The Global Market for Automotive Cybersecurity: Safeguarding the Software-Defined Vehicle

상품코드:1618862

리서치사:VDC Research Group, Inc.

발행일:2024년 12월

페이지 정보:영문 50 Pages/13 Exhibits; plus 416 Exhibits/Excel

라이선스 & 가격 (부가세 별도)

한글목차

자동차 업계는 자동차 사이버 보안 요구사항을 근본적으로 변화시키는 소프트웨어 정의 차량(SDV) 개념으로 전례 없는 전환을 추진하고 있습니다.

이 보고서는 텔레매틱스, V2X(Vehicle-to-Everything) 통신, 차량 내 결제, 차량 충전, 인포테인먼트 시스템 기능, 오픈 소스 아키텍처, 기타 업계 소프트웨어의 발전과 노력 등 자동차 사이버 보안 시장에 영향을 미치는 기술 및 동향에 대한 개요를 기술하고 있습니다. 또한, VDC의 지속적인 조사 대상 기술 시장과의 연계 활동의 일환으로 VDC의 'Voice of the Engineer(엔지니어의 목소리)' 설문조사를 통해 얻은 최종사용자들의 의견도 소개합니다. 마지막으로, 이 보고서는 자동차 사이버 보안 시장을 주도하고 있는 수십 개의 주요 벤더들을 소개합니다.

인포그래픽

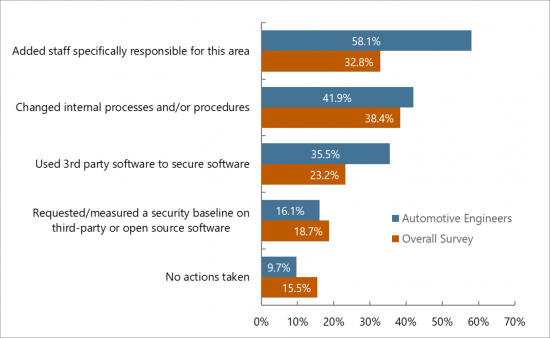

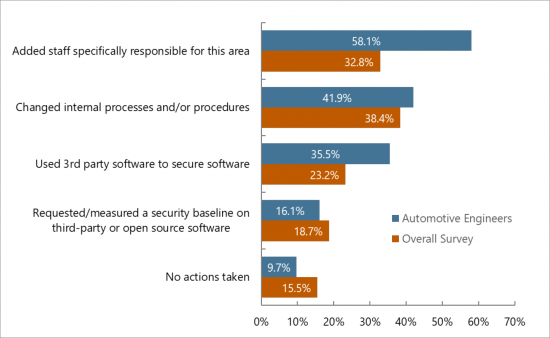

표 9 : 보안 요구사항에 대응하기 위해 응답 조직이 취한 조치

(응답자 비율, 복수응답 가능)

대응하는 질문:

소프트웨어와 커넥티비티의 대규모 도입은 자동차 사이버 보안에 어떤 영향을 미쳤을까?

보안 소프트웨어, SaaS, 전문 서비스 중 어떤 분야가 가장 빠르게 성장하고 있는가?

자동차 사이버 보안 규제의 미래와 규제의 미래를 이해함으로써 얻을 수 있는 것은 무엇인가?

2028년까지 자동차 사이버 보안 시장의 성장을 주도할 지역은 어디일까?

IoT 엔지니어와 자동차 엔지니어는 사이버 보안 문제에 어떻게 대응하고 있는가?

자동차 사이버 보안 시장을 형성하고 있는 기업은 누구이며, 어떤 방식으로 시장을 형성하고 있는가?

본 보고서에 게재된 조직:

