTD 차는 사용자 친화적인 디자인, 특히 재밀봉 가능한 뚜껑으로 인해 소비자에게 선호됩니다. 이 병은 외부 요인으로부터 제품을 보호해 맛, 신선도, 영양 성분을 장시간 유지합니다. 또한 소매 및 자판기 환경에서 견고한 구조, 편리한 취급 및 보관의 장점을 갖추고 있습니다.

가당 RTD 차 부문은 2024년에 157억 달러의 매출을 올렸습니다. 이 카테고리는 다양한 맛을 제공하여 약간 단맛을 선호하는 사람과 단맛을 좋아하는 사람 모두의 취향을 만족시키며, 폭넓은 소비자층에게 큰 반향을 일으키고 있습니다. 이 제품의 인기는 상쾌한 맛과 친숙함에서 비롯되며, 즉각적인 맛을 원하는 사람들에게 인기 있는 음료로 자리매김했습니다. 이 부문은 지배적 지위를 차지하고 있지만, 건강에 민감한 소비자들이 당 함량을 줄이고 건강에 좋은 제품을 요구함에 따라 점차 진화하고 있습니다. 이러한 변화에 따라 브랜드들은 맛과 건강의 균형을 맞추기 위해 천연 감미료와 저칼로리 제형을 사용한 혁신을 추진하고 있습니다.

아시아태평양 RTD 차 시장은 2024년에 72억 달러를 달성했으며, 2034년까지 연평균 5.6%의 성장률을 보일 것으로 예상됩니다. 중국의 시장 리더십은 차에 대한 문화적 친밀감, 강력한 국내 생산 능력, 기능성 차의 이점에 대한 소비자 인식 증가에 뿌리를 두고 있습니다. 도시 인구 증가와 생활 방식의 속도화 속에서 RTD 차의 편의성과 휴대성은 이동 중 수분 보충에 필수적인 요소로 자리 잡았습니다. 또한 전통적인 맛과 현대적인 건강 혜택의 융합은 젊은 층과 건강을 중시하는 소비자에게 선호되는 음료로 RTD 차를 포지셔닝했습니다.

Unilever PLC, Nestle S.A., Suntory Holdings, PepsiCo Inc. 및 The Coca-Cola Company와 같은 기업들은 특히 기능성 차 부문에서 제품 범위를 확대하는 데 주력하고 있습니다. 이러한 기업들은 지속 가능한 포장 솔루션에 투자하고, 다양한 맛을 제공하며, 현지 유통업체들과 제휴를 맺어 주요 시장에서 입지를 강화하고 있습니다. 소매 및 온라인 채널을 통한 접근성을 개선하고 건강에 초점을 맞춘 혁신에 집중함으로써, 이러한 기업들은 성장하는 RTD 차 시장에서 더 많은 점유율을 확보하는 것을 목표로 하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

업계 생태계 분석

트럼프 정권에 의한 관세에 대한 영향

무역에 미치는 영향

무역량의 혼란

보복 조치

업계에 미치는 영향

공급측의 영향(원자재)

주요 원자재의 가격 변동

공급망 재구성

생산 비용에 미치는 영향

수요측의 영향(판매가격)

최종 시장에의 가격 전달

시장 점유율 동향

소비자의 반응 패턴

영향을 받는 주요 기업

전략적인 업계 대응

공급망 재구성

가격 설정 및 제품 전략

정책관여

전망과 향후 검토 사항

무역 통계(HS코드)

주요 수출국(2021-2024년)

주요 수입국(2021-2024년)

참고 : 위의 무역 통계는 주요 국가에 대해서만 제공됩니다.

업계 밸류체인 분석

제품 개요

티의 가공 방법

RTD 차 제작 프로세스

보존 기술

풍미를 높이는 기술

시장 역학

시장 성장 촉진요인

건강 및 기능성 음료에 대한 수요 증가

도시화와 바쁜 라이프 스타일의 확대

향료 첨가 차 블렌드의 혁신

시장 성장 억제요인

다른 RTD 음료와의 격렬한 경쟁

원재료(차 잎) 가격 변동

시장 기회

시장의 과제

업계에 미치는 영향요인

성장 가능성 분석

업계의 잠재적 리스크 및 과제

규제 프레임워크과 기준

식품안전규제

라벨 요건

유기농 및 내츄럴 제품 인증

건강 강조 표시 규제

제조 공정 분석

차 추출 방법

블렌드와 배합

저온 살균과 보존

포장 기술

원자재 분석 및 조달 전략

가격 분석

지속가능성과 환경영향 평가

PESTEL 분석

Porter's Five Forces 분석

제4장 경쟁 구도

소개

전략 틀

합병과 인수

합작투자 콜라보레이션

신제품 개발

확대 전략

경쟁 벤치마킹

벤더 상황

경쟁 포지셔닝 매트릭스

전략적 대시보드

브랜드 포지셔닝과 소비자 인식 분석

신규 참가자 시장 진출 전략

제5장 시장 규모와 예측 : 제품 유형별(2021-2034년)

