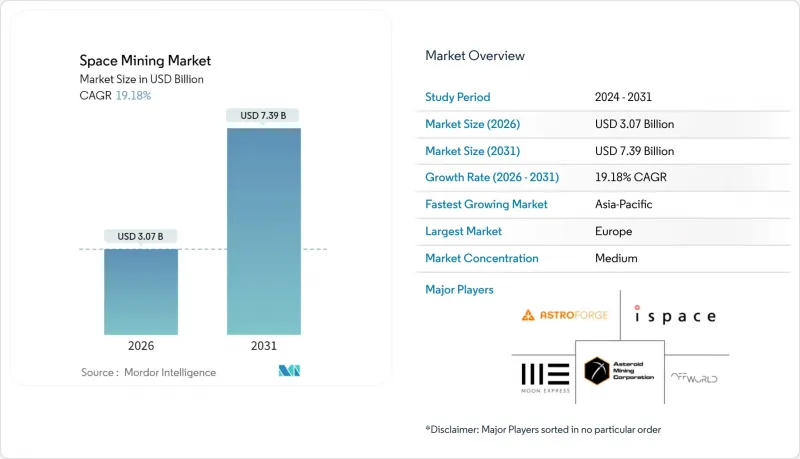

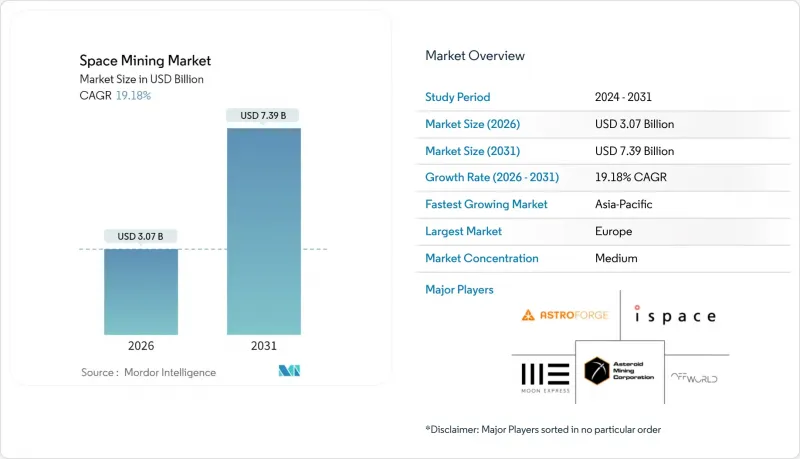

우주 채굴 시장은 2025년에 25억 8,000만 달러로 평가되었고 2026년 30억 7,000만 달러에서 2031년까지 73억 9,000만 달러에 이를 것으로 예측됩니다. 예측 기간(2026-2031년) CAGR은 19.18%로 전망됩니다.

재사용 가능한 로켓을 통한 발사 비용의 급격한 감소, 지구상의 주요 광물 부족 심화, 행성 외 자원을 전략적 자산으로 간주하는 수십억 달러 규모의 정부 프로그램이 견조한 성장을 견인하고 있습니다. 순수 탐사 임무에서 초기 단계의 채굴 시험으로의 꾸준한 전환은 상업화의 길을 넓혀가고 있습니다. 동시에 현지 자원 이용(ISRU) 기술의 향상으로 자본 집약형 프로젝트의 투자 회수 기간이 단축됩니다. 아르테미스 협정에 근거한 정책의 명확성과 각국 규제의 일관성은 투자자의 불확실성을 더욱 감소시키고, 민간 부문의 다음 단계의 참여를 지원할 것입니다.

