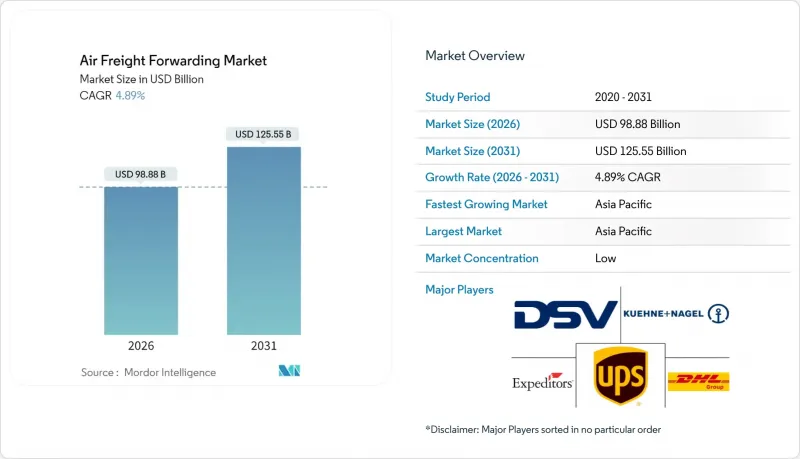

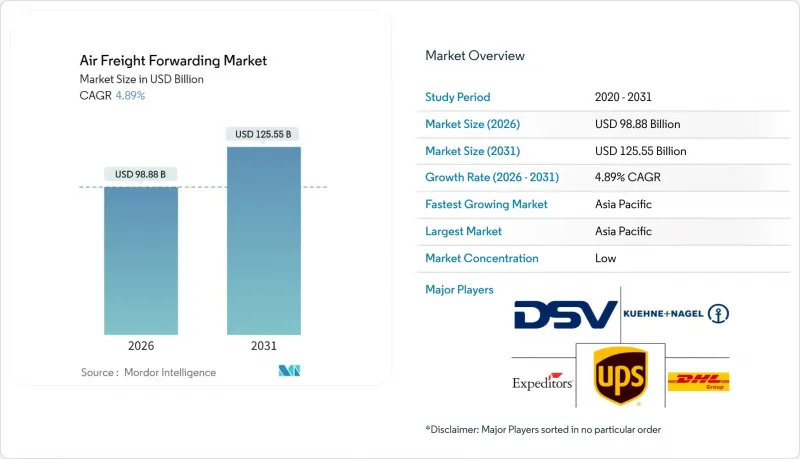

항공 화물 운송 시장은 2025년에 942억 7,000만 달러로 평가되었으며, 2026년 988억 8,000만 달러에서 2031년까지 1,255억 5,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 4.89%로 예상됩니다.

성장 요인으로는 탄탄한 국경 간 E-Commerce, 온도 관리가 필요한 의약품의 급증, 화물기 전환 프로그램의 지속적인 시행으로 화물칸 용량 부족을 보완하고 있습니다. 경쟁 환경에서는 규모 확대를 위한 합병이 두드러지고 있으며, DSV와 쉥커의 통합으로 주요 무역 루트의 가격 결정력과 계약 협상이 재구성되고 있습니다. 실시간 화물 시각화 도구를 포함한 디지털화는 서비스의 신뢰성을 향상시키고 프리미엄 가격 책정을 가능하게 합니다. 한편, 지속가능성에 대한 요구와 제트 연료 가격의 변동은 포워더의 수익률 관리를 복잡하게 만들고, 전략적 운송 능력의 다양화를 촉진하고 있습니다.

