우주 채굴 및 로봇 시장(2025-2030년) : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측

Space Mining & Robots - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1693947

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

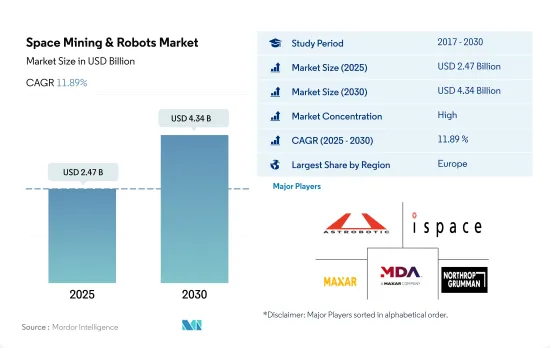

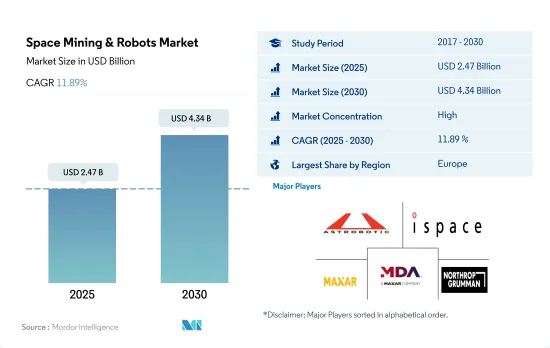

우주 채굴 및 로봇 시장 규모는 2025년에 24억 7,000만 달러로 추정되고, 2030년에는 43억 4,000만 달러에 이를 전망이며 예측 기간(2025-2030년) 동안 CAGR 11.89%로 성장할 것으로 예측됩니다.

우주 자원 채굴 범위의 확대가 시장의 성장을 뒷받침할 전망

세계의 우주 채굴 및 로봇 시장은 소행성, 달, 기타 천체로부터의 자원 추출에 응용할 수 있는 가능성을 지닌 신흥 부문입니다. 과거에는 다양한 기업들이 우주 채굴을 탐구하기 위해 신기술을 연구하였으며 현재도 개발을 계속하고 있습니다.

희귀 금속과 물 등의 귀중한 자원과 우주 탐사의 가능성을 배경으로 우주 채굴 및 로봇 시장에 대한 관심과 투자가 높아지고 있습니다. 여러 비공개 회사와 우주 기관이 우주 채굴 및 로봇을 위한 기술과 시스템 개발에 투자하고 있습니다. 2029년에는 유럽이 32.4%의 점유율을 차지하고 다음으로 북미가 27.5%, 기타 지역이 21.1%, 아시아태평양이 19%로 이어질 것으로 예측됩니다.

우주 채굴 및 로봇 시장은 급속히 진보하고 있는 로봇 공학과 자동화 기술에 크게 의존하고 있습니다. 2022년 NASA의 Dual Asteroid Redirection Test(DART) 임무는 '키네틱 임팩트' 기술을 사용하여 지구를 보호하기 위해 소행성을 편향시키는 방법을 테스트하기 위해 설계되었습니다. 이 야심찬 미션은 소행성이 지구로 향했을 경우에 NASA의 과학자가 실시할 조치를 시뮬레이션한 것입니다. 전체적으로, 세계의 위성 채굴과 우주 로봇 시장은 성장 단계에 있으며 2023-2029년 사이에 183%의 성장이 전망되고 있습니다.

세계의 우주 채굴 및 로봇 시장 동향

나노 위성과 미니 위성이 시장 수요를 창출할 전망

우주선의 질량별 분류는 위성을 궤도에 발사하기 위한 로켓의 크기와 비용을 결정하기 위한 주요 지표 중 하나입니다. 북미에서는 2017-2022년 45기 이상의 대형 위성이 발사되었으며 80기 이상의 중형 위성을 북미의 조직이 소유하고 있었습니다.

유럽은 주로 다른 질량의 위성에 대한 수요 증가로 인해 최근 현저한 성장을 이루고 있습니다. 위성 질량은 유럽의 위성 제조 시장에 영향을 미치는 가장 중요한 요소 중 하나입니다. 2017-2022년 사이에 이 지역에서는 합계 571기의 위성이 발사되었습니다.

