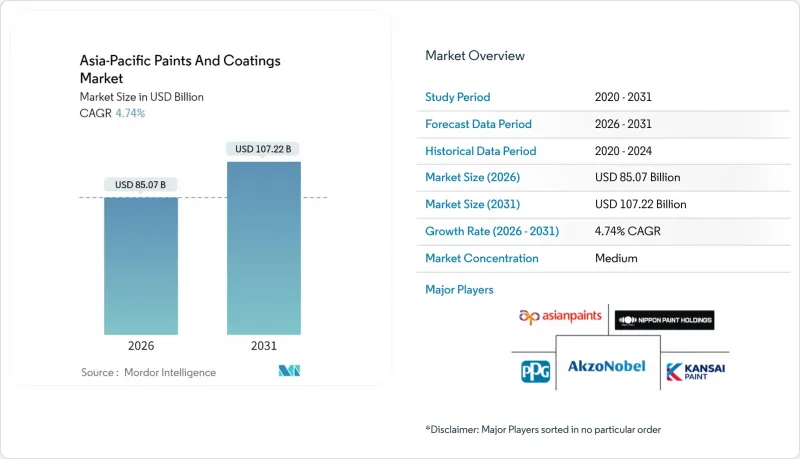

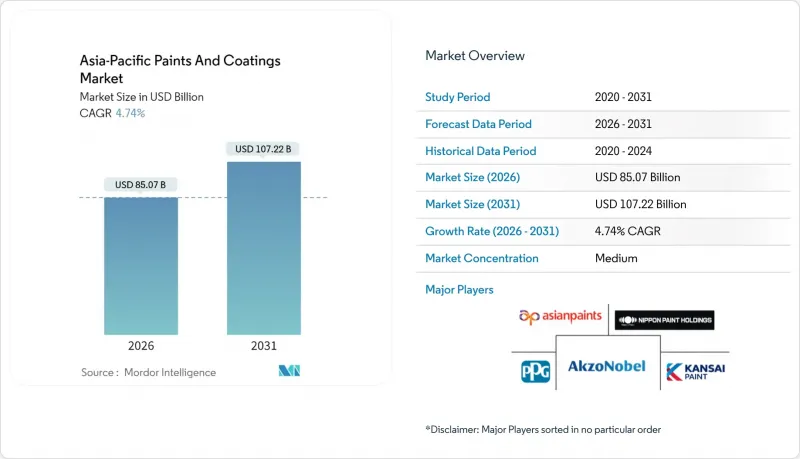

아시아태평양의 페인트 및 코팅 시장은 2025년 812억 2,000만 달러에서 2026년에는 850억 7,000만 달러로 성장하며, 2026-2031년에 CAGR 4.74%로 추이하며, 2031년에는 1,072억 2,000만 달러에 달할 것으로 예측되고 있습니다.

환경 규제 강화, 도시화 가속화, 자동차 및 산업 생산의 급속한 확대가 지속적인 수요를 지원하는 한편, 수성 플랫폼으로의 전환으로 기술 선도 기업은 이익률의 안정성을 확보할 수 있는 위치에 있습니다. 2024년 기준 중국이 56.42%의 점유율을 유지하며 주도권을 쥐고 있지만, 인프라 투자와 주택 개보수가 활발해지면서 2030년까지의 성장 속도는 인도가 주도할 것으로 보입니다. 특히 이산화티타늄 가격 변동을 비롯한 원자재 가격 변동으로 이익률 관리에 대한 관심이 높아지고 있으며, BASF와 AkzoNobel의 사업 매각과 같은 전략 재검토는 규모, 포트폴리오의 균형, 지역적 깊이가 경쟁 우위를 결정짓는다는 것을 시사하고 있습니다. 디지털화된 컬러 툴, 고급 도시 주택의 재도장 주기 단축, 정책적으로 지원되는 '그린십' 리노베이션 등이 수요를 점진적으로 확대하고 있으며, 이러한 요소들은 아시아태평양의 페인트 및 코팅 시장을 보다 성숙한 화학제품 밸류체인과 차별화하고 있습니다. 차별화시키고 있습니다.

