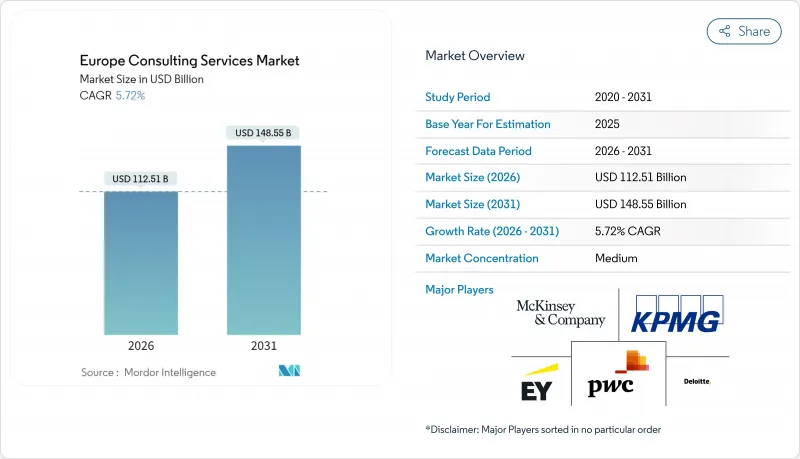

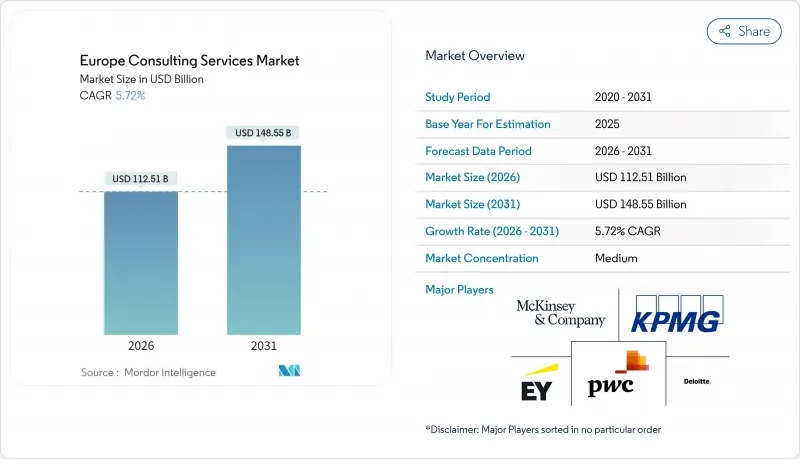

유럽의 컨설팅 서비스 시장은 2025년 1,064억 2,000만 달러로 평가되었고, 2026년에는 1,125억 1,000만 달러, 2031년까지 1,485억5,000만 달러에 이를 전망입니다. 2026년부터 2031년에 걸쳐 CAGR 5.72%로 성장할 전망입니다.

이러한 꾸준한 성장은 전문 서비스 기업들이 경제적 불확실성, 디지털 우선 요구, 엄격한 지속가능성 규정에 적응해 왔음을 보여줍니다. 유럽위원회의 '디지털·유럽계획'이 기술 도입에 79억 유로를 투입함으로써 수요가 강화되어 서비스 제공업체는 국경을 넘어선 대처를 확대할 수 있습니다. 지정 학적 공급망의 긴장으로 인해 Operational Excellence 프로젝트는 고객의 우선 과제이며, 주요 기업의 대규모 AI 투자는 신기술을 일상적인 컨설팅 아티팩트로 전환하고 있습니다. EU 부흥·탄력 기금(RRF)으로부터의 자금 제공에 의해 중소기업의 외부 전문지식 도입이 가속해, 고객 기반이 확대됨과 함께 대기업 예산에의 의존도가 저하하고 있습니다. 빅포가 40억 달러 이상을 AI 능력에 투자하는 가운데 경쟁 격화가 진행되고 서비스 제공의 경제성이 재구축되는 한편, 중견 기업은 틈새 분야에 대한 특화를 강요당하고 있습니다.

유럽 연합(EU)은 디지털 규제의 정합화에 의해 행정상의 마찰을 경감하고, 컨설팅 기업이 보다 적은 컴플라이언스 체크로 국경을 넘은 솔루션의 복제를 가능하게 하고 있습니다. 독일과 프랑스는 2024년에 공공 부문 소프트웨어의 상호 운용성에 관한 협력을 공식화하고 선행 기업은 프로젝트 리드 타임을 단축하는 재사용 가능한 플레이북 개발 기회가 주어지고 있습니다. 중견 공급자는 각 국가에 대해 완전한 법무 팀을 필요로 하지 않으므로 새로운 배포 기회를 얻고 있습니다. 완전한 조화가 실현되기 위해서는 2027년까지 기다려야 하지만, 다국어 대응의 규제 전문 지식에 지금 투자하는 기업은 정부가 공동 서비스를 확대하는 가운데 여러 해에 걸친 틀 계약을 획득할 수 있을 가능성이 있습니다.