재사용 가능한 대형 발사체 덕분에 2020년 이후 궤도 진입의 평균 비용이 60% 이상 감소했습니다. 주요 시스템의 경우, 고빈도 발사 시나리오에서 Kg당 약 100달러의 비용 목표를 설정하고 있습니다. 이러한 경제성으로 인해 고부가가치 소행성 채굴 임무, 특히 백금족 금속의 회수는 이론적 모델에서 신뢰할 수 있는 비즈니스 사례로 전환할 수 있게 되었습니다. 이러한 저비용화로 인해 기존에는 승차공유에 의존하던 중소사업자들이 진입하여 경쟁의 격화와 가격 하락을 촉진하고 있습니다. 각국 우주기관은 고정가격 계약을 민간 사업자에게 이관함으로써 공적 자금을 달 인프라 및 ISRU 실증 실험에 투입할 수 있는 이점을 얻고 있습니다. 이러한 수요의 선순환이 우주 채굴 시장의 성장 궤도를 더욱 강화시키고 있습니다.

연료전지 자동차, 전해장치, 고용량 배터리에는 대체 불가능한 금속이 다량으로 필요합니다. 백금족 금속공급 부족은 2028년까지 연간 50만 온스를 넘어설 것으로 예상되며, 지구 기후 목표 달성을 위해 2050년까지 희토류 수요는 4배로 증가할 수 있습니다. 지표면 생산은 지리적으로 집중되어 있고, 지정학적 긴장의 영향을 받기 쉽기 때문에 제조업체는 가격 변동과 공급 중단의 위험에 노출되어 있습니다. 우주 금속 광상은 지표 시장의 압박을 완화하고 청정 기술 제조업체의 투입 비용을 안정화시킬 수 있는 다각화 경로를 제공합니다. 초기 단계의 행성 외 조달 활동은 지표면 생태계에 대한 부하를 줄임으로써 기업의 지속가능성 목표에 부합하는 활동입니다.

복잡한 열적, 기계적, 로봇 공학적인 문제로 인해 미션 예산은 수억 달러 규모로 증가하며, 자원의 가공 및 운송이 완료될 때까지 현금 흐름이 지연될 수 있습니다. 연마성 레고리스 환경과 저중력 소행성대에서의 미지의 공학적 과제는 성공과 실패의 양자택일적 결과를 낳고 자본 비용을 증가시킵니다. 심우주 자산의 보험료는 여전히 높은 수준이며, 전통적인 프로젝트 파이낸싱 구조에서는 수익이 발생하지 않는 다년간의 기간에 대응하는 경우가 드뭅니다. 따라서 투자자들은 하이브리드형 투자 및 보조금 모델과 정부의 마일스톤 지급(전체 수익률을 희석시키는)을 요구하며 우주 채굴 시장의 확장 속도를 억제하고 있습니다.

우주 채굴 시장의 용도별 규모에서 3D 프린팅은 42.12%를 차지하고 있습니다. 이러한 장점은 궤도상 제조의 즉각적인 가치에서 비롯되며, 지구에서 부피가 큰 예비 부품을 우주로 발사할 필요성을 줄여줍니다. 구조물 수리 및 도구 제작에 현지 자원을 활용하면 물류 비용이 절감되고 임무 수행 속도가 빨라집니다. 건설 분야는 연평균 25.85%의 성장률로 가장 빠르게 성장하고 있습니다. 현지에서 채굴한 금속 프레임워크로 보강된 팽창식 거주시설이라는 새로운 개념은 달 기지 건설에 있어 비용 효율적인 방법을 입증하며 이러한 추진력을 뒷받침하고 있습니다. 생명 유지 시스템은 세 번째 기둥을 형성하고, 안정적으로 채굴된 휘발성 물질에 의존하는 물 재활용 장치와 산소 발생 장치에 대한 전문적인 관심이 집중되고 있습니다. 연료 보급 서비스는 꾸준히 발전하고 있으며, 극저온 저장 시설을 활용하여 자원 기지와 운송 회랑 간의 폐쇄 루프 거래를 구축하는 극저온 저장 시설을 활용하고 있습니다. 이러한 요소들이 결합되어 우주 채굴 시장이 지속 가능한 외계 경제의 물질적 기반을 제공한다는 핵심 전제를 강화합니다.