최근 아시아태평양에서는 첨단 위성 기능에 대한 수요가 증가함에 따라 위성 제조가 점점 더 중요한 산업이 되고 있습니다. 이 지역에서는 총 470기의 위성이 발사되었습니다. 470기의 위성 중 중형 위성이 점유율의 대부분을 차지하였으며 152개의 위성이 궤도에 발사되었고 이어 132개의 초소형 위성, 78개의 대형 위성, 66개의 초소형 위성 순으로 발사되었습니다.

다양한 유형의 인공위성 개발과 다양한 용도로의 이용이 증가하고 있는 점이 세계의 우주 개발 지출을 견인하고 있습니다.

세계 우주 개발에 대한 정부 지출은 2021년에 약 1,030억 달러를 기록했습니다. 세계 최대의 우주 기관인 NASA가 존재하고, 우주 혁신과 연구의 진원지인 북미에는 세계 최대의 우주 로봇 회사인 GITAI가 있습니다. GITAI는 미국에서의 사업 기술 개발을 가속 확대하기 위해, 총액 40억엔(약 3,000만 달러)의 시리즈 B 익스텐션 라운드에 의한 자금 조달을 완료했습니다.

유럽 국가들은 또한 우주 부문에서의 다양한 투자의 중요성을 인식하고 있습니다. 2021년 6월, 7개국의 유럽 기업 22사로 구성된 컨소시엄이 유럽우주국(ESA)에 로봇을 납품했습니다.

아시아태평양에서 증가하는 우주 관련 활동 중 2022년 일본의 예산안에 따르면 일본의 우주 예산은 14억 달러를 돌파하였으며 여기에는 H3 로켓, 기술 검사 위성 9호, 국가 정보 수집 위성(IGS) 계획의 개발이 포함됩니다. 인도의 2022년도 우주 개발 예산안은 18억 3,000만 달러였습니다.

우주 채굴 및 로봇 산업 개요

우주 채굴 및 로봇 시장은 상당히 통합되어 있으며 상위 5개 기업에서 69.52%를 차지하고 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

위성의 질량

우주 개발에의 지출

규제 프레임워크

세계

호주

브라질

캐나다

중국

프랑스

독일

인도

이란

일본

뉴질랜드

러시아

싱가포르

한국

아랍에미리트(UAE)

영국

미국

밸류체인과 유통채널 분석

제5장 시장 세분화

지역

아시아태평양

유럽

북미

기타

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

Asteroid Mining Corporation

Astrobotic

GITAI Inc.

Honeybee Robotics

iSpace Inc.

Maxar Technologies Inc.

MDA Ltd

Moon Express

Motiv Space Systems

Northrop Grumman Corporation

Offworld

Space Applications Services

Trans Astronautiaca Corporation

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Porter's Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

CSM

영문 목차

영문목차

The Space Mining & Robots Market size is estimated at 2.47 billion USD in 2025, and is expected to reach 4.34 billion USD by 2030, growing at a CAGR of 11.89% during the forecast period (2025-2030).

Increased scope for extraction of resources from space is expected to aid the market's growth

The global space mining and robots market is an emerging field with potential applications in extracting resources from asteroids, the moon, and other celestial bodies. During the historic period, various companies have explored new technologies and are still developing them to explore space mining.

There is growing interest and investment in the space mining and robots market, driven by the potential for valuable resources such as rare metals and water, as well as the exploration of space. Several private companies and space agencies are investing in developing technologies and systems for space mining and robots. Europe is expected to occupy a major share of 32.4% in 2029, followed by North America, Rest of the World, and Asia-Pacific with 27.5%, 21.1%, and 19%, respectively.

The space mining and robots market relies heavily on robotics and automation technologies, which are rapidly advancing. These advancements include the development of autonomous robots, machine learning algorithms, and advanced sensors, which enable robots to operate in harsh space environments and perform complex tasks. In 2022, NASA's DART (Dual Asteroid Redirection Test) mission was designed to test a method of deflecting an asteroid to protect the planet using a "kinetic impact" technique. According to NASA, DART crashed into a small asteroid, Dimorphos, in an attempt to change the asteroid's orbital speed by 1%. Although Dimorphos poses no threat to Earth, the ambitious mission mimics what NASA scientists would do if an asteroid were headed for Earth. Overall, the global satellite mining and space robots market is in the growth stage and is expected to grow by 183% during 2023-2029.

