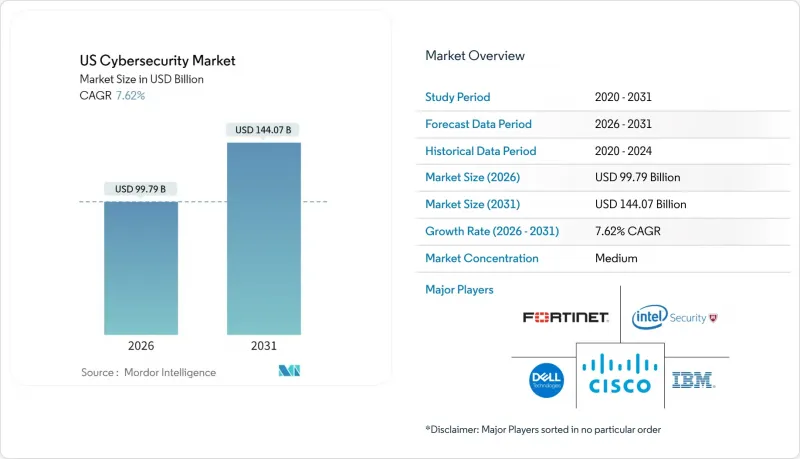

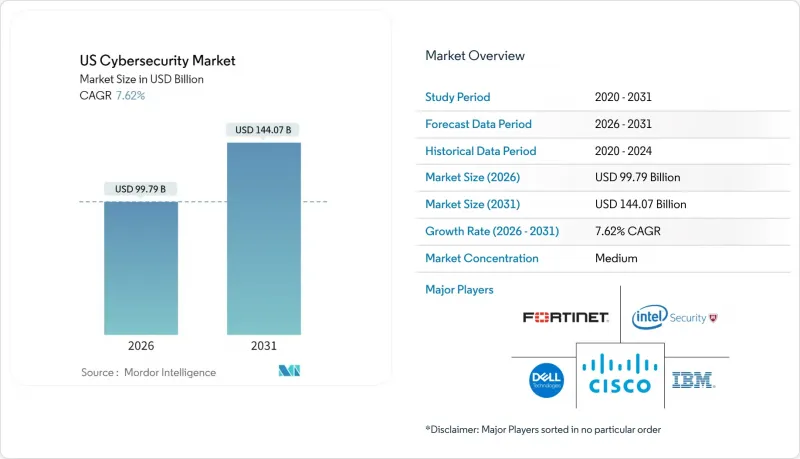

미국의 사이버 보안 시장은 2025년 927억 3,000만 달러에서 2026년에는 997억 9,000만 달러로 성장하여 2026년부터 2031년까지 CAGR 7.62%를 기록하며 2031년까지 1,440억 7,000만 달러에 달할 것으로 예측됩니다.

이러한 확대는 연방 정부의 제로 트러스트 의무화, 중요 인프라에 대한 랜섬웨어 공격의 급증, 그리고 현재 94%의 조직이 멀티 클라우드 환경을 채택한 클라우드 마이그레이션의 가속화로 인해 가속화되고 있습니다. 국방, 금융 서비스, 의료 분야의 사업자들은 로컬에서 관리해야 하는 레거시 시스템을 유지하고 있기 때문에 온프레미스형 아키텍처가 여전히 가장 큰 도입 점유율을 차지하고 있습니다. 그러나 기업이 확장 가능한 보호와 실시간 위협 인텔리전스를 요구함에 따라 클라우드 기반 보안은 15%의 CAGR로 계속 성장하고 있습니다. 벤처 캐피털은 계속해서 혁신을 촉진하고 있으며, 2024년 미국 사이버 보안 스타트업에 116억 달러가 투자되었습니다. 그 중 상당 부분은 분석가의 업무 부담을 덜어주는 AI 기반 위협 탐지 플랫폼에 투입되고 있습니다. 미국 증권거래위원회(SEC)의 의무적인 정보 유출 공개 규정, 상승하는 사이버 보험 보험료, 그리고 지속적인 인력 부족이 결합되어 장기적인 수요를 강화하고 있으며, 미국 사이버 보안 시장은 민관 모두의 전략적 우선 순위로 자리매김하고 있습니다.

