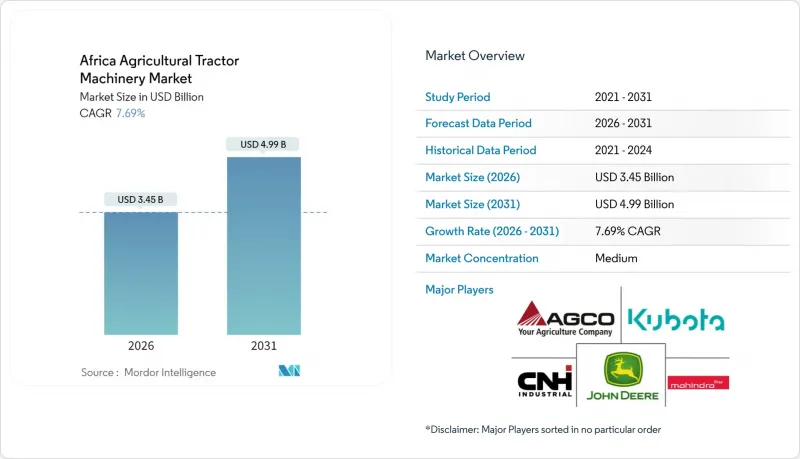

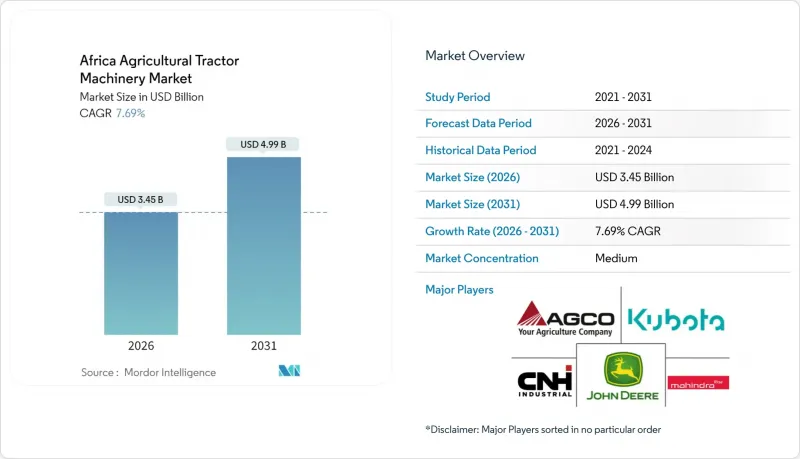

아프리카의 농업용 트랙터 기계 시장은 2025년 32억 달러에서 2026년에는 34억 5,000만 달러로 성장하고, 2026-2031년 CAGR 7.69%로 성장을 지속하여, 2031년까지 49억 9,000만 달러에 이를 것으로 예측됩니다.

이러한 확대는 대상별 보조금, 성장하는 디지털 고용 플랫폼, 다양한 아프리카 생산 시스템에서 트랙터가 필수적인 기후 적응형 농기구의 부상으로 인해 기계화 격차가 해소되고 있음을 반영합니다. 각국 정부는 현지 통화로 신용공여를 지속하는 한편, 공여국 지원 프로젝트는 연료와 투입자재를 절약할 수 있는 정밀 살포기, 파종기, GPS 지원 트랙터에 대한 새로운 수요를 창출하고 있습니다. 환율 하락, 통관 지연 등 구조적인 역풍에도 불구하고 종량제 비즈니스 모델과 저비용 완전조립제품(CKD) 조립의 결합으로 오랫동안 기계화 도입을 가로막았던 가격 장벽이 완화되기 시작했습니다. 대규모 상업용 농장의 마력 요구 사항이 동시에 증가하고 있으며, 소규모 농가를 위한 90마력 미만의 모델부터 수출 지향적인 농장을 위한 450마력 기계까지 양극화 된 제품 구성이 발생했습니다. OEM 제조업체는 현지 조립, 차량 금융 패키지, 애프터서비스 거점 정비로 대응하여 브랜드 충성도를 강화하는 동시에 대륙 전체의 가동률 향상을 도모하고 있습니다.