현재 국경 간 EC는 아시아발 항공화물 물동량의 50% 이상을 차지하고 있으며, 성수기의 타임라인을 단축시키는 동시에 포워더의 특급 운송 능력에 대한 수요를 확대시키고 있습니다. 2025년까지 전 세계 온라인 소매 보급률이 24%, 미국에서는 26%에 달할 것으로 예상되며, 해상 운송보다 항공 운송을 우선시하는 신속한 운송 솔루션에 대한 수요가 강화되고 있습니다. 2025년 8월 29일로 예정되어 있는 미국의 데미니미스(소액물품) 면세조치 폐지는 통관 절차의 복잡성을 초래하고, 컴플라이언스 부담 경감을 위해 화주들이 화물을 집적화하려는 움직임으로 인해 국제 소포 화물의 증가가 예상됩니다. 이에 대해 포워더들은 특히 아시아-북미 노선 등 소량 소포 밀도가 높은 노선에 블록 스페이스 계약을 재분배하고, 견적 주기를 단축하는 API 기반 예약 시스템을 도입하고 있습니다. 이러한 움직임은 수익성 변동성을 높이는 한편, 계절적 수요 급증에 대응할 수 있는 네트워크 용량의 유연성을 갖춘 사업자에게 유리하게 작용합니다.

제조업의 지역화로 인해 기업들이 최저 비용 조달보다 탄력성을 우선시하는 가운데, 북미 중심의 새로운 운송 회랑이 탄생하고 있습니다. 이로 인해 샌버나디노 국제공항과 윌밍턴 에어파크 등 미국의 지방 공항들은 2024년과 2025년에 기록적인 화물 처리량 증가를 보였습니다. 니어쇼어링의 움직임은 혼잡한 연안 게이트웨이에서 트럭에서 항공기로 신속하게 운송할 수 있는 내륙 시설로 화물을 이동시켜 고부가가치 전자제품 및 자동차 부품의 가치사슬의 민첩성을 높이고 있습니다. 티후아나와 피닉스 메사 게이트웨이 공항과 같은 국경 간 허브는 전문적인 인프라가 멕시코와 미국의 E-Commerce 흐름을 어떻게 가속화할 수 있는지를 보여줍니다. 분산형 네트워크는 주요 공항의 슬롯 제약을 완화하고 지정학적 리스크를 분산시킵니다. 포워더는 이러한 경로를 활용하여 보다 짧은 보충 주기를 원하는 고객들을 위한 서비스 제공의 차별화를 꾀하고 있습니다.

국제항공 운송협회(IATA)는 2025년 제트연료 평균 가격을 배럴당 87달러(2024년 99달러)로 예측하고 있지만, 연료비는 여전히 항공사 운영비용의 26.4%를 차지하며 포워더의 조달 마진에 압박을 가하고 있습니다. 지속가능한 항공 연료(SAF) 의무화로 인해 SAF가 등유보다 훨씬 높은 가격에 거래되고 있어 비용 변동성이 커지고 있습니다. 생산량은 2025년 7억 1,326만 갤런에 달할 것으로 예상되지만, 공급 제한으로 인해 가격은 고공행진을 이어가고 있습니다. 포워더는 지수 연동 계약으로 위험을 헤지하고 있지만, 중소 화주들은 연료 할증료 인상에 저항하는 경우가 많아 마진에 압박을 받고 있습니다. 순 제로 목표 달성 의무로 인해 항공사는 비용에 관계없이 SAF를 채택할 수밖에 없으며, 항공화물 경제에 구조적인 가격 리스크가 내재되어 있습니다.

일반화물은 2025년 매출의 61.35%를 차지했으며, 전자제품, 의류, 예비 부품의 취급량이 항공 화물 운송 시장 규모를 견인할 것으로 보입니다. 가격 경쟁의 심화와 모달 시프트 선택의 증가로 인해 그 성장률은 완만하게 유지되고 있습니다. 특수화물 및 기타 부문은 온도 관리가 필요한 의약품, 위험물, 고가 전자제품 등 고도의 서비스 수준을 요구하는 화물에 대한 수요로 인해 2026년부터 2031년까지 연평균 4.38%의 성장률을 보일 것으로 예상됩니다. 이 부문은 IATA와 ICAO의 규제로 인한 진입장벽이 신규 진입자의 진입을 제한하고 매력적인 수익률을 뒷받침하는 혜택을 누리고 있습니다.

