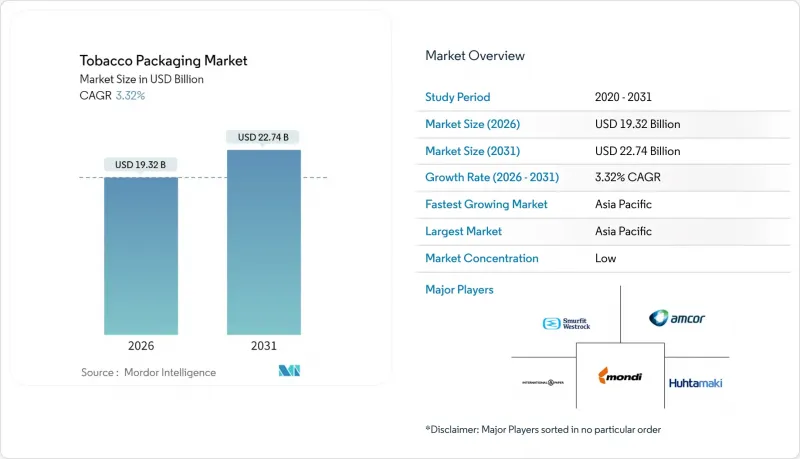

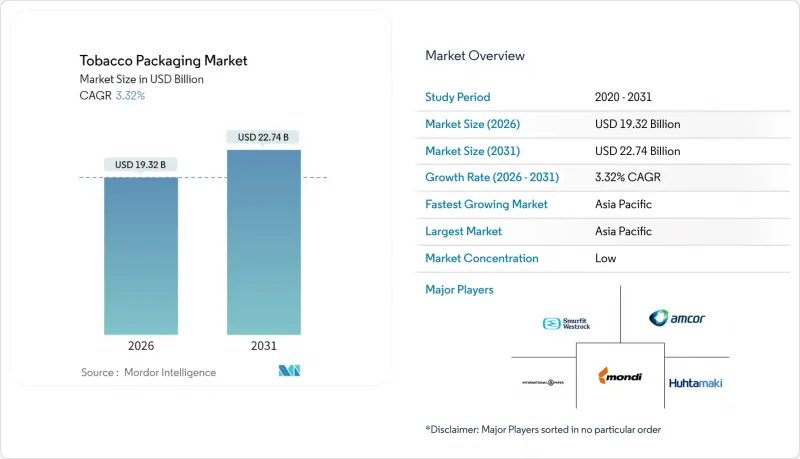

2026년 담배 포장 시장 규모는 193억 2,000만 달러로 추정되며, 2025년 187억 달러에서 성장하며, 2031년에는 227억 4,000만 달러에 달할 것으로 예측됩니다.

2026-2031년 연평균 복합 성장률(CAGR) 3.32%로 확대될 것으로 예측됩니다.

현재 25개 관할권에서 시행되고 있는 무지 포장 의무화, EU 포장 및 포장 폐기물 규제에 따른 100% 재활용 가능 재료로의 전환, 추적 관리 솔루션에 대한 투자 가속화가 결합되어 담배 포장 시장의 가장 강력한 성장 동력이 되고 있습니다. 위조 방지 기술, 종이 기반 배리어 소재, 자동화 지원 포맷을 통합할 수 있는 공급업체는 고소득 지역의 흡연율 감소로 인해 정체되기 쉬운 수요를 포착할 수 있습니다. 판지와 생분해성 플라스틱으로의 소재 전환은 규제 리스크를 줄이는 한편, 습기 및 향기 차단재에 대한 수요를 증가시키고, 호일 라이너, 홀로그램 티어 테이프와 같은 고부가가치 부품에 대한 수요를 지속시킬 것입니다. 아시아태평양은 대규모 소비량과 중국, 일본, 한국의 가열식 담배 포장법의 급속한 조화로 인해 선도적 지위를 유지할 것입니다. 이러한 요인들이 결합되며, 2030년까지 담배 포장 시장은 안정적이면서도 규제 중심의 성장 경로를 따라갈 것입니다.