대통령령 14028호에 따라 모든 민간 기관은 제로 트러스트 아키텍처를 의무적으로 채택해야 하며, 주정부와 지방 정부로 파급되는 다년간의 현대화 프로젝트가 시작되었습니다. 최근 국토안보부는 ASRC Federal에 1,700만 달러의 USCIS 통합 서비스를 제공하기로 결정했으며, 재무부의 새로운 200억 달러 규모의 PROTECTS 프로그램은 연방정부의 구매력을 보여주고 있습니다. 23개 주에서 제로 트러스트 로드맵을 발표했으며, 캘리포니아주는 2026년까지 모든 기관에서 ID 중심 관리를 실현하기 위해 5,000만 달러를 책정했습니다. 계약자들도 이를 따라 국방 및 금융 서비스 공급망 깊숙한 곳까지 제로 트러스트 요건을 확대해야 합니다. 이러한 연쇄효과로 인해 미국 사이버 보안 시장은 지속적인 공공부문 지출의 최대 수혜자로 자리매김하고 있습니다.

2024년 2월 체인지 헬스케어(Change Healthcare)의 정보 유출 사건으로 67,000개 약국에서 처방전 처리가 중단되었고, 유나이티드 헬스 그룹은 23억 달러의 복구 비용을 지불해야 했습니다. 어센션 헬스(Ascension Health)도 3개월 후 비슷한 혼란을 겪었고, 랜섬웨어 공격으로 인해 140개 병원의 전자건강기록 시스템이 마비되었습니다. 보건복지부는 지난해 1억 건의 환자 기록이 유출된 것을 확인했으며, 병원의 방어체계 현대화를 요구하는 연방정부의 압력을 강화하고 있습니다. 교육기관도 마찬가지로 취약하며, FBI는 학생 서비스 데이터베이스를 지운 랜섬웨어로 인해 여러 캠퍼스가 폐쇄되었다고 보고했습니다. 이러한 사건들은 지출의 시급성을 증폭시켜 의료 보안 지출은 CAGR 14.6%로 예측되며, 미국 전체 사이버 보안 시장의 성장 궤도를 크게 상회할 것으로 예상됩니다.

캘리포니아주 CCPA, 버지니아주 CDPA, 코네티컷주 CTDPA는 각기 다른 정보 유출 통지 의무와 소비자 권리 요건을 부과하고 있어, 벤더는 각 주별 컴플라이언스 체제를 유지해야 합니다. SEC가 개정한 Regulation S-P는 금융기관이 데이터 침해 발생 후 30일 이내에 개인에게 통지하도록 의무화하고 있으며, 이는 더 엄격한 주정부의 기한과 중복됩니다. 중견 보안업체들은 연간 평균 230만 달러의 컴플라이언스 비용을 보고하고 있으며, 이는 수익률을 압박하고 시장 진입을 가로막는 요인으로 작용하고 있습니다. 규제 단편화로 인해 제품 출시가 지연되고 시장 출시 계획이 복잡해져 미국 사이버 보안 시장의 연평균 성장률(CAGR)이 약 1.2%포인트 하락할 것으로 예상됩니다.

솔루션은 주요 수익원이며, 2025년 미국 사이버 보안 시장 점유율의 67.30%를 차지했습니다. 한편, 매니지드 서비스는 2031년까지 CAGR 15.1%로 확대될 것으로 예상됩니다. 연방 정부의 제로 트러스트 지침 이후 ID 및 액세스 관리 도입이 급증했고, 컨테이너화된 개발 파이프라인의 확산과 함께 애플리케이션 보안 지출이 증가했습니다. 네트워크 보안 어플라이언스는 소프트웨어 정의형 대체품으로 대체되고 있으며, 엔드포인트 보호는 노트북, 서버, 모바일 기기의 원격 측정 정보를 수집하는 XDR 제품군으로 진화하고 있습니다. 클라우드 보안의 하위 카테고리, 특히 클라우드 네이티브 애플리케이션 보호 플랫폼(CNAPP)은 기존 도구로는 대응할 수 없는 멀티 클라우드 환경의 복잡성을 반영하여 가장 빠른 성장세를 보이고 있습니다. 전문 서비스는 컴플라이언스 감사 및 사고 대응 분야에서 견고한 틈새 시장을 유지하고 있지만, 인력 부족으로 인해 대응 능력이 제한되어 청구 단가가 상승하고 있습니다.

