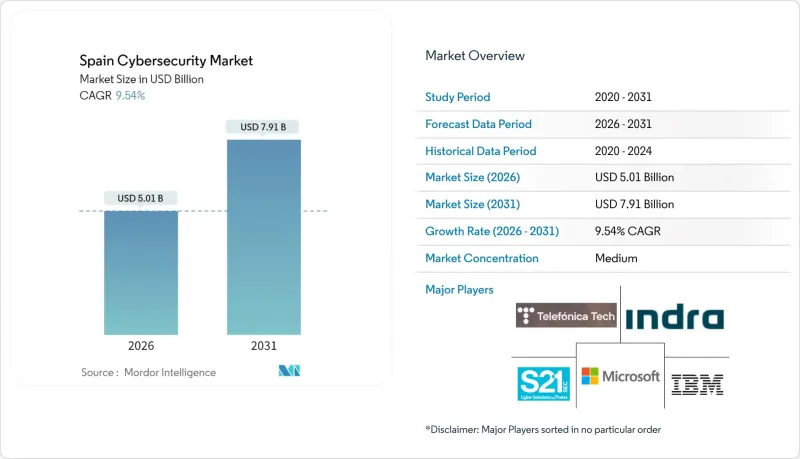

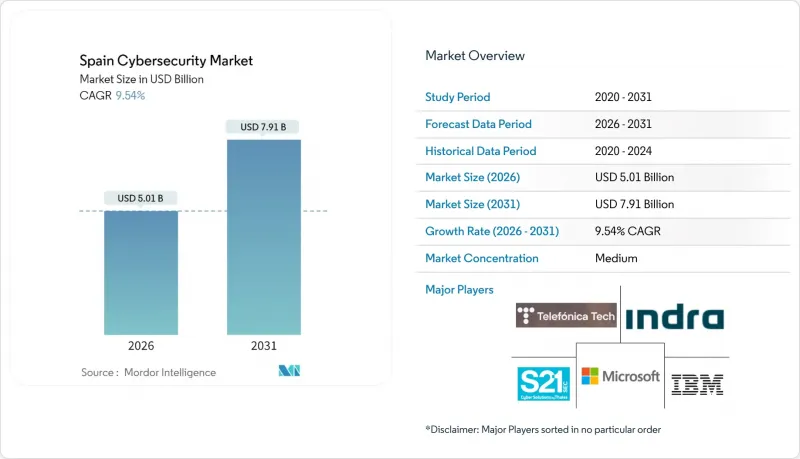

스페인의 사이버 보안 시장은 2025년 45억 7,000만 달러에서 2026년에는 50억 1,000만 달러에 이르고, 2026-2031년 CAGR 9.54%로 성장을 지속하여 2031년까지 79억 1,000만 달러에 달할 것으로 예측됩니다.

스페인이 대륙 차원의 사이버 보안 거점으로서의 입지를 구축하려는 정책과 함께 급증하는 랜섬웨어 활동과 EU 차원의 엄격한 규제가 결합되어 클라우드 기반 보호, 관리형 감지, 양자 내성 암호화 솔루션에 대한 지속적인 지출을 촉진하고 있습니다. 12억 유로 규모의 국가 사이버 보안 전략, 디지털 스페인 2026 로드맵, CorA 클라우드 마이그레이션 계획 등 공공 부문 프로그램은 벤더의 국내 시장 규모를 확대하고 있습니다. 5G의 급속한 전개, 관광 중심의 현금 없는 소매, 산업 디지털화의 진전은 공격 대상 영역을 더욱 확대할 것이며, 기업은 보안 오케스트레이션과 사고 대응 아웃소싱을 우선순위에 둘 수밖에 없습니다. 중소기업의 인력 부족과 예산 제약이 역풍으로 작용하는 반면, 스페인의 활기찬 스타트업 생태계와 타겟팅된 공공 보조금은 스페인의 사이버 보안 시장에 외국 자본과 기술 제휴를 계속 끌어들이고 있습니다.

정부는 2025년까지 GDP의 2%를 안보 및 국방에 투자할 방침이며, 이 중 31.16%를 통신 및 사이버 역량 강화에 할당할 예정입니다. 이로 인해 발생한 12억 유로의 자금은 양자 내성 암호 시범 사업, 대규모 SOC(보안 운영 센터) 업그레이드, 그리고 스페인을 세계 5위권의 사이버 혁신 국가로 끌어올리기 위한 인재 육성 프로그램에 사용됩니다. 스페인 은행들은 이미 기술 지출을 두 배로 늘리고 있으며, 이는 스페인의 사이버 보안 시장에서 네트워크 보안 및 IAM(ID 관리) 계약의 동시 급증을 촉진하고 있습니다.

