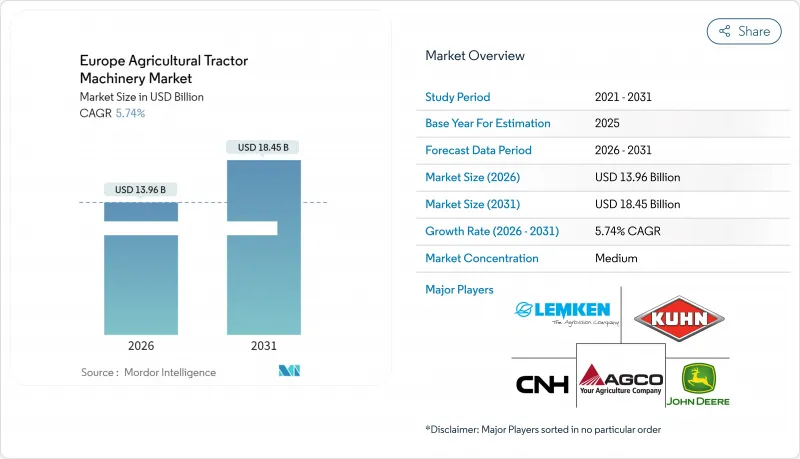

유럽의 농업용 트랙터 기계 시장은 2025년 132억 달러로 평가되었으며, 2026년 139억 6,000만 달러에서 2031년까지 184억 5,000만 달러에 이를 것으로 예상됩니다.

예측 기간(2026-2031년)의 CAGR은 5.74%를 나타낼 것으로 전망됩니다.

수요 증가의 요인으로는 정밀농업기기를 지원하는 유럽연합 공통농업정책의 에코스킴, 차량 갱신을 가속시키는 스테이지 V 배출가스 규제 대응, 농업의 자동화를 촉구하는 지속적인 노동력 부족을 들 수 있습니다. 이에 대해, 공급자는 ISO 11783(ISOBUS) 프로토콜로 통합 가능한 동력식 센서 탑재형 작업기로 대응합니다. 한편, 전동화 파일럿 사업은 배터리식 트랙터와 호환되는 저전력 소비 어태치먼트에 대한 수요를 병행하여 창출하고 있습니다. 한편, 2023년부터 판매점 재고 과잉, 변동하는 상품 가격, 혼합 플릿의 상호 운용성에 있어서 마찰이, 가격에 민감한 중동 유럽에서의 도입을 억제하고 있습니다. 톱 5 벤더가, 스트립 틸 경작, 과수원의 수하초 깎기, 온실 용도 등 틈새 분야에 대응하는 전문업자에게 여지를 남기고 있기 때문에 경쟁의 격렬함은 중간 정도에 머물고 있습니다.

의무화된 에코 방식은 직접 지불의 25%를 입증된 투입 효율화 프로젝트에 돌려주고, 가변율 플랜터, ISOBUS 대응 분무기, 수량 매핑 센서의 구입을 촉진하고 있습니다. 프랑스, 독일, 폴란드에서는 이러한 업데이트가 진행되고 있습니다. 도입 확대가 데이터 공유를 촉진, 협동조합 텔레나에서는 2024년에 회원의 38%가 텔레메트리를 실장해, 기기 수명을 15% 연장했습니다. 인증 요구사항은 ISO 11783 준수 브랜드를 뛰어넘어 주변 공급업체를 보조금 대상에서 제거하고 수요를 소수의 대규모 텔레매틱스 에코시스템에 집약하고 있습니다.

독일의 농업 상근 고용자 수는 2024년 전년 대비 12% 감소했습니다. 네덜란드의 원예 분야에서도 유사한 인력 부족이 발생하고 있으며, 로봇식 식재기나 비전 가이드식 살포기의 도입이 촉진되고 있습니다. 디어는 2024년 유럽용 'See and Spray' 시스템 출하량이 47% 증가했다고 보고했습니다. 덴마크의 아그로사는 15대의 자율형 깎기 및 컨디셔너를 도입해, 주야 가동에 의해 건초 수확의 노동 코스트를 30% 삭감했습니다. 이 때문에 유럽의 농업용 트랙터 기계 시장은 자율 기능을 탑재한 동력 작업기로 기울어져 기존의 수동적 작업기와의 차이가 확산되고 있습니다.

유럽 딜러의 작업기 재고는 2024년 초에 9.2개월분(보통 5.5개월분)에 도달했습니다. 바이에와사는 미판매의 경기·파종기 재고가 3억 4,000만 유로(3억 6,000만 달러)에 달했기 때문에 2025년 구입 계획을 22% 삭감했습니다. 프랑스 유통업체인 InVivo 역시 신규 주문을 18% 줄였고 중고자산 개보수로 축발을 옮겼습니다. 제조업체는 지불 조건을 180일로 연장해 위탁 판매도 제안했습니다만, 이익률의 압박에 의해 딜러는 추가 모델의 재고 확보를 주저하고 있어 유럽의 농업용 트랙터 기계 시장의 단기적인 성장은 둔화하고 있습니다.