매니지드 서비스의 성장은 심각한 인력 부족과 규제 압력으로 인해 자원이 풍부한 기업조차도 외부의 전문성을 요구하고 있는 상황입니다. MSSP(Managed Security Service Provider)는 보안관제센터(SOC) 기능을 서브스크립션 형태로 제공하는 사례가 증가하면서 중견기업의 진입장벽을 낮추고 있습니다. 제공 컨텐츠의 구성은 도구의 난립으로 인한 피로감에도 영향을 받고 있습니다. 대기업의 90%가 중복된 취약점 스캐너를 운영하고 있으며, 이를 통합 플랫폼으로 통합하려고 합니다. 벤더들은 AI 분석 기능과 오케스트레이션 기능을 접목하여 대응하고 있으며, 솔루션의 정착성을 강화하는 동시에 고객 1인당 평균 수익을 확대하고 있습니다. 그 결과, 솔루션은 규모를 유지하면서 서비스가 미국 사이버 보안 시장 전체에 높은 성장 속도를 가져오고 있습니다.

2025년 기준 온프레미스 환경이 매출의 57.20%를 차지했으며, 그 주요 요인은 국방, 금융 서비스, 의료 분야에서 데이터 주권 및 레거시 통합 유지가 필수적이기 때문입니다. 연방 정부 기관은 에어갭 환경에서 기밀 네트워크를 계속 유지하고 있지만, 분석 계층은 상업용 클라우드로의 전환이 진행되고 있습니다. JP모건 체이스(JP Morgan Chase)와 같은 금융기관은 온프레미스 키 관리와 클라우드 네이티브 탐지 기능을 결합한 하이브리드 아키텍처에 투자하여 민첩성을 유지하면서 규제 준수를 보장하고 있습니다.

클라우드 기반 보안 솔루션은 자본 지출 감소, 탄력적인 확장성, SaaS(Software as a Service) 도입 가속화에 힘입어 14.4%의 CAGR로 성장했습니다. SECaaS를 도입한 조직은 어플라이언스 기반 대안에 비해 구현 주기를 40% 단축하고, 위험 감소까지 걸리는 시간을 단축할 수 있습니다. 위협 인텔리전스 피드와 행동 분석을 통합하여 진화하는 공격자 기법에 맞춰 지속적으로 업데이트되는 제어 플레인을 제공합니다. 이러한 성장 격차는 시간이 지남에 따라 수익 격차를 확대시키고 있으며, 규제가 엄격한 산업에서 절대적인 지출이 안정적임에도 불구하고 미국 사이버 보안 시장에서 온프레미스 분야의 점유율은 상대적으로 줄어들고 있습니다.

The US cybersecurity market is expected to grow from USD 92.73 billion in 2025 to USD 99.79 billion in 2026 and is forecast to reach USD 144.07 billion by 2031 at 7.62% CAGR over 2026-2031.

This expansion is fueled by federal zero-trust mandates, a sharp increase in ransomware attacks on critical infrastructure, and accelerated cloud migration that now places 94% of organizations in multi-cloud settings . On-premise architectures still hold the largest deployment footprint because defense, financial services, and healthcare operators retain legacy systems that must remain behind local controls; however, cloud-delivered security is advancing at a 15% CAGR as enterprises seek scalable protection and real-time threat intelligence. Venture capital continues to stimulate innovation, with USD 11.6 billion invested in US cyber start-ups during 2024, much of it channeled into AI-driven threat-detection platforms that reduce analyst workload. Mandatory SEC breach-disclosure rules, rising cyber-insurance premiums, and a persistent talent shortage collectively reinforce long-term demand, positioning the US cybersecurity market as a strategic priority for both public and private sectors.