앞으로의 성장은 적층 가공 툴체인과 자율 드릴링 플랫폼의 통합에 달려 있습니다. 머신러닝(ML) 알고리즘은 미세중력 하에서 소결 정밀도를 향상시키고, 금속-고분자 복합 기술은 사용 가능한 원료의 범위를 확대합니다. 국제우주정거장(ISS)에서의 실증 실험을 통해 조형 품질이 검증되어 저궤도(LEO)를 넘어선 유인 임무에 채택이 가속화되고 있습니다. 규제 당국은 부품 인증 기준을 법제화하기 시작했고, 사업자는 내하중 용도의 인쇄 부품 도입에 대한 확신을 가질 수 있게 되었습니다. 인프라가 확대됨에 따라 우주 채굴 시장의 용도 구성은 압력 용기, 방사선 차폐 패널 등 고적층 가공로 전환되어 정제된 금속 및 세라믹 전구체 수요를 더욱 촉진할 것으로 예측됩니다.

물과 휘발성 화합물은 2025년 매출의 47.55%를 차지할 것입니다. 그 우수성은 음용액, 방사선 차폐재, 수소-산소 추진제의 전해질 원료로서 보편적인 유용성을 반영하고 있습니다. 영구적으로 그늘진 달의 분화구에는 호핑 착륙선으로 도달할 수 있는 얼음 자원이 존재하며, 복잡한 금속 제련 시설이 가동되기 전에 초기 현금 흐름을 제공합니다. 청정 에너지 공급의 압력에 힘입어 희토류 원소와 백금족 금속은 23.52%의 연평균 복합 성장률(CAGR)로 가장 큰 성장을 보일 것으로 예측됩니다. 샘플 반환 임무를 통해 M형 소행성에서 팔라듐, 이리듐, 네오디뮴의 존재를 확인하여 소행성 자원 모델을 입증했습니다. 알루미늄과 티타늄과 같은 구조용 금속은 매출 총이익률이 떨어지지만, 특히 용융 레고리스 전해가 파일럿 플랜트 단계에 도달하면서 필수적인 건설 수요를 충족시킬 수 있습니다.

기술의 성숙으로 궤도상의 분석 결과가 지구상의 JORC 및 NI-43-101 기준에 준하는 매장량 분류로 꾸준히 전환되고 있습니다. 분광분석과 중성자 감마선 로거의 조합으로 실시간 품위관리가 가능하여 탐사 리스크를 줄일 수 있습니다. 동시에 개선된 고진공로는 태양열 집광기만을 사용하여 금속 회수율이 85%에 육박하여 에너지 수입을 줄였습니다. 이 기술의 수렴은 비용 곡선을 축소하고 다양한 자원 포트폴리오를 지원함으로써 우주 채굴 시장이 단일 상품 사이클에 과도하게 의존하지 않도록 보장합니다.

북미는 전 세계 매출의 36.12%를 차지하며 1위 자리를 지켰습니다. 연방정부의 달 추진제 조달과 민간 착륙선에 대한 수출 신용 지원은 이러한 우위를 뒷받침하고 있습니다. '상업용 우주발사 경쟁력법'에 따라 채굴 자원은 사유재산으로 인정되어 기업이들에게 법적 확실성을 부여하고 있습니다. 주력인 아르테미스 계획은 추진제 및 건설용 원료의 주요 수요처로 작용하는 한편, 탄탄한 벤처캐피털 생태계가 레고리스 이송 장비에서 진공 야금 장비에 이르는 하드웨어 스핀오프 기업을 재정적으로 뒷받침하고 있습니다.

아시아태평양은 2031년까지 23.62%의 가장 빠른 지역 CAGR을 달성할 것으로 예측됩니다. 중국의 부처 간 프로그램에서는 대학이 주도하는 기술 클러스터와 탐사, 채굴, 시료 분석을 종합적으로 다루는 국가 계약이 연계되어 있습니다. 2025년 3월에 발사된 다기능 소행성-달 채굴 로봇은 미세중력 환경에 적합한 국산 앵커 메커니즘의 실용성을 입증했습니다. 일본의 64억 달러 규모의 우주전략기금은 ISRU 로봇 기술에 대한 보조금을 투입하고 있으며, 인도의 찬드라얀 계획의 다음 단계는 저비용 발사의 이점을 활용하여 탐사 페이로드의 동반 상승을 실현할 것입니다.

