Vegan Ingredients Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1750453

리서치사:Global Market Insights Inc.

발행일:2025년 05월

페이지 정보:영문 235 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

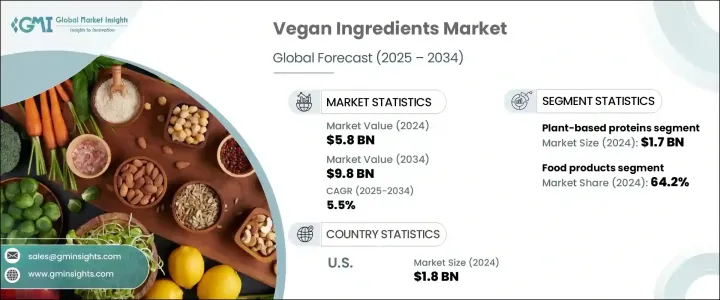

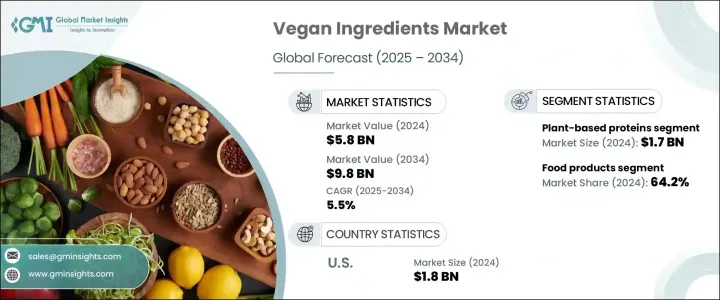

세계의 비건 재료 시장 규모는 2024년 58억 달러로 평가되었고, 식물성 식품으로의 전환과 소비자 선호도의 변화, 환경에 대한 인식의 제고, 전통적인 동물성 식품에 비해 더 건강한 대체 식품에 대한 접근성 향상으로 인해, 2034년에는 98억 달러에 이를 것으로 예측되며, CAGR 5.5%로 성장할 전망입니다.

사람들이 음식 선택과 동물에 대한 윤리적 대우에 대해 점점 더 인식이 높아짐에 따라 비건 재료는 식품 혁신의 핵심 초점이 되었습니다. 식물성 영양에 대한 관심 증가로 인해 콩, 완두콩, 쌀, 렌틸콩 등 식물성 단백질에 대한 수요가 급증하고 있습니다. 이러한 단백질은 지속 가능성뿐 아니라 다양한 식품 응용 분야에서 기능적 혜택을 제공하기 때문입니다. 이는 식품의 생산, 유통, 소비 방식에 근본적인 변화를 가져오고 있습니다.

이 동향의 주요 촉진 요인은 식물성 식단의 채택이 증가하면서 즉석식, 스낵, 음료, 심지어 건강 보조 식품에 이르기까지 다양한 카테고리에서 비건 식품이 폭발적으로 증가했기 때문입니다. 동물성 제품보다 생산에 필요한 자원이 적은 식물성 원료의 환경적 이점도 이러한 변화를 촉진했습니다. 지속 가능한 농업을 지원하고 대체 단백질 원료의 사용을 촉진하는 정부 정책도 시장 확장을 더욱 가속화하고 있습니다. 이 제품에 대한 수요가 증가함에 따라 혁신은 계속 중요한 역할을 하고 있으며, 식물성 식품의 텍스처와 영양 프로필을 향상시키기 위해 발효 마이코단백질과 같은 새로운 원료가 시장에 진입하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

58억 달러

예측 금액

98억 달러

CAGR

5.5%

식물성 단백질 부문은 30.2%의 점유율을 차지했으며, 2024년 시장 규모는 17억 달러였습니다. 콩, 완두콩, 렌틸콩 등 작물에서 추출된 이 단백질들은 소비자들이 육류 대체품을 찾는 추세에 따라 인기를 얻고 있습니다. 식물성 단백질에 대한 관심 증가로 단백질 원천의 다양화가 진행 중이며, 정부들도 지속 가능한 농업에서 콩류와 곡물을 중요한 작물로 홍보하고 있습니다. 이 식물성 단백질은 육류 대체품뿐 아니라 베이커리 제품, 스낵, 편의 식품 등 다양한 식품에 사용되고 있으며, 단백질 함량이 건강 혜택으로 강조되고 있습니다.

