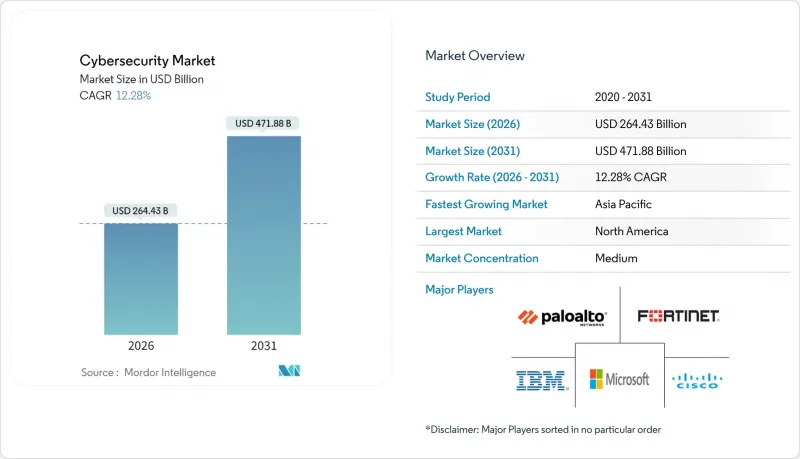

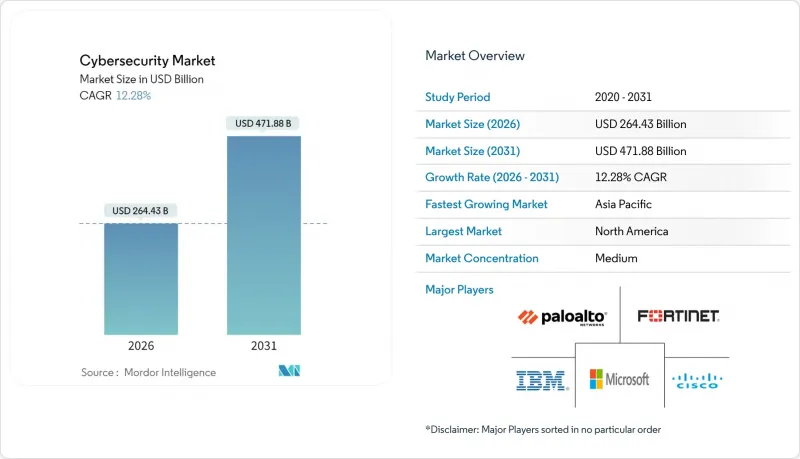

2026년 사이버 보안 시장 규모는 2,644억 3,000만 달러로 추정되며, 2025년 2,355억 달러에서 성장이 전망됩니다. 2031년의 예측에서는 4,718억 8,000만 달러에 달하며, 2026-2031년에 CAGR 12.28%로 확대할 전망입니다.

이러한 확장의 주요 요인은 제로 트러스트 아키텍처에 대한 지출 증가, IT와 운영 기술(OT)의 방어적 통합, 양자 내성 암호화에 대한 준비 등입니다. 북미가 지출 측면에서 선두를 유지한 반면, 아시아태평양은 기업이 워크로드를 클라우드 우선 환경으로 전환함에 따라 가장 빠른 성장세를 보이고 있습니다. 또한 사이버 보험 인수업체들이 검증 가능한 관리 방안을 요구하면서 예산 배분도 증가하고 있으며, 모니터링을 간소화하는 통합 보안 플랫폼으로의 전환을 촉구하고 있습니다. 동시에 각 벤더들이 새로운 위협 벡터에 대응하기 위해 경쟁하는 가운데, 인수합병을 통한 플랫폼 통합 움직임도 활발히 일어나고 있습니다.

