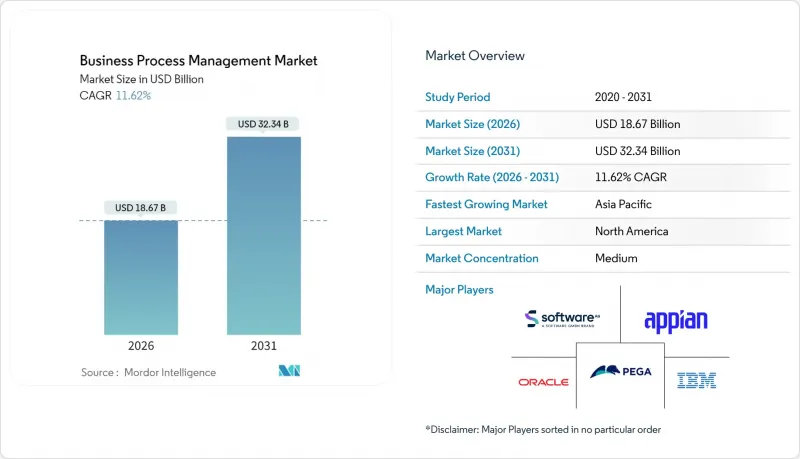

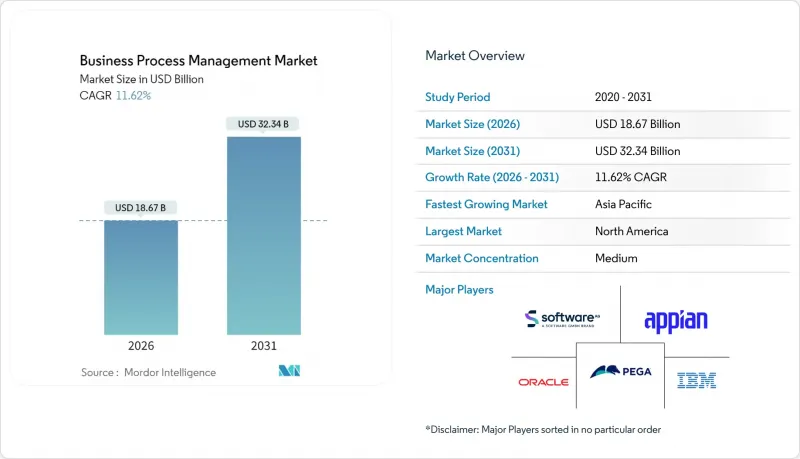

비즈니스 프로세스 관리 시장은 2025년에 167억 3,000만 달러로 평가되며, 2026년 186억 7,000만 달러에서 2031년까지 323억 4,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 11.62%로 예상됩니다.

디지털 우선 운영 모델의 확대, 워크플로우 스위트에 AI 엔진의 통합, 규제 모니터링 강화는 엔드투엔드 프로세스 오케스트레이션 플랫폼에 대한 안정적인 수요를 지원하고 있습니다. 클라우드 네이티브 딜리버리, 로우코드 개발, 프로세스 마이닝을 활용한 디지털 트윈이 융합되어 대기업과 중견기업 모두 가치 실현 시간을 단축하고 있습니다. 아시아태평양의 적극적인 자동화 추진 계획과 BFSI(은행, 금융, 보험) 및 의료 분야의 컴플라이언스 프로그램 적용 범위 확대가 맞물려 성장 잠재력을 더욱 높이고 있습니다. 이에 따라 시장 선도 기업은 분석, 룰 엔진, 로봇 어시스턴트를 통합한 하이퍼자동화 스택을 구축하는 생태계 전략을 가속화하고 있습니다.