ANSYS

Aptiv/Wind River

AUTOCRYPT

AWS

BlackBerry QNX

Block Harbor

BMW

Bosch/ETAS

Broadcom

C2A Security

Capgemini

Continental/ Elektrobit/PlaxidityX

Cybellum

CYMOTIVE

CYRES

Dellfer

Denso

DENSO

DigiCert

Enigmatos

Entrust

Eviden

Excelfore

Ford

Futurex

Garrett Motion

Giesecke + Devrient

GM

GMV

Google

Green Hills Software

GuardKnox

HARMAN

Hitachi/Astemo

Honda

Hyundai

IDIADA Automotive

INTEGRITY Security Services

Intertrust

Irdeto

itemis

ITK Engineering

J.P. Morgan

Jaguar Land Rover

Karamba Security

Kaspersky

Keyfactor

Lear

LG Electronics

LHP Engineering Solutions

Luxoft

Magna

Mercedes-Benz

Microsoft

Mitsubishi Motors

Mitsubishi Electric

Mobis

Nexus Group

Nissan

NNG

NTT Data

NXP

Panasonic

Qualcomm

Red Balloon Security

Renault

RunSafe Security

SAIC

Sectigo

Secunet

SiriusXM

Sonatus

StealthLabs

Stellantis

Subaru

Suzuki

SyncShield

Telefonica

Tencent

Tesla

Thales

Toyota

Trillium Secure

TrustCentral

Upstream Security

Utimaco GmbH

Valeo

Vector Informatik

Vic One

VinCSS JSC

Volkswagen

ZF Group

목차

본 보고서의 내용

다루고 있는 질문

본보고서를 읽어야 할 사람

본 보고서에 게재된 조직

주요 요약

주요 조사 결과

소개

소프트웨어 정의 차량이 취약성을 드러냄

SDV로의 전환에서 사이버 보안은 어떤 위치를 차지할 것인가?

V2X 접속

차량내 결제

차량 충전

앱과 API

AI의 역할

오픈 소스와 오픈 아키텍처

제품 상황

세계 시장 개요

자동차 사이버 보안 제품 분류

성장을 촉진하는 규제

WP.29 규칙 155 및 156

ISO/SAE 21434

미국의 규제

중국의 GB 44495-2024 및 GB 44496-2024

인도의 AISC AIS-189 및 AIS-190

지역 분석

업계 컨소시엄과 표준화 단체

ASRG

AUTO-ISAC

COVESA

digital.auto initiative

Eclipse SDV

eSync Alliance

MIPI Alliance

Uptane

벤더 상황

벤더 개요

BlackBerry QNX

Block Harbor

Bosch/ETAS

Continental/Elektrobit/PlaxidityX

Green Hills Software

Integrity Security Services

Irdeto

Karamba Security

Kaspersky

HARMAN

Sonatus

Thales

VicOne

Upstream

Vector

최종사용자 인사이트

보안 요구사항에 대한 업계의 적응

벤더 상황은 혁신을 지지

임베디드 보안 소프트웨어, 하드웨어, FOTA 구현

자동차 기술의 미래

저자 소개

VDC Research에 대해

도표 리스트*

ksm

영문 목차

영문목차

Inside this Report

The automotive industry is undergoing an unprecedented shift toward the software-defined vehicle (SDV) concept that is fundamentally changing the requirements for automotive cybersecurity. This report includes an overview of technologies and trends that influence the automotive cybersecurity market, including telematics and vehicle-to- everything (V2X) communication, payment by car, vehicle charging, infotainment system capabilities, open source architectures, and other industry software initiatives and advancements. As part of VDC's continued efforts to engage with the technology markets we research, this report includes end user insights from VDC's "Voice of the Engineer" survey. Lastly, this report highlights dozens of key automotive cybersecurity vendors that are shaping the market.

INFOGRAPHICS

Exhibit 9: Actions Taken by Respondents Organization in Response to Security Requirements

(Percentage of Respondents, Multiple Responses Permitted)

What Questions are Addressed?

How has the mass introduction of software and connectivity affected automotive cybersecurity?

Which segment is growing the fastest - Security software, Security-as-a-service or Professional services?

What is the future of automotive cybersecurity regulations and what can be gained by understanding the future of regulations?

Which geographic regions are driving growth in the automotive cybersecurity market through 2028?

How are IoT engineers and automotive engineers responding to cybersecurity concerns?

Which firms are shaping the automotive cybersecurity market and how are they doing it?

Who Should Read this Report?

