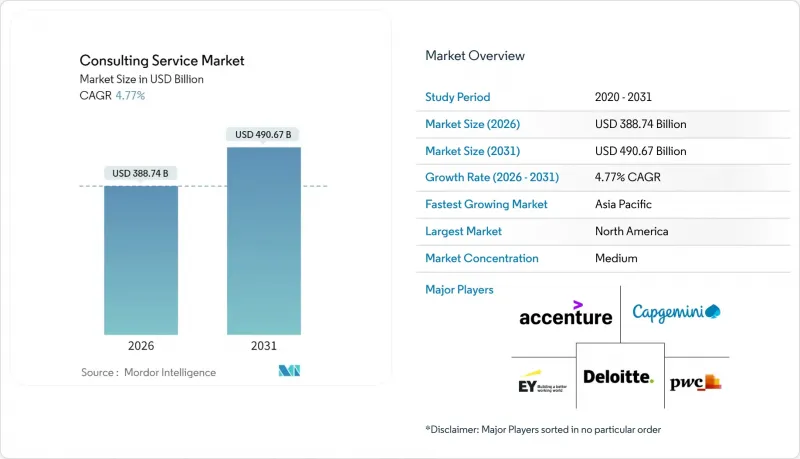

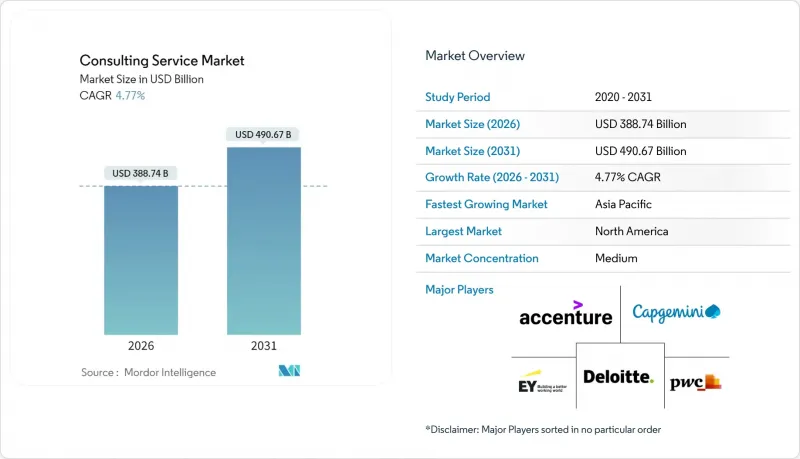

컨설팅 서비스 시장은 2025년 3,710억 4,000만 달러에서 2026년에는 3,887억 4,000만 달러로 성장하여 2026년부터 2031년까지 CAGR 4.77%를 기록하며 2031년까지 4,906억 7,000만 달러에 달할 것으로 예측됩니다.

시장의 안정적 확대는 전통적인 자문 업무에서 기술을 활용한 성과 중심의 참여 모델로 결정적인 전환을 반영하고 있습니다. 디지털 전환에 대한 이사회 차원의 시급성, 환경-사회-지배구조(ESG) 성과에 대한 규제 당국의 감시 강화, 사이버 리스크의 심각성이 기업 지출을 고부가가치 컨설팅 서비스로 유도하고 있습니다. 주요 기업들은 인공지능(AI), 클라우드 전환, 에너지 전환에 대한 전문성 부족을 보완하기 위해 인수를 통해 역량을 확대하고 있습니다. 반면, 전문 특화형 기업은 깊이 있는 전문성과 민첩한 제공 체계를 무기로 사업을 수주하고 있습니다. 온사이트와 가상 제공을 결합한 하이브리드 참여 모델이 표준화되고 있으며, 기업들은 세계 인재에 대한 접근성, 프로젝트 비용 절감, 출장으로 인한 탄소발자국 감소를 실현하고 있습니다. 경쟁적 차별화는 고유한 플랫폼, 데이터 기반 조사 방법론, 그리고 보상을 측정 가능한 고객 성과로 연결시키는 입증 가능한 영향력 지표에 달려 있습니다.

기업들은 수년에 걸친 현대화 프로그램을 단기간에 압축하고 있으며, 클라우드 마이그레이션, 데이터 현대화, 대규모 고급 분석을 통합적으로 추진할 수 있는 컨설턴트에 대한 수요가 증가하고 있습니다. 산업별 클라우드 솔루션은 업종별 맞춤화가 가능하며, 컨설턴트들은 프로세스 재설계와 기술 도입을 통합해야 하는 상황에 직면해 있습니다. 의료 제공자는 원격의료 생태계를 도입하고, 제조업체는 예지보전을 위한 센서를 내장하고, 금융기관은 실시간 결제 기반을 구축하고 있습니다. 컨설팅 기업들은 아키텍처 설계, 데이터 마이그레이션, 컴플라이언스 무결성을 아우르는 산업별 전문 클라우드 프랙티스로 대응하며 순수 전략 어드바이저에서 실행 파트너로 재편하고 있습니다. 이러한 전환을 통해 초기 혁신 단계에 이어 관리형 서비스에서 장기적으로 지속적인 수익을 창출할 수 있습니다.