Executive Order 14028 obliges every civilian agency to adopt zero-trust architecture, triggering multi-year modernization projects that ripple through state and local governments. The Department of Homeland Security recently awarded USD 17 million to ASRC Federal for USCIS integration services, and the Treasury's new USD 20 billion PROTECTS vehicle underscores federal buying power. Twenty-three states have published their zero-trust roadmaps, with California allocating USD 50 million for identity-centric controls across all agencies by 2026. Contractors must follow suit, extending zero-trust requirements deep into defense and financial services supply chains. The cascade effect positions the US cybersecurity market as the primary beneficiary of sustained public-sector spending.

Change Healthcare's February 2024 breach halted prescription processing for 67,000 pharmacies and cost UnitedHealth Group USD 2.3 billion in remediation. Ascension Health faced a similar disruption three months later when a ransomware attack paralyzed electronic health-record systems across 140 hospitals. The Department of Health and Human Services confirmed that 100 million patient records were exposed last year, fueling federal pressure on hospitals to modernize defenses. Educational institutions are equally vulnerable; the FBI attributes multiple campus closures to ransomware that erased student-services databases. These events amplify spending urgency, pushing healthcare security outlays to an expected 14.6% CAGR, well above the overall US cybersecurity market trajectory.

CCPA in California, CDPA in Virginia, and CTDPA in Connecticut impose divergent breach-notification and consumer-rights requirements that force vendors to maintain state-specific compliance frameworks. The SEC's amended Regulation S-P now obliges financial institutions to notify individuals within 30 days of a data compromise, overlapping with stricter state deadlines. Mid-market security providers report average annual compliance costs of USD 2.3 million, eroding margins, and deterring market entry. Fragmentation slows product rollouts and complicates go-to-market planning, shaving an estimated 1.2 percentage points from the US cybersecurity market CAGR.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solutions remain the primary revenue driver, holding 67.30% of the US cybersecurity market share in 2025, while managed services are forecast to grow at a 15.1% CAGR through 2031. Identity and access management adoption surged after federal zero-trust directives, and application security spending expanded alongside containerized development pipelines. Network security appliances face displacement from software-defined alternatives, whereas endpoint protection evolves toward XDR suites that ingest telemetry from laptops, servers and mobile devices. Cloud-security subcategories-particularly cloud-native application protection platforms (CNAPP)-post the fastest acceleration, reflecting multi-cloud complexity that legacy tools cannot address. Professional services hold a resilient niche in compliance audits and incident response, though the labor shortage constrains capacity and pushes billable rates higher.

Managed services growth stems from acute talent constraints and regulatory pressures that force even resource-rich enterprises to seek external expertise. MSSPs increasingly deliver security-operations-centre (SOC) functions via subscription, lowering entry thresholds for mid-market businesses. The offering mix is also shaped by tool-sprawl fatigue: 90% of large organizations run overlapping vulnerability scanners that they now seek to consolidate into integrated platforms. Vendors respond by embedding AI analytics and orchestration features, reinforcing solution stickiness and expanding average revenue per customer. Consequently, solutions retain scale, while services inject higher growth velocity into the overall US cybersecurity market.

On-premises setups accounted for 57.20% of revenue in 2025, largely because defence, financial-services and healthcare sectors must preserve data sovereignty and legacy integrations. Federal agencies continue to maintain classified networks behind air-gapped environments, although analytics layers increasingly migrate to commercial clouds. Financial institutions such as JPMorgan Chase invest in hybrid architecture that combines on-premises key-management with cloud-native detection, ensuring regulatory compliance without sacrificing agility.

Cloud-delivered security solutions expanded at a 14.4% CAGR, buoyed by reduced capital spending, elastic scaling and the speed of software-as-a-service rollouts. Organizations deploying SECaaS report implementation cycles 40% shorter than appliance-based alternatives, accelerating time to risk reduction. Providers integrate threat-intelligence feeds and behavioral analytics, delivering a continuously updated control plane that adapts to evolving attacker techniques. The growth differential widens the revenue gap over time, causing the on-premises slice of the US cybersecurity market to contract in relative terms, even as absolute spending remains stable in compliance-heavy industries.

The US Cybersecurity Market Report Segments the Industry Into Offering (Solutions, Services), by Deployment Mode (Cloud, and On-Premise), by Organization Size (SMEs, and Large Enterprises), by End User (BFSI, Healthcare, and More). The Market Forecasts are Provided in Terms of Value (USD).