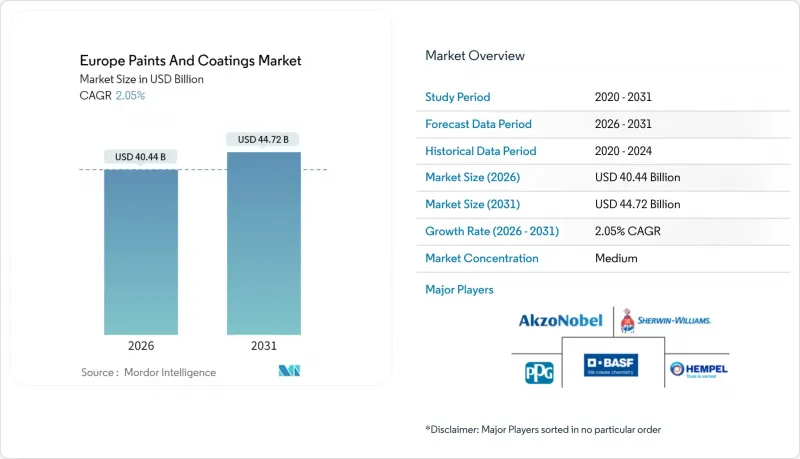

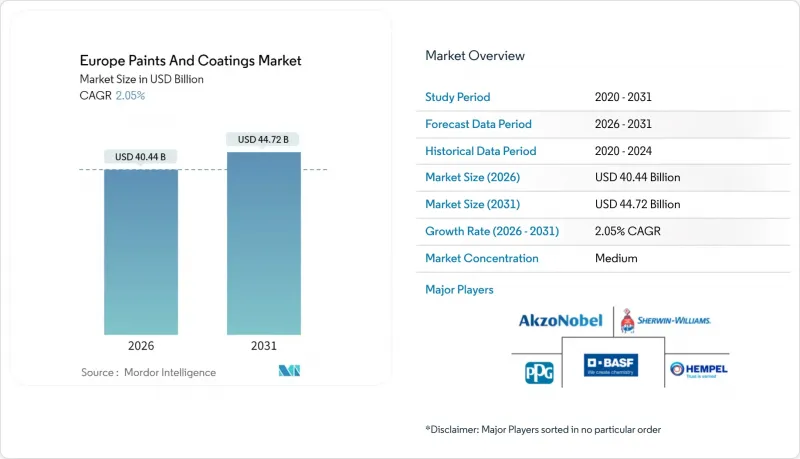

유럽의 페인트 및 코팅 시장은 2025년 396억 3,000만 달러에서 2026년에는 404억 4,000만 달러로 성장하고, 2026-2031년 CAGR 2.05%로 성장을 지속하여, 2031년에는 447억 2,000만 달러에 이를 것으로 예측됩니다.

유럽의 페인트 및 코팅 시장은 서유럽 국가에서 성숙기에 접어들었지만, 개보수 활동, 전기자동차 생산, 재생에너지 인프라가 고부가가치 수요를 안정적으로 확보하고 있습니다. 이러한 성장은 엄격한 VOC 규제를 충족시키면서 도포 효율을 향상시키는 프리미엄 수성 배합 제품에 의해 뒷받침되고 있습니다. 특히 이산화티타늄과 같은 원자재 비용 압력으로 인해 조달 전략이 재구성되고 있습니다. 중국산 제품에 대한 반덤핑 관세 부과로 인해 조달처 다변화가 촉진되고 있는 것이 그 배경입니다. 지역별 분절화로 가격경쟁은 억제되고 있지만, 다국적 기업들은 점유율 방어를 위해 공장 통합과 기술 업그레이드를 가속화하고 있습니다. 현재 경쟁의 초점은 지속가능성에 대한 노력으로 옮겨가고 있으며, 바이오 바인더와 나노기술을 활용한 보호 시스템이 시험 단계에서 상업적 도입으로 전환되고 있습니다.

유럽 그린딜(Green Deal)에 힘입어 2030년까지 3,500만 채의 건물 개보수 프로그램이 추진되고 있으며, 평방미터당 특수 도료 소비량은 신축 프로젝트보다 훨씬 더 많이 소비되고 있습니다. 에너지 효율화를 목적으로 한 석조 건축물의 개보수에는 내장용 프라이머, 엘라스토머계 실러, 저VOC 탑코트가 표준 사양으로 적용되고 있습니다. 건축용 도료 개발자들은 역사적인 건축물의 기질에 수분을 가두지 않고 더 엄격한 단열 규정을 충족시키기 위해 통기성과 방습 성능을 중요시하고 있습니다. 공공 부문의 보조금은 중소기업의 일자리 창출로 이어졌지만, 통합된 색조 시스템과 적시 물류 네트워크로 인해 대형 공급업체가 고급 부문을 장악하고 있습니다. 프랑스, 이탈리아, 스페인의 오래된 주택 재고가 U 값 목표를 달성하기 위해 다층 코팅 시스템이 필요하기 때문에 유럽의 페인트 및 코팅 시장은 혜택을 받고 있습니다. 소매 전문가에 따르면, 가정 내 환경의 건강 증진을 위해 항균 및 방오 마감재 선택이 증가하고, 평균 구매 단가도 상승하고 있다고 합니다.

