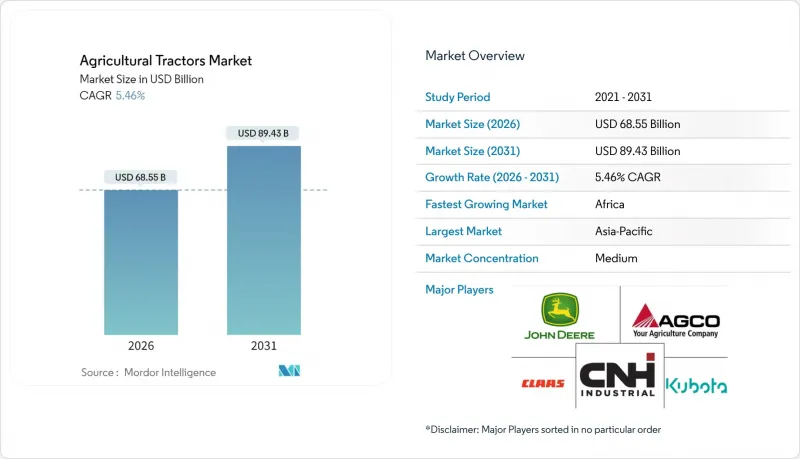

농업용 트랙터 시장은 2025년 650억 달러에서 2026년에는 685억 5,000만 달러로 성장하며, 2026-2031년에 CAGR 5.46%로 추이하며, 2031년까지 894억 3,000만 달러에 달할 것으로 예측됩니다.

현재의 성장은 신흥 국가에서의 지속적인 기계화, 선진국의 정밀농업으로의 빠른 전환 활동, 전기 및 자율주행 트랙터 플랫폼의 조기 상용화에 의해 지원되고 있습니다. 아시아태평양은 가장 강력한 성장세를 유지하고 있으며, 인도의 광범위한 보조금 프로그램과 중국의 농업 현대화 추진은 갱신 수요를 자극하고 있습니다. 한편, 아프리카는 CAADP 2.0이 최소한의 기계화 목표를 설정하고, 우대 대출을 가능하게 함으로써 가장 빠른 성장률을 보이고 있습니다. 40-100마력 부문은 중규모 농업 경영에서 최적의 출력 대 비용 비율을 보여주며, 이륜구동 구성은 낮은 구매 비용과 유지보수의 용이성으로 인해 지배적인 위치를 유지하고 있습니다. 유틸리티 트랙터는 경작부터 자재 운반까지 다양한 농업용도에 대응합니다. 그러나 곡물 대기업이 노동력 부족 해소와 밭 작업 최적화를 위해 무인운전 시스템을 시범 운영하면서 자율주행 트랙터는 폭발적인 성장세를 보이고 있습니다. 세계 벤더 간 통합은 여전히 완만한 수준이지만, 지역 브랜드는 비용 최적화에 초점을 맞춘 제품 라인과 지역 맞춤형 유통망을 통해 계속 성장하고 있습니다. Tier 4 F 엔진공급망 변동과 딜러의 평면도 대출에 영향을 미치는 금리 상승은 단기적인 역풍으로 작용하고 있지만, 정밀농업용 개조 수요와 전동화 구상은 장기적인 성장 모멘텀을 계속 주도하고 있습니다.

인도는 'Xan Credit Card' 제도에 따른 보조금 대출 한도를 2029년까지 연장하고, 농업기계화에 1조 6,800억 루피(202억 달러)를 배정했습니다. 이 중 트랙터가 대출액의 약 15%를 차지하고 있습니다. 브라질에서는 '가족 농업 강화 국가 프로그램'을 통해 3% 금리 대출을 제공하여 40-100마력 모델의 구매 부담을 경감시키고 있습니다. 2022년 이후 인건비가 40-60% 상승함에 따라 5헥타르 이상의 농지에서는 트랙터 도입이 경제적으로 수익성이 높아져 농업용 트랙터 시장의 보급이 가속화되고 있습니다.

60마력 미만의 전기 트랙터는 배출가스 제로를 통한 환기 비용 절감과 지역 규제 대응이 요구되는 과수원이나 온실에서 보급이 진행되고 있습니다. Fendt의 e100 Vario는 최대 6시간 동안 작동할 수 있으며, 유럽연합의 그린딜을 통해 전기 농기계 구매시 최대 40%의 보조금을 받을 수 있습니다. 또한 캘리포니아주 대기자원국은 2030년까지 유틸리티 차량량의 무공해 기준을 의무화하고 있으며, 전동화 추진을 위한 규제적 측면의 순풍이 불고 있습니다. 배터리 팩의 가격은 여전히 1kWh당 400-600달러 수준이지만, 국제에너지기구(IEA)는 2030년까지 40%의 비용 하락을 예측하고 있으며, 가격의 균형화가 가시권에 들어왔다고 볼 수 있습니다.