경작 및 경작 기계는 유럽의 농업용 트랙터 기계 시장에서 2025년 수익의 45.30%를 차지했습니다. 정점 주행 규제와 실시간 가변률 알고리즘의 보급으로 파종기계는 2031년까지 연평균 복합 성장률(CAGR) 7.66%를 나타낼 것으로 전망됩니다. 프랑스 협동조합 액세리얼은 8만 5,000헥타르에 GPS 섹션 제어를 도입한 후 헥타르당 씨앗 비용을 12% 절감했다고 보고했습니다.

파종기계가 가장 급속한 확대를 이루고 있는 배경은 에코스킴의 지급제도가 특히 종자의 폐기절감을 장려하고 있다는 점을 들 수 있습니다. 렘켄의 전기식 미터 탑재 애슬릿 플랜터는 28% 고가이면서 500헥타르 이상의 농장에서는 3시즌 이내에 투자 회수가 가능합니다. 목초·사료용 기계는 유럽의 초원지대에서 계속 수요가 있습니다만, 안정된 젖소·육우의 사육두수에 의존하고 있습니다. 다른 특수 작업 기계는 여전히 분산 상태입니다. 이 분야는 보조금 제도와 데이터 활용 능력이 유럽의 농업용 트랙터 기계 시장 전체에서 동력식 및 소프트웨어 정의형 기계로의 이익 이동을 어떻게 촉진하는지를 보여줍니다.

The Europe agricultural tractor machinery market was valued at USD 13.2 billion in 2025 and estimated to grow from USD 13.96 billion in 2026 to reach USD 18.45 billion by 2031, at a CAGR of 5.74% during the forecast period (2026-2031).

Demand gains stem from the European Union Common Agricultural Policy eco-schemes that underwrite precision-farming hardware, Stage V emissions compliance that accelerates fleet renewal, and persistent labor shortages that nudge farms toward automation. Suppliers answer with powered, sensor-rich implements that integrate through the ISO 11783 (ISOBUS) protocol, while electrification pilots create a parallel pull for low-draw attachments compatible with battery tractors. At the same time, dealer inventory overhang from 2023, volatile commodity prices, and mixed-fleet interoperability frictions temper adoption in price-sensitive pockets of Central and Eastern Europe. Competitive intensity remains moderate because the top five vendors leave room for niche specialists that address strip-till, orchard under-vine mowing, or greenhouse applications.

Mandatory eco-schemes now channel 25% of direct payments into proven input-efficiency projects, pushing farms to buy variable-rate planters, ISOBUS sprayers, and yield-mapping sensors. France, Germany, and Poland are moving toward such upgrades. Adoption lifts data-sharing, cooperative Terrena saw 38% of members stream implement telemetry in 2024, extending equipment life by 15%. Certification requirements favor ISO 11783-compliant brands and squeeze fringe suppliers out of subsidy eligibility, consolidating demand around a few large telematics ecosystems.

Full-time farm employment in Germany fell 12% year on year in 2024. Horticulture in the Netherlands faces similar gaps, spurring take-up of robotic planters and vision-guided sprayers. Deere and Company reported a 47% jump in European shipments of its See and Spray system during 2024. Danish Agro deployed 15 autonomous mower-conditioner units that cut hay harvest labor costs by 30% while running day and night. The Europe agricultural tractor machinery market, therefore, tilts toward powered implements with embedded autonomy, widening the gap with legacy passive tools.

European dealers carried 9.2 months of implement supply at the start of 2024 versus a normal 5.5 months. BayWa posted EUR 340 million (USD 360 million) in unsold tillage and seeding stock, then cut 2025 purchase plans by 22%. French distributor InVivo similarly trimmed new orders 18% and pivoted to refurbishing used assets. Manufacturers extended payment terms to 180 days and offered consignment, but the margin squeeze still discourages dealers from stocking incremental models, slowing near-term growth in the Europe agricultural tractor machinery market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Plowing and cultivating machinery tools secured 45.30% of 2025 revenue in the Europe agricultural tractor machinery market. Planting machinery, aided by controlled-traffic mandates and real-time variable-rate algorithms, will grow at a 7.66% CAGR through 2031. French cooperative Axereal documented a 12% reduction in seed cost per hectare after rolling out GPS section control across 85,000 hectares.

Planting machinery capture the fastest expansion because eco-scheme payments specifically reward reductions in seed waste. Lemken's electric-meter Azurit planter sells at a 28% premium yet pays back within three seasons on farms above 500 hectares. Haying and forage machinery continue to serve the continent's grassland but hinge on stable dairy and beef herds. Other specialty implements remain fragmented. The segment illustrates how subsidy rules and data capability shift profits toward powered, software-defined machines within the wider Europe agricultural tractor machinery market size.

The Europe Agricultural Tractor Machinery Market Report is Segmented by Machinery Type (Plowing and Cultivating Machinery, Planting Machinery, and More) and by Geography (Germany, France, Italy, and More). Market Forecasts are Provided in Terms of Value (USD).