해상풍력 발전 용량은 2030년까지 10배인 300GW로 확대될 것으로 예상되며, 각 터빈 타워, 나셀, 블레이드에는 1기당 200-300리터의 내식성 에폭시-폴리우레탄 복합도료가 요구됩니다. 보호 도료 제조업체는 북해의 저온 환경에서도 경화 가능한 표면 불균일 대응 프라이머를 개발하여 연중 설치가 가능합니다. 자산 소유주들은 25년의 내구성 보증을 요구하고 있으며, 도막 하부 녹의 진행을 지연시키는 접착 촉진제 및 희생 아연 함유층에 대한 관심이 높아지고 있습니다. 유럽의 페인트 및 코팅 시장에서는 최소한의 오버 스프레이로 고막 두께를 구현하는 자동 혼합 스키드 및 다성분 스프레이 장비에 대한 투자가 집중되고 있습니다. 페인트 제조업체는 유지보수 주기를 예측하는 원격 모니터링 분석 기술을 통해 서비스 계약 수익을 얻고 있습니다. 발트해 지역도 북해와 유사한 성장이 예상되며, 핀란드와 에스토니아가 여러 GW 규모의 프로젝트를 승인함에 따라 내빙성 탑코트 수요 증가가 예상됩니다.

이산화티타늄은 현재 많은 제제 제조업체에서 직접 생산 비용의 40%를 차지하고 있으며, 중국산 수입품에 대한 0.25-0.74유로/kg의 반덤핑 관세로 인해 고가의 유럽산으로 대체되고 있습니다. 주요 그룹들은 조달 안정화를 위해 사우디와 멕시코의 염화티타늄계 제조업체와 다년간의 오프 테이크 계약을 체결하여 헤지하고 있습니다. 중소 제조업체들은 은폐력을 손상시키지 않고 은폐성을 높이는 루틸-안켈라이트 혼합 기술 도입을 가속화하고 있습니다. 이를 통해 유럽 페인트 시장에서 수직적 협력이 강화되어 여러 OEM 제조업체가 직접 안료 할당량을 확보하여 페인트 파트너를 현물 시장의 급등으로부터 보호하고 있습니다. 혁신 예산은 증량제 기술 최적화로 전환되고, 일부 색상 안정성 프로젝트는 연기되었습니다.

아크릴계 페인트는 2025년 매출액의 38.32%를 차지하며 CAGR 3.52%로 유럽의 페인트 및 코팅 시장에서 가장 큰 비중을 차지할 것으로 예측됩니다. 이 화학 구조의 극성이 물 분산성을 촉진하기 때문에 EU 규제에 부합하는 표준 선택이 되었습니다. 알키드계 도료는 광택의 깊이로 인한 미적 아름다움으로 장인의 목공예품 보호라는 틈새 시장에서 선호되고 있지만, 건조시간이 길고 용제 함량이 높아 연간 판매량은 감소하는 추세입니다.

에폭시 수지는 화물칸 라이닝과 교량 데크에서 대체 불가능한 지위를 유지하고 있으며, 유럽의 페인트 및 코팅 시장에서 이 분야의 점유율은 12.35%를 차지하고 있습니다. 그러나 자산 소유주의 유지보수 주기 연장으로 인해 성장은 정체된 상태입니다. 폴리우레탄 수지는 파단 연신율 10% 이상을 중시하는 풍력 터빈 블레이드 생산 라인에서 수요가 확대되고 있습니다. 아크릴 수지는 자동차 클리어 코트 배합에서도 진전을 보이고 있으며, 초분지형 변종은 점도를 증가시키지 않으면서도 내스크래치성을 제공합니다. 분말 도료에서 선호되는 폴리에스테르 수지는 자동차 알루미늄 트림의 인기에 힘입어 단일 공정으로 도포할 수 있는 빠른 경화 특성으로 생산성 향상을 실현하고 있습니다.

유럽의 페인트 및 코팅 시장 보고서는 수지 유형별(아크릴, 알키드, 폴리우레탄 등), 기술별(수성, 솔벤트 기반, 분체 코팅, UV 경화형 코팅), 최종 사용자 산업별(건축, 자동차, 목재, 보호 코팅) 등으로 분류됩니다. 기술(수성, 용제계, 분체도장, UV 경화도장), 최종 사용자 산업(건축, 자동차, 목재, 보호도장 등), 지역(독일, 영국, 프랑스, 이탈리아, 스페인, 러시아, 튀르키예, 기타 유럽) 별로 분류되어 있습니다. 시장 예측은 금액 기준(USD)으로 제공됩니다.