전기 트랙터의 도입은 자동차 용도의 2-3배에 달하는 배터리 팩 비용이라는 큰 역풍에 부딪혀 환경 규제 강화에도 불구하고 시장 침투가 제한되고 있습니다. 농업용 리튬이온 팩의 가격은 kWh당 400-600달러로 소형차 수준의 약 3배에 달할 전망입니다. 전기 트랙터의 총 소유비용은 낮은 운영비용과 정부 인센티브를 감안하더라도 5년 동안 디젤 동급 기종보다 20-40% 더 높은 것으로 나타났습니다. 농업용 트랙터는 먼지가 많고 진동이 심한 환경에서 작동하고 충전 주기가 불규칙하므로 배터리의 열화가 진행됩니다. 이로 인해 연간 15-25%의 유효 용량이 감소하여 상업적 농업 경영의 경제성이 더욱 악화됩니다.

2025년 기준 40-100마력 부문은 농업용 트랙터 시장 점유율의 42.94%를 차지합니다. 이는 밭작물 재배부터 자재 운반 용도까지 다양한 농작업에서 최적의 생산량 대비 비용 비율을 실현하고 있기 때문입니다. 이 부문은 여러 농작업에 대응할 수 있는 범용성이 강점이며, 계절에 국한된 운영이 아닌 연중 활용이 가능하여 농가가 고가의 초기 투자를 정당화할 수 있다는 점이 장점입니다. 40마력 미만 카테고리는 주로 특수 작물, 포도원 작업, 신흥 시장의 소규모 농가를 대상으로 공급되며, 컴팩트한 크기와 기동성이 순수한 출력 요구 사항보다 더 많은 수요를 충족시켜 점유율을 유지하고 있습니다.

200마력 이상의 고출력 부문은 광범위한 작업기와의 호환성 향상과 에이커당 작업 시간 단축을 통한 밭 효율성 극대화를 추구하는 대규모 농업 경영으로 인해 7.49%의 연평균 복합 성장률(CAGR)을 보이고 있습니다. 101-200마력 부문은 Tier 4 Final 엔진에 영향을 미치는 공급망 제약으로 인해 역풍을 맞고 있지만, 정밀농업용 개조로 인해 가변 속도 살포 및 자율주행 시스템을 지원하는 ISOBUS 지원 모델에 대한 수요가 증가하고 있습니다.

2025년 기준 농업용 트랙터 시장 규모의 71.80%를 차지하는 것은 이륜구동(2WD) 사양입니다. 이는 낮은 구매 비용과 간단한 유지관리가 평가받은 결과입니다. 일반적인 40-100마력 2WD 트랙터는 4WD 모델보다 8,000-1만 5,000달러 저렴하며, 이는 가격에 민감한 경제권에서 중요한 가격차입니다. 보전 경작과 습윤 재배 기간의 확대로 견인력 수요가 증가함에 따라 사륜구동 수요는 연간 7.62% 성장할 것으로 예측됩니다.

4WD 시스템으로의 전환은 초기 설비 비용보다 밭의 효율성과 토양 보존을 우선시하는 농업 관행의 변화를 반영합니다. 현대의 4WD 트랙터에는 전자식 트랙션 관리 시스템이 장착되어 있으며, 슬립 감지에 따라 전륜 구동을 자동으로 작동시켜 견인 성능을 유지하면서 연료 효율을 최적화합니다. 미국과 유럽연합의 토양 보전 프로그램의 규제적 영향은 토양 밀도를 낮추고 습한 조건에서 밭의 통행성을 개선함으로써 4WD 도입을 촉진하고, 생산성 수준을 유지하면서 지속가능한 농업 관행을 지원하고 있습니다.

아시아태평양은 인도의 기계화 추진 정책, 중국의 농업 현대화 프로그램, 일본의 정밀농업 도입에 힘입어 38.60%의 점유율로 세계 농업용 트랙터 시장을 주도하고 있습니다. 인도에서는 35마력 미만 트랙터 구매시 25-50%의 보조금 제도가 지역 수요를 지원하고 있으며, 중국에서는 2024년 52%에서 2030년까지 기계화율 75% 달성을 목표로 중형 트랙터 도입이 촉진되고 있습니다. 일본은 자율 시스템 기술의 리더십을 바탕으로 로봇화 장비의 세계 진출을 위한 시험장으로서 입지를 구축하고 있습니다.