2024년에 37억 달러로 평가된 식품 분야는 2034년까지의 점유율 64.2%를 차지하고, 비건 재료 시장에서의 지배적 위치를 유지할 것으로 예상됩니다. 이 카테고리에는 식물성 유제품 및 육류 대체품, 즉석 조리 식품, 스낵, 과자 등 다양한 제품이 포함됩니다. 이 부문에서 비건 재료에 대한 수요가 크게 증가하는 것은 주로 건강에 대한 소비자의 인식이 높아지고, 동물 사육에 대한 윤리적 우려와 전통적인 동물성 식품 생산이 환경에 미치는 영향이 커지고 있기 때문입니다.

미국의 비건 재료 시장은 2024년에는 18억 달러로 2034년까지 연평균 성장률(CAGR) 6.3%의 강력한 성장을 계속할 것으로 전망됩니다. 미국은 소비와 혁신 측면에서 모두 선도적 역할을 하며, 세계의 시장의 주요 성장 동력으로 작용하고 있습니다. 이러한 급증에 기여한 요인은 개인 건강에 대한 인식의 증가, 공장식 축산의 윤리적 문제에 대한 우려의 증가, 식물성 식단으로의 전환 등입니다. 미국 시장은 더 건강하고 지속 가능한 식품에 대한 수요에 대응할 뿐만 아니라 비건 식품의 혁신을 촉진하고 있습니다.

세계의 비건 식재료 시장의 주요 기업으로는 Cargill, ADM, Evonik, BASF, Beyond Meat 등이 있습니다. 이 기업들은 혁신적인 기술을 도입해 제품 포트폴리오를 확장하고 제품 품질을 개선하는 데 집중하고 있습니다. 또한 친환경 생산 공정 투자와 다양한 산업에서의 식물성 원료 채택을 촉진하기 위한 파트너십을 강화하며 지속 가능성 노력을 강화하고 있습니다. 제품 라인 다각화와 비건 원료의 새로운 응용 분야 탐구를 통해 이 기업들은 급성장하는 시장에서 입지를 공고히 하려는 목표를 추구하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

밸류체인에 영향을 주는 요인

이익률 분석

혁신

장래의 전망

제조업자

리셀러

트럼프 정권에 의한 관세에 대한 영향

무역에 미치는 영향

무역량의 혼란

보복 조치

업계에 미치는 영향

공급측의 영향(원재료)

주요 원재료의 가격 변동

공급망 재구성

생산 비용에 미치는 영향

수요측의 영향(판매가격)

최종 시장에의 가격 전달

시장 점유율 동향

소비자의 반응 패턴

영향을 받는 주요 기업

전략적인 업계 대응

공급망 재구성

가격 설정 및 제품 전략

정책관여

전망과 향후 검토 사항

무역 통계(HS코드)

주요 수출국(2021-2024년)

주요 수입국(2021-2024년)

공급자의 상황

이익률 분석

주요 뉴스와 대처

규제 상황

세계의 규제 틀의 개요

FDA 규제

EU의 화장품 규제

중국의 CSAR(화장품 감독 관리 규제)

