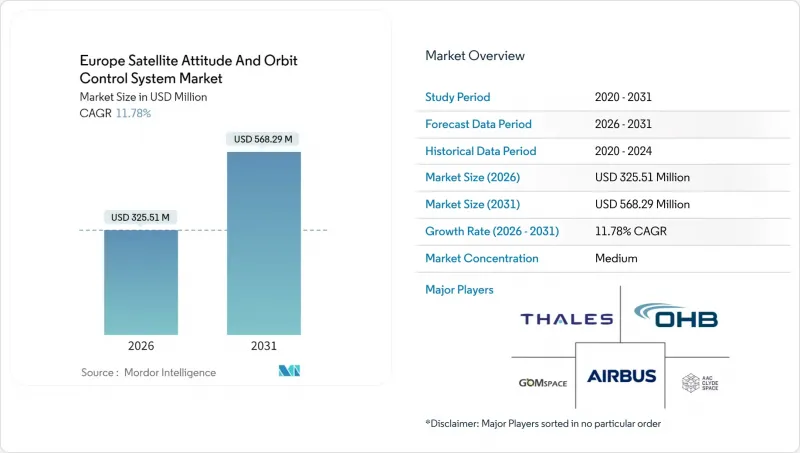

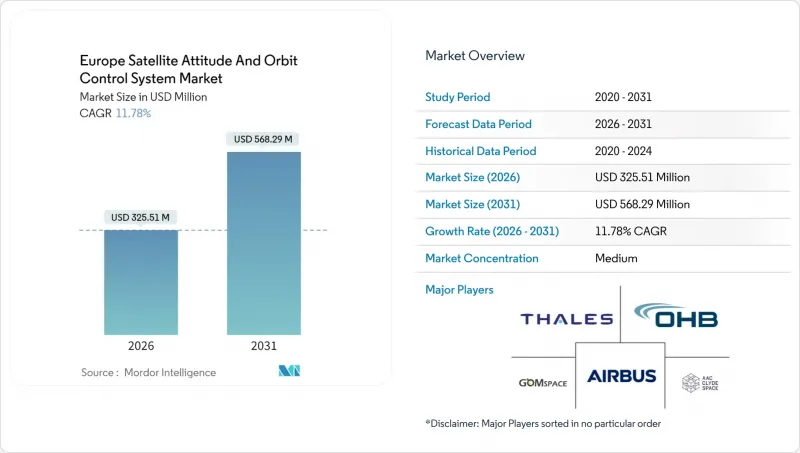

유럽의 위성 자세 및 궤도 제어 시스템(AOCS) 시장은 2025년에 2억 9,120만 달러로 평가되었고, 2026년 3억 2,551만 달러에서 2031년까지 5억 6,829만 달러에 이를 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 11.78%로 추정됩니다.

이러한 빠른 성장은 유럽연합(EU)의 IRIS2 별자리, 유럽우주국(ESA)의 자금 확대, 상용 부품(COTS) 비용의 하락, 그리고 지상국의 작업 부하를 줄여주는 AI 탑재 자율 제어 기술의 보급에 기인합니다. 상업적 최종 사용자가 가장 큰 수익원이지만, 정부가 탄력성과 전략적 자율성을 위한 이중 사용 플랫폼을 요구하면서 군용 수요도 가속화되고 있습니다. 중형 위성(100-500kg)이 물량 면에서 주류를 이루고 있는 반면, 100kg 미만의 우주선은 큐브샛 컨스텔레이션과 유럽의 신흥 마이크로 로켓이 가장 빠른 성장을 보이고 있습니다. 경쟁의 강도는 중간 정도이며, 기존 대기업들은 현재 머신러닝 알고리즘과 모듈식 하드웨어에 중점을 둔 민첩한 소프트웨어 정의형 자세 궤도 제어 시스템(AOCS) 전문 기업들과 경쟁해야 합니다. 수출 규제, 방사선 내성 시험 비용, 우주 파편 저감 규정 등이 견조한 전망을 억제하는 요인으로 작용하고 있습니다.