아프리카는 가장 빠르게 성장하는 지역입니다. 이 지역의 농업용 트랙터 시장은 연간 7.62% 성장할 것으로 예상되며, CAADP 2.0 계획에 따라 정부 조달과 우대 대출을 통해 기계화율 40% 달성을 목표로 하고 있습니다. 나이지리아는 2024년 8,500대의 트랙터를 수입(전년 대비 15% 증가)하고, 케냐와 가나는 총 4억 8,000만 달러의 다자간 신용 한도를 확보하여 공동 농기계 풀 자금을 확보했습니다.

북미에서는 성숙한 갱신 수요가 두드러집니다. 옥수수 벨트 지역에서는 평균 600헥타르 규모의 농장에서 광폭 작업기 및 노동 생산성 향상이 요구되므로 고마력 트랙터 구매가 주류를 이루고 있습니다. 미국이 지역 가치의 대부분을 차지하는 반면, 캐나다에서는 낙농 및 온실 재배를 위한 전기 콤팩트 유닛에 대한 투자가 진행되고 있습니다. 유럽은 이에 이어, Stage V 배출 규제에 대한 대응과 2030년까지 농업 배출량을 25% 감축하는 유럽 그린딜 목표에 따라 특수 용도 분야에서 디젤에서 전기로의 전환이 가속화되고 있습니다. 독일과 프랑스는 4WD 및 오토스티어 플랫폼을 가장 먼저 도입한 국가로, 2025년 유럽 출하량의 42%를 차지할 것으로 예측됩니다.

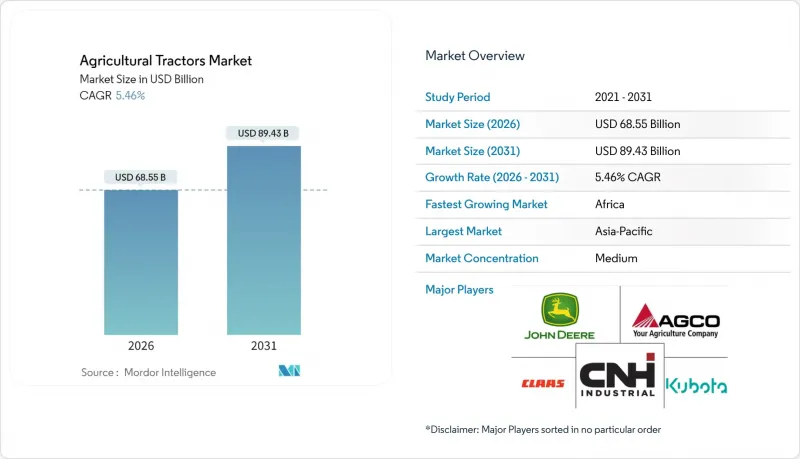

The agricultural tractors market is expected to grow from USD 65 billion in 2025 to USD 68.55 billion in 2026 and is forecast to reach USD 89.43 billion by 2031 at 5.46% CAGR over 2026-2031.

Current growth is underpinned by continuing mechanization in emerging economies, rapid precision-agriculture retrofit activity in developed regions, and early commercialization of electric and autonomous tractor platforms. Asia-Pacific sustains the strongest regional momentum, as expansive subsidy programs in India and China's farm-modernization push stimulate replacement demand, while Africa posts the fastest growth as CAADP 2.0 sets minimum mechanization targets and unlocks concessional financing. The 40-100 HP segment reflects optimal power-to-cost ratios for mid-scale farming operations, while 2-wheel drive configurations maintain dominance due to lower acquisition costs and maintenance simplicity. Utility tractors serve diverse agricultural applications from tillage to material handling. However, autonomous tractors are experiencing explosive growth as grain majors pilot driverless systems to address labor shortages and optimize field operations. Consolidation among global vendors remains moderate; yet regional brands continue to grow through focused cost-optimized product lines and locally aligned distribution. Supply chain volatility in Tier 4 F engines and rising interest rates affecting dealer floor-plan financing present near-term headwinds, yet precision agriculture retrofit demand and electrification initiatives continue driving long-term growth momentum.

India extended subsidized credit lines under the Kisan Credit Card scheme to fiscal 2029, allocating INR 1.68 trillion (USD 20.2 billion) for farm mechanization, with tractors capturing roughly 15% of disbursements . Brazil's Programa Nacional de Fortalecimento da Agricultura Familiar offers 3% interest financing, improving affordability for 40-100 HP models . As manual labor costs have risen 40-60% since 2022, tractors have become financially viable for holdings above 5 ha, accelerating agricultural tractor market adoption.