영향요인

성장 촉진요인

건강 의식 향상

환경의 지속가능성

식물성 식품 분야의 기술 발전

정부 지원 및 정책 조치

업계의 잠재적 위험 및 과제

높은 생산 비용

소비자 인식 및 수용도 부족

시장 기회

개발도상국 시장 진출

영양제 및 화장품용 기능성 비건 원료 혁신

식품 서비스 및 사설 브랜드를 위한 맞춤형 B2B 솔루션

지속 가능한 포장 및 클린 라벨 포지셔닝

시장 진입과 확대 전략

시장 진입 장벽과 과제

규제상의 장애물 및 규정 준수 비용

지적재산의 제약

확립된 기업의 우위성

기술적 전문지식 요건

시장 진출 전략

합작사업과 전략적 제휴

라이선싱과 기술이전

인수와 브라운필드 진입

그린필드 투자와 유기적 성장

지리적 확대의 기회

고성장 지역 시장

미개척 시장의 잠재적 평가

문화 및 규제 고려 사항

현지화 및 적응 전략

제품 포트폴리오 확대 전략

라인 확장 및 제품 변형

카테고리간 확장

프리미엄 및 가치 부문 타겟팅

맞춤형 및 개인화 접근 방식

위험 평가 및 경감 전략

시장 위험

수요 변동성 및 주기성

경쟁 강도 및 가격 압력

대체 제품 및 기술

소비자의 기호의 변화

운영 위험

공급망의 혼란

품질관리 및 제품안전

제조와 배합의 과제

인력 및 인재 관리

규제 및 규정 준수 위험

규제 상황의 변화

원재료의 제한과 금지

라벨 표시 및 마케팅 클레임의 위험

미래 전망과 시장 예측

단기 시장 전망(1-2년)

곧 성장 기회

단기적인 과제

경쟁 구도의 진화

중기 시장 전망(3-5년)

신흥 시장 부문

기술 채택 곡선

수급 밸런스 예측

장기 시장 전망(5-10년)

파괴적 기술과 혁신

지속가능성 주도 시장변혁

소비자 행동의 진화

업계 통합과 재편 시나리오

시나리오 분석과 긴급시 대응 계획

최상의 성장 시나리오

기본 시장의 진화

최악 시장 축소

파괴적 시나리오 분석

투자 기회와 전략적 제안

투자 매력도 평가

고성장 시장 부문

기술 투자 기회

지리적 투자 핫스팟

M&A와 파트너십의 기회

원료 제조업체를 위한 전략적 제안

제품 개발과 혁신의 중점 분야

시장 포지셔닝과 차별화 전략

지속 가능성과 규제 준수 로드맵

파트너십 및 협업 기회

최종 제품 제조업체를 위한 전략적 권장 사항

제형 및 제품 개발 우선순위

소비자 참여 및 마케팅 전략

유통과 채널 최적화

지속가능성과 브랜드 포지셔닝

투자자 및 금융 이해관계자에 대한 전략적 제안

잠재성이 높은 투자대상

위험 평가 및 완화 전략

포트폴리오 분산 전략

퇴출 전략 고려 사항

성장 가능성 분석

Porter's Five Forces 분석

PESTEL 분석

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

제5장 시장 추계 및 예측 : 제품별(2024-2034년)

주요 동향

식물성 단백질

콩 단백질

콩 단백질 분리물

콩 단백질 농축물

텍스처드 콩 단백질

콩가루

기타

완두콩 단백질

완두콩 단백질 분리물

완두콩 단백질 농축물

텍스처드 완두콩 단백질

밀 단백질

필수 밀 글루텐

밀 단백질 분리물

텍스처드 밀 단백질

쌀 단백질

쌀 단백질 분리물

쌀 단백질 농축물

기타

감자 단백질

조류 단백질

스피루리나

클로렐라

기타

식물 유래 유제품 대체품

식물성 우유

아몬드 밀크의 재료

두유의 재료

오트밀크의 재료

코코넛 밀크의 재료

쌀 우유 재료

기타

식물 유래 치즈 원료

단백질 염기

유지

향료

기능성 성분

식물성 요구르트 재료

단백질 염기

배양물 및 발효제

텍스처제

향료 성분

식물 유래 버터와 스프레드 원료

식물성 기름지

유화제

향료

착색제

식물 유래 아이스크림 재료

식물성 우유 기반

유지

감미료

안정제 및 유화제

계란 대체품

전분 기반 계란 대체품

단백질 기반 계란 대체품

섬유 기반 계란 대체품

콩류 계란 대체품

과일 기반 계란 대체품

아쿠아파바

식물 유래 유지

코코넛 오일

팜유

올리브유

아보카도 오일

해바라기 기름

캐놀라 오일

특수 식물성 기름

구조화 식물 지질

천연 향료 및 조미료

식물 유래의 풍미 풍부한 맛

식물 유래의 달콤한 맛

우마미 증강제

훈제 맛

향신료 추출물

허브 추출물

자연스러운 색상

안토시아닌

카로티노이드

클로로필

커큐민

비트 루트

기타

하이드로콜로이드 및 텍스처 라이저

한천

카라기난

구아검

로커스트 콩껌

펙틴

크산탄검

곤약 껌

가공 전분

채식 감미료

사탕수수당

비트당

코코넛당

메이플시럽

아가베넥터

데이트시럽

스테비아

라칸카 열매 추출물

비건 유화제

레시틴(콩, 해바라기)