현재 25개국이 플레인 패키지를 시행하고 있으며, 호주는 2025년부터 담배 막대 본체에 경고그림을 직접 표기하는 정책을 내놓았습니다. 이로 인해 브랜드 이미지는 거의 사라질 것으로 보입니다. 공급업체는 패키지의 75% 이상의 면적을 건강 경고 그래픽에 할당해야 하는 경우에도 패키지의 무결성을 유지하기 위해 구조적 특성을 재설계해야 합니다. 이를 통해 담배 판매량이 급감하더라도 예측 가능한 컴플라이언스 매출을 확보할 수 있습니다. 캐나다의 슬라이드 & 쉘 형식은 경고 표시 면적을 41% 확대하여, 규제 변경이 완전히 새로운 패키지 구조를 촉진하는 좋은 예가 되고 있습니다. 영국에서는 2024년 모든 담배제품에 대한 표준화 확대에 대한 협의가 진행 중이며, 추가적인 진전이 있을 것으로 예측됩니다.

EU의 일회용 플라스틱 지침은 담배 필터가 해안에서 두 번째로 많은 폐기물로 분류되어 각 브랜드는 라미네이트 구조를 재검토해야 합니다. 금속화 필름을 대체할 수 있는 고배리어성 종이 코팅을 채택하면서 수분 함량을 안정화할 필요가 생겼습니다. ITC의 InnovPack은 현재 연간 10만 톤 이상의 재생 판지를 Bioseal 및 Oxyblock 규격으로 가공하고 있으며, 다층 플라스틱과의 대규모 원가경쟁력을 입증하고 있습니다. 이중층 수성 코팅판 조사 결과, 알루미늄 증착지가 폴리머 필름과 동등한 향기 보호 성능을 발휘하면서 퇴비화 목표를 달성하는 것으로 나타났습니다.

캐나다의 2025년 담배 과징금 규정에 따라 제조업체는 매출액에 연동된 연간 과징금을 지불해야 하며, 이는 포장 예산에도 영향을 미치는 비용 압박을 증가시키고 있습니다. 인도네시아의 2024년 규정은 20병 최소 포장 크기를 의무화하여 세제 정책과 포장 디자인의 상호 작용을 명확히 했습니다.

종이 및 판지는 2025년 기준 담배 포장 시장의 82.74%를 차지할 것으로 예상되며, 이는 규제 우선순위와 배리어 코팅 기술의 성숙도를 반영합니다. 플라스틱 부문은 규모는 작지만, 가열식 담배 카트리지 및 어린이용 전자담배 카트리지 및 전자 리퀴드 포드용으로 설계된 다층 필름의 점유율 확대에 힘입어 7.08%의 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 플라스틱 담배 포장 시장 규모는 2026-2031년 10억 6,000만 달러로 증가할 것으로 예측됩니다. 이는 분봉 실패 없이 분당 600팩을 생산할 수 있는 자동화 대응 라미네이트 소재의 보급에 힘입은 것입니다. 알루미늄 포일은 트레저러 런던 알루미늄과 같은 고급 라인에서 향기 유지를 위한 협소하지만 안정적인 역할을 유지하고 있습니다.

리그닌-HDPE 복합재와 해조류 유래 필름에 대한 빠른 연구 결과에 따르면 2030년까지 플라스틱 사용량의 5%를 버진 플라스틱에서 전환할 수 있는 잠재력이 있다고 합니다. 이는 EU의 '100% 재활용 가능한 포장' 목표에 부합합니다. 스마핏 웨스트락의 금속화 배리어를 통합한 하이브리드 보드는 이미 산소 투과율 1g/m2 미만을 달성하면서 일반 폐기물 회수 대응을 유지하고 있으며, 컨버터가 규모를 활용하여 연구실의 획기적인 성과를 빠르게 상용화할 수 있는 실례를 보여주고 있습니다.

2025년, 소매 단위당 건강 경고 표시를 의무화하는 규정으로 인해 1차 포장은 담배 포장 시장 점유율의 65.10%를 차지했습니다. 면세점용 번들 형태 및 추적 관리를 위한 RFID/QR코드 탑재 수요 증가로 인해 2차 포장용 상자는 5.34%의 연평균 복합 성장률(CAGR)로 확대될 것으로 예측됩니다. 온라인 직렬화 기능을 통합한 고속 케이스 포장기의 보급으로 2차 포장 솔루션 시장 규모는 2031년까지 66억 6,000만 달러에 달할 것으로 예측됩니다.