'디지털 스페인 2026'은 50만 명의 노동자 기술 향상을 목표로 보안 도입 비용을 보조하는 보조금을 지급하고 있지만, 현재 공격의 70%가 중소기업을 표적으로 삼고 있어 기본 대책의 취약성을 드러내고 있습니다. Kit Digital의 보조금 지원으로 10-49인 기업용 엔터프라이즈급 방화벽 및 MDR 구독에 대한 자금 조달이 가능해짐에 따라, 벤더들은 가볍고 자동화된 솔루션에 집중할 수 있게 되었습니다. 이를 통해 스페인의 사이버 보안 시장에 새로운 수익 기반이 창출되고 있습니다.

INCIBE의 추정에 따르면, 스페인은 2025년에 99,600명의 전문가가 필요하며, 이는 전년도 83,000명의 부족분보다 증가한 수치입니다. 특히 포스트 양자암호기술과 AI를 활용한 위협 헌팅 스킬이 부족해 기업들은 24시간 365일 가동되는 SOC를 운영하는 현지 MSSP에 모니터링 업무를 외주화할 수밖에 없는 실정입니다. INCIBE와 Digital Spain 프로그램이 무료 교육 과정을 제공하고 있지만, 인력 공급은 여전히 부족하여 스페인의 사이버 보안 시장 전체에서 사내 도입 속도를 억제하고 있습니다.

솔루션은 2025년 매출의 69.12%를 차지하며, 조직이 NGFW, EDR, IAM과 같은 핵심 방어를 강화하는 가운데 스페인의 사이버 보안 시장의 근간을 이루고 있습니다. NIS2 지침 준수가 기업의 용도 보안 지출을 촉진하는 한편, 자치주 기관은 ENS를 준수하는 클라우드 제어를 우선시하고 있습니다. 가장 빠르게 성장하고 있는 매니지드 서비스 부문은 기술력 부족에 대응하기 위해 원격 SOC 기능을 제공하여 평균 감지 시간을 48% 단축하고 있습니다. 텔레포니카 테크는 현재 스페인 고객을 위해 하루 4,000건 이상의 클라우드 경보를 분석하고 있으며, 이는 스페인의 사이버 보안 시장에서 국내 업체가 현지 전문성을 경쟁 우위의 차별화 요소로 전환하고 있는 사례입니다.

전문 서비스에 대한 수요는 ENS 감사 및 NIS2 대응을 중심으로 지속되고 있습니다. 에너지 사업자는 2024년 공격이 43% 증가함에 따라 인드라의 컨설턴트에게 OT 세분화 재설계를 의뢰했습니다. 한편, 스타트업 기업들은 온보딩과 정책 설정을 자동화하여 중소기업의 도입을 효율화하고 있습니다. 하이엔드 매니지드 서비스와 셀프 서비스 SaaS의 두 가지 궤적은 서비스 수익이 가속화되는 가운데 솔루션을 계속 주도하고 있으며, 스페인의 전체 사이버 보안 시장 규모 전망을 강화하고 있습니다.

클라우드 도입은 2025년 매출의 62.18%를 차지하며 13.12%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. CorA 지침, 멀티 클라우드 전략, 주권 호스팅 요구 사항으로 인해 정부 기관과 은행은 아이덴티티를 새로운 경계로 취급해야 할 필요성이 대두되고 있습니다. ENS '알트' 인증은 벤더의 최소 기준 자격으로 진입 장벽을 높이고, 준수하는 공급업체에 대한 지출 집중을 촉진하고 있습니다. 국방 기관과 주요 공공 기관에서는 On-Premise 제어가 계속될 것이지만, 대기업 로드맵에서는 하이브리드 구성이 주류가 될 것이며, 스페인의 사이버 보안 시장에서 SaaS, IaaS, 레거시 자산을 아우르는 통합 정책 엔진이 요구되고 있습니다.

중소기업의 경우, 클라우드 보안은 자본 지출을 줄이고 위협 인텔리전스 피드에 대한 즉각적인 액세스를 제공합니다. 카나리아 제도 응급 서비스는 주권 클라우드의 모든 워크로드를 암호화하여 시민 데이터를 보호하고 공공 기관이 보호와 지연 요구 사항의 균형을 맞추는 방법을 보여주었습니다. 이러한 광범위한 채택은 2031년까지 스페인의 사이버 보안 시장 규모에서 클라우드가 차지하는 비중이 더욱 확대될 것으로 예상되는 이유를 뒷받침합니다.

스페인의 사이버 보안 시장 보고서는 제공 형태(솔루션, 서비스), 도입 모드(On-Premise, 클라우드), 최종사용자 업종(은행, 금융서비스 및 보험(BFSI), 의료, IT/통신, 산업/방위산업, 제조, 소매/전자상거래, 에너지/유틸리티, 기타), 최종사용자 기업 규모(중소기업(SME), 대기업)에 따라 산업을 세분화하고 있습니다.(중소기업(SME), 대기업)에 따라 업계를 세분화하고 있습니다.