EU가 지원하는 IRIS2 프로그램은 2030년까지 290개의 위성을 궤도에 올려놓을 계획이며, 자세 및 궤도 제어 시스템 공급업체는 수백 대의 우주선 사이에서 원활하게 작동하는 자율 편대 비행 및 충돌 회피 기능을 제공해야 합니다. 다양한 벤더가 표준화된 AOCS 모듈을 멀티 벤더 컨스텔레이션에 통합할 수 있는 공통 소프트웨어 프레임워크가 구축되어 통합 주기를 단축하고 비용을 절감할 수 있습니다. 콘스텔레이션의 경제성을 위해 기존 고정궤도(GEO) 하드웨어보다 60-80% 저렴한 가격대에 서브미터급 지향성 정확도를 요구하고 있으며, 유럽 업체들은 모듈식 스타트락커와 확장 가능한 리액션 휠 클러스터를 채택하고 있습니다. 실시간 함대 관리는 100기가 넘는 위성군에서는 인간 운영자가 각 위성을 세밀하게 관리할 수 없기 때문에 탑재체 자율성 기준도 높이고 있습니다. 그 결과, 정확성, 경제성, AI 기반 자체 조정 기능을 결합한 플랫폼이 유럽의 위성 AOCS 시장에서 확실한 승자로 부상하고 있습니다.

ESA의 2024-2025년 예산은 17% 증가한 89억 7,000만 달러로, 양자 센서 및 AI 내비게이션 연구에 새로운 예산이 배정되어 차세대 AOCS 프로그램을 직접 지원하게 됩니다. 독일의 14억 달러 규모의 우주 계획과 프랑스의 104억 9,000만 달러 규모의 인프라 구축 계획은 2030년까지 프로토타입 비행 및 부품 인증 캠페인을 지원하여 그 추진력을 더욱 강화할 것입니다. 자금 지원 패키지는 민수용 위성과 국방용 위성이 공통의 AOCS 아키텍처를 공유하여 규모의 경제를 실현할 수 있는 이중 사용 기술에 중점을 두고 있습니다. ESA의 ARTES와 같은 협력 체계는 뉴로모픽 프로세서와 같은 실험실 개념을 궤도에 올려놓고, 공공 예산이 한정된 지역과의 혁신 격차를 확대하고 있습니다. 공급업체 입장에서는 막대한 보조금이 고가의 경상적 엔지니어링 비용을 상쇄하고, 첨단 자세 제어 솔루션 시장 출시 시간을 단축할 수 있습니다.

ITAR 및 EU의 이중 사용 규정으로 인해 기업이 자이로스코프 및 마이크로 래스터의 라이선싱을 진행함에 따라 개발 일정이 최대 25%까지 연장될 수 있습니다. 브렉시트 이후 영국 기업이 EU 파트너와 협력할 경우 별도의 허가를 받아야 하며, 거래 비용이 상승하고 공급망이 복잡해집니다. 러시아산 부품에 대한 제재로 조달처가 더욱 좁아지면서 유럽의 주요 기업들은 자국산 부품을 중심으로 레거시 플랫폼을 재설계해야 하는 상황에 처해 있습니다. 대기업은 수출관리 전문팀을 통해 컴플라이언스 비용을 흡수할 수 있지만, 중소기업은 어려움을 겪고 있으며, EU가 국내 반도체 이니셔티브를 가속화하지 않는 한 신규 진입의 모멘텀이 둔화될 수 있습니다.

유럽의 위성 자세 및 궤도 제어 시스템(AOCS) 시장에서 통신 위성은 2025년 매출의 44.45%를 차지할 것으로 예측됩니다. 이는 브로드밴드 구축과 주권적 연결성 이니셔티브에 힘입은 것입니다. 한편, 지구관측(EO) 플랫폼은 코페르니쿠스 계획의 확대와 하이퍼스펙트럼 장비의 지향성 정확도 향상을 요구하는 기후 감시 임무에 힘입어 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 9.58%의 가장 빠른 성장을 이룰 것으로 예측됩니다.

하이브리드 5G-위성 네트워크를 추구하는 컨스텔레이션 사업자는 지상 셀 사이트의 혼잡에 대응하여 빔을 재할당하기 위해 민첩한 AOCS 스택을 통합하고 있습니다. 한편, 지구관측 시스템 설계자들은 궤도 궤도의 재현성을 중요시하고 있으며, 궤도 온도 변동에 강한 고성능 스타트락커와 토크 로드 시스템에 대한 투자를 촉진하고 있습니다. 유럽의 위성 AOCS 시장은 항법, 우주과학, 우주 상황 인식(SSA) 페이로드 분야에서 견고한 기회 다양성을 유지하고 있습니다.