범아프리카적 보조금 프로그램과 우대 융자제도는 트랙터 구매 장벽을 빠르게 낮추고 아프리카의 농업용 트랙터 기계 시장 전체에 대한 수요를 자극하고 있습니다. 나이지리아의 '앵커 농부 프로그램'은 2015년 이후 4억 8천만 명의 농부들에게 1조 1,200억 나이라(1,500만 달러)를 지원하여 5억 3천만 헥타르에 달하는 농지를 경작하고 있습니다. 또한 '농업신용보증기금'은 대출의 75%를 보증하여 대출자의 리스크를 줄여주고 있습니다. 케냐도 2024/25년 예산안에서 농업 분야에 683억 케냐 실링(5억 2,000만 달러)을 배정하는 등 유사한 노력을 강화했습니다. 여기에는 농업 기업이가 운영하는 트랙터 차량과 유제품 밸류체인을 통합하는 230대의 우유 냉각기 배포가 포함됩니다. 트랙터의 평균 보급률은 여전히 헥타르당 0.27마력에 불과해 아시아의 1.5마력에 비해 기계화를 통한 성장 여지가 크다는 것을 알 수 있습니다. 명목금리가 18%에서 30%에 이르는 높은 수준으로 대출 이용이 제한적이지만, 현지 통화로 표시된 금융상품 증가와 부분 위험 보증의 도입으로 농촌 지역에서의 접근성이 개선되고 있습니다. 이러한 조치들은 아프리카의 농업용 트랙터 기계 시장 예측된 성장 궤도를 뒷받침하는 기반이 되고 있습니다.

농지 집약화로 인해 고출력 모델과 첨단 농기계에 대한 수요가 증가하고 있습니다. 이집트 사막 농업 프로젝트에서는 7,500-9,000에이커(약 3,000-3,600헥타르)의 기업 소유 토지를 운영하며, 센터 피벗 관개와 기계 수확을 도입했습니다. 이를 위해서는 GPS 유도식 120-450마력 유닛이 필요합니다. 기관 투자자들은 이미 450억 달러를 전 세계 농장 인수에 투자하고 있으며, 그 중 일부는 규모의 경제로 인해 고성능 장비의 도입이 정당화되는 아프리카의 대규모 농장을 대상으로 하고 있습니다. 무경운 재배와 피복 작물을 장려하는 새로운 탄소배출권 제도는 대규모 농장이 추가 수익원을 얻기 위해 투입물 사용량과 수확량을 정확하게 추적해야 하기 때문에 기계화를 더욱 가속화하고 있습니다. 그 결과, 아프리카의 농업용 트랙터 기계 시장에서 고급 텔레매틱스 기능을 갖춘 고급 모델에 대한 수요가 점차 증가하여 평균 판매 가격이 상승하고 있습니다. 이러한 추세는 장기적인 성격을 띠고 있으며, 사모펀드, 연기금, 국부펀드 등 투자자들의 수십 년에 걸친 토지 개발 계획을 고려할 때, 주기적인 상품 가격 변동에 영향을 받지 않는 장기적 성격을 띠고 있습니다.

조립된 트랙터의 명목 관세는 낮지만, 서류 절차 장벽, 항만 혼잡, 검사 체계의 차이로 인해 아프리카 시장에서는 실제 착륙 비용이 청구 가격보다 최대 25% 더 높은 것으로 나타났습니다. 나이지리아는 CKD 화물의 통관 주기가 60-90일에 달하고, 현지 조립업체의 운전자금을 동결시키고 있습니다. 케냐의 몸바사항도 비슷한 체선 사태에 직면해 있으며, 체선료가 총비용을 증가시키고 있습니다. 아프리카 대륙자유무역협정(AfCFTA)은 무역 프로세스의 조화를 약속하고 있지만, 이행 상황은 여전히 불균등하고 통관 서류의 디지털화도 초기 단계에 있습니다. 통관 시간이 정상화 될 때까지 제조업체는 현금 전환 주기가 길어지고 재고 계획에 부담을 주며 아프리카의 농업용 트랙터 기계 시장에 새로 진입하는 것을 막고 있습니다.