유럽은 국경을 초월한 조달을 효율화시키는 ESA의 통합적인 규제 환경의 혜택을 누리고 있습니다. 문라이트 이니셔티브는 민간 채굴업자들에게 표준화된 항법 및 통신 서비스를 제공하는 안전한 위성 네트워크를 구상하고 있습니다. NASA가 주도하는 게이트웨이에 협력적으로 참여함으로써 유럽 기업들은 건축자재 공급에 있어 우선적인 접근권을 얻게 될 것입니다. 중동 및 라틴아메리카 국가들은 헬륨3 및 전략 금속 공급을 확보하기 위해 국부펀드 투자 및 양자 파트너십을 모색하고 있으며, 이는 10년 말까지 우주 채굴 시장의 지리적 분산이 더욱 심화될 것임을 시사하고 있습니다.

The space mining market was valued at USD 2.58 billion in 2025 and estimated to grow from USD 3.07 billion in 2026 to reach USD 7.39 billion by 2031, at a CAGR of 19.18% during the forecast period (2026-2031).

Robust growth is encouraged by sharply falling launch costs enabled by reusable rockets, rising shortages of critical minerals on Earth, and multibillion-dollar government programs that treat off-planet resources as strategic assets. A steady shift from pure research missions to early-stage extraction trials widens the commercial funnel. At the same time, improved in-situ resource utilization (ISRU) technologies shorten payback horizons for capital-intensive projects. Policy clarity under the Artemis Accords and compatible national regulations further reduces investor uncertainty, supporting the next wave of private-sector participation.

Reusable heavy-lift vehicles have reduced average orbital launch prices by more than 60% since 2020, with leading systems targeting costs of around USD 100 per kilogram for high-flight-rate scenarios. These economics enable high-value asteroid mining missions to transition from theoretical models to credible business cases, particularly for the retrieval of platinum group metals. The lower threshold attracts smaller operators that previously relied on ride-shares, spurring competition and additional price declines. National space agencies benefit by shifting fixed-price contracts to commercial providers, redirecting public funds toward lunar infrastructure and ISRU demonstrations. The resulting demand flywheel reinforces the growth trajectory of the space mining market.

Fuel-cell vehicles, electrolyzers, and high-capacity batteries require substantial volumes of irreplaceable metals. Forecast supply gaps for platinum group metals exceed 500,000 oz annually through 2028, while rare-earth requirements may quadruple by 2050 to meet global climate goals. Terrestrial production remains geographically concentrated and vulnerable to geopolitical tensions, exposing manufacturers to price fluctuations and supply disruptions. Celestial metal deposits offer a diversification path that could relieve tightness in terrestrial markets and stabilize input costs for clean-tech manufacturers. Early-stage off-planet sourcing aligns with corporate sustainability mandates by lowering land-based ecological footprints.

Complex thermal, mechanical, and robotic challenges raise mission budgets into the hundreds of millions of dollars, with cash flows delayed until resources are processed and transported. Engineering unknowns in abrasive regolith environments or low-gravity asteroid fields create binary success-failure outcomes, increasing the cost of capital. Insurance premiums for deep-space assets remain elevated, and conventional project finance structures seldom accommodate multi-year, non-revenue-generating periods. Investors, therefore, demand hybrid equity-grant models or government milestone payments that dilute overall returns, tempering the pace at which the space mining market can scale.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

3D printing corresponds to 42.12% of the space mining market size for applications. This dominance stems from the immediate value of on-orbit manufacturing, which reduces the need to loft bulky spare parts from Earth. Utilizing local feedstock for structural repair and tool fabrication reduces logistics costs and facilitates rapid mission turnaround. Construction applications have the fastest-growing outlook, with a 25.85% CAGR. Emerging concepts for inflatable habitats reinforced with in-situ metal frameworks underpin this momentum by demonstrating a cost-effective approach to the rollout of a lunar base. Human-life-support systems form a third pillar, drawing specialized attention to water recycling and oxygen generation units that depend on reliably mined volatiles. Fuel-refueling services are showing steady progress, leveraging cryogenic depots that establish a closed-loop trade between resource nodes and transportation corridors. Collectively, these threads reinforce the core premise that the space mining market supplies the material backbone of sustainable off-planet economies.