Global Space Mining & Robots Market Trends

Nano and mini-satellites are poised to create demand in the market

The classification of spacecraft by mass is one of the main metrics for determining the launch vehicle size and cost of launching satellites into orbit. In North America, during 2017-2022, around 45+ large satellites launched were owned by North American organizations. North American organizations operated more than 80 medium-sized satellites launched, and around 2,900+ small satellites were manufactured and launched in this region.

Europe has witnessed significant growth over recent years, primarily driven by the increasing demand for different satellite masses. Satellite mass is one of the most critical factors influencing the European satellite manufacturing market. This is because different types of satellites require different masses, which, in turn, affects the launch vehicle market. For instance, during 2017-2022, a total of 571 satellites were launched in the region. Of these 571 satellites, minisatellites accounted for most of the shares, with 452 satellites launched into orbit, followed by 45 nanosatellites, 37 large satellites, 30 medium size satellites, and seven microsatellites.

Satellite manufacturing has become an increasingly important industry in the Asia-Pacific region over recent years, driven by the need to meet the growing demand for advanced satellite capabilities. The range of satellite mass being manufactured in the Asia-Pacific region varies significantly, and this has a significant impact on the market's growth. For instance, during 2017-2022, a total of 470 satellites were launched in the region. Of these 470 satellites, medium satellites accounted for most of the shares, with 152 satellites launched into orbit, followed by 132 microsatellites, 78 large satellites, 66 nanosatellites, and 42 minisatellites.

Rising developments across all types of satellites and increased usage for several applications is driving the spending on space programs across the world

Global government expenditure for space programs hit a record of approximately USD 103 billion in 2021. In the North American region, which is the epicenter of space innovation and research, with the presence of the world's biggest space agency, NASA. GITAI, the world's leading space robotics company, completed a Series B Extension round of funding totaling JPY 4 billion (approximately USD 30 million) to accelerate and expand its business and technology development in the United States.

European countries are also recognizing the importance of various investments in the space domain. They are increasing their spending on space activities and innovation to stay competitive and innovative in the global space industry. The European Space Agency (ESA) is requesting its 22 nations to back a budget of EUR 18.5 billion during 2023-2025. Germany, France, and Italy are the major contributors. In June 2021, a consortium of 22 European companies from seven countries built a robot for ESA. The launch and installation of the European Robotic Arm was a first for Europe and Russia in space. This was the long-awaited premiere of this European-made robot that followed 14 years of perseverance.

Considering the increase in space-related activities in the Asia-Pacific region, in 2022, according to the draft budget of Japan, the space budget of the country was over USD 1.4 billion, which included the development of the H3 rocket, Engineering Test Satellite-9, and the nation's Information Gathering Satellite (IGS) program. Similarly, the proposed budget for India's space programs for FY22 was USD 1.83 billion. In 2022, South Korea's Ministry of Science and ICT announced a space budget of USD 619 million for manufacturing satellites, rockets, and other key space equipment.

Space Mining & Robots Industry Overview

The Space Mining & Robots Market is fairly consolidated, with the top five companies occupying 69.52%. The major players in this market are Astrobotic, iSpace Inc., Maxar Technologies Inc., MDA Ltd and Northrop Grumman Corporation (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Satellite Mass

4.2 Spending On Space Programs

4.3 Regulatory Framework

4.3.1 Global

4.3.2 Australia

4.3.3 Brazil

4.3.4 Canada

4.3.5 China

4.3.6 France

4.3.7 Germany

4.3.8 India

4.3.9 Iran

4.3.10 Japan

4.3.11 New Zealand

4.3.12 Russia

4.3.13 Singapore

4.3.14 South Korea

4.3.15 United Arab Emirates

4.3.16 United Kingdom

4.3.17 United States

4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

5.1 Region

5.1.1 Asia-Pacific

5.1.2 Europe

5.1.3 North America

5.1.4 Rest of World

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).