경영진은 인공지능을 비용억제와 성장의 필수 수단으로 파악하고 있어 이것이 대규모 권고안건의 창출로 이어지고 있습니다. 독일의 AI 시장만으로도 연간 15% 성장하고 있으며, 2030년까지 GDP를 4,300억 유로 밀어올릴 가능성이 있어 AI 전략, 데이터 엔지니어링, 체인지 매니지먼트 안건의 급증을 지원하고 있습니다. 델로이트의 새로운 플랫폼 'Zora'와 EY의 150개 AI 에이전트 군은 대기업이 지적 재산을 제품화하고 고객에게 25-40%의 생산성 향상을 가져오는 방법을 보여줍니다. 중소 컨설팅 기업은 기본적인 자동화가 상품화되는 동안 하이퍼 전문 AI 용도으로 전환하지 않으면 이익률의 압박 위험에 직면합니다.

유럽의 컨설팅 기업은 데이터 사이언스자의 채택을 따라잡지 못했습니다. 유럽직업훈련개발센터(CEDEFOP)의 노동력 및 스킬 부족지수는 2035년까지 분석·AI 관련 직종이 심각한 인력 부족에 직면한다고 지적하고 있습니다. 독일과 프랑스 정부는 기술직 고용이 과거 최고를 기록했음에도 불구하고 지속적인 인력 부족을 보고하고 있으며, 기업은 고액의 보상을 지불하거나 업무를 해외로 이전할 수밖에 없는 상황입니다. 인력 부족은 프로젝트 비용을 높이고 납기를 지연시키고 고급 분석 업무의 대응 가능한 안건량을 감소시키고 있습니다. 중소 공급자는 주요 4개 회사의 보상 체계를 따르지 못하고 시장 통합 리스크가 높아지기 때문에 가장 심각한 영향을 받고 있습니다.

운영 컨설팅은 최대 매출 점유율을 창출했으며 2025년 유럽의 컨설팅 서비스 시장의 28.12%를 차지했습니다. 이는 지정학적 긴장 속에서 기업이 공급망의 탄력성과 비용 절감을 요구했기 때문입니다. 유럽의 컨설팅 서비스 시장에서는 린 생산 방식, 프로세스 재설계, 운전 자금 최적화가 지속적으로 우선되고 전문가에게 안정적인 수익원이 되고 있습니다. 병행하여 디지털 변환 컨설팅은 AI, 클라우드 마이그레이션 및 지속가능성 대시보드를 원동력으로 모든 부문 중 가장 빠른 7.49%의 연평균 복합 성장률(CAGR)로 성장하고 있습니다.

전략, 재무 권고, 인사/변혁 관리는 여전히 중요한 역할을 하고 있지만, 수요는 기술, 리스크 관리, 인재 육성을 융합한 통합 변혁 솔루션에 집중하고 있습니다. 사이버 위협 증가와 클라우드 아키텍처의 단편화는 기술 권고의 중요성을 높이고 있습니다. 기업이 탄소 회계를 업무 흐름에 통합하는 동안 지속가능성과 ESG 컨설팅은 핵심 업무 요구사항과 겹치고 있습니다. 유럽의 컨설팅 서비스 시장이 사일로화된 이슈에서 플랫폼 기반 성과 연동형 프로그램으로 이동하는 동안 업계 특화형 플레이북을 기반으로 다분야 횡단팀을 구축하는 서비스 제공업체가 경쟁 우위를 유지할 것입니다.

ICT 및 미디어 분야는 2025년 수익의 29.56%를 차지하며 지속적인 기술 업데이트 사이클과 활발한 소프트웨어 혁신을 반영합니다. 이 고객층은 생성형 AI, 5G 수익화, 엣지 컴퓨팅 프로젝트의 시험 운영을 계속하고 있으며, 유럽의 컨설팅 서비스 시장에서의 견고한 수요를 지원하고 있습니다. 한편 소비재 및 소매 업계에서는 옴니채널 투자, 라스트마일 물류, 데이터 구동형 머천다이징이 가속화되어 2031년까지 연평균 복합 성장률(CAGR) 7.41%를 기록할 전망입니다.

금융 서비스 분야에서는 자기 자본 규제와 디지털 뱅킹의 경쟁을 배경으로 컨설팅 지출이 높은 수준을 유지하고 있습니다. 제조업은 인더스트리 4.0 로드맵이나 에너지 절약형 플랜트 개수에 주력하고 있습니다. 의료 분야에서는 전자 차트 통합과 클라우드 기반 ERP 이행이 가속화되고 있어, 아스클레피오스·클리니켄사의 SAP S/4HANA 도입에서는 18개월에 이르는 외부 지원이 필요했습니다. 에너지 및 유틸리티 분야에서는 전력망의 디지털화와 수소 대응 인프라 계획이 요구되고 있으며, 지속가능성에 초점을 맞춘 어드바이저에게 틈새 기회가 탄생하고 있습니다.