항법위성(주로 갈릴레오 위성군)은 원자시계의 안정성을 최우선으로 하기 때문에 반응륜에서 발생하는 미세진동을 억제하는 AOCS 서브시스템이 요구됩니다. SSA 임무는 우주 파편이나 지구 주변 천체를 추적하기 위해 신속한 재표적화가 필요하며, 몇 초 만에 큰 회전이 가능한 고토크 제어 모멘트 자이로가 필수적입니다. 다중 임무 위성으로의 전환에 따라, 공급업체는 발사 후 운영자가 전환할 수 있는 펌웨어 정의 자세 모드를 만들어야 하며, 이는 위성의 수명 기간 동안 수익성 향상 가능성을 높입니다.

100-500kg급은 페이로드 용량과 동승 경제성의 균형이 잘 맞아떨어져 2025년 유럽의 위성 AOCS 시장 매출의 46.20%를 차지할 것으로 예측됩니다. 그러나 10kg에서 100kg의 위성(주로 큐브샛)은 9.69%의 연평균 복합 성장률(CAGR)로 시장 점유율을 확대할 것으로 예상되며, 소형화 휠, 콜드 가스 스러스터, 저전력 항공 전자공학을 향한 공급업체들의 로드맵을 재구성하고 있습니다. 자동차 등급 센서를 통한 비용 절감으로 큐브샛의 보급이 가속화되고 있습니다. 그러나 초각 단위의 방향 정확도 유지가 여전히 과제로 남아 있어, 마이크로 리액션 휠의 진동 격리 기술과 저지터 통합형 스타트락커 어셈블리에 대한 연구가 추진되고 있습니다. 매스모듈러 플랫폼은 여러 위성에 미션 목표를 분산시켜 위험을 분산시키지만, 함대 규모가 커질수록 함대 관리의 복잡성이 증가하게 됩니다. 이에 대해 공급자는 수백 개의 노드에 걸친 자세 제어 작업을 조정하는 지상 부문 소프트웨어를 도입하고 AI를 활용하여 운동량 축적을 예측하고 전체 함대 전체의 운동량 덤프 스케줄을 예약하고 있습니다.

상위 모델에서는 500-1,000kg의 플랫폼이 고해상도 광학 이미저나 정밀한 열 제어가 필요한 과학 장비에 대응합니다. 이러한 미션은 수익률이 높은 반면 점유율이 작기 때문에 광학 자이로스코프, 자기 베어링식 리액션 휠과 같은 유럽산 고급 AOCS 부품에 대한 수요가 지속될 것입니다.

유럽의 위성 자세 궤도 제어 시스템 시장 보고서는 용도별(통신, 지구관측, 항법, 우주 관측, 기타), 위성 질량별(10kg 미만, 10-100kg, 100kg 이상), 궤도 등급별(정지궤도, 저궤도, 중궤도), 최종사용자별(상업용, 군사/정부, 기타), 지역별(영국, 프랑스, 기타)로 분석됩니다. 프랑스, 기타) 별로 분석되고 있습니다. 시장 예측은 금액 기준(달러)으로 제공되며, 시장 예측은

The Europe satellite attitude and orbit control system (AOCS) market was valued at USD 291.20 million in 2025 and estimated to grow from USD 325.51 million in 2026 to reach USD 568.29 million by 2031, at a CAGR of 11.78% during the forecast period (2026-2031).

Rapid growth springs from the European Union's IRIS2 constellation, expanded European Space Agency (ESA) funding, falling commercial-off-the-shelf (COTS) component costs, and the spread of AI-enabled autonomous control that trims ground-station workloads. Commercial end-users remain the biggest revenue driver, yet military demand is accelerating as governments seek dual-use platforms for resilience and strategic autonomy. Mid-range 100 to 500 kg satellites dominate volumes, while sub-100 kg spacecraft post the fastest growth thanks to CubeSat constellations and Europe's emerging microlaunchers. Competitive intensity is moderate; traditional primes must now compete with nimble software-defined AOCS specialists focusing on machine-learning algorithms and modular hardware. Export controls, radiation-qualification costs, and debris-mitigation rules temper the otherwise robust outlook.

The EU-backed IRIS2 program will place 290 satellites in orbit by 2030, compelling attitude-and-orbit-control suppliers to deliver autonomous formation-flying and collision-avoidance capabilities that operate seamlessly across hundreds of spacecraft. is building common software frameworks that let different manufacturers plug standardized AOCS modules into multi-vendor constellations, shortening integration cycles and lowering costs. Constellation economics demand sub-meter pointing accuracy at price points 60-80% below legacy GEO hardware, pushing European vendors to adopt modular star trackers and scalable reaction-wheel clusters. Real-time fleet management also raises the bar for onboard autonomy, since human operators cannot micromanage every satellite in flocks that exceed 100 nodes. As a result, platforms combining precision, affordability, and AI-driven self-coordination are emerging as clear winners within the European satellite AOCS market.