인도네시아, 태국, 베트남, 베트남, 말레이시아, 필리핀의 건설 활동이 급증하면서 건축 및 보호용 도료에 대한 수요가 지속적으로 증가하고 있습니다. 인도네시아는 2025년까지 세계 3위의 건설시장이 될 것으로 예상되며, 국내총생산(GDP)의 9%를 차지하며 전년 대비 13%의 성장률을 보이고 있습니다. 대규모 교통 회랑, 산업 단지, 저렴한 주택 프로그램, 콘크리트, 철재, 목재 기판에서 페인트의 접촉점을 증가시키고 있습니다. 국제적인 건설사들은 그린 빌딩 인증에 부합하는 저 VOC 페인트를 지정하는 경향이 강하며, 이로 인해 수성 페인트에 대한 수요가 더욱 증가하고 있습니다. 자동차 및 전자기기 산업 클러스터에 대한 외국인 직접투자도 고성능 OEM 도료, 바닥용 도료, 기계용 도료의 수주를 늘리고 있습니다. 지속적인 투자 유입은 거시경제의 안정과 지정학적 평온에 달려있지만, 단기적인 수주 잔고로 인해 아시아태평양의 페인트 시장은 건설 관련 수요 증가를 예상하고 충분한 공급이 유지되고 있습니다.

중국의 성숙한 부동산 시장에서는 소유주가 미관 개선과 자산 보존을 우선시하는 경향으로 인해 재도장 간격이 짧아지고 있습니다. 일본페인트 보고서에 따르면 재도장 주기가 5-7년 3-5년으로 단축된 일선 및 이선급 도시에서의 성장을 볼 수 있습니다. 장기적인 색상 유지가 보장되는 프리미엄 브랜드는 이러한 추세를 파악하여 고객을 더 높은 이익률의 SKU로 유도하고 있습니다. 신규 주택 착공 건수의 구조적 둔화로 인해 가처분 소득이 개보수 지출로 전환되어 완성된 주택 수는 감소하는 추세이지만, 가구당 가치는 상승하고 있습니다. 수요는 GB/T 33372-2020 배출 기준을 충족하는 인테리어 페인트, 수성 프라이머, 무취 탑 코트에 집중되어 있습니다. 지속적인 성장은 가계 소득 증가와 전체 부동산 시장 동향에 따라 달라지겠지만, 단기적으로는 이미 아시아태평양의 페인트 및 코팅 시장에 눈에 띄는 상승 효과를 가져왔습니다.

중국 GB/T 33372-2020 표준에 따라 건축용 도료의 VOC 허용 기준치가 120g/L로 낮아졌고, 각 성의 시행 캠페인으로 인해 감사 빈도가 증가하고 있습니다. 연구개발 능력과 수성 분산 기술 기반이 부족한 중소 제조업체는 재배합 비용 부담과 함께 규정 준수 기한을 넘길 경우 공급망 혼란의 위험에 직면해 있습니다. 베트남과 말레이시아에서도 비슷한 규제가 마련되고 있으며, 국경을 넘나드는 공급업체들은 제품 라인의 통합, 다른 SKU의 재고 확보 또는 저마진 용제 카테고리에서 철수해야 하는 상황에 처해 있습니다. 장기적으로는 고부가가치 수성 제품에 대한 수요가 촉진되는 반면, 단기적으로는 생산 능력의 합리화와 전환 비용이 총 생산량을 억제하여 아시아태평양의 페인트 및 코팅 시장의 발전 모멘텀을 둔화시키고 있습니다.

수성 페인트는 2025년 아시아태평양 페인트 및 코팅 시장 점유율의 56.43%를 차지할 것으로 예상되며, 2031년까지 연평균 복합 성장률(CAGR) 5.52%로 확대될 것으로 예측됩니다. 2018년 상하이에서 시행된 외벽용 용제 금지령은 광둥성, 베이징시, 연안 산업단지의 정책 파급을 촉진하여 건설업체를 저VOC, 저냄새 대체품으로 이끌었습니다. 이러한 배경에서 아시아태평양의 페인트 및 코팅 시장은 점진적인 채택에서 체계적인 교체로 전환하고 있습니다. 이는 용제계 알키드 수지와 동등한 내막성, 조기 내수성, 빠른 재도장 시간을 실현하는 신개발 아크릴 에멀전이 기여하고 있습니다. 자동차 제조업체는 동남아시아의 잦은 습도 변동에 견딜 수 있는 수성 베이스코트-클리어코트 적층 기술을 입증하여 기존의 품질 우려를 해소했습니다.

분체도료, UV 경화형 도료, 고형분 도료는 아시아태평양의 도료 및 코팅 산업에서 규모는 작지만 빠르게 성장하고 있는 분야로, 특히 금속 가구, 가전제품, 3C 전자기기에서 채택이 증가하고 있습니다. 분말도료는 VOC 제로 특성뿐만 아니라 95% 이상의 회수 효율로 싱가포르와 호주의 ESG 중심 조달 정책에 부합하는 제품입니다. 그러나 소성로와 전처리 라인의 설비투자 비용이 자금력이 부족한 중소기업 클러스터에 보급을 가로막고 있습니다.

