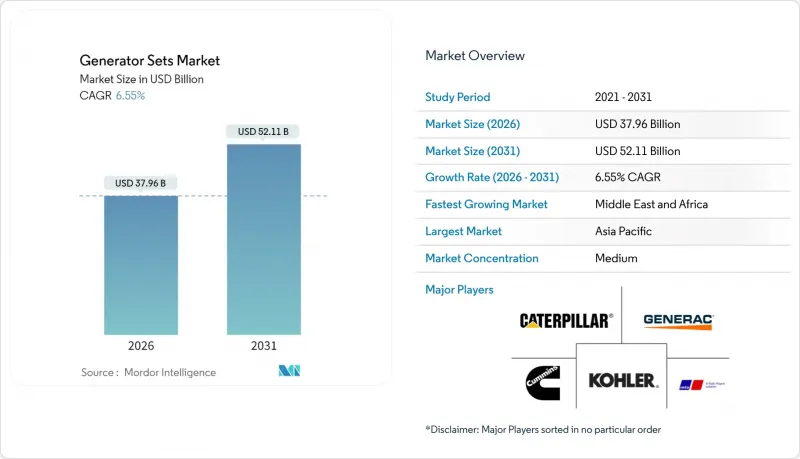

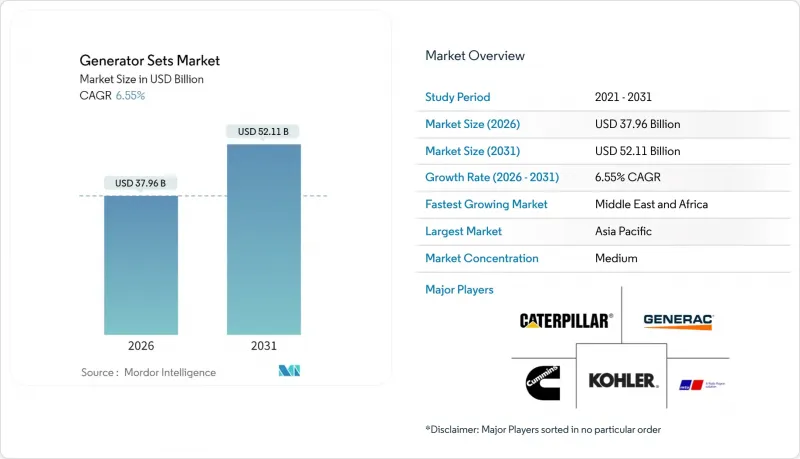

발전기 시장은 2025년에 356억 3,000만 달러로 평가되었고, 2026년 379억 6,000만 달러에서 2031년까지 521억 1,000만 달러에 이를 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 6.55%로 예상됩니다.

최근 성장세는 데이터센터 건설, 산업 전기화, 신흥 경제국의 지속적인 전력망 불안정성 등에 기인합니다. 발전기 시장은 변동이 심한 기상 조건과 불안정한 전력망 하에서 가동 시간이 연장됨에 따라 서비스 수익이 증가하고 강력한 애프터마켓의 혜택을 누리고 있습니다. 기업들이 탈탄소화 목표에 부합하는 백업 전략을 수립하는 가운데, 이중 연료, 수소 지원, 디지털 연결 모델이 추가 지출을 이끌어내고 있습니다. 한편, 공급업체들은 저kVA 범위를 위협하는 배터리 전용 솔루션에 대한 점유율 방어를 위해 대형 엔진 생산, 첨단 발전기, 원격 분석 기술에 대한 투자를 진행하고 있습니다.

개발도상국의 잦은 정전으로 인해 기업들은 발전기를 주요 설비 및 예비 설비로 취급할 수밖에 없습니다. 나이지리아의 최대 발전량은 2024년 6,003MW에 달했지만, 지속적인 공급 부족으로 인해 대부분의 중규모 공장은 75-375kVA의 디젤 발전기를 매일 몇 시간씩 계속 가동해야만 했습니다. 동남아시아, 라틴아메리카, 사하라 사막 이남 아프리카의 일부 지역에서도 비슷한 불안정성이 만연해 있으며, 계획되지 않은 가동 중단으로 인한 생산 손실이 연료비 및 유지보수 비용보다 더 큰 것으로 나타났습니다. 신뢰성 향상에 대한 수요는 발전기 시장을 디젤에 단단히 묶고 있으며, 서비스 네트워크, 부품 조달 가능성, 운전자 숙련도는 여전히 이 연료 등급에서 가장 우수합니다. 동시에 전력 품질에 대한 우려로 인해 기업들은 디지털 모니터링 및 예지보전 모듈을 통합하여 설치된 설비군의 가동률을 향상시키고 있습니다.