Electric tractors under 60 HP gain traction in orchards and greenhouses where zero-tailpipe emissions reduce ventilation costs and meet local regulations. Fendt's e100 Vario delivers up to six operating hours, the European Union's Green Deal provides up to 40% purchase subsidies for electric agricultural equipment, and California's Air Resources Board mandates zero-emission standards for utility vehicles by 2030, creating regulatory tailwinds for electrification initiatives. Battery packs still cost USD 400-600 per kWh, yet the International Energy Agency projects a 40% cost decline by 2030, bringing parity within reach .

Electric tractor adoption faces significant headwinds from battery pack costs that remain 2-3 times higher than automotive applications, limiting market penetration despite growing environmental regulations. Agricultural lithium-ion packs cost USD 400-600 per kWh, roughly triple light-duty automotive levels. The total cost of ownership for electric tractors exceeds diesel equivalents by 20-40% over five-year periods, even accounting for lower operating costs and government incentives. Battery degradation in agricultural applications, where tractors operate in dusty, high-vibration conditions with irregular charging cycles, reduces effective capacity by 15-25% annually, further impacting economic viability for commercial farming operations.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The 40-100 HP segment captured 42.94% of the agricultural tractors market share in 2025, reflecting optimal power-to-cost ratios for diverse farming operations from row-crop cultivation to material handling applications. This segment benefits from versatility across multiple agricultural tasks, enabling farmers to justify higher capital investments through year-round utilization rather than seasonal deployment. The sub-40 HP category maintains its share by primarily serving specialty crops, vineyard operations, and smallholder agriculture in emerging markets where compact size and maneuverability outweigh raw power requirements.

High-horsepower segments above 200 HP demonstrate 7.49% CAGR growth, driven by large-scale farming operations seeking to maximize field efficiency through wider implement compatibility and reduced operating hours per acre.The 101-200 HP segment faces headwinds from supply chain constraints affecting Tier 4 Final engines, yet precision agriculture retrofits are driving demand for ISOBUS-compatible models that support variable-rate application and autonomous guidance systems.

Two-wheel configurations delivered a 71.80% share of the agricultural tractor market size in 2025, favored for lower acquisition cost and simpler upkeep. The typical 40-100 HP 2WD tractor is USD 8,000-15,000 cheaper than its 4WD counterpart, an important gap in price-sensitive economies. Four-wheel drive demand is projected to expand 7.62% annually as conservation tillage and wetter planting windows raise traction needs.

The shift toward 4WD systems reflects changing farming practices that prioritize field efficiency and soil conservation over initial equipment costs. Modern 4WD tractors incorporate electronic traction management systems that automatically engage front-wheel assist based on slip detection, optimizing fuel efficiency while maintaining traction advantages. Regulatory influence from soil conservation programs in the United States and European Union encourages 4WD adoption through reduced soil compaction and improved field trafficability during wet conditions, supporting sustainable farming practices while maintaining productivity levels.

The Agricultural Tractors Market Report is Segmented by Power Output (less Than 40 HP, and More), by Drive Type ( 2-Wheel Drive, and 4-Wheel Drive ), by Engine Type (Diesel and More), by Tractor Type (Utility, Row-Crop and More), and by Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Report Offers Market Size and Forecasts in Terms of Value (USD).

Asia-Pacific dominates the global agricultural tractors market with a 38.60% share, driven by India's mechanization initiatives, China's agricultural modernization programs, and Japan's precision agriculture adoption. India anchors regional demand through 25-50% purchase subsidies on tractors below 35 HP, while China seeks 75% mechanization by 2030 versus 52% in 2024, spurring mid-range tractor uptake. Japan's technology leadership in autonomous systems positions the country as a testing ground for the global rollout of robotized equipment.

Africa is the fastest-growing region. The agricultural tractors market in Africa is projected to advance 7.62% annually, with government procurement and concessionary financing targeting 40% mechanization under CAADP 2.0. Nigeria imported 8,500 tractors in 2024, a 15% rise year on year, while Kenya and Ghana collectively secured USD 480 million in multilateral credit lines to fund cooperative machinery pools

North America exhibits mature replacement dynamics. High-horsepower purchases dominate in the Corn Belt as farms averaging 600 ha seek wider implements and labor productivity gains. The United States accounts for the majority share of regional value, while Canada invests in electric compact units for dairy and greenhouse operations. Europe follows, driven by Stage V emissions compliance and the European Green Deal target to cut agricultural emissions 25% by 2030, accelerating the diesel-to-electric transition in specialty applications. Germany and France remain early adopters of 4WD and autosteer platforms and jointly represent 42% of European shipments in 2025.