2025년까지 BPM 플랫폼의 4분의 3이 로우코드 툴을 내장하여 비즈니스 팀이 깊은 코딩 지식 없이도 워크플로우를 설정할 수 있게 될 것입니다. 이를 통해 프로젝트 납기를 몇 개월에서 몇 주로 단축하고, 초기 도입 단계에서 프로세스 효율을 30% 향상시킬 수 있습니다. Citizen Developer의 도입은 중소기업이 제한된 IT 리소스를 우회하면서 템플릿과 시각적 버전 관리를 통해 거버넌스를 유지할 수 있도록 도와줍니다. Bizagi와 같은 벤더들은 자연 언어 프롬프트에서 모델을 자동 생성하는 AI 에이전트를 확장하여 컴플라이언스를 훼손하지 않고 접근성을 확장합니다.

Camunda Zeebe와 같은 수평적 스케일링 엔진은 클러스터 노드 추가에 따라 처리량이 선형적으로 증가하며, 공공 부문 청구 처리의 초기 도입 기업의 경우 자동화 커버리지가 65% 향상되었습니다. 클라우드 제공은 설비투자를 줄이고, 하이브리드 환경 전체에 대한 내결함성을 보장합니다. 이러한 특성은 Oracle의 최근 분기 클라우드 매출 62억 달러가 지원하고 있습니다. 빠른 커넥터 라이브러리는 통합을 가속화하고, 클라우드 BPM 서비스 소비가 전년 대비 27% 급증한 상황과 일치합니다.

레거시 ERP, 클라우드 SaaS, 틈새 핵심 업무 용도이 혼합된 다층적인 에코시스템은 BPM 통합의 범위를 확장하고, ERP에 대한 종단적 연구에서 보고된 바와 같이 초기 예산 추정치를 두 배로 늘릴 수 있습니다. BPM Institute는 API 깊이, 이벤트 스트림, 데이터 매핑의 요구사항을 간과하면 프로젝트 실패 확률과 총소유비용이 높아진다고 경고하고 있습니다.

비즈니스 프로세스 관리 시장 규모에서 하이브리드 배포는 17.80%를 차지하며 2031년까지 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 한편, 클라우드는 2025년 61.35%의 점유율을 유지했습니다. 금융 규제 당국의 위치 기반 데이터 규정으로 인해 On-Premise 감사 추적이 필요하지만 탄력적인 분석 샌드박스의 이점을 누릴 수 있는 워크로드에는 하이브리드가 최적의 선택이 될 수 있습니다.

조직들은 하이브리드의 위험 균형 특성이 고비용의 대량 트랜잭션 코어를 대량으로 이전하지 않고도 현대화를 지속할 수 있는 중요한 요소라고 지적하고 있습니다. 예를 들어 유럽의 GDPR(EU 개인정보보호규정) 규정에 따라 정부 기관은 개인 데이터를 로컬 서버에 보관하면서 문서 분류에는 클라우드 AI 엔진을 활용하도록 요구하고 있습니다. 미국 재향군인회가 카문다의 유연한 파티셔닝 기술을 통해 자동화율을 65% 향상시킨 사례가 이를 잘 보여줍니다. 통합 기반이 성숙해짐에 따라 2031년까지 하이브리드 환경의 비즈니스 프로세스 관리 시장 점유율이 확대될 것으로 예상되지만, 신규 도입 환경에서 순수 퍼블릭 클라우드의 우위는 흔들리지 않을 것으로 보입니다.

프로세스 자동화가 39.20%의 점유율로 매출을 주도한 반면, 프로세스 마이닝 및 분석은 22.10%의 연평균 복합 성장률(CAGR)로 성장하여 비즈니스 프로세스 관리 시장에서 가장 역동적인 부문이 될 것으로 예측됩니다. 초기 도입 기업은 기존 업무 자동화로는 구현할 수 없었던 능동적 이상 감지 및 예측적 워크플로우 조정으로 방향을 전환하고 있습니다.

