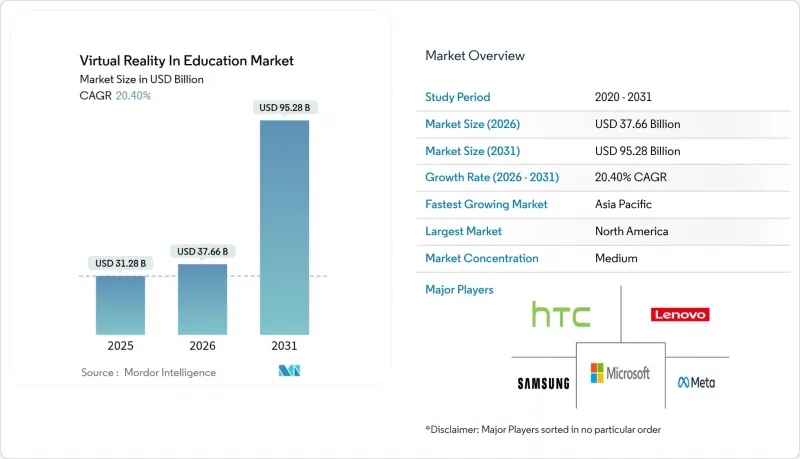

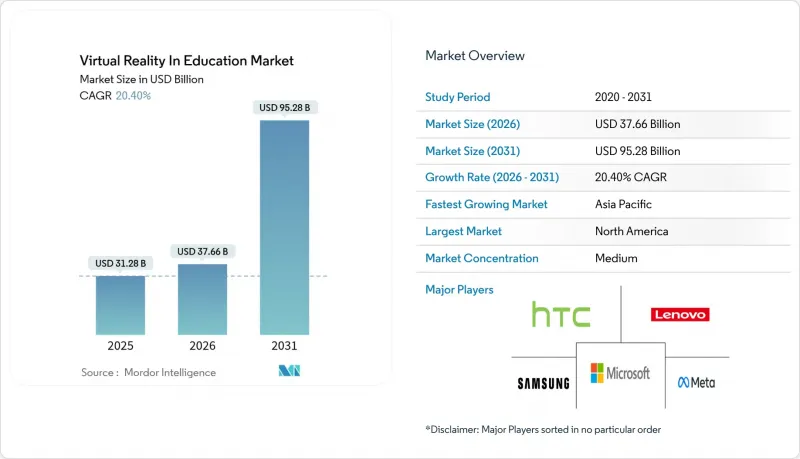

교육용 가상현실(VR) 시장은 2025년에 312억 8,000만 달러로 평가되었고, 2026년 376억 6,000만 달러에서 2031년까지 952억 8,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 20.4%로 예상됩니다.

헤드셋 가격의 하락, 정부의 막대한 보조금 지원, 학습자의 성과 측정 가능한 향상으로 교육용 가상현실(VR) 시장의 성장을 지속적으로 촉진하고 있습니다. 특히, 기업에서 몰입형 교육 프로그램을 도입하면 학습 시간을 최대 75%까지 단축하고 지식 정착률을 4배까지 높이는 효과를 기대할 수 있습니다. 여전히 하드웨어가 매출의 대부분을 차지하고 있지만, 교육기관이 턴키형 컨텐츠와 분석 기능을 요구하면서 서비스 중심의 구독 패키지가 가장 빠르게 성장하고 있습니다. 북미에서는 바이든-해리스 행정부의 2억 7,700만 달러의 혁신 기금을 배경으로 도입이 선행되고 있으며, 아시아태평양에서는 중국과 일본의 인프라 구축 계획에 힘입어 도입이 가속화되고 있습니다. 경쟁사 간의 적대관계는 중간 정도이며, Meta, Microsoft와 같은 대형 플랫폼이 커리큘럼 연동형 컨텐츠와 비용 효율적인 도입 모델을 제공하는 zSpace, Labster와 같은 전문 기업들과 경쟁하고 있습니다.

교육기관에서는 다양한 학습 스타일에 적응하는 몰입형 수업의 가치가 점점 더 중요시되고 있습니다. 연구에 따르면, VR 학습자는 교실에서 학습하는 그룹에 비해 자신감이 275% 향상되고, 코스 완료 속도가 4배 더 빠르다는 결과가 나왔습니다. 대학에서는 현재 VR 커리큘럼에서 디자인적 사고력이 부족하다는 지적이 제기되고 있으며, 기술적 엄격함과 교육학을 융합한 제공업체에게 기회가 생기고 있습니다. AI 기반 엔진은 학습자별로 컨텐츠를 최적화합니다. 예를 들어 zSpace의 커리어 코치 AI는 지역 노동 시장 데이터와 학습자의 진로를 연동합니다. 통제된 가상 환경은 정서적 장애가 있는 학생들의 불안을 감소시키고, 학습 정착률을 향상시킵니다. 학습자 중심 모델이 주류로 자리 잡으면서 교육에서 가상현실은 성과 향상을 위한 교육기관의 핵심 인프라로 자리 잡고 있습니다.