공급업체는 개봉시 홀로그램이 나타나는 스마트 티어 테이프를 통해 부가가치를 제공하고 재사용을 억제합니다. 간선 운송에서는 기업 Scope 3 배출량 감축 목표 달성을 위해 소비 후 원료 30% 이상의 재생 골판지 등급을 운송 포장에 활용합니다. 고급 리지드 박스는 한정 생산으로 계속되고 있으며, 예를 들어 Davidoff의 Winston Churchill 2025 에디션은 재생 보드 심재에 층상 너도밤나무 베니어 베니어를 붙였습니다.

담배 포장 시장 보고서는 재료별(종이/판지, 플라스틱, 금속, 유리, 바이오플라스틱), 포장 유형별(1차 포장, 2차 포장, 벌크 포장, 고급 경질 박스), 제품 형태별(소프트팩, 하드팩, 파우치, 튜브, 스틱), 담배 유형별(흡연용, 무연, 차세대 제품, 담배, 무연, 차세대 제품, 시가), 지역별(북미, 유럽, 아시아, 중동, 중남미, 남미) 등으로 분석됩니다. 시가), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)으로 분석되고 있습니다. 시장 예측은 금액 기준(USD)으로 제시됩니다.

아시아태평양은 2025년 매출의 37.95%를 차지할 것으로 예상되며, 중국, 인도, 인도네시아가 전자담배 기준을 강화하는 동시에 세계 최대 흡연 인구를 유지하면서 연간 6.45% 성장할 것으로 예측됩니다. 아시아태평양의 담배 포장 시장 규모는 2026-2031년 17억 2,000만 달러에 달할 것으로 예상되며, 이는 국내 판지 제조업체의 배리어 코팅 등급 생산 확대에 기인합니다. 중국 일선 도시의 도시화와 프리미엄화도 축제 기간 중 금속화 선물용 캔에 대한 수요를 촉진하고 있습니다.

북미는 소재 혁신의 선두주자이며, 암코의 AmFiber 종이는 2025년 유럽 특허를 취득하고 미국에서 상업적으로 출시될 예정입니다. 이는 궐련형 담배의 오버랩 포장에 있으며, PVdC 필름을 대체하고자 하는 컨버터 업체에 공급됩니다. 캐나다의 연간 담배세와 대형 그래픽 경고 표시로 인해 담배 한 갑당 약 2센트의 준수 비용이 증가하여 담배 판매량이 정체되어 있음에도 불구하고 포장 가치가 소폭 상승할 것으로 예측됩니다.

유럽의 엄격한 PFAS 금지 규제와 2040년까지 담배를 사용하지 않겠다는 목표가 다가옴에 따라 컨버터 기업은 수성 배리어 화학 기술 및 폐쇄 루프 재활용에 대한 투자를 해야 합니다. 중동 및 아프리카에서는 걸프 국가를 중심으로 프리미엄 성장이 예상됩니다. 면세점에서는 금박 엠보싱 처리된 상자를 선호합니다. 남미는 경제 변동으로 인해 진전이 더디지만, 2026년 브라질에서 예정된 전국적인 건강 경고 표시 업데이트는 지역 전체의 인쇄 품질 향상을 촉진할 것으로 예측됩니다.

The tobacco packaging market size in 2026 is estimated at USD 19.32 billion, growing from 2025 value of USD 18.70 billion with 2031 projections showing USD 22.74 billion, growing at 3.32% CAGR over 2026-2031.

Mandatory plain-pack rules now enforced in 25 jurisdictions, the drive for 100% recyclable materials under the EU Packaging and Packaging Waste Regulation, and accelerating investment in track-and-trace solutions together shape the most powerful growth levers for the tobacco packaging market. Suppliers able to integrate anti-counterfeit technology, paper-based barrier materials and automation-ready formats capture volume that would otherwise stagnate as smoking prevalence edges down in high-income regions. Material shifts toward paperboard and biodegradable plastics lower regulatory risk yet increase demand for moisture and aroma barriers, sustaining premiumisation in components such as foil liners and hologram tear tapes. Asia-Pacific retains leadership thanks to large-scale consumption and rapid harmonisation of heated-tobacco packaging laws in China, Japan, and South Korea. Together, these forces keep the tobacco packaging market on a steady yet regulation-dominated growth path through 2030.

Twenty-five countries now enforce plain packaging, and Australia moved warnings directly onto cigarette sticks in 2025, leaving brand imagery almost obsolete. Suppliers must redesign structural features to preserve pack integrity despite 75 %-plus panel space devoted to health graphics, ensuring predictable compliance revenue even where cigarette volumes plateau. Canada's slide-and-shell format enlarged warning area by 41 %, illustrating how rule changes prompt entirely new pack architectures. The UK's 2024 consultation to extend standardisation to all tobacco products signals further momentum.