ESA's 2024-2025 budget rose 17% to USD 8.97 billion, with fresh allocations for quantum sensors and AI-navigation research directly supporting next-generation AOCS programs. Germany's USD 1.4 billion space plan and France's USD 10.49 billion infrastructure push reinforce that momentum, underwriting prototype flights and component-qualification campaigns through 2030. Funding packages emphasize dual-use technology, ensuring that civil and defense satellites can share common AOCS architectures for economies of scale. Cooperative schemes like ESA's ARTES speed laboratory concepts like neuromorphic processors into orbit, widening Europe's innovation gap versus regions with narrower public budgets. For suppliers, generous grants offset high non-recurring engineering costs, accelerating time to market for advanced attitude-control solutions.

ITAR and EU dual-use regulations extend development schedules by up to 25% as companies navigate licensing for gyroscopes and micro-thrusters. Post-Brexit, United Kingdom firms must secure separate clearances when collaborating with EU partners, hiking transaction costs and complicating supply chains. Sanctions on Russian components further squeeze sourcing, pushing European primes to reengineer legacy platforms around indigenous parts. Larger firms absorb compliance overhead through dedicated export-control teams, but small and medium enterprises struggle, which could slow new-entrant momentum unless the EU accelerates domestic semiconductor initiatives.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Communication satellites delivered 44.45% of 2025 revenue within the European satellite AOCS market, supported by broadband rollouts and sovereign connectivity initiatives. EO platforms, however, post the fastest 2026-2031 advance at 9.58% CAGR, propelled by Copernicus expansion and climate-monitoring missions that demand tighter pointing accuracy for hyperspectral instruments.

Constellation operators pursuing hybrid 5G-satellite networks now embed agile AOCS stacks to reassign beams in response to terrestrial cell-site congestion. Conversely, Earth-observation designers emphasize coordinated ground-track repeatability, prompting investment in high-performance star trackers and torque-rod systems resilient to orbital temperature swings. The European satellite AOCS market maintains robust opportunity diversity across navigation, space-science, and space-situational-awareness (SSA) payloads.

Navigation spacecraft, chiefly the Galileo constellation, prioritize atomic-clock stability, demanding AOCS subsystems to damp micro-vibrations from reaction wheels. SSA missions rely on rapid retargeting to track debris or near-Earth objects, necessitating high-torque control-moment gyros capable of large slews in seconds. The shift towards multi-mission satellites pressures suppliers to create firmware-defined attitude modes that operators can toggle post-launch, enhancing revenue potential throughout the satellite's lifespan.

The 100 to 500 kg class generated 46.20% of 2025 revenue in the Europe satellite AOCS market, favored for its balance of payload capacity and rideshare economics. Yet units between 10 kg and 100 kg, mostly CubeSats, are projected to capture an incremental 9.69% CAGR, reshaping supplier roadmaps toward miniaturized wheels, cold-gas thrusters, and low-power avionics. Affordability gains through automotive-grade sensors accelerate the CubeSat curve. However, maintaining arc-second pointing remains a hurdle, motivating research into micro-reaction wheel vibration isolation and low-jitter integrated star-tracker assemblies. Mass-modular platforms diversify risk by distributing mission objectives across multiple satellites; however, scaling fleets introduces fleet-management complexity. Providers respond with ground-segment software that orchestrates attitude tasks across hundreds of nodes, applying AI to predict momentum buildup and schedule momentum dumps fleet-wide.

At the upper end, 500 to 1,000 kg platforms cater to high-resolution optical imagers and scientific instruments requiring precise thermal control. These missions command premium margins while representing a smaller share, ensuring continued demand for high-end European AOCS components such as optical gyroscopes and magnetic-bearing reaction wheels.

The Europe Satellite Attitude and Orbit Control System Market Report is Segmented by Application (Communication, Earth Observation, Navigation, Space Observation, and Others), Satellite Mass (Below 10 Kg, 10 To 100 Kg, and More), Orbit Class (GEO, LEO, and MEO), End User (Commercial, Military and Government, and Other), and Geography (United Kingdom, France, and More). The Market Forecasts are Provided in Terms of Value (USD),