Follow-on growth hinges on integrating additive manufacturing tool chains and autonomous excavation platforms. Machine learning (ML) algorithms enhance sintering accuracy in microgravity, while metal-polymer composite techniques expand the range of usable feedstocks. Demonstrations aboard the International Space Station (ISS) validate print quality, accelerating acceptance in crewed missions beyond low-Earth orbit (LEO). Regulatory agencies have begun codifying part-qualification standards, giving operators confidence to deploy printed components in load-bearing roles. As infrastructure scales, the application mix within the space mining market will likely shift toward higher-end fabrication, such as pressure vessels and radiation-shielding panels, further boosting demand for refined metals and ceramic precursors.

Water and volatile compounds hold 47.55% of the 2025 revenue. Their primacy reflects universal utility as a drinkable fluid, a radiation shield, and an electrolysis feedstock for hydrogen-oxygen propellant. Permanently shadowed lunar craters host ice reserves reachable by hopping landers, offering early cash flow before complex metal refineries come online. Rare-earth elements and platinum group metals are expected to hold the highest upside, with a 23.52% CAGR, driven by clean-energy supply pressures. Sample-return missions have confirmed the presence of palladium, iridium, and neodymium in M-type asteroids, thereby validating resource models for these asteroids. Structural metals such as aluminum and titanium trail in gross margins but fill essential construction demand, especially as molten-regolith electrolysis achieves pilot-plant status.

Technology maturation is steadily translating orbital assays into reserve classifications akin to terrestrial JORC or NI-43-101 standards. Spectroscopy, combined with neutron-gamma loggers, provides real-time grade control, reducing exploration risk. Simultaneously, improved high-vacuum furnaces now approach 85% metal recovery factors using only solar power concentrators, reducing energy imports. This convergence tightens the cost curve and supports a diversified resource slate, ensuring that the space mining market is not overly reliant on a single commodity cycle.

The Space Mining Market Report is Segmented by Application (Extraterrestrial Commodity, Construction, and More), Resource Type (Water and Volatiles, and More), Extraction Target Body (Near-Earth Asteroids, and More), Mission Phase (Spacecraft Design and Engineering, Launch Services, and More), and Geography (North America, Europe, Asia-Pacific and More). The Market Forecasts are Provided in Terms of Value (USD).

North America retained its top position, accounting for 36.12% of global revenue. Federal procurement of lunar propellant and export-credit support for private landers underpins this lead. The Commercial Space Launch Competitiveness Act ensures that mined resources are recognized as private property, giving entrepreneurs legal certainty. Flagship Artemis missions serve as anchor tenants for propellant and construction feedstock, while a deep venture-capital ecosystem funds hardware spin-offs ranging from regolith conveyors to vacuum metallurgy units.

Asia-Pacific is projected to deliver the fastest regional CAGR of 23.62% through 2031. China's interagency program pairs university-led technology clusters with comprehensive state contracts that cover prospecting, excavation, and sample analysis. The launch of a multifunctional asteroid- and lunar-mining robot in March 2025 validated indigenous anchoring mechanisms suitable for microgravity. Japan's USD 6.4 billion Space Strategy Fund channels subsidies into ISRU robotics, while India's next phase of Chandrayaan leverages its low-cost launch niche to piggyback prospecting payloads.

Europe benefits from ESA's cohesive regulatory environment, which streamlines cross-border procurement. The Moonlight initiative envisions a secure satellite network offering private miners standardized navigation and communication services. Cooperative participation in the NASA-led Gateway will grant European firms preferential access to delivering construction materials. Countries in the Middle East and Latin America are exploring sovereign wealth investments and bilateral partnerships to secure the supply of helium-3 and strategic metals, suggesting broader geographical diversification for the space mining market by the end of the decade.