공급측의 인플레이션과 임금 압박으로 인한 수익률 하락에 따라 비용 절감은 이사회의 최우선 과제입니다. 조직은 컨설팅 계약에 대한 정량적 투자 효과를 요구하고 있으며, 처리 능력 향상, 자동화 추진도, 운전자금 확보에 연동된 성과 연동형 요금 모델이 활성화되고 있습니다. 업무 위탁은 프로세스 마이닝, 지능형 자동화, 하이브리드형 인력 린(Lean) 재구축을 중심으로 전개되는 경향이 강해지고 있습니다. 컨설턴트는 주요 성과 평가 지표를 실시간으로 추적하는 성과 대시보드를 내장하여 투명성을 보장하고 의사결정을 가속화합니다. 이러한 성과중심의 자세를 통해 컨설팅 회사는 임의지출 항목이 아닌 가치창출 파트너로서의 지위를 확립하고, 비용에 민감한 고객사의 지갑 점유율을 강화하고 있습니다.

경제적 신중함으로 인해 기업은 외부 지출을 전략적 격차에만 재분배하고 일상적인 자문 기능은 사내 전문 센터가 흡수하는 경향이 있습니다. 선택적 소싱 전략은 가치 획득을 중시하며, 컨설턴트는 고유한 툴, 업계 벤치마킹, 성과 보장을 통해 차별화를 꾀하고 있습니다. 동시에 기업은 공동 소싱 모델을 제공하고 컨설턴트를 고객 팀에 통합하여 지식 이전과 역량 성숙을 가속화하고 예산 제약 하에서도 업무 기회를 유지합니다.

2025년 운영 컨설팅은 컨설팅 서비스 시장 점유율의 28.94%를 차지했으며, 이는 제조업, 소매업, 에너지 분야의 프로세스 최적화에 대한 지속적인 수요를 뒷받침합니다. 기술 자문은 기업들이 AI 거버넌스, 클라우드 혁신, 사이버 복원력에 대한 전문성을 요구하면서 CAGR 6.29%로 성장하고 있습니다. 시장은 기술과 전통적인 경영 자문의 융합의 혜택을 누리고 있으며, 기업들은 전략 수립, 실행, 관리 서비스 전반에 걸친 엔드 투 엔드 역량에 대한 투자를 촉진하고 있습니다. 기술 자문 업무에서 클라우드 마이그레이션 로드맵과 사이버 보안 대책, 데이터 현대화 청사진을 결합하는 사례가 증가하고 있습니다. 기업들은 자체 개발한 액셀러레이터를 통합하여 타임라인 단축과 리스크 감소를 꾀하는 한편, 매니지드 클라우드 운영을 통해 지속적인 수익을 창출하고 있습니다. 오퍼레이션즈 컨설팅은 디지털 트윈, 프로세스 마이닝 분석, 로봇 프로세스 자동화를 기존의 린 툴킷에 통합하여 그 중요성을 유지하고 있습니다. 운영과 기술 업무 간의 교차 판매는 고객의 총 지출에서 차지하는 비중이 확대되고 있으며, 컨설팅 서비스 시장이 통합형 혁신 솔루션으로 전환하고 있음을 보여줍니다.

헬스케어 및 생명과학 분야는 CAGR 6.63%로 예측되며, 디지털 치료, 원격 환자 모니터링, AI 지원 신약개발이 사업모델을 변화시키면서 타 업종을 능가하는 성장이 예상됩니다. BFSI(은행, 금융, 보험) 분야는 2025년 기준 컨설팅 서비스 시장 규모의 22.10%를 차지하며, 사이버 보안 대책, 규제 준수, 핵심 뱅킹 시스템 현대화 프로젝트에 대한 지속적인 수요를 반영하고 있습니다. 에너지 및 유틸리티 분야의 컨설팅 기회는 탈탄소화 전략, 전력망 현대화, 수소 생태계 계획 등에 집중되어 있으며, 이는 에너지 및 유틸리티 분야가 다분야 자문 서비스에 대한 의존도가 높아지고 있음을 보여줍니다.