2025년 기준, 경작 및 경운 카테고리는 아프리카의 농업용 트랙터 기계 시장에서 30.68%의 매출 점유율을 차지했습니다. 이는 세분화된 농지를 경작할 수 있도록 준비하는 로터리 경운기, 경운기, 써레 등 수요에 힘입은 것입니다. 잠비아에서는 헥타르당 19-28달러, 짐바브웨에서는 51-69달러에 제공되는 계약 기계화 서비스는 경작 작업에 대한 지속적인 수요를 뒷받침하고 있습니다. 그러나 말라위와 잠비아의 일부 지역에서는 경작의 최대 57%가 여전히 동물 견인에 의해 이루어지고 있어 트랙터 기반 시스템으로의 완전한 전환이 완료되지 않았음을 보여주고 있습니다. 보전농업 프로그램은 무경운 재배를 장려하고 있지만, 전용 파종기가 비싸고 잡초 관리에 대한 추가 지식이 필요하기 때문에 보급이 제한적입니다. 예측 기간 동안 이 부문은 정밀 농기구에 상대적인 점유율을 내어줄 가능성이 있지만, 식량 생산량 증가를 배경으로 절대적인 물량은 계속 성장할 것으로 예측됩니다.

분무기는 가장 빠르게 성장하는 제품군으로 2031년까지 연평균 복합 성장률(CAGR) 9.67%로 확대되어 아프리카의 농업용 트랙터 기계 시장을 재편하고 있습니다. 중동 및 아프리카에서는 2024년 95만 대의 분무기가 등록되었으며, 나이지리아와 남아프리카공화국이 34만 대를 차지했습니다. 트랙터 탑재형은 현재 전 세계 수요의 34-38%를 차지하고 있으며, 수동식 백팩형을 대체하여 작업 시간을 단축하고 살포의 균일성을 향상시키고 있습니다. 태양광 발전식 분무기는 오프 그리드 농장에서 무공해 운전을 실현할 수 있지만, 배터리 비용과 충전 인프라 부족으로 인해 주류화가 늦어지고 있습니다. 정밀화학, 가변율 노즐, IoT 센서도 도입이 진행되어 기후 스마트 농업을 요구하는 지원기관의 요청에 부응하고 있습니다. 아프리카 농가의 51%가 여전히 분무기를 공유하거나 임대하고 있는 상황에서 임대 풀과 디지털 예약 플랫폼은 앞으로도 보급을 촉진하는 데 중요한 역할을 할 것입니다.

The Africa agricultural tractor machinery market is expected to grow from USD 3.20 billion in 2025 to USD 3.45 billion in 2026 and is forecast to reach USD 4.99 billion by 2031 at 7.69% CAGR over 2026-2031.

This expansion reflects widening mechanization gaps being closed through targeted subsidies, growing digital hiring platforms, and the rise of climate-smart implements that make tractors indispensable across a variety of African production systems. Governments continue to anchor credit lines in local currencies, while donor-backed projects create new demand for precision sprayers, planters, and GPS-enabled tractors capable of conserving fuel and inputs. Despite structural headwinds such as currency depreciation and customs delays, pay-per-use business models combined with lower-cost CKD (Completely Knocked Down) assembly have begun easing the affordability barrier that long constrained mechanization adoption. Large-scale commercial farms are simultaneously pushing horsepower requirements higher, creating a bifurcated product mix that ranges from sub-90 horsepower units for smallholders to 450 horsepower machines for export-oriented estates. Original equipment manufacturers are responding with localized assembly, fleet-financing packages, and after-sales service hubs that tighten brand loyalty while improving uptime across the continent.