하이퍼스케일 플랫폼, 코로케이션 제공업체, 국가 주도 클라우드 프로그램은 100% 가동률의 인프라에 적극적으로 투자하고 있습니다. ABB에 따르면, 전력 계통의 한 자릿수 단위의 정전조차도 불안정한 AI 워크로드를 위협할 수 있기 때문에 백업 발전이 설계상 필수 요건으로 자리 잡았다고 합니다. 엔지니어링, 조달 및 건설 기업은 원활한 병렬 운전과 빠른 출력 상승이 가능한 2000kVA 이상의 멀티 블록 설계로 대응하고 있습니다. 펜실베니아의 4.5GW 천연가스 프로젝트는 미래지향적인 데이터센터 및 하이퍼스 사이트에 특화된 출력 규모를 설계했습니다. 제너럴 일렉트릭과 같은 업체들은 2025년 초에 이러한 캠퍼스를 위해 수소 전용 발전기를 도입했습니다. 이러한 추세는 조달 주기를 가속화하고, 고용량 유닛에 대한 수요를 증가시키며, 지속가능성 스코어카드를 충족하기 위한 배출가스 후처리 기술에 대한 새로운 투자를 촉진하고 있습니다.

미국 내 디젤 연료의 평균 도매가격은 2024년 3.30-4.05달러/갤런을 기록한 후 2025년에는 3.61달러/갤런을 기록할 것으로 예측됩니다. 산업용 핵심 전원 공급 장치 사용자는 수명주기 비용의 최대 70%를 연료비로 인식하고 있으며, 가격과 공급의 불안정성은 운영 비용(OPEX)에 직접적인 압력을 가하고 있습니다. 외딴 지역의 광산과 섬 지역의 전력망은 운송 장애와 정유소 가동 중단으로 인해 몇 주 동안 공급 부족이 발생할 수 있기 때문에 가장 큰 영향을 받기 쉽습니다. 이 때문에 최종 사용자는 가스 파이프라인, LPG 교체 또는 1시간 방전 시간에 대응하는 고정형 배터리 팩의 도입 가능성 조사에 박차를 가하고 있습니다. 디젤은 물류 측면에서 우위를 유지하고 있지만, 조달 패턴은 선물 연료 계약이나 변동성 위험을 헤지하는 이중 연료 변환 키트를 번들링할 수 있는 공급업체를 점점 더 선호하는 경향이 있습니다.

75-375kVA 발전기 시장 규모는 2025년 139억 3,000만 달러로 세계 매출의 39.10%를 차지했습니다. 상업용 사무실, 중소기업, 엣지 데이터 시설에서는 출력과 비용 대비 성능의 균형 때문에 이 범위가 중요하게 여겨지고 있습니다. 중국과 브라질은 이미 설치된 설비가 성숙기에 접어들면서 성장은 지속되나 둔화되는 추세입니다.

375-750kVA 유닛은 고밀도 공조설비 및 IoT 제어부하를 도입하는 중규모 공장 및 고성능 빌딩 수요 증가로 2031년까지 연평균 복합 성장률(CAGR) 8.95%의 가파른 성장이 예상됩니다. 제조업체는 도시 대기질 규제에 대응하기 위해 스마트 병렬 운전 키트 및 Tier 4F 적합 기술로 대응. 대형 발전기는 엘리베이터 그룹 및 반도체 제조 장비에 적합한 과도 응답 특성을 제공합니다. 더 큰 750-2000kVA 대역 및 2000kVA 이상의 모델은 하이퍼스케일 데이터센터, LNG 액화 플랜트, 전력 피크 조정용 섬 발전용으로 제공됩니다. 캐터필러의 7억 2,500만 달러 규모의 인디애나 공장 증설은 대형 엔진 생산 능력을 강화하고 발전기 시장의 프리미엄 분야를 공략하기 위한 것입니다.

디젤은 에너지 밀도, 물류, 서비스 네트워크에서 여전히 독보적인 우위를 가지고 있기 때문에 2025년 세계 매출의 70.85%를 차지할 것으로 예측됩니다. 규제 면제가 적용되는 지방의 광산이나 건설 현장에서는 Tier 2 또는 Tier 3 엔진이 계속 지정되고 있습니다.