플랫폼의 로드맵은 마이닝 모듈과 실시간 추천 기능이 통합되어 전환 비용 증가와 비용 절감까지의 기간을 단축하는 것을 목표로 하고 있습니다. 2024년 포브스 클라우드 100에서 셀로니스의 순위는 프로세스 인텔리전스에 대한 시장의 높은 수요를 보여주며, 심비오 등의 인수는 디자인 거버넌스 및 지속적 개선 분야로의 진출을 의미합니다. 컨텐츠 관리, 사례 관리, 규칙 엔진은 전문적인 중요성을 유지하지만, 성장의 주역은 분석 중심의 오케스트레이션 제품군으로 옮겨가고 있습니다.

북미는 성숙한 클라우드 배포, 높은 수준의 통합 기술력, AI 지원 서비스 프로바이더의 밀집된 생태계로 인해 2025년 비즈니스 프로세스 관리 시장 규모의 41.10%를 차지할 것으로 예측됩니다. 금융 서비스, 공공 부문, 기술 분야가 지역 수요의 대부분을 차지하고 있으며, 하이퍼 자동화 시범 프로젝트가 꾸준히 대규모 프로그램으로 전환되고 있습니다. 업체 간 경쟁이 치열해지면서 지속적인 기능 혁신을 촉진하고, 구독 가격 책정 혁신을 촉진하고 있습니다.

아시아태평양은 2031년까지 14.20%의 연평균 복합 성장률(CAGR)로 확대될 것으로 예측됩니다. 이는 인도, 인도네시아, 베트남의 정부 주도의 디지털 전환 정책이 자동화 예산을 BPM 플랫폼으로 유도하고 있음을 반영하고 있습니다. IBM의 조사에 따르면 아시아태평양 기업의 71%가 디지털 투자에 대한 완전한 매출을 얻기 위해 고군분투하고 있으며, BPM은 엔드투엔드 최적화를 위한 구조적 프레임워크로 자리매김하고 있습니다. 통신, E-Commerce, 공공 부문 디지털 ID 체계가 초기 도입의 중점 분야입니다. 로우코드에 대한 접근은 빠르게 성장하는 중소기업의 도입 리스크를 더욱 줄여줍니다.

유럽에서는 GDPR(EU 개인정보보호규정), ESG 보고, 새로운 AI 법규의 요구로 인해 기업이 데이터 계보 및 동의 관리를 조정된 프로세스에 통합해야 하는 상황이 발생하여 꾸준한 성장을 유지하고 있습니다. 라틴아메리카에서는 브라질에서 1억 3,000만 명의 사용자에게 서비스를 제공하는 실시간 결제 시스템 'PIX'로 대표되는 핀테크의 급격한 성장이 백오피스 업무 조정 및 리스크 분석 모듈에 대한 수요의 연쇄를 만들어내고 있습니다. 중동 및 아프리카에서는 국가 디지털 정부 헌장(National Digital Government Charter)이 세금, 세관, 시민 서비스 기능의 워크플로우 현대화를 재정적으로 지원하는 등 선택적 가속화가 이루어지고 있습니다.

The business process management market was valued at USD 16.73 billion in 2025 and estimated to grow from USD 18.67 billion in 2026 to reach USD 32.34 billion by 2031, at a CAGR of 11.62% during the forecast period (2026-2031).

Expanding digital-first operating models, the integration of AI engines into workflow suites, and heightened regulatory oversight are reinforcing steady demand for end-to-end process orchestration platforms. Cloud-native delivery, low-code development, and process-mining-enabled digital twins are converging to reduce time-to-value for both enterprise and mid-market adopters. Asia-Pacific's aggressive automation agenda, combined with the widening scope of compliance programs across BFSI and healthcare, further amplifies growth potential. Market leaders are therefore accelerating ecosystem plays that blend analytics, rules engines, and robotic assistants into unified hyper-automation stacks.

Three out of four BPM platforms embed low-code tooling in 2025, allowing business teams to configure workflows without deep coding knowledge, which trims project delivery cycles from months to weeks and lifts process efficiency by 30% in early programs .Citizen-developer rollouts help SMEs bypass scarce IT resources while preserving governance through templates and visual version control . Vendors such as Bizagi extend AI agents that auto-generate models from natural-language prompts, broadening access without jeopardizing compliance.