모노글리세리드 및 디글리세라이드(식물 유래)

감귤류의 섬유

기타

비건 방부제

로즈마리 추출물

토코페롤

아스코르브산

기타

전문 분야 비건 식재료

영양효모

해초 및 조류 유래 제품

발효 식품

기타

제6장 시장 추계 및 예측 : 용도별(2024-2034년)

주요 동향

식품

식물 유래의 대체 고기

햄버거와 퍼티

소시지와 핫도그

너겟과 스트립

갈고기의 대체품

델리스라이스

식물 유래의 유제품 대체품

우유 대체품

치즈의 대체품

요구르트의 대체품

버터와 스프레드의 대체품

아이스크림의 대체품

베이커리 제품

빵과 롤빵

케이크와 패스트리

쿠키와 비스킷

과자류

스낵

풍미 풍부한 스낵

에너지 바

국물

소스와 그레이비

드레싱과 마요네즈의 대체품

조리된 식사

냉동식품

유아용 조제 분유와 유아식

음료

식물성 우유

식물성 단백질 링크

스무디와 주스

커피와 차의 첨가물

알코올 음료

퍼스널케어 및 화장품

스킨케어 제품

헤어 케어 제품

색조 화장품

구강 케어 제품

영양보조식품

동물사료의 대체품

반려동물 식품

가축 사료

양식사료

기타

제7장 시장 추계 및 예측 : 지역별(2024-2034년)

주요 동향

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

네덜란드

아시아태평양

중국

인도

일본

한국

호주

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제8장 기업 프로파일

Aadhunik Ayurveda

ADM

BASF

Beyond Meat

Cargill

Evonik

Schouten

Symega

Tofurky

Trader Joe’s

HBR

영문 목차

영문목차

The Global Vegan Ingredients Market was valued at USD 5.8 billion in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 9.8 billion by 2034, driven by the shift toward plant-based foods and changes in consumer preferences, increasing environmental awareness, and greater access to healthier alternatives compared to traditional animal-based options. As people become more conscious of their food choices and ethical treatment of animals, vegan ingredients have become a key focus in food innovation. The growing interest in plant-based nutrition has led to increased demand for plant proteins, including soy, pea, rice, and lentils, which are not only more sustainable but also offer functional benefits in a variety of food applications. This has sparked a transformation in how food is produced, distributed, and consumed.

A major driving force behind this trend is the growing adoption of plant-based diets, which has led to an explosion of vegan food products across multiple categories, such as ready-to-eat meals, snacks, beverages, and even dietary supplements. The environmental benefits of plant-based ingredients-requiring fewer resources to produce than animal products-have also spurred the shift. Government initiatives supporting sustainable agriculture and the promotion of alternative protein sources are further boosting the market's expansion. As demand for these products rises, innovation continues to play a significant role, with new ingredients such as fermented mycoprotein entering the market to enhance the texture and nutritional profile of plant-based foods.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$5.8 Billion

Forecast Value

$9.8 Billion

CAGR

5.5%

The plant-based proteins segment held a 30.2% share and was valued at USD 1.7 billion in 2024. These proteins, sourced from crops like soy, peas, and lentils, are becoming increasingly popular as consumers seek alternatives to meat. The growing focus on plant proteins has led to a diversification of protein sources, as governments also promote legumes and pulses as vital crops in sustainable agriculture. These plant-based proteins are being used not only in meat substitutes but also in other food items, such as baked goods, snacks, and convenience meals, where their protein content is marketed as a health benefit.

The food products segment, valued at USD 3.7 billion in 2024, holds a dominant position in the vegan ingredients market, representing 64.2% share through 2034. This category encompasses a wide range of offerings, including plant-based dairy and meat alternatives, ready-to-bake items, snacks, and sweets. The significant demand for vegan ingredients within this sector is largely driven by increasing consumer awareness regarding health benefits, ethical concerns about animal farming, and the environmental impact of traditional animal-based food production.