그러나 듀얼 연료 및 하이브리드 시스템은 신뢰성을 훼손하지 않고 ESG 목표를 추구하는 기업들에 의해 기준치인 5.29%를 크게 상회하는 10.2%의 연평균 복합 성장률(CAGR)을 기록하고 있습니다. 천연가스 발전기는 안정적인 파이프라인 요금을 활용하고, 수소 혼합 키트는 캠퍼스의 넷제로 공약 실현에 기여합니다. 미쓰비시, DEUTZ, 제네라크는 수소 대응 로드맵을 발표하며 발전기 시장의 연료 구성 변화가 불가피함을 시사하고 있습니다. 바이오디젤과 재생가능 합성연료는 '기타'로 분류되지만, 유럽의 ReFuelEU 프레임워크에서 정책적 지원을 받고 있습니다.

발전기 시장 보고서는 용량별(75KVA 미만, 75-375KVA, 375-750KVA, 750KVA 이상), 연료별(디젤, 천연가스, 이중연료/하이브리드, 기타), 용도별(비상전원, 주전원/연속전원, 마이크로그리드 및 하이브리드 지원), 최종사용자별(주택, 산업, 데이터센터 등), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카) 등), 최종사용자(주거, 산업/제조, 데이터센터 등), 지역(북미, 아시아태평양, 중동/아프리카 등)별로 분석되었습니다.

아시아태평양은 2025년 전 세계 매출의 36.65%를 차지했습니다. 중국 연안성에서는 공장 업그레이드가 가속화되고 있으며, 인도의 생산 연동형 인센티브 제도에 따라 72시간의 내결함성을 보장하기 위해 250kVA 디젤 유닛 2대를 표준으로 장착한 클러스터가 형성되고 있습니다. 아세안 국가들의 건설 붐으로 임대 차량에 대한 수요가 증가하고 있으며, 한국과 일본에서는 병원 캠퍼스에서 수소 혼합 연료의 시범 운영이 진행되고 있습니다.

중동 및 아프리카은 9.35%의 가장 빠른 CAGR을 달성했습니다. GCC 국가들의 알루미늄 산업, 데이터파크, 그린수소로의 다각화가 비상용 및 상설 발전설비 도입을 견인. 이 지역의 전력 수요는 2020년부터 2030년까지 29-37% 급증할 것으로 예측됩니다. 나이지리아의 전력 부문 수익은 2024년 70% 증가, 공급 부족으로 공장들은 자가 발전 설비에 계속 의존하고 있음.

북미에서는 안정적인 갱신 주기와 더불어 버지니아와 텍사스 주 데이터센터 회랑에서 최고 성장세를 보일 것으로 예측됩니다. 유럽의 Stage V 규제 환경은 가스-수소 혼합 연료에 초점을 맞추고 있으며, 남미에서는 광산용 트럭, 항만 확장, 가뭄으로 인한 수력 발전 부족으로 디젤 전력 렌탈 수요가 증가하고 있습니다. 이를 통해 발전기 시장은 지역적으로 균형 잡힌 포트폴리오를 형성하여 경기순환 리스크를 완화하고 있습니다.

The Generator Sets Market was valued at USD 35.63 billion in 2025 and estimated to grow from USD 37.96 billion in 2026 to reach USD 52.11 billion by 2031, at a CAGR of 6.55% during the forecast period (2026-2031).

Recent momentum stems from data-center construction, industrial electrification, and persistent grid instability in emerging economies. The generator sets market benefits from a strong aftermarket because fleets run longer hours under volatile weather and volatile grids, raising service revenue. Dual-fuel, hydrogen-ready, and digitally connected models are capturing incremental spend as enterprises align backup strategies with decarbonization targets. Meanwhile, suppliers invest in large-engine production, advanced alternators, and remote analytics to defend share against battery-only solutions that threaten the lower-kVA range.

Frequent outages in developing regions continue to compel businesses to treat generator sets as primary and standby assets. Nigeria's peak generation touched 6,003 MW in 2024, yet persistent supply gaps required most mid-size factories to keep 75-375 kVA diesels running for several hours each day. Similar instability pervades parts of Southeast Asia, Latin America, and Sub-Saharan Africa, where manufacturing losses during unplanned downtime outweigh fuel and maintenance outlays. The reliability driver keeps the generator sets market firmly anchored in diesel because service networks, parts availability, and operator familiarity remain strongest for that fuel class. At the same time, power-quality worries are prompting enterprises to embed digital monitoring and predictive-maintenance modules to squeeze higher uptime from installed fleets.