Horizontal scale-out engines like Camunda Zeebe maintain linear throughput growth as cluster nodes are added, which delivers 65% gains in automation coverage for early adopters in public-sector claims processing. Cloud delivery mitigates capex and ensures fault tolerance across hybrid footprints, an attribute underscored by USD 6.2 billion in Oracle's latest quarterly cloud revenue . Rapid connector libraries accelerate integration, aligning with the 27% YoY surge in cloud BPM services consumption.

Multi-layered ecosystems blending legacy ERPs, cloud SaaS, and niche line-of-business apps inflate BPM integration scopes and can double original budget estimates, as documented in longitudinal ERP studies. The BPM Institute warns that overlooking API depth, event streams, and data-mapping demands elevates project-failure odds and total cost of ownership.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Hybrid deployment accounted for 17.80% of the business process management market size and is forecast to post the fastest CAGR through 2031, whereas cloud retained 61.35% share in 2025. Financial regulators' location-based data rules make hybrid the preferred pathway for workloads requiring on-premise audit trails yet benefiting from elastic analytics sandboxes.

Organizations cite hybrid's risk-balanced profile as critical to sustain modernization while avoiding expensive wholesale migration of high-volume transactional cores. Europe's GDPR mandates, for instance, push government agencies to retain personal data in local servers while tapping cloud AI engines for document classification, exemplified by the U.S. Veterans Affairs' 65% automation rate leap using Camunda's flexible partitioning. As integration fabrics mature, hybrid footprints are expected to capture a larger slice of the business process management market by 2031 without displacing pure public-cloud exemplars in greenfield contexts.

Process automation dominated revenue with 39.20% share, yet process mining and analytics is set to expand at 22.10% CAGR, making it the most dynamic segment within the business process management market. Early adopters pivot toward proactive anomaly detection and predictive workflow tuning, capabilities that conventional task automation lacks.

Platform roadmaps now bundle mining modules with real-time recommendations, thereby raising switching costs and shrinking time to savings. Celonis' ranking in the 2024 Forbes Cloud 100 underlines market appetite for process intelligence, while acquisitions such as Symbio extend reach into design governance and continuous improvement. Content management, case management, and rule engines retain specialist relevance but cede headline growth to analytics-centric orchestration suites.

The Business Process Management Market Report Segments the Industry Into by Deployment (Cloud, On-Premise), by Solution (Process Improvement, Process Automation, Content and Document Management, and More), by End-User Industry (Banking, Financial Services, and Insurance (BFSI), Government and Defense, Healthcare, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America accounted for 41.10% of the business process management market size in 2025 thanks to mature cloud adoption, deep integration skill sets, and a dense ecosystem of AI-enabled service providers. Financial services, public sector, and technology verticals represent the bulk of regional demand, with hyper-automation pilots shifting steadily into scaled programs. Vendor competition is pronounced, spurring continuous feature refresh and driving subscription-pricing innovations.

Asia-Pacific is on track for a 14.20% CAGR to 2031, reflecting government-backed digital-transformation mandates across India, Indonesia, and Vietnam that funnel automation budgets into BPM platforms. IBM's survey shows 71% of Asia-Pacific enterprises struggle to unlock full digital investment returns, positioning BPM as the structural framework for end-to-end optimization. Telecommunications, e-commerce, and public-sector digital-identity schemes are early adoption hotspots; low-code access further de-risks adoption for burgeoning SMEs.

Europe maintains steady growth buoyed by GDPR, ESG reporting, and emerging AI-act requirements that force enterprises to codify data lineage and consent management into orchestrated processes. Latin America's fintech surge, exemplified by Brazil's PIX real-time payment rails serving 130 million users, creates a demand cascade for back-office orchestration and risk analysis modules. Middle East and Africa see selective acceleration where national digital-government charters bankroll workflow modernization for tax, customs, and citizen-service functions.