강화된 데이터 프라이버시 규제, 환자 중심 케어 모델, 상환 제도의 변화가 헬스케어 컨설팅의 성장세를 뒷받침하고 있습니다. 규제에 대한 전문 지식과 기술 도입 지원을 결합하여 전자건강기록 업그레이드 및 클라우드 기반 임상시험 플랫폼을 통해 의료 서비스 제공자를 안내하고 있습니다. 금융 서비스 분야에서는 실시간 결제 시스템, 디지털 ID, 환경 리스크 스트레스 테스트에 대한 수요가 증가하고 있습니다. ESG 공시 규정과 데이터 거버넌스 기준의 수렴에 따라 분야 간 시너지 효과가 발생하며 시장의 대응 범위가 확대되고 있습니다.

북미는 2025년 매출의 40.62%를 차지했으며, 높은 기술 도입률, 연방 정부의 사이버 보안 기금, 엄격한 금융 서비스 규제에 힘입어 성장세를 이어갈 것으로 보입니다. 미국 기업들은 AI 거버넌스 프레임워크, 제로 트러스트 아키텍처 도입, ESG 컴플라이언스 로드맵 수립을 위해 컨설턴트를 활용하고 있습니다. 캐나다는 자원이 풍부한 경제를 바탕으로 탄소회수 및 수소 파일럿 계획의 시범운영을 통해 에너지 전환 컨설팅 분야에서 틈새시장으로 성장하고 있습니다. 기후변화 관련 공시 의무 강화로 인해 양국의 장기적인 컨설팅 수요가 지속되고 있습니다.

아시아태평양은 가장 빠르게 성장하는 지역으로 대규모 디지털 인프라 프로젝트, 전자정부 이니셔티브, 재생에너지 확대에 힘입어 2031년까지 CAGR 6.92%로 성장할 것으로 예상됩니다. 중국은 AI를 활용한 공급망 최적화와 소비자 은행 업무의 디지털화를 통해 지역 수요를 지원할 것입니다. 일본의 산업용 로봇에 대한 집중과 싱가포르의 금융 서비스 혁신 거점으로서의 지위는 전문 컨설팅 기업에게 비옥한 토양을 형성하고 있습니다. 인도에서는 의료의 디지털화, 제조업의 자동화, 스마트 시티 계획이 융합되어 이 지역의 컨설팅 서비스 시장의 모멘텀을 강화하고 있습니다.

유럽은 에너지 전환의 필요성, 데이터 프라이버시 규제, 지속가능성 리더십을 원동력으로 안정적인 성장을 유지하고 있습니다. CSRD(Corporate Sustainability Reporting Directive)에 따라 기업들은 엄격한 보고 일정과 보증 기준을 충족하는 자문사를 찾아야 합니다. 독일과 프랑스는 인더스트리 4.0을 통한 생산성 향상에 집중하는 반면, 북유럽 국가들은 순환경제 전략의 선구자로서 혁신적인 운영 모델 재구축에 대한 요구가 높아지고 있습니다. 중동 및 아프리카에서는 다각화 정책과 대규모 인프라 프로젝트를 활용하여 전 세계 컨설팅 전문 인력을 유치하고 있습니다. 한편, 남미의 천연자원 생산국들은 세계 경쟁력을 유지하기 위해 ESG 및 경영효율화 로드맵을 필요로 하고 있습니다.

The Consulting Service market is expected to grow from USD 371.04 billion in 2025 to USD 388.74 billion in 2026 and is forecast to reach USD 490.67 billion by 2031 at 4.77% CAGR over 2026-2031.

The market's stable expansion reflects a decisive pivot from traditional advisory toward technology-enabled, outcome-oriented engagement models. Board-level urgency around digital transformation, heightened regulatory scrutiny on environmental, social, and governance (ESG) performance, and intensifying cyber risk are funneling enterprise spending toward high-value consulting offerings. Large firms are broadening capability sets through acquisitions that plug expertise gaps in artificial intelligence (AI), cloud migration, and energy transition, while boutique specialists win mandates by offering deep domain knowledge and agile delivery. Hybrid engagement models that combine on-site and virtual delivery are normalizing, allowing firms to access global talent, lower project costs, and reduce travel-related carbon footprints. Competitive differentiation hinges on proprietary platforms, data-driven methodologies, and demonstrable impact metrics that tie fees to measurable client outcomes.

Enterprises are compressing multi-year modernization programs into shorter cycles, driving premium demand for consultants who can orchestrate cloud migration, data modernization, and advanced analytics at scale. Industry-specific cloud solutions allow sector customization, prompting consultants to blend process redesign with technology implementation. Healthcare providers are deploying telehealth ecosystems, manufacturers are embedding sensors for predictive maintenance, and financial institutions are rolling out real-time payment rails. Consulting firms respond with dedicated industry-cloud practices that cover architecture design, data migration, and compliance alignment, repositioning themselves as execution partners rather than purely strategic advisors. The shift elevates long-term annuity revenue from managed services that follow the initial transformation phase.