Hyperscale platforms, colocation providers, and sovereign-cloud programs are spending aggressively on 100% uptime infrastructure. ABB notes that even single-digit-minute utility-grid outages jeopardize turbulent AI workloads, cementing backup generation as a design imperative. Engineering, Procurement & Construction firms have responded with multi-block, above-2000 kVA designs that can parallel seamlessly and ramp quickly. Pennsylvania's 4.5 GW natural-gas project specifically sized its output around future-proof data-center hypersites. Vendors such as Generac introduced purpose-built, hydrogen-capable gensets for these campuses in early 2025. The trend accelerates procurement cycles, lifting high-capacity unit volume and spurring fresh investment in emissions-aftertreatment to satisfy sustainability scorecards.

Average wholesale diesel in the United States is forecast at USD 3.61 per gallon in 2025 after swinging between USD 3.30 and USD 4.05 during 2024. Industrial prime-power users attribute up to 70% of lifecycle cost to fuel, so unreliability in price and delivery exerts direct pressure on OPEX. Remote mines and island grids are most exposed because shipping disruptions or refinery outages create multi-week shortages. End users are therefore accelerating feasibility studies on gas pipelines, LPG swaps, or stationary battery packs sized for one-hour discharge windows. While diesel retains logistical advantages, procurement patterns increasingly favor suppliers able to bundle forward-fuel contracts or dual-fuel conversion kits that hedge volatility.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The generator sets market size for 75-375 kVA reached USD 13.93 billion in 2025, equal to 39.10% of global revenue. Commercial offices, SMEs, and edge-data facilities prize this range for its balance of power and affordability. Growth continues but moderates as installed fleets mature in China and Brazil.

A sharper 8.95% CAGR through 2031 is predicted for 375-750 kVA units, driven by medium-scale factories and high-performance buildings adopting dense HVAC and IoT control loads. Manufacturers respond with smart paralleling kits and Tier 4F compliance to satisfy urban air-quality ordinances. Enlarged alternators offer transient response suitable for elevator banks and semiconductor tools. Larger bands-750-2000 kVA and above-2000 kVA-serve hyperscale data centers, LNG liquefaction, and utility peak-shaving islands. Caterpillar's USD 725 million Indiana expansion boosts large-engine throughput to capture that premium slice of the generator sets market.

Diesel commanded 70.85% of global revenue in 2025 because its energy density, logistics, and service footprint remain unmatched. Rural mining and construction sites continue to specify Tier 2 or Tier 3 engines where regulatory waivers exist.

Yet dual-fuel and hybrid systems log a 10.2% CAGR, far above the 5.29% base-line, as enterprises chase ESG targets without sacrificing reliability. Natural-gas sets exploit stable pipeline tariffs, while hydrogen-blend kits position campuses for net-zero pledges. Mitsubishi, DEUTZ, and Generac have public hydrogen-ready roadmaps, signaling an inevitable mix shift inside the generator sets market. Bio-diesel and renewable synthetic fuels appear under the "Others" banner but gain policy support in Europe's ReFuelEU framework.

The Generator Sets Market Report is Segmented by Capacity (Below 75 KVA, 75 To 375 KVA, 375 To 750 KVA, and More), Fuel Type (Diesel, Natural Gas, Dual-Fuel and Hybrid, and More), Application (Standby Power, Prime/Continuous Power, Micro-Grid and Hybrid Support, and More), End-User (Residential, Industrial and Manufacturing, Data Centers, and More), and Geography (North America, Asia-Pacific, Middle East and Africa, and More).

Asia-Pacific commanded 36.65% of global revenue in 2025. Chinese coastal provinces accelerate factory upgrades, and India's Production-Linked Incentives spawn clusters that standardize on twin 250 kVA diesel units for 72-hour resilience. ASEAN construction booms add rental fleet demand, while Korea and Japan test hydrogen blends in hospital campuses.

The Middle East and Africa deliver the fastest 9.35% CAGR. GCC diversification toward aluminum, data parks, and green hydrogen drives standby and prime installations. Regional electricity demand could jump 29-37% between 2020 and 2030. Nigerian power-sector revenue rose 70% in 2024, yet supply gaps keep factories on captive sets.

North America yields steady replacement cycles plus peak growth in data-center corridors of Virginia and Texas. Europe's Stage V landscape shifts focus to gas and H2 blends, while South America benefits from mining trucks, port expansion, and drought-driven hydro shortfalls triggering diesel rentals. The generator sets market therefore shows a balanced geographic portfolio, cushioning cyclical risk.