United States Vegan Ingredients Market was valued at USD 1.8 billion in 2024 and is expected to continue growing at a robust CAGR of 6.3% through 2034. The U.S. leads both in terms of consumption and innovation, serving as a key driver of the global market. Factors contributing to this surge include rising awareness about personal health, a growing concern over the ethical implications of factory farming, and a shift towards plant-based diets. The American market is not only responding to the demand for healthier and more sustainable food options but also driving forward innovation in vegan food products.

Key companies in the Global Vegan Ingredients Market include Cargill, ADM, Evonik, BASF, and Beyond Meat. These companies have been focusing on expanding their portfolios and improving product offerings by adopting innovative technologies. They are also enhancing their sustainability efforts by investing in eco-friendly production processes and forging partnerships to promote the adoption of plant-based ingredients across various industries. By diversifying their product ranges and exploring new applications for vegan ingredients, these firms aim to solidify their positions in the rapidly growing market.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope & definitions

1.2 Base estimates & calculations

1.3 Forecast calculations

1.4 Data sources

1.4.1 Primary

1.4.2 Secondary

1.4.2.1 Paid sources

1.4.2.2 Public sources

Chapter 2 Executive Summary

2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Factor affecting the value chain

3.1.2 Profit margin analysis

3.1.3 Disruptions

3.1.4 Future outlook

3.1.5 Manufacturers

3.1.6 Distributors

3.2 Trump administration tariffs

3.2.1 Impact on trade

3.2.1.1 Trade volume disruptions

3.2.1.2 Retaliatory measures

3.2.2 Impact on the industry

3.2.2.1 Supply-side impact (raw materials)

3.2.2.1.1 Price volatility in key materials

3.2.2.1.2 Supply chain restructuring

3.2.2.1.3 Production cost implications

3.2.3 Demand-side impact (selling price)

3.2.3.1 Price transmission to end markets

3.2.3.2 Market share dynamics

3.2.3.3 Consumer response patterns

3.2.4 Key companies impacted

3.2.5 Strategic industry responses

3.2.5.1 Supply chain reconfiguration

3.2.5.2 Pricing and product strategies

3.2.5.3 Policy engagement

3.2.6 Outlook and future considerations

3.3 Trade statistics (HS code)

3.3.1 Major exporting countries, 2021-2024 (kilo tons)

3.3.2 Major importing countries, 2021-2024 (kilo tons)

3.4 Supplier landscape

3.5 Profit margin analysis

3.6 Key news & initiatives

3.7 Regulatory landscape

3.7.1 Global regulatory framework overview

3.7.2 FDA regulations

3.7.3 EU cosmetics regulation

3.7.4 China's CSAR (cosmetic supervision and administration regulation)

3.8 Impact forces

3.8.1 Growth drivers

3.8.1.1 Rising health consciousness

3.8.1.2 Environmental sustainability

3.8.1.3 Technological advancements in plant-based foods

3.8.1.4 Government support and policy initiatives

3.8.2 Industry pitfalls & challenges

3.8.2.1 High production costs

3.8.2.2 Limited consumer awareness and acceptance

3.9 Market opportunities

3.9.1 Expansion into developing economies

3.9.2 Innovation in functional vegan ingredients for nutraceuticals and cosmetics

3.9.3 Customized B2B solutions for food service and private label

3.9.4 Sustainable packaging and clean label positioning

3.10 Market entry and expansion strategies

3.10.1 Market entry barriers and challenges

3.10.1.1 Regulatory hurdles and compliance costs

3.10.1.2 Intellectual property constraints

3.10.1.3 Established player dominance

3.10.1.4 Technical expertise requirements

3.10.2 Market entry strategies

3.10.2.1 Joint ventures and strategic alliances

3.10.2.2 Licensing and technology transfer

3.10.2.3 Acquisition and brownfield entry

3.10.2.4 Greenfield investment and organic growth

3.10.3 Geographic expansion opportunities

3.10.3.1 High-growth regional markets

3.10.3.2 Untapped market potential assessment

3.10.3.3 Cultural and regulatory considerations

3.10.3.4 Localization and adaptation strategies

3.10.4 Product portfolio expansion strategies

3.10.4.1 Line extensions and product variants

3.10.4.2 Cross-category expansion

3.10.4.3 Premium and value segment targeting

3.10.4.4 Customization and personalization approaches