Cost containment remains a board priority as supply-side inflation and wage pressure erode margins. Organizations demand quantifiable return-on-investment from consulting engagements, spurring outcome-based fee models tied to throughput gains, automation intensity or working-capital release. Assignments increasingly revolve around process mining, intelligent automation and lean restructuring of hybrid workforces. Consultants embed performance dashboards that track key performance indicators in real time, ensuring transparency and accelerating decision-making. This results-oriented mindset cements consulting firms as value-creation partners rather than discretionary spend items, strengthening wallet share among cost-conscious clients.

Economic caution is prompting enterprises to rebalance external spend toward strategic gaps only, while internal centers of excellence absorb routine advisory functions. Selective sourcing strategies emphasize value capture, pushing consultants to differentiate through proprietary tools, industry benchmarks and outcome guarantees. Simultaneously, firms offer co-sourcing models that embed consultants within client teams to transfer knowledge and speed capability maturation, preserving engagement opportunities despite budget restraint.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Operations consulting captured 28.94% of the consulting service market share in 2025, underscoring persistent demand for process optimization across manufacturing, retail, and energy sectors. Technology Advisory is expanding at a 6.29% CAGR as enterprises seek expertise in AI governance, cloud transformation, and cyber-resilience. The market benefits from the convergence of technology and traditional management advisory, prompting firms to invest in end-to-end capabilities spanning strategy, implementation, and managed services.Technology Advisory engagements increasingly bundle cloud-migration road maps with cybersecurity safeguards and data-modernization blueprints. Firms integrate proprietary accelerators to compress timelines and lower risk, creating annuity revenue through managed cloud operations. Operations consulting remains relevant by embedding digital twins, process-mining analytics, and robotic process automation into classic lean toolkits. Cross-selling between Operations and Technology practices deepens wallet share and exemplifies the consulting service market's shift toward integrated transformation solutions.

The Healthcare and Life Sciences segment is forecast to post a 6.63% CAGR, outpacing all other verticals as digital therapeutics, remote patient monitoring, and AI-assisted drug discovery reshape operating models. BFSI retained 22.10% of the consulting service market size in 2025, reflecting sustained cybersecurity, regulatory compliance, and core-bank modernization projects. Consulting opportunities in energy and utilities concentrate on decarbonization strategy, grid modernization, and hydrogen ecosystem planning, reinforcing the sector's reliance on multidisciplinary advisory.

Heightened data-privacy regulation, patient-centric care models, and reimbursement shifts underpin healthcare consulting momentum. Firms combine regulatory know-how with technology enablement, guiding providers through electronic-health-record upgrades and cloud-based clinical trial platforms. In financial services, demand centers on real-time payment rails, digital identity, and environmental risk stress-testing. Cross-vertical synergies emerge as ESG disclosure rules and data-governance standards converge, expanding the market's addressable scope.

The Consulting Service Market Report is Segmented by Service Type (Operations, Strategy, Financial Advisory, Technology Advisory, Human-Capital, Risk and Compliance, Other Service Types), Client Industry (BFSI, Healthcare and Life Sciences, and More), Delivery Model (On-Site, Remote/Virtual, Hybrid), Organisation Size, and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America generated 40.62% of 2025 revenue, buoyed by high technology adoption, federal cybersecurity funding, and stringent financial services regulation. U.S. enterprises engage consultants for AI governance frameworks, zero-trust architecture implementation, and ESG compliance road maps. Canada contributes niche growth in energy-transition consulting, leveraging its resource-rich economy to test carbon-capture and hydrogen pilot schemes. Intensifying climate-related disclosure mandates sustains long-term consulting demand across both countries.

Asia-Pacific is the fastest-growing region, set to expand at a 6.92% CAGR through 2031, propelled by large-scale digital-infrastructure projects, e-government initiatives, and renewables build-out. China anchors regional demand with AI-infused supply-chain optimization and consumer banking digitization. Japan's emphasis on industrial robotics and Singapore's status as a financial-services innovation hub create fertile terrain for specialized consulting shops. India blends healthcare digitalization, manufacturing automation, and smart-city programs, reinforcing the consulting service market's momentum in the subcontinent.

Europe maintains steady growth, driven by energy-transition imperatives, data-privacy regulation and sustainability leadership. The Corporate Sustainability Reporting Directive compels companies to seek advisors who can meet stringent reporting timelines and assurance thresholds. Germany and France focus on Industry 4.0 productivity gains, while the Nordics pioneer circular-economy strategies that elevate demand for innovative operating-model rewiring. Middle East and Africa harness diversification policies and mega-infrastructure projects to attract global consulting expertise, whereas South America's natural-resource producers require ESG and operational-efficiency road maps to remain globally competitive.