화물기로의 개조는 특히 특수화물에 큰 이점을 제공합니다. 주갑판 접근과 특정 적재 구성으로 인해 복부 화물실보다 대형 물품을 더 쉽게 취급할 수 있기 때문입니다. DHL이 2025년 인수한 CRYOPDP(연간 60만 건 이상의 임상시험 및 바이오의약품 운송을 관리하는 회사)는 특수화물 운송 역량에 대한 전략적 투자를 보여주는 사례입니다. 일반화물 운송은 E-Commerce의 급증으로 회복력을 유지하고 있지만, 화주들이 기본 서비스를 상품화하면서 수익률 하락이 지속되고 있습니다. 이에 반해 특수화물 운송은 가격 결정력을 유지하고 있으며, 유류할증료 논의로부터 사업자를 보호하고, 높은 서비스 제공업체가 보유한 항공 화물 운송 시장 점유율에 긍정적으로 기여하고 있습니다.

아시아태평양은 2025년 세계 매출의 34.62%를 차지했으며, 중국의 수출 엔진, 인도의 6-9% 화물 성장 전망, 역내 E-Commerce 확대에 힘입어 2026년부터 2031년까지 CAGR 5.14%로 성장할 것으로 전망됩니다. 인도에서 와이드바디 화물기의 부족은 신속하게 운송 능력을 투입할 수 있는 포워더에게 성장의 기회를 제공하고 있습니다. 한편, 앵커리지와 같은 허브공항은 효율적인 태평양 횡단 운송을 가능하게 하고 있습니다.

북미는 잘 구축된 E-Commerce 인프라와 멕시코-캐나다와의 니어쇼어링 무역으로 인해 여전히 큰 점유율을 유지하고 있습니다. 지역 게이트웨이는 정시성 화물 수요에 대응하기 위해 확장되고 있으며, 샌버나디노나 윌밍턴과 같은 내륙 공항이 기존 로스앤젤레스나 뉴욕을 경유하던 화물량을 흡수하는 사례가 두드러집니다. 유럽에 비해 환경 규제 압력이 낮기 때문에 특송화물 서비스는 성장의 여지가 남아 있습니다.

유럽에서는 환경 규제가 강화되면서 긴급성이 낮은 화물은 해운이나 철도 운송으로 전환하는 경향이 있습니다. 그러나 의약품과 고부가가치 전자제품은 항공화물 수요를 지탱하고 있으며, 항공사는 엄격한 슬롯 배분 속에서 합작투자를 통해 운송 능력을 최적화하고 있습니다. 중동 및 아프리카는 아시아, 유럽, 아프리카를 연결하는 연결 허브 역할을 합니다. 데이터센터 및 E-Commerce 인프라에 대한 투자와 지리적 이점이 결합되어 IT 장비 및 신선식품을 위한 전문 화물 운송을 촉진하고 있습니다.

The Air Freight Forwarding Market was valued at USD 94.27 billion in 2025 and estimated to grow from USD 98.88 billion in 2026 to reach USD 125.55 billion by 2031, at a CAGR of 4.89% during the forecast period (2026-2031).

Growth stems from resilient cross-border e-commerce, a surge in temperature-controlled pharmaceuticals, and sustained freighter-conversion programs that counteract belly-hold capacity shortages. Competitive activity is marked by scale-seeking mergers, with the DSV-Schenker combination reshaping pricing power and contract negotiations across major trade lanes. Digitalization, including real-time cargo-visibility tools, improves service reliability and enables premium pricing. At the same time, sustainability mandates and volatile jet-fuel costs complicate forwarders' margin management and prompt strategic capacity diversification.

Cross-border e-commerce now represents more than 50% of Asia-originating air cargo volumes, compressing peak-season timelines and amplifying forwarder demand for express capacity. It is forecasted that global online retail penetration to reach 24% worldwide and 26% in the United States by 2025, reinforcing demand for fast transit solutions that favor air over ocean. The scheduled removal of the U.S. de minimis exemption on August 29, 2025, increases customs-clearance complexity and is expected to lift international parcel volumes as shippers consolidate shipments to reduce compliance burdens. Forwarders respond by reallocating block-space agreements toward lanes with high small-parcel density, particularly Asia-North America, while deploying API-based booking engines that shorten quotation cycles. These dynamics raise yield volatility yet reward operators that can flex network capacity to seasonal surges.