클라우드 마이그레이션은 분산 환경에서 경계 제어가 작동하지 않기 때문에 보안 투자의 우선순위를 재구성하고 있습니다. 클라우드 배포는 계속 확대되고 있으며, On-Premise 환경의 할당량을 초과하여 아이덴티티, 워크로드, 데이터 보호 기능을 통합하는 클라우드 네이티브 애플리케이션 보호 플랫폼에 대한 수요를 주도하고 있습니다. 기업은 툴의 난립을 줄일 수 있는 통합 콘솔을 원하고 있으며, 벤더들은 하이브리드 환경 전반에서 텔레메트리를 상호 연관시키는 플랫폼을 제공함으로써 가시성과 대응 효율을 향상시키고자 합니다.

인더스트리 4.0의 발전으로 인해 기존 에어갭으로 보호되던 시스템이 온라인화되면서 레거시 제어 네트워크가 IT 자산을 노리는 동일한 공격자에게 노출되고 있습니다. 이로 인해 사이버 보안 시장에서 수요가 증가하고 있습니다. ISA/IEC 62443과 같은 규제 프레임워크는 생산 현장에서 데이터센터까지 아우르는 통합 방어를 의무화하고 있으며, 전문적인 OT 위협 감지 및 세분화 툴에 대한 투자를 촉진하고 있습니다. 국가 차원의 공격 주체가 전력망의 취약점을 탐색하는 가운데, 에너지 사업자가 도입을 주도하고 있으며, OT 특화형 보안 대책의 위험 감소 효과는 동급 IT 프로젝트 대비 투자 대비 효과를 가져오고 있습니다.

클라우드, OT, AI 기반 방어와 같은 희소성 있는 기술에 대한 급여 상승과 함께 340만 명의 전문가 부족으로 인해 예산이 압박을 받고 있습니다. 이러한 제약은 운영 인력이 적은 플랫폼으로 시장 통합을 촉진하는 동시에, 관리형 보안 서비스 및 AI 기반 자동화 툴을 제공하는 벤더들에게 기회를 제공합니다. 이러한 상황은 높은 이직률로 인해 더욱 악화되고 있으며, 사이버 보안 전문가의 64%가 업무 스트레스로 인해 이직을 고려하고 있습니다. 이로 인해 조직의 보안 예산에 영향을 미치는 채용 및 교육 비용의 지속적인 사이클이 발생하고 있습니다.

북미는 성숙한 규제 환경과 주요 벤더의 존재로 인해 2025년 사이버 보안 시장 매출의 43.20%를 차지할 것으로 예측됩니다. 대통령령 14028호에 따라 광범위한 제로 트러스트 전환이 의무화됨에 따라 이 지역의 지출은 2027년까지 1,376억 달러 이상에 달할 것으로 예측됩니다. 미국에서는 2023년 9,036건의 사이버 사고가 발생해 유럽의 2,557건을 크게 웃돌았습니다. 이로 인해 고급 위협 인텔리전스 피드와 매니지드 SOC 서비스에 대한 수요가 지속되고 있습니다. 캐나다와 멕시코는 국경 간 침해 보고와 사고 대응을 조화시키는 민관 합동 프로그램을 통해 성장에 기여하고 있습니다.

아시아태평양은 16.85%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하고 있으며, 국가 주도의 디지털 국가 계획으로 인해 보안이 핵심 인프라의 지위로 격상되고 있습니다. 중국, 인도, 일본, 한국은 국가 사이버 전략에 다년간의 예산을 배정하고 있으며, 호주 및 뉴질랜드는 사고 공개를 의무화하는 종합적인 복원력 프레임워크를 시행하고 있습니다. 지역 구매자들은 초기부터 클라우드 네이티브 보안을 채택함으로써 기존의 제어를 뛰어넘어 아이덴티티 중심 및 AI 기반 분석의 도입을 가속화하고 있습니다.