주요 동향

홍차

가당 홍차

무당 홍차

향료 첨가 홍차

녹차

가당 녹차

무당 녹차

향료 첨가 녹차

허브차

카모마일

민트

루이보스

기타 허브차

과일 차

감귤류

베리

트로피컬

믹스 과일

우롱차

백차

말차

콤부차

기타

제6장 시장 규모와 예측 : 포장별(2021-2034년)

주요 동향

병

페트병

유리병

기타 병 유형

캔

알루미늄 캔

강철 캔

판지

무균 판지

게이블 탑 판지

파우치

기타

제7장 시장 규모와 예측 : 단맛 수준별(2021-2034년)

주요 동향

가당

설탕

고과당 옥수수 시럽

꿀과 천연 감미료

저당

무당

인공 감미료

아스파탐

수크랄로스

스테비아

기타

제8장 시장 규모와 예측 : 기능적 효능별(2021-2034년)

주요 동향

일반 RTD 차

강화 RTD 차

비타민 강화

미네랄 강화

항산화 물질 강화

기능성 RTD 차

에너지 향상

면역 지원

소화기계의 건강

이완 및 스트레스 해소

유기농 RTD 차

클린 라벨 RTD 차

제9장 시장 규모와 예측 : 유통 채널별(2021-2034년)

주요 동향

슈퍼마켓 및 대형 슈퍼마켓

편의점

전문점

온라인 소매

푸드서비스

카페 및 레스토랑

패스트 푸드 체인

시설내 케이터링

자동판매기

기타

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제11장 기업 프로파일

The Coca-Cola Company

PepsiCo, Inc

Unilever PLC

Nestle SA

Suntory Holdings Limited

ITO EN, Ltd.

Danone SA

Arizona Beverages USA

Keurig Dr Pepper Inc.

Tata Consumer Products Limited

Starbucks Corporation

Honest Tea(Coca-Cola)

Lipton(Unilever/PepsiCo)

Tejava(Crystal Geyser Water Company)

Harney &Sons

The Republic of Tea

Numi Organic Tea

Pokka Corporation

Oi Ocha(ITO EN)

Vita Coco

GT's Living Foods(Kombucha)

Health-Ade Kombucha

Steaz

Pure Leaf(Unilever/PepsiCo)

Gold Peak(Coca-Cola)

Snapple(Keurig Dr Pepper)

Tazo(Unilever)

Fuze Tea(Coca-Cola)

HBR

영문 목차

영문목차

The Global RTD Tea Market was valued at USD 39.5 billion in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 69.2 billion by 2034, driven by increasing health awareness among consumers and the rising demand for convenient beverage options. As more people look for healthier alternatives to sugary drinks, RTD tea has gained popularity for its natural ingredients like green tea, matcha, and herbal teas. There is a growing preference for clean-label products, and consumers are seeking beverages that offer added health benefits such as antioxidants, probiotics, and adaptogens. Sustainability also plays a significant role, with recyclable packaging materials becoming a key factor in purchasing decisions.

RTD tea serves as a healthier, low-calorie option compared to soft drinks and sugary juices, making it a favorite among office workers, athletes, and health-conscious individuals. It is widely accessible through supermarkets, convenience stores, vending machines, and online platforms, catering to people of all ages. Depending on the variant, RTD tea offers various health benefits, from boosting mental alertness with green and black teas to aiding digestion with herbal or kombucha options. Its portability, variety of flavors, and health advantages make it an ideal choice for many consumers looking for a tasty, convenient drink.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$39.5 Billion

Forecast Value

$69.2 Billion

CAGR

5.8%

The bottle-based packaging segment commands the largest portion of the RTD tea market, holding a substantial 45.2% share in 2024 and projected to grow steadily at a 6% CAGR through 2034. Bottled RTD teas are preferred by consumers largely due to their user-friendly design, particularly the resealable caps that make them ideal for active, on-the-go lifestyles. These bottles offer superior protection against external elements, preserving the product's taste, freshness, and nutritional integrity over time. Their sturdy build, easy handling, and storage, especially in retail and vending environments.