CEO or other C-level executives

Corporate development and M&A teams

Marketing executives

Business development and sales leaders

Product development and product strategy leaders

Channel management and channel strategy leaders

Organizations Listed in this Report:

ANSYS

Aptiv/Wind River

AUTOCRYPT

AWS

BlackBerry QNX

Block Harbor

BMW

Bosch/ETAS

Broadcom

C2A Security

Capgemini

Continental/ Elektrobit/PlaxidityX

Cybellum

CYMOTIVE

CYRES

Dellfer

Denso

DENSO

DigiCert

Enigmatos

Entrust

Eviden

Excelfore

Ford

Futurex

Garrett Motion

Giesecke + Devrient

GM

GMV

Google

Green Hills Software

GuardKnox

HARMAN

Hitachi/Astemo

Honda

Hyundai

IDIADA Automotive

INTEGRITY Security Services

Intertrust

Irdeto

itemis

ITK Engineering

J.P. Morgan

Jaguar Land Rover

Karamba Security

Kaspersky

Keyfactor

Lear

LG Electronics

LHP Engineering Solutions

Luxoft

Magna

Mercedes-Benz

Microsoft

Mitsubishi Motors

Mitsubishi Electric

Mobis

Nexus Group

Nissan

NNG

NTT Data

NXP

Panasonic

Qualcomm

Red Balloon Security

Renault

RunSafe Security

SAIC

Sectigo

Secunet

SiriusXM

Sonatus

StealthLabs

Stellantis

Subaru

Suzuki

SyncShield

Telefonica

Tencent

Tesla

Thales

Toyota

Trillium Secure

TrustCentral

Upstream Security

Utimaco GmbH

Valeo

Vector Informatik

Vic One

VinCSS JSC

Volkswagen

ZF Group

Table of Contents

Inside this Report

What Questions are Addressed?

Who Should Read this Report?

Organizations Listed in this Report

Executive Summary

Key Findings

Introduction

Software-Defined Vehicles Expose Vulnerabilities

Where does Cybersecurity Fit in the Transition to the SDV?

V2X Connectivity

In-Car Payments

Vehicle Charging

Apps and APIs

The Role of Artificial Intelligence

Open Source and Open Architecture

Product Landscape

Global Market Overview

Automotive Cybersecurity Product Segmentation

Product Segmentations within the Automotive Cybersecurity Market

Regulations Driving Growth

WP.29 Regulations 155 and 156

ISO/SAE 21434

Regulations in the United States

China GB 44495-2024 and GB 44496-2024

India AISC AIS-189 and AIS-190

Regional Analysis

Industry Consortia and Standards Organizations

ASRG

AUTO-ISAC

COVESA

digital.auto initiative

Eclipse SDV

eSync Alliance

MIPI Alliance

Uptane

Vendor Landscape

Vendor Profiles

BlackBerry QNX

Block Harbor

Bosch / ETAS

Continental / Elektrobit / PlaxidityX

Green Hills Software

Integrity Security Services

Irdeto

Karamba Security

Kaspersky

HARMAN

Sonatus

Thales

VicOne

Upstream

Vector

End User Insights

Industry Adaptation to Security Requirements

Vendor Landscape Favors Innovation

Diminishing Influence of Established Tech and System Integrators

Implementation of Embedded Security Software, Hardware, and FOTA

The Future of Automotive Technology

About the Authors

About VDC Research

List of Exhibits*

Exhibit 1 Biggest Obstacle to the Development and Growth of the Connected/Software-Defined Vehicle Industry

Exhibit 2: Current Concerns About AI-generated Software Code

Exhibit 3: Sample Table of Vendors Offering Automotive Cybersecurity Solutions

Exhibit 4: Global Revenue of Automotive Cybersecurity Software and Services

Exhibit 5: Global Revenue for Automotive Cybersecurity Software and Services by Product Category

Exhibit 6: Global Revenue for Automotive Cybersecurity and Software, 2023 to 2028, Share by Product Category

Exhibit 7: Global Revenue for Automotive Cybersecurity Software and Services by Region

Exhibit 8: Global Revenue of Automotive Cybersecurity Software & Services by Geographic

Exhibit 9: Actions Taken by Respondents Organization in Response to Security Requirements

Exhibit 10: Current Major Competition in the Software-defined Space

Exhibit 11: Use of Embedded Security Software, Hardware, & Firmware-Over-the-Air Updating in Current Automotive Projects vs. Overall IoT Projects

Exhibit 12: Technologies Automotive Respondent's Organization is Most Interested in and/or Building for Future Customers

*This report also includes access to 416 Exhibits from our 2024 Voice of the Engineer Survey.