유럽의 성장은 GDPR(EU 개인정보보호규정)의 시행과 더 많은 분야로의 적용 범위 확대를 규정한 NIS2 지침의 시행에 의해 촉진되고 있습니다. 독일, 영국, 프랑스가 지출을 주도하는 반면, 중동부 유럽 시장은 EU 요건을 충족하면서 소규모 기반에서 성장하고 있습니다. 프랑스와 스페인의 소버린 클라우드 구상은 국내 호스팅 보안 스택에 대한 수요를 자극하고, 국경 간 데이터 전송 제한은 프라이버시 강화 암호화 기술 채택을 가속화하고 있습니다.

Cybersecurity Market size in 2026 is estimated at USD 264.43 billion, growing from 2025 value of USD 235.5 billion with 2031 projections showing USD 471.88 billion, growing at 12.28% CAGR over 2026-2031.

Increased spending on zero-trust architectures, the integration of IT and operational technology (OT) defenses, and preparations for quantum-ready encryption are the primary forces behind this expansion. North America retains spending leadership, while Asia-Pacific registers the most rapid gains as enterprises migrate workloads to cloud-first environments. Budget allocations are also rising as cyber-insurance underwriters demand verifiable controls, pushing organizations toward unified security platforms that simplify oversight. Simultaneously, platform consolidation through mergers and acquisitions is intensifying as vendors race to cover emerging threat vectors.

Cloud migration is reshaping security investment priorities as perimeter controls fail in distributed environments. Cloud deployment is growing, outpacing on-premise allocations and driving demand for cloud-native application protection platforms that integrate identity, workload, and data safeguards. Enterprises are seeking unified consoles to reduce tool sprawl, and vendors are responding with platforms that correlate telemetry across hybrid estates, improving visibility and response efficiency .

Industry 4.0 forces formerly air-gapped systems online, exposing legacy control networks to the same adversaries that target IT assets, driving heightened demand in the cybersecurity market. Regulatory frameworks such as ISA/IEC 62443 now require integrated defenses that span production floors and data centers, encouraging investment in specialized OT threat detection and segmentation tools. Energy utilities are leading adoption as nation-state actors probe grid vulnerabilities, and returns on OT-focused security initiatives now exceed comparable IT projects in risk-reduction value.

The shortfall of 3.4 million professionals strains budgets as salaries climb for scarce skills in cloud, OT, and AI-driven defense. This constraint is driving market consolidation toward platforms that require fewer specialized personnel to operate, while simultaneously creating opportunities for vendors offering managed security services and AI-powered automation tools. The situation is exacerbated by high turnover rates, with 64% of cybersecurity professionals considering job changes due to workload stress, creating a continuous cycle of recruitment and training costs that impact organizational security budgets .

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

North America controlled 43.20% of 2025 revenue in the cybersecurity market, underpinned by mature regulations and the presence of major vendors. Regional spending is forecast to surpass USD 137.6 billion by 2027 as Executive Order 14028 obliges extensive zero-trust migration. The United States reported 9,036 cyber incidents in 2023, dwarfing Europe's 2,557 events and sustaining demand for advanced threat intelligence feeds and managed SOC services. Canada and Mexico contribute to growth through joint public-private programs that harmonise cross-border breach reporting and incident response.

Asia-Pacific is the fastest-growing area at 16.85% CAGR, with state-backed digital-nation plans elevating security to critical-infrastructure status. China, India, Japan, and South Korea allocate multi-year budgets to national cyber strategies, while Australia and New Zealand implement comprehensive resilience frameworks that require mandatory incident disclosure. Regional buyers often leapfrog legacy controls by adopting cloud-native security from the outset, accelerating uptake of identity-centric and AI-driven analytics.

Europe region growth is propelled by GDPR enforcement and the forthcoming NIS2 directive that expands coverage to more sectors. Germany, the United Kingdom, and France headline spending, whereas Central and Eastern European markets grow from a smaller base as they align with EU requirements. Sovereign-cloud initiatives in France and Spain stimulate demand for domestically hosted security stacks, while cross-border data-transfer restrictions accelerate adoption of privacy-enhancing encryption techniques.