The Spain cybersecurity market is expected to grow from USD 4.57 billion in 2025 to USD 5.01 billion in 2026 and is forecast to reach USD 7.91 billion by 2031 at 9.54% CAGR over 2026-2031.

Spain's decision to position itself as a continental cybersecurity hub, combined with surging ransomware activity and strict EU-level mandates, is fuelling sustained spending on cloud-based protection, managed detection, and quantum-safe encryption solutions. Public-sector programs such as the EUR 1.2 billion National Cybersecurity Strategy, the Digital Spain 2026 roadmap, and the CorA cloud migration plan are enlarging the domestic addressable base for vendors. Rapid 5G rollout, tourism-led cashless retail, and growing industrial digitisation further widen the attack surface, prompting enterprises to prioritise security orchestration and incident-response outsourcing. Although the talent shortage and budget limits at micro-SMEs act as headwinds, Spain's vibrant start-up ecosystem and targeted public subsidies continue to draw foreign capital and technology partnerships into the Spain cybersecurity market.

Government pledges to channel 2% of GDP into security and defence in 2025 include a dedicated 31.16% slice for telecom and cyber capabilities. The resulting flow of EUR 1.2 billion is being directed toward quantum-safe cryptography pilots, large-scale SOC upgrades, and workforce programmes that aim to elevate Spain into the global top five for cyber innovation. Spanish banks have already doubled technology outlays, prompting a parallel surge in network-security and IAM contracts within the Spain cybersecurity market .

Digital Spain 2026 targets the upskilling of 500,000 workers and dispenses grants that offset security adoption costs, yet 70% of current attacks hit SMEs, exposing gaps in basic controls. Kit Digital subsidies now finance enterprise-grade firewalls and MDR subscriptions for firms with 10-49 staff, stimulating vendor focus on lightweight, automated offerings that anchor new revenue in the Spain cybersecurity market.

INCIBE estimates that Spain needed 99,600 specialists in 2025, up from 83,000 vacancies the previous year. Post-quantum cryptography and AI-enabled threat hunting skills are especially rare, prompting enterprises to outsource monitoring to local MSSPs that run 24/7 SOCs. Although INCIBE and Digital Spain programmes deliver free courses, the pipeline remains insufficient, curbing in-house deployment pace across the Spain cybersecurity market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solutions accounted for 69.12% of 2025 revenue and continue to anchor the Spain cybersecurity market as organisations bolster core defences such as NGFWs, EDR and IAM. Compliance with the NIS2 Directive spurs enterprise spending on application security, while autonomous-community agencies prioritise ENS-aligned cloud controls. Managed services, the fastest-growing subsegment, respond to skills shortages by supplying remote SOC functions that compress mean time to detect by 48%. Telefonica Tech now analyses more than 4,000 cloud alerts daily for Spanish customers, illustrating how domestic providers convert local expertise into competitive differentiation within the Spain cybersecurity market.

Demand for professional services endures, centred on ENS audits and NIS2 readiness. Energy utilities relied on Indra consultants to redesign OT segmentation after a 43% attack spike in 2024. Meanwhile, startups automate onboarding and policy configuration to streamline SME adoption. The dual trajectory of high-end managed services and self-service SaaS keeps solutions in the lead even as service revenues accelerate, reinforcing the overall Spain cybersecurity market size outlook.

Cloud deployments captured 62.18% revenue in 2025 and are forecast to advance at a 13.12% CAGR. CorA mandates, multicloud strategies, and sovereign hosting requirements push agencies and banks to treat identity as the new perimeter. ENS "Alto" certification has become a baseline vendor qualification, raising barriers to entry and concentrating spend among compliant suppliers. On-premise controls persist in defence and critical utilities, but hybrid topologies dominate large-enterprise roadmaps, requiring unified policy engines that span SaaS, IaaS, and legacy assets inside the Spain cybersecurity market.

For SMEs, cloud security removes capital expense and provides instant access to threat intelligence feeds. Canary Islands emergency services secured citizen data by encrypting all workloads in a sovereign cloud, showing how public agencies can balance protection and latency requirements. This broad adoption underlines why cloud's share of the Spain cybersecurity market size will widen further by 2031.

The Cybersecurity Market in Spain Report Segments the Industry Into by Offering (Solutions, and Services), Deployment Mode (On-Premise, and Cloud), End-User Vertical (BFSI, Healthcare, IT and Telecom, Industrial and Defense, Manufacturing, Retail and E-Commerce, Energy and Utilities, Manufacturing, and Others), and End-User Enterprise Size (Small and Medium Enterprises (SMEs), and Large Enterprises).