The Europe Paints And Coatings market is expected to grow from USD 39.63 billion in 2025 to USD 40.44 billion in 2026 and is forecast to reach USD 44.72 billion by 2031 at 2.05% CAGR over 2026-2031.

The European paints and coatings market is maturing in Western economies, yet renovation activity, electric-vehicle output, and renewable-energy infrastructure ensure a steady volume of high-value demand. Growth remains anchored in premium, water-borne formulations that satisfy stringent VOC caps while improving application efficiency. Raw-material cost pressures, notably for titanium dioxide, are reshaping sourcing strategies as anti-dumping duties on Chinese grades compel procurement diversification. Regional fragmentation keeps pricing disciplined, but multinationals are accelerating factory consolidations and technology upgrades to defend their share. Competition now hinges on sustainability credentials, with bio-based binders and nano-enabled protective systems moving from pilot scale toward commercial adoption.

Renovation programmes backed by the European Green Deal are stimulating refurbishment of 35 million buildings by 2030, lifting specialty-coatings consumption per square metre well above that of new-build projects. Interior primers, elastomeric sealers, and low-VOC topcoats are now standard specifications for masonry upgrades that target energy efficiency. Architectural formulators emphasise breathability and moisture-barrier performance to meet stricter thermal regulations without trapping humidity in historic substrates. Public-sector grants channel work toward SMEs, yet large suppliers dominate premium segments through integrated tint systems and just-in-time logistics networks. The European paints and coatings market benefits as older housing stock across France, Italy, and Spain requires multiple-layer coating systems to achieve U-value targets. Retail professionals also report higher average ticket values as householders opt for antibacterial and stain-resistant finishes to enhance indoor wellness.

Offshore wind capacity is set to jump tenfold to 300 GW by 2030, and every turbine tower, nacelle, and blade demands corrosion-resistant epoxy-polyurethane stacks of 200-300 litres per unit. Protective coatings suppliers now develop surface-tolerant primers that cure at low North Sea temperatures, allowing year-round deployment. Asset owners specify 25-year durability warranties, intensifying focus on adhesion promoters and sacrificial zinc-rich layers that slow under-film rust creep. The European paints and coatings market attracts investment in automated mixing skids and plural-component spray equipment that achieve high-build thickness with minimal overspray. Coating producers capture service-contract revenue through remote-monitoring analytics that predict maintenance intervals. Growth in the Baltic Sea mirrors North Sea momentum as Finland and Estonia approve multi-GW projects, extending demand for ice-resistant topcoats.

Titanium dioxide now represents 40% of direct production costs for many formulators, and anti-dumping levies of EUR 0.25-0.74 kg on Chinese imports have forced substitution toward higher-priced European capacity. To stabilise procurement, large groups hedge through multi-year offtake contracts with chloride-route producers in Saudi Arabia and Mexico. Smaller firms accelerate rutile-ankerite blends that extend hiding power without compromising opacity. The European paints and coatings market thus witnesses greater vertical cooperation; several OEMs secure direct pigment allocations to insulate their coating partners from spot-market spikes. Innovation budgets shift toward extender-technology optimisation, delaying certain colour-stability projects.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Acrylic systems delivered 38.32% of 2025 sales and are pacing a 3.52% CAGR, commanding the largest slice of the Europe paints and coatings market. The chemistry's polarity promotes water dispersion, making it the default for EU regulatory compliance. Alkyds cling to artisan woodcare niches because of depth-of-gloss aesthetics; however, longer drying times and higher solvent content shrink their volume annually.

Epoxies remain irreplaceable for cargo hold linings and bridge decks, where Europe's paints and coatings market share for the class stays at 12.35% but with flat growth as asset owners elongate maintenance cycles. Polyurethanes flourish in wind-blade production lines that value elongation-at-break above 10%. Acrylics also advance in automotive clearcoat blends, where hyper-branched variants deliver scratch resistance without raising viscosity. Polyester resins, preferred in powder coatings, ride automotive aluminium-trim popularity, with throughput gains from faster curing profiles that permit single-pass application.

The Europe Paints and Coatings Report is Segmented by Resin Type (Acrylic, Alkyd, Polyurethane, and More), Technology (Water-Borne, Solvent-Borne, Powder Coatings, and UV-Cured Coatings), End-User Industry (Architectural, Automotive, Wood, Protective Coatings, and More), and Geography (Germany, United Kingdom, France, Italy, Spain, Russia, Turkey, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).