Regionalization of manufacturing has spawned new North America-centric corridors as companies prioritize resilience over lowest-cost sourcing, pushing secondary U.S. airports such as San Bernardino International and Wilmington Air Park to record cargo growth in 2024 and 2025. Near-shoring dynamics shift volume away from congested coastal gateways toward inland facilities that offer faster truck-to-air transfers, enhancing supply-chain agility for high-value electronics and automotive components. Cross-border hubs in Tijuana and Phoenix-Mesa Gateway Airport illustrate how specialized infrastructure accelerates Mexico-U.S. e-commerce flows. Distributed networks mitigate slot constraints at tier-1 airports and disperse geopolitical risk. Forwarders leverage these routes to differentiate service offerings aimed at customers seeking shorter replenishment cycles.

IATA projects average jet-fuel at USD 87 per barrel in 2025 versus USD 99 in 2024, yet fuel still accounts for 26.4% of airline operating costs, putting pressure on forwarder procurement margins. Sustainable Aviation Fuel mandates elevate cost variability because SAF trades at a significant premium to kerosene. Production volumes are slated to reach 713.26 million gallons in 2025, but supply limitations keep prices elevated. Forwarders hedge exposure through index-linked contracts, yet smaller shippers often resist fuel-surcharge escalations, squeezing margins. Net-zero commitments press carriers to adopt SAF irrespective of cost, embedding structural price risk into air cargo economics.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

General cargo accounted for 61.35% of 2025 revenues, anchoring the air freight forwarding market size through volumes generated by electronics, apparel, and spare parts. Its growth rate remains modest as pricing competition intensifies and modal shift options proliferate. Special cargo and others are expected to climb at a 4.38% CAGR (2026-2031) because temperature-controlled pharmaceuticals, dangerous goods, and high-value electronics demand elevated service standards. This segment benefits from regulatory moats created by IATA and ICAO rules that limit new entrant penetration and underpin attractive yields.

Freighter conversions have disproportionate benefits for special cargo because main-deck access and specific load configurations accommodate outsized items better than belly holds. DHL's 2025 acquisition of CRYOPDP, which manages more than 600,000 clinical-trial and biopharma shipments annually, demonstrates strategic investment in special-cargo capacity. General cargo retains resilience from the e-commerce surge, but margin dilution persists as shippers commoditize basic services. Specialized cargo, by contrast, maintains pricing power that shields operators from fuel-surcharge debates, contributing positively to the air freight forwarding market share held by high-service providers.

The Air Freight Forwarding Market Report is Segmented by Cargo Type (General Cargo and Special Cargo & Others), Destination (International and Domestic), End-User Industry (E-Commerce & Retail, Manufacturing & Automotive, Healthcare & Pharmaceuticals, Perishables & Fresh Produce, and More), Geography (North America, South America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific accounted for 34.62% of global revenues in 2025 and is projected to advance at a 5.14% CAGR (2026-2031), propelled by China's export engine, India's 6-9% projected cargo growth, and intra-regional e-commerce expansion. Wide-body freighter scarcity in India offers growth prospects for forwarders that can deploy capacity quickly, while hubs like Anchorage enable efficient trans-Pacific transfers.

North America maintains a significant share through embedded e-commerce infrastructure and near-shoring trade with Mexico and Canada. Regional gateways expand to accommodate time-critical flows, with San Bernardino and Wilmington illustrating how inland airports capture volumes that once funneled through Los Angeles or New York. Sustainability pressures are lower relative to Europe, granting growth runway for express freight services.

Europe faces tighter environmental regulations that nudge shippers toward sea or rail for non-urgent cargo. Still, pharmaceuticals and high-value electronics sustain air freight demand, and carriers leverage joint ventures to optimize capacity amid stringent slot allocations. The Middle East and Africa serve as connective hubs linking Asia, Europe, and Africa. Investments in data centers and e-commerce infrastructure, paired with the region's geographic advantage, foster specialized freight flows for IT equipment and perishables.