Pan-African subsidy programs and concessional credit lines have rapidly lowered purchase barriers for tractor ownership, stimulating demand across the Africa agricultural tractor machinery market. Nigeria's Anchor Borrowers' Programme disbursed ₦1.12 trillion (USD 1.5 billion) to 4.8 million farmers cultivating 5.3 million hectares since 2015, while the Agricultural Credit Guarantee Scheme Fund covers 75% of loan defaults, mitigating lender risk. Kenya reinforced a similar approach in its 2024/25 budget, allocating KES 68.3 billion (USD 520 million) for agriculture, including tractor fleets operated by agripreneurs and the distribution of 230 milk coolers that integrate dairy value chains. Average tractor density remains just 0.27 horsepower per hectare versus 1.5 horsepower per hectare in Asia, underscoring the scope for mechanization gains. Although high nominal interest rates between 18% and 30% limit credit uptake, the growing presence of local-currency instruments and partial-risk guarantees is easing access in rural areas. These programs thereby underpin the projected growth trajectory of the Africa agricultural tractor machinery market.

Consolidation of farmland is shifting demand toward larger horsepower models and sophisticated implements. Egypt's desert agriculture projects operate corporate holdings of 7,500 to 9,000 acres, using center-pivot irrigation and machine harvesting that call for GPS-guided 120-450 horsepower units. Institutional capital has already deployed USD 45 billion into global farm acquisitions, a portion of which targets African estates where scale efficiencies justify premium equipment. Emerging carbon-credit programs that reward no-till and cover crops further accelerate mechanization, because large farms must track input use and yields precisely to earn additional revenue streams. As a result, the Africa agricultural tractor machinery market is witnessing a gradual tilt toward high-end models with advanced telematics, boosting average selling prices. The trend is long-term in nature and resilient to cyclical commodity swings, given the multi-decade land-development horizons of private equity, pension funds, and sovereign wealth investors.

Despite low nominal tariffs on assembled tractors, documentation hurdles, port congestion, and varied inspection regimes keep effective landed costs up to 25% above invoice prices in several African markets. Nigeria's clearance cycle stretches 60-90 days for CKD consignments, immobilizing working capital for local assemblers. Kenya's Mombasa port faces similar backlogs, with demurrage charges increasing total costs. While AfCFTA promises to harmonize trade processes, implementation remains uneven, and the digitization of customs paperwork is still in early stages. Until clearance times normalize, manufacturers face elongated cash conversion cycles that weigh on inventory planning and deter new entrants in the Africa agricultural tractor machinery market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The plowing and cultivating category held a 30.68% revenue share of the Africa agricultural tractor machinery market in 2025, driven by rotovators, cultivators, and harrows that prepare fragmented plots for planting. Contract mechanization services priced between USD 19-28 per hectare in Zambia and USD 51-69 per hectare in Zimbabwe underline the persistent need for tillage operations. Nonetheless, animal draft power still covers up to 57% of tillage in parts of Malawi and Zambia, indicating that full transition to tractor-based systems is incomplete. Conservation agriculture programs promote no-till practices, but uptake remains limited because specialized planters are expensive and weed management requires additional knowledge. Over the forecast horizon, the segment is likely to cede relative share to precision implements, yet absolute volumes will still grow on the back of rising food output.

Sprayers form the fastest-growing product line, advancing at a 9.67% CAGR through 2031 and reshaping the Africa agricultural tractor machinery market. The Middle East and Africa region registered 0.95 million sprayer units in 2024, with Nigeria and South Africa jointly accounting for 0.34 million. Tractor-mounted configurations now capture 34-38% of global demand, replacing manual knapsack units and cutting labor hours while improving coverage uniformity. Solar-powered sprayers offer emissions-free operation for off-grid farms, although battery costs and charging gaps postpone mainstream adoption. Precision chemistry, variable-rate nozzles, and IoT sensors are also entering the field, aligning with donor mandates for climate-smart agriculture. Given that 51% of African farmers still share or rent sprayers, leasing pools and digital booking platforms will remain pivotal in unlocking further penetration.

The Africa Agricultural Tractor Machinery Market Report is Segmented by Product Type ( Plowing and Cultivating Machinery, Planting Machinery, Sprayers, Haying and Forage Machinery, and Other Types) and by Geography (Nigeria, South Africa, Kenya, and Rest of Africa). The Report Offers the Market Size and Forecasts in Terms of Value (USD).