The EU Single-Use Plastics Directive ranks cigarette filters as the second most littered beach item, prompting brands to overhaul laminates and adopt high-barrier paper coatings that replace metallised films while keeping moisture content stable. ITC's InnovPack now converts more than 100,000 tonnes of recyclable board into Bioseal and Oxyblock formats annually, demonstrating large-scale cost parity with multi-layer plastics. Research on double-layer water-based coated boards shows aluminium-plated paper achieving comparable aroma protection to polymer films yet meeting compostability targets.

Canada's 2025 Tobacco Charges Regulations oblige manufacturers to pay annual levies indexed to sales, adding cost pressure that trickles into packaging budgets. Similar hikes appear in Indonesia's 2024 rule mandating minimum pack sizes of 20 cigarettes, showing how tax policy and packaging design interact.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Paper & paperboard captured 82.74 % of the tobacco packaging market in 2025, reflecting both regulatory preference and maturing barrier-coating technology. The plastics segment, though smaller, will post the highest 7.08 % CAGR as multilayer films tailored for heated-tobacco cartridges and child-resistant e-liquid pods gain share. The tobacco packaging market size for plastics is forecast to add USD 1.06 billion between 2026 and 2031, buoyed by automation-ready laminates that run at 600 packs/minute without seal failure. Aluminium foil maintains a narrow but stable role for aroma retention in premium lines such as Treasurer London Aluminum.

Rapid research into lignin-HDPE blends and seaweed-based films indicates potential to shift a further 5 % volume away from virgin plastic by 2030, aligning with the EU target of 100 % recyclable packs. Smurfit WestRock's hybrid board with integrated metallised barrier already satisfies <1 g/m2 oxygen transmission while remaining curb-side recyclable, demonstrating how converters use scale to commercialise lab breakthroughs swiftly.

Primary packs delivered 65.10 % of the tobacco packaging market share in 2025 thanks to regulatory mandates for health messaging on every retail unit. Secondary cartons will outpace at 5.34 % CAGR, driven by duty-free bundle formats and growing need to embed RFID or QR codes for track-and-trace. Tobacco packaging market size for secondary solutions is projected to touch USD 6.66 billion by 2031, supported by high-speed case packers integrating on-line serialisation.

Suppliers add value through smart tear tapes that reveal holograms when opened, deterring reuse. In line haul, transit packaging leverages recycled corrugated grades exceeding 30 % post-consumer content to meet corporate scope-3 emission commitments. Luxury rigid boxes endure in limited runs, such as Davidoff's Winston Churchill 2025 edition using layered beech veneer over recycled board cores.

The Tobacco Packaging Market Report is Segmented by Material (Paper and Paperboard, Plastics, Metals, Glass, Bioplastics), Packaging Type (Primary, Secondary, Bulk, Luxury Rigid Boxes), Product Form (Soft Pack, Hard Pack, Pouch, Tube and Stick), Tobacco Type (Smoking, Smokeless, Next-Generation Products, Cigars), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are in Value (USD).

Asia-Pacific commanded 37.95 % of revenue in 2025 and will expand 6.45 % annually as China, India and Indonesia tighten e-cigarette standards yet maintain the world's largest smoking populations. Tobacco packaging market size additions in Asia-Pacific will reach USD 1.72 billion over 2026-2031, supported by domestic board mills scaling barrier-coated grades. Urbanisation and premiumisation in tier-one Chinese cities also fuel demand for metallicised gift tins during festival peaks.

North America stays material-innovation leader, with Amcor's AmFiber paper gaining European patent in 2025 and slated for US commercial roll-out, supplying converters aiming to replace PVdC films in cigarette overwrap.Canada's annual tobacco charges and large graphic warnings will lift compliance spend per pack by an estimated 2 US cents, modestly boosting packaging value despite flat cigarette volumes.

Europe faces stringent PFAS bans and the 2040 tobacco-free goal, compelling converters to invest in water-based barrier chemistries and closed-loop recycling. The Middle East & Africa offer pockets of premium growth in the Gulf, where duty-free outlets favour gold-foil embossed cartons. South America's progress is slower amid economic volatility but Brazil's national health-warning refresh slated for 2026 should spark regional print-quality upgrades.