유럽의 컨설팅 서비스 시장은 서비스 유형(업무 컨설팅, 전략 컨설팅, 재무 권고 등), 고객 업계(은행, 금융서비스 및 보험(BFSI), 제조업 및 산업 등), 기업 규모(대기업, 중소기업), 제공 모델(온사이트 계약, 원격/가상, 하이브리드 모델), 국가별로 시장 세분화됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

The Europe Consulting Services Market is expected to grow from USD 106.42 billion in 2025 to USD 112.51 billion in 2026 and is forecast to reach USD 148.55 billion by 2031 at 5.72% CAGR over 2026-2031.

This steady climb underscores how professional services firms have adapted to economic uncertainty, digital-first mandates, and tightening sustainability rules. Demand strengthens as the European Commission's Digital Europe Programme channels EUR 7.9 billion toward technology adoption, allowing service providers to expand cross-border engagements. Geopolitical supply-chain stress keeps operational excellence projects at the top of client agendas, while heavy AI investment by leading firms converts emerging technology into day-to-day consulting deliverables. Funding from the EU Recovery and Resilience Facility (RRF) accelerates small-business adoption of external expertise, widening the customer base and reducing dependence on large-enterprise budgets. Competitive intensity rises as the Big Four plough more than USD 4 billion into AI capabilities, reshaping service delivery economics and pushing mid-tier players toward niche specialisms.

The European Union is reducing administrative friction by aligning digital regulations, letting consulting firms replicate solutions across borders with fewer compliance checks. Germany and France formalized cooperation on interoperable public-sector software in 2024, giving early movers a chance to develop reusable playbooks that cut project lead times. Mid-sized providers gain new reach because they no longer need full legal teams for each country. While complete harmonization will not occur until 2027, firms that invest now in multilingual regulatory expertise stand to win multiyear frameworks as governments scale joint services.

C-suites view artificial intelligence as an essential lever for cost containment and growth, translating into sizeable advisory pipelines. Germany's AI market alone is growing 15% annually and could add EUR 430 billion to GDP by 2030, underpinning a surge in AI strategy, data engineering, and change-management engagements. Deloitte's new Zora platform and EY's fleet of 150 AI agents illustrate how the largest firms are productizing intellectual property to deliver 25-40% productivity gains for clients. Smaller consultancies must pivot to hyper-specialized AI applications or risk margin squeeze as basic automation becomes commoditized.

European consultancies cannot hire data scientists fast enough. CEDEFOP's Labour and Skills Shortage Index flags analytics and AI roles as high-pressure occupations through 2035. German and French governments report persistent gaps despite record tech job creation, forcing firms to pay premiums or offshore work. Scarcity inflates project costs and slows delivery, reducing the addressable volume for advanced analytics engagements. Smaller providers feel the pinch hardest because they struggle to match Big Four compensation packages, thereby intensifying market consolidation risks.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Operations consulting generated the largest revenue slice, capturing 28.12% of the European consulting services market share in 2025 as companies sought supply-chain resilience and cost savings amid geopolitical strains. The European consulting services market continues to prioritise lean manufacturing, process re-engineering, and working-capital optimization, anchoring steady fee streams for specialists. In parallel, digital transformation consulting is growing at a 7.49% CAGR, the fastest among all segments, powered by AI, cloud migration, and sustainability dashboards.

Strategy, financial advisory, and HR/change management retain essential roles, yet demand increasingly converges around integrated transformation offerings blending technology, risk management, and workforce enablement. Technology advisory enjoys heightened relevance because cyber threats multiply and cloud architectures fragment. Sustainability and ESG consulting now overlap with core operational mandates as firms embed carbon accounting into process flows. Service providers that create multidisciplinary squads around sector-specific playbooks will defend relevance as the European consulting services market shifts from siloed engagements toward platform-based, outcome-linked programmes.

The ICT and Media sector contributed 29.56% of 2025 revenue, reflecting constant technology refresh cycles and heavy software innovation. This client group continues to pilot generative AI, 5G monetization, and edge computing projects, sustaining robust demand within the European consulting services market. Consumer and Retail, however, is registering a 7.41% CAGR to 2031 as omnichannel investment, last-mile logistics, and data-driven merchandising accelerate.

Financial services keep consulting spend elevated on account of capital adequacy regulations and digital banking competition, while manufacturing turns to Industry 4.0 roadmaps and energy-efficient plant retrofits. Healthcare clients ramp up electronic-medical-record consolidation and cloud-hosted ERP migrations such as Asklepios Kliniken's SAP S/4HANA rollout, which required 18 months of external support. Energy and Utilities look for grid digitization and hydrogen-ready infrastructure planning, creating niche opportunities for sustainability-focused advisers.

Europe Consulting Services Market is Segmented by Service Type (Operations Consulting, Strategy Consulting, Financial Advisory, and More), Client Industry (BFSI, Manufacturing and Industrials, and More), Enterprise Size (Large Enterprises and Small and Medium Enterprises), Delivery Model (On-Site Engagement, Remote/Virtual, and Hybrid Model), and Country. The Market Forecasts are Provided in Terms of Value (USD).