The Asia-Pacific Paints and Coatings Market is expected to grow from USD 81.22 billion in 2025 to USD 85.07 billion in 2026 and is forecast to reach USD 107.22 billion by 2031 at 4.74% CAGR over 2026-2031.

Tightening environmental regulations, accelerating urbanization, and the rapid scale-up of automotive and industrial production underpin sustained demand, while the shift to water-borne platforms positions technology leaders for margin resilience. China retained dominance with a 56.42% share in 2024, yet India is setting the growth pace through 2030 as infrastructure outlays and housing upgrades gain momentum. Raw-material volatility, especially in titanium-dioxide pricing, keeps margin management in sharp focus, and strategy realignments, such as divestitures by BASF and AkzoNobel, signal that scale, portfolio balance, and regional depth will define competitive advantage. Digitalized color tools, faster repaint cycles in premium urban housing, and policy-backed "green ship" retrofits add incremental layers of demand that distinguish the Asia-Pacific paints and coatings market from more mature chemical value chains.

Surging construction activity in Indonesia, Thailand, Vietnam, Malaysia, and the Philippines continues to lift architectural and protective coating volumes. Indonesia is on track to become the world's third-largest construction market by 2025, contributing 9% to national GDP while growing 13% year-on-year. Large transport corridors, industrial estates, and affordable-housing programs multiply coating touchpoints across concrete, steel, and wood substrates. International contractors typically specify low-VOC paints that align with green-building certifications, further tilting demand toward water-borne chemistry. Foreign direct investment in automotive and electronics clusters is also pushing orders for high-performance OEM, floor, and machinery coatings. Continued inflows hinge on macroeconomic stability and geopolitical calm, but near-term backlogs keep the Asia-Pacific paints and coatings market well supplied with construction-linked volume upside.

China's mature property markets are experiencing shorter repaint intervals as owners prioritize aesthetic upgrades and asset preservation. Nippon Paint reported growth in Tier-1 and Tier-2 cities where repaint cycles have narrowed from 5-7 years to 3-5 years. Premium brands able to guarantee color retention for extended periods are exploiting the trend to trade customers up to higher-margin SKUs. Structural deceleration in new housing starts has redirected disposable incomes toward renovation outlays, raising value per dwelling even as unit completions soften. Demand is concentrated in interior finishes, water-borne primers and odor-free top-coats that meet GB/T 33372-2020 emission limits. Sustained momentum will depend on household income growth and sentiment in the broader real-estate market, yet the near-term uplift is already material for the Asia-Pacific paints and coatings market.

China's GB/T 33372-2020 standard lowered permissible VOC thresholds for architectural coatings to 120 g/L, and provincial enforcement campaigns have intensified audit frequency. Smaller manufacturers lacking research and development and water-borne dispersion infrastructure face reformulation expenses and risk supply-chain disruptions if compliance deadlines lapse. Similar directives are taking shape in Vietnam and Malaysia, pushing cross-border suppliers to harmonize product lines, stock separate SKUs or exit low-margin solvent categories. While the long-term net effect channels demand into higher-value water-borne offerings, near-term capacity rationalization and transition costs suppress overall output, trimming Asia-Pacific paints and coatings market momentum.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Water-borne formulations captured 56.43% of the Asia-Pacific paints and coatings market share in 2025 and are projected to record a 5.52% CAGR through 2031. Shanghai's 2018 exterior-wall solvent ban crystallized a wider policy wave across Guangdong, Beijing, and coastal industrial parks, steering builders toward low-VOC and low-odor alternatives. The Asia-Pacific paints and coatings market has therefore shifted from incremental adoption to systemic replacement, helped by new acrylic emulsions that deliver block resistance, early-water resistance, and rapid re-coat times comparable with solvent-borne alkyds. Automotive OEMs have validated water-borne base-coat clear-coat stacks that withstand humidity swings common to Southeast Asia, erasing previous quality concerns.

Powder, UV-curable, and high-solids systems together account for a smaller but fast-growing slice of the Asia-Pacific paints and coatings industry, particularly in metal furniture, appliances, and 3C electronics. Powder's zero-VOC credentials, plus reclamation efficiencies above 95%, appeal to ESG-driven procurement policies in Singapore and Australia. However, capital costs for ovens and pre-treatment lines limit penetration in cash-constrained SME clusters.

The Asia-Pacific Paints and Coatings Market Report is Segmented by Technology (Water-Borne, Solvent-Borne, Powder Coating, and Other Technologies), Resin Type (Acrylic, Alkyd, Polyurethane, and More), End-User Industry (Architectural/Decorative, Automotive, Wood, and More), and Geography (China, India, Japan, South Korea, Australia and New Zealand, Indonesia, and More). The Market Forecasts are Provided in Terms of Value (USD).