정량화된 성과가 관리자, 학부모, 기업의 인재개발 담당자를 설득하고 있습니다. 간호 프로그램에서는 VR 시나리오 진행 시 참여율이 95%에 달하는 반면, 기존 실습실에서는 15%에 불과한 것으로 나타났습니다. 제조업의 경우, VR 안전교육 실시 후 직장 내 부상률이 43% 감소했다는 보고가 있습니다. 수학 수업에서는 추상적인 개념을 명확히 하는 3D 오브젝트를 조작함으로써 교실에서의 학습 의욕이 급상승합니다. 메타가 13개 대학과 함께 진행한 프로그램은 교육기관의 확고한 신뢰를 보여주며, 다른 기관의 채용을 유도하는 모범사례를 만들어내고 있습니다. 이러한 성과는 교육 분야 VR 시장의 투자와 수용의 선순환을 만들어내고 있습니다.

많은 용도이 교육 효과보다 오락성을 우선시하기 때문에 교육 관계자들은 학습 기준에 부합하는 교재를 충분히 확보하지 못하고 있으며, 특히 영어권 이외 시장에서는 이러한 경향이 두드러집니다. 교사들은 평가 도구와 구성주의 기법을 통합한 VR 모듈을 찾는 데 어려움을 겪고 있으며, 하드웨어를 사용할 수 있음에도 불구하고 도입에 어려움을 겪고 있습니다. 의학 등 전문 분야에서는 규제 준수가 필요하지만, 검증된 시나리오공급은 여전히 부족한 상황입니다. 피어슨 XR 부트캠프와 같은 파트너십은 초기 진전을 보이고 있지만, 세계 수요를 충족시키기에는 충분하지 않습니다. 컨텐츠 라이브러리가 확대되기 전까지는 교육용 가상현실(VR) 시장의 성장은 기반이 되는 하드웨어의 능력에 뒤쳐질 수밖에 없습니다.

2025년 기준, 하드웨어는 학교 및 교육센터로의 기기 도입에 힘입어 교육용 VR 시장 점유율의 60.72%를 차지할 것으로 예측됩니다. 그러나 교육기관이 컨텐츠, 디바이스 관리, 분석 기능을 결합한 구독형 번들을 선호하는 추세로 인해 서비스 분야는 22.2%의 연평균 복합 성장률(CAGR)로 확대될 것으로 예측됩니다. 서비스 관련 교육용 VR 시장 규모는 2031년까지 소프트웨어 매출을 넘어설 것으로 예측됩니다. 독립형 헤드셋의 저렴한 가격으로 인해 하드웨어에 대한 수요는 유지되지만, 공급업체들은 이미 영구 업데이트를 번들로 제공하여 업데이트 주기를 단축하고 있습니다.

구독 모델은 예산이 한정된 학군의 자본 지출 장벽을 낮춰줍니다. ArborXR의 학습 분석 분야 진출과 zSpace의 AI 기반 가이던스 툴은 벤더들이 하드웨어 기반을 지속적인 수익 생태계로 전환하는 방법을 보여주고 있습니다. 교육 설계를 개선하는 교육 컨설팅 서비스는 현재 RFP(제안요청서)에서 중요한 요소가 되고 있습니다. 이러한 추세는 성과 기반 조달로의 전환을 의미하며, VR 산업 전반에 걸쳐 지속적인 수익원을 강화하고 있습니다.

교육 분야 VR 도입의 64.62%는 여전히 학술기관이 차지하고 있으며, 초중고부터 대학까지 보조금에 의한 선행 도입이 반영된 것으로 나타났습니다. 그러나 기업 교육 분야는 22.9%의 연평균 복합 성장률(CAGR)로 성장하고 있으며, 안전 대책, 컴플라이언스, 고객 서비스 분야에서 측정 가능한 ROI(투자수익률)가 그 원동력이 되고 있습니다. 기업용 교육용 VR 시장 규모는 2031년까지 학술 분야와 동등한 수준에 도달할 것으로 예측됩니다. 의료 및 광업 분야의 기업들은 몰입형 프로그램 도입 후 오류 발생률이 40% 이상 감소하여 투자 회수 기간을 단축하고 있습니다.