The sweetened RTD tea segment generated USD 15.7 billion in 2024. This category resonates strongly with a wide consumer base, offering a variety of flavors that cater to both mildly sweet and heavily sweetened preferences. Its popularity stems from its refreshing taste and familiarity, making it a go-to beverage for those seeking instant gratification in flavor. Despite its dominance, the segment is gradually evolving as more health-conscious consumers demand reduced sugar content and better-for-you options. This shift has prompted brands to innovate with naturally sweetened and low-calorie formulations to balance indulgence with wellness.

Asia-Pacific RTD Tea Market generated USD 7.2 billion in 2024 and is anticipated to have a CAGR of 5.6% through 2034. China's leadership in the market is deeply rooted in its cultural affinity for tea, strong domestic production capabilities, and increasing consumer awareness around the benefits of functional teas. As the nation's urban population grows and lifestyles become more fast-paced, the convenience and portability of RTD teas are becoming essential for on-the-go hydration. Additionally, the fusion of traditional flavors with modern health benefits has positioned RTD teas as a preferred beverage among the younger, health-aware population.

Companies like Unilever PLC, Nestle S.A., Suntory Holdings, PepsiCo Inc., and The Coca-Cola Company focus on expanding their product ranges, particularly in the functional tea segment. These companies are investing in sustainable packaging solutions, offering flavors, and partnering with local distributors to strengthen their presence in key markets. By improving accessibility through retail and online channels and focusing on health-focused innovations, these players aim to capture more of the growing RTD tea market.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope & definition

1.2 Base estimates & calculations

1.3 Forecast calculation

1.4 Data sources

1.4.1 Primary

1.4.2 Secondary

1.4.2.1 Paid sources

1.4.2.2 Public sources

1.5 Primary research and validation

1.5.1 Primary sources

1.5.2 Data mining sources

Chapter 2 Executive Summary

2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.2 Trump administration tariffs

3.2.1 Impact on trade

3.2.1.1 Trade volume disruptions

3.2.1.2 Retaliatory measures

3.2.2 Impact on the industry

3.2.2.1 Supply-side impact (raw materials)

3.2.2.1.1 Price volatility in key materials

3.2.2.1.2 Supply chain restructuring

3.2.2.1.3 Production cost implications

3.2.2.2 Demand-side impact (selling price)

3.2.2.2.1 Price transmission to end markets

3.2.2.2.2 Market share dynamics

3.2.2.2.3 Consumer response patterns

3.2.3 Key companies impacted

3.2.4 Strategic industry responses

3.2.4.1 Supply chain reconfiguration

3.2.4.2 Pricing and product strategies

3.2.4.3 Policy engagement

3.2.5 Outlook and future considerations

3.3 Trade statistics (HS Code)

3.3.1 Major exporting countries, 2021-2024 (Kilo Tons)

3.3.2 Major importing countries, 2021-2024 (Kilo Tons)

Note: the above trade statistics will be provided for key countries only.

3.4 Industry value chain analysis

3.5 Product overview

3.5.1 Tea processing methods

3.5.2 RTD tea production process

3.5.3 Preservation technologies

3.5.4 Flavor enhancement techniques

3.6 Market dynamics

3.6.1 Market drivers

3.6.1.1 Rising demand for healthy and functional beverages

3.6.1.2 Increasing urbanization and busy lifestyles

3.6.1.3 Innovation in flavors and tea blends

3.6.2 Market Restraints

3.6.2.1 High competition from other RTD beverages

3.6.2.2 Fluctuating raw material (tea leaf) prices

3.6.3 Market opportunities

3.6.4 Market challenges

3.7 Industry impact forces

3.7.1 Growth potential analysis

3.7.2 Industry pitfalls & challenges

3.8 Regulatory framework & standards

3.8.1 Food safety regulations

3.8.2 Labeling requirements

3.8.3 Organic & natural product certifications

3.8.4 Health claim regulations

3.9 Manufacturing process analysis

3.9.1 Tea extraction methods

3.9.2 Blending & formulation

3.9.3 Pasteurization & preservation

3.9.4 Packaging technologies

3.10 Raw material analysis & procurement strategies