기업들은 소프트 스킬과 제품 지식 모듈을 중시하고, 빠른 컨텐츠 제작 도구와 분석 기능 통합에 대한 수요를 주도하고 있습니다. 교육 분야의 성장은 계속될 것이며, 예산 주기 및 커리큘럼 승인 프로세스가 장벽이 될 수 있습니다. 벤더 입장에서는 두 부문을 아우르는 다양한 포트폴리오를 통해 VR 산업의 경기 변동에 대한 내성을 확보할 수 있습니다.

교육용 가상현실(VR) 시장은 구성요소(하드웨어, 소프트웨어, 서비스), 최종 사용자(학술기관, 기업 교육), 디바이스 유형(독립형 헤드셋, 유선 PC 연결형 VR 헤드셋 등), 응용 분야(STEM 및 기술 교육, 의료 및 헬스케어 교육 등), 지역(북미 등)으로 구분됩니다. 등), 지역(북미 등)으로 구분됩니다. 시장 예측은 금액 기준(USD)으로 제공됩니다.

북미는 풍부한 보조금 프로그램과 성숙한 교육 기술(EdTech) 생태계로 인해 2025년 매출의 38.95%를 차지할 것으로 예측됩니다. 정부의 2억 7,700만 달러의 혁신 보조금은 몰입형 대수학 도구에 사용되었고, 국립과학재단은 2,500만 달러를 연구개발(R&D)에 투자하여 대학 간 협력을 촉진하고 있습니다. 기업 도입은 의료, 소매, 전문 기술 분야로 확대되고 있으며, Interplay Learning 등 기업들이 인력 부족 대책으로 VR 모듈을 확대하고 있습니다. 이러한 요인들로 인해 교육용 가상현실(VR) 시장은 견조한 성장세를 유지하고 있지만, 보급률 상승에 따라 성장률은 둔화되는 추세입니다.

아시아태평양은 2031년까지 21.5%의 가장 빠른 지역 CAGR을 나타낼 것으로 예측됩니다. 중국에서는 2025년에만 각 성(省)에서 직업훈련용 VR랩을 위해 1,500만 달러 이상의 입찰을 진행했으며, 일본에서는 'DX 고등학교' 계획을 통해 캠퍼스당 최대 1,000만 엔을 디지털화 추진에 투입하고 있습니다. 한국에서는 기술 훈련의 설비 비용 절감을 위해 VR을 도입하고 있으며, 이 방식은 세계은행 연구진에 의해 주목받고 있습니다. 이러한 정책적 협력으로 교실로의 도입이 가속화되고 있으며, 아시아태평양은 교육용 가상현실(VR) 시장에서 북미와의 격차를 좁힐 준비를 하고 있습니다.

유럽에서는 '디지털 유럽 계획'에 따른 13억 유로의 예산 배분과 가상세계 커리큘럼을 포함한 전문 아카데미에 대한 1억 8천만 유로의 지원이 효과를 발휘하고 있습니다. 스코틀랜드의 지방정부 전체에서 ClassVR을 도입한 것은 지역 기관이 체계적인 조달을 추진하고 있음을 보여줍니다. 남미와 중동의 신흥 시장에서는 하드웨어 가격이 300달러 이하로 내려가면서 도입이 진행되고 있지만, 인프라 제약으로 인해 즉각적인 보급에 어려움을 겪고 있습니다. 전반적으로, 정책의 일관성과 자금 투입 밀도는 교육 분야 가상현실 시장의 지역적 견인력을 예측하는 주요 지표로 남아있습니다.

The Virtual Reality In Education Market was valued at USD 31.28 billion in 2025 and estimated to grow from USD 37.66 billion in 2026 to reach USD 95.28 billion by 2031, at a CAGR of 20.4% during the forecast period (2026-2031).

Lower headset prices, sizable government grants, and measurable improvements in learner performance continue to propel the virtual reality in education market, especially as corporations adopt immersive training programs that reduce seat time by up to 75% while quadrupling knowledge retention. Hardware still supplies most revenue, but service-oriented subscription packages are expanding fastest as institutions seek turnkey content and analytics. North America leads the adoption due to the Biden-Harris Administration's USD 277 million innovation fund, whereas the Asia Pacific accelerates on the back of Chinese and Japanese infrastructure programs. Competitive rivalry is moderate, as large platforms such as Meta and Microsoft contend with specialists like zSpace and Labster, which pair curriculum-aligned content with cost-effective deployment models.

Institutions increasingly value immersive lessons that adapt to diverse learning styles, with studies showing VR learners achieve 275% higher confidence and complete courses four times faster than classroom cohorts. Universities highlight gaps in design-thinking skills within current VR curricula, opening opportunities for providers that combine technical rigor with pedagogy. AI-driven engines tailor content to each learner; zSpace's Career Coach AI, for instance, matches local labor-market data to personalized study pathways Controlled virtual environments also reduce anxiety for students with emotional impairments while boosting retention. As learner-centric models move mainstream, the virtual reality in education market becomes core infrastructure for institutions seeking improved outcomes.

Quantified gains are persuading administrators, parents, and corporate L&D heads alike. Nursing programs see 95% participation when scenarios run in VR versus 15% in traditional labs. Manufacturing firms report 43% drops in workplace injuries after VR safety drills. Classroom engagement spikes in mathematics when students manipulate 3-D objects that clarify abstract concepts. Meta's program with 13 universities demonstrates institutional confidence, creating reference sites that spur peer adoption. These outcomes generate a virtuous cycle of investment and acceptance for the virtual reality in education market.

Many applications prioritize entertainment over pedagogy, leaving educators short of materials that match learning standards, especially outside English-speaking markets. Teachers struggle to locate VR modules that embed assessment tools and constructivist methods, hampering adoption despite hardware availability. Specialized domains such as medicine need regulatory compliance, yet the pipeline of validated scenarios remains thin. Partnerships like Pearson-XR Bootcamp illustrate early progress but are insufficient to satisfy global demand. Until content libraries scale, growth of the virtual reality in education market will trail underlying hardware capability.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Hardware captured 60.72% of the virtual reality in education market share in 2025 on the strength of device rollouts across schools and training centers. However, the services segment is on pace for 22.2% CAGR as institutions favor subscription bundles that bundle content, device management, and analytics. The virtual reality in education market size tied to services is poised to overtake software revenue approaching 2031. Standalone headset affordability keeps hardware relevant, yet platform vendors are already bundling perpetual updates, reducing replacement cycles.

Subscription models also mitigate capital-expenditure barriers for districts with limited budgets. ArborXR's shift into learning analytics and zSpace's AI-powered guidance tools illustrate how vendors convert hardware footholds into recurring-revenue ecosystems. Training and consulting services that improve instructional design now factor prominently in RFPs. These patterns signal a pivot toward outcomes-based procurement, reinforcing recurrent income streams across the virtual reality industry.

Academic institutions still own 64.62% of the virtual reality in education, reflecting early grant-funded pilots across K-12 and universities. Yet corporate training advances at 22.9% CAGR, propelled by measurable ROI in safety, compliance, and customer-service scenarios. The virtual reality in education market size attributable to enterprises is projected to approach parity with academia by 2031. Corporations in healthcare and mining have logged 40%-plus error reductions after immersive programs, shortening payback periods.

Enterprises champion soft-skills and product-knowledge modules, fueling demand for rapid-authoring tools and analytics integrations. Academic growth continues but faces budget cycles and curriculum-approval processes. For vendors, diversified portfolios that address both segments offer resilience against economic swings within the virtual reality industry.

Virtual Reality in Education Market is Segmented by Component (Hardware, Software, and Services), End User (Academic Institutions, and Corporate Training), Device Type (Standalone Headsets, Tethered PC-VR Headsets, and More), Application Area (STEM and Technical Education, Medical and Healthcare Training, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America retained 38.95% of 2025 revenue thanks to robust grant programs and a mature EdTech ecosystem. The Administration's USD 277 million innovation grants earmark immersive algebra tools, while the National Science Foundation commits USD 25 million to R&D, seeding university partnerships. Corporate uptake spans healthcare, retail, and skilled trades as companies such as Interplay Learning scale VR modules for talent shortages. These forces keep the virtual reality market in education expanding at a healthy clip, though growth moderates as penetration rises.

Asia Pacific is set to log the fastest regional CAGR of 21.5% through 2031. China's provinces issued tenders exceeding USD 15 million for vocational VR labs in 2025 alone, while Japan's DX High School scheme funds up to JPY 10 million per campus for digital upgrades. South Korean institutions deploy VR to cut equipment costs in technical training, an approach highlighted by World Bank researchers. These coordinated policies accelerate classroom integration, positioning Asia Pacific to narrow its gap with North America in the virtual reality in education market.

Europe benefits from the Digital Europe Programme's EUR 1.3 billion allocation and EUR 108 million for specialist academies that include virtual-worlds curricula. Scotland's council-wide ClassVR rollout shows regional bodies embracing systemic procurement. Emerging markets in South America and the Middle East follow as hardware prices dip below USD 300, though infrastructure constraints still curb immediate uptake. Overall, policy alignment and funding density remain the primary